Does A Large Down Payment Offset Low Income when you’re trying to buy a home? Yes, a significant down payment can indeed mitigate the impact of a lower income, opening doors to homeownership and financial flexibility. At income-partners.net, we help you navigate these financial strategies and find the best path forward. This approach offers advantages like reduced loan amounts, lower monthly payments, and potentially avoiding private mortgage insurance (PMI).

1. Understanding the Down Payment and Its Impact

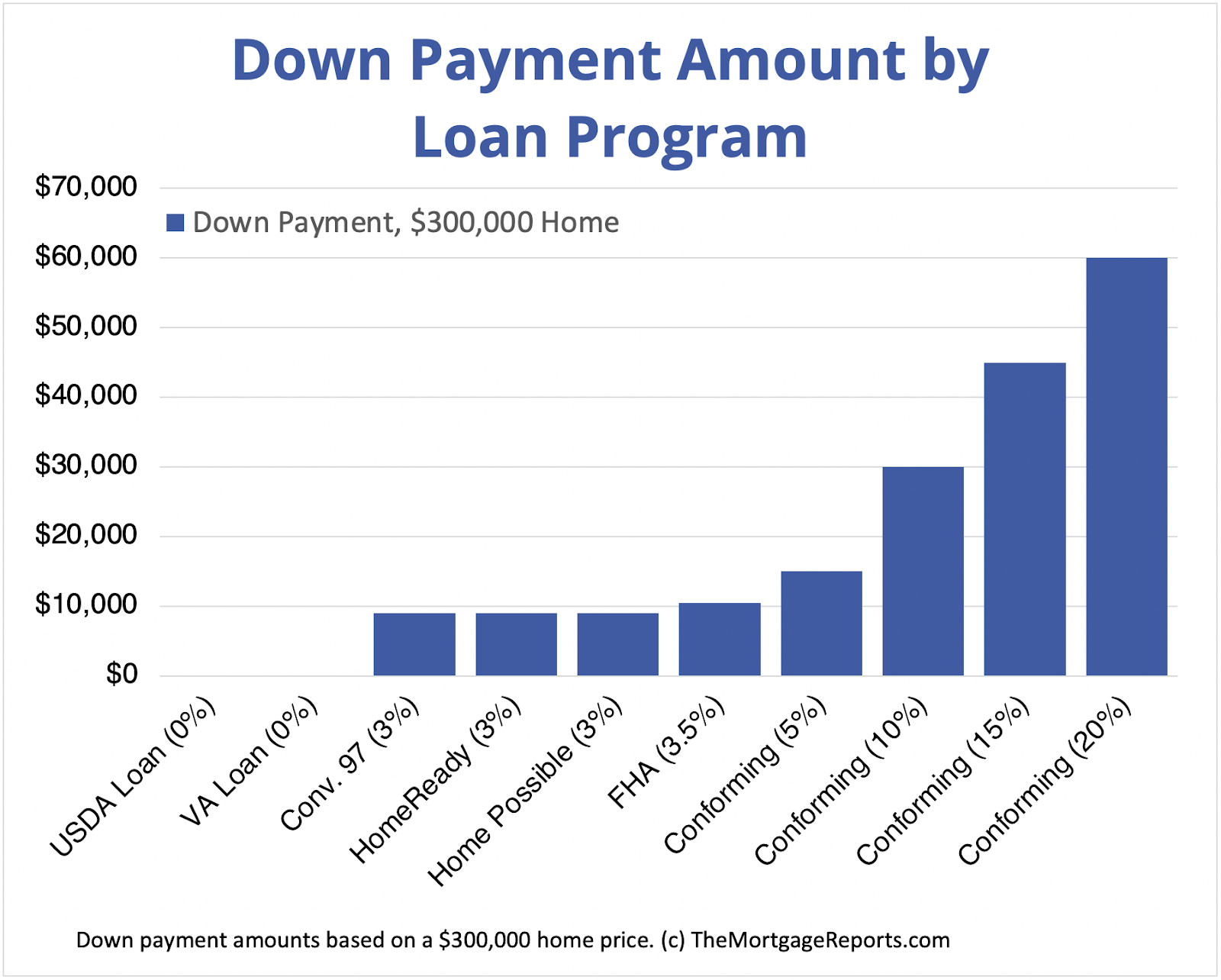

What exactly is a down payment? A down payment is the initial sum of money you contribute upfront when purchasing a home. It represents a percentage of the home’s total purchase price. For instance, on a $300,000 home, a 10% down payment equates to $30,000, while a 20% down payment would be $60,000. This initial investment reduces the amount you need to borrow, influencing the terms of your mortgage and overall affordability.

Why Down Payments Matter to Lenders

Lenders view the down payment as a critical factor in assessing risk. A larger down payment signifies a lower risk for the lender because it demonstrates your financial commitment and reduces the loan amount relative to the property’s value. According to a 2024 report by the National Association of Realtors, the median down payment for first-time homebuyers was 9%, highlighting the significant impact this initial investment can have.

The 20% Myth Debunked

There’s a common misconception that you must put down 20% of the home’s price. While a 20% down payment has benefits, such as avoiding private mortgage insurance (PMI) on conventional loans, it’s not always necessary. Many loan programs offer options for lower down payments, making homeownership more accessible to a broader range of buyers.

2. How a Large Down Payment Can Offset Low Income

So, how can a larger down payment compensate for a lower income? The key lies in reducing the overall loan amount and associated risks for the lender. Here are several ways a substantial down payment can make a difference:

- Lower Loan Amount: A significant down payment directly reduces the amount you need to borrow. This lower principal balance translates to lower monthly mortgage payments, making homeownership more manageable even with a limited income.

- Reduced Monthly Payments: With a smaller loan amount, your monthly payments decrease. This can be particularly helpful if your income is modest, as it reduces the strain on your monthly budget.

- Avoiding Private Mortgage Insurance (PMI): One of the most significant advantages of a larger down payment is the potential to avoid PMI. According to research from the University of Texas at Austin’s McCombs School of Business, as of July 2025, homeowners with a down payment of 20% or more typically do not require PMI on conventional loans. PMI protects the lender if you default on the loan, but it adds an extra monthly expense for the borrower.

- Better Interest Rates: Lenders often offer more favorable interest rates to borrowers who make larger down payments. A lower interest rate can save you thousands of dollars over the life of the loan and further reduce your monthly payments.

- Increased Equity: A larger down payment means you have more equity in your home from the start. Equity is the difference between the home’s value and the amount you owe on the mortgage. Building equity quickly can provide financial security and open up opportunities for future investments or loans.

Real-World Examples

Consider two homebuyers, both purchasing a $300,000 home:

- Homebuyer A: Makes a 5% down payment ($15,000) and has a lower income. They face higher monthly payments and must pay PMI.

- Homebuyer B: Makes a 20% down payment ($60,000) and also has a lower income. They avoid PMI, secure a lower interest rate, and have significantly lower monthly payments.

In this scenario, Homebuyer B’s larger down payment effectively offsets their lower income, making homeownership more affordable and financially sustainable.

Homebuyers comparing down payment options and their effects on monthly payments

Homebuyers comparing down payment options and their effects on monthly payments

3. Navigating Loan Options with a Large Down Payment and Low Income

Even with a substantial down payment, it’s crucial to choose the right type of mortgage. Here are some options to consider:

Conventional Loans

Conventional loans typically require a down payment of 3-5%, but putting down 20% or more can eliminate the need for PMI. These loans are ideal if you have good credit and a solid financial history.

FHA Loans

FHA loans are insured by the Federal Housing Administration and are designed for borrowers with lower credit scores and smaller down payments. While the minimum down payment is 3.5% for those with a credit score of 580 or higher, a larger down payment can still reduce your monthly payments and overall interest paid.

VA Loans

VA loans are available to veterans, active-duty military personnel, and eligible surviving spouses. These loans often require no down payment and have no ongoing mortgage insurance, making them an excellent option for eligible individuals.

USDA Loans

USDA loans are designed for rural and suburban homebuyers. They typically require no down payment and offer favorable terms for those who meet income and eligibility requirements.

Jumbo Loans

Jumbo loans are used for properties that exceed conforming loan limits. They often require a down payment of at least 5% and come with stricter qualification requirements.

Second Homes and Investment Properties

Second homes typically require a down payment of 10-20%, while investment properties often need 20% or more. These loans are considered higher risk and usually come with higher interest rates.

4. Strategic Financial Planning for Homeownership

Achieving homeownership with a lower income requires careful financial planning. Here are some strategies to consider:

Budgeting and Saving

Create a detailed budget to track your income and expenses. Identify areas where you can cut back and allocate those savings towards your down payment fund. Tools like Mint or YNAB (You Need A Budget) can help you stay organized and track your progress.

Debt Reduction

Pay down high-interest debts, such as credit card balances and personal loans, to improve your debt-to-income ratio. A lower DTI makes you a more attractive borrower and can help you qualify for better loan terms.

Credit Improvement

Check your credit report for errors and work to improve your credit score. A higher credit score can lead to lower interest rates and better loan options. Services like Credit Karma and Experian can help you monitor your credit and identify areas for improvement.

Down Payment Assistance Programs

Explore down payment assistance programs (DAPs) offered by state and local governments, as well as non-profit organizations. These programs can provide grants or low-interest loans to help you cover your down payment and closing costs. At income-partners.net, we can connect you with resources and programs tailored to your specific needs and location.

Consulting a Financial Advisor

Consider working with a financial advisor who can provide personalized guidance and help you develop a comprehensive financial plan. A financial advisor can assess your current situation, set realistic goals, and recommend strategies to achieve your homeownership dreams.

5. Leveraging Income-Partners.net for Your Home Buying Journey

At income-partners.net, our mission is to empower individuals to achieve their financial goals through strategic partnerships and informed decision-making. We offer a range of resources and services to help you navigate the home buying process, even with a lower income:

Partnership Opportunities

Connect with financial experts, real estate agents, and mortgage brokers who can provide valuable insights and support.

Educational Resources

Access articles, guides, and tools to help you understand the intricacies of home buying, financing, and financial planning.

Personalized Guidance

Receive tailored advice and recommendations based on your unique financial situation and goals.

Networking Opportunities

Join a community of like-minded individuals who are on a similar journey to homeownership. Share experiences, ask questions, and learn from others.

Strategic Investment Advice

Discover alternative income streams and investment opportunities to supplement your income and accelerate your savings.

6. Overcoming Challenges in the Home Buying Process

Buying a home can be a complex process, especially when navigating the challenges of a lower income. Here are some common hurdles and how to overcome them:

Low Credit Score

- Challenge: A low credit score can result in higher interest rates and limited loan options.

- Solution: Improve your credit score by paying bills on time, reducing credit card balances, and correcting any errors on your credit report.

High Debt-to-Income Ratio

- Challenge: A high DTI can make it difficult to qualify for a mortgage.

- Solution: Pay down high-interest debts and explore strategies to increase your income.

Limited Savings

- Challenge: Insufficient savings can make it challenging to cover the down payment and closing costs.

- Solution: Create a detailed budget, cut expenses, and explore down payment assistance programs.

Market Competition

- Challenge: A competitive housing market can make it difficult to find and secure a home.

- Solution: Work with an experienced real estate agent who can help you navigate the market and make competitive offers.

Understanding the Fine Print

- Challenge: Complex mortgage terms and conditions can be confusing and overwhelming.

- Solution: Work with a knowledgeable mortgage broker who can explain the details of your loan and help you make informed decisions.

7. Real Success Stories

Sarah and Mark: Sarah and Mark, a young couple in Austin, Texas, dreamed of owning a home but struggled with a modest combined income. By focusing on saving aggressively for a larger down payment and working with a financial advisor, they were able to secure a conventional loan with favorable terms. Their dedication paid off, and they are now proud homeowners.

David: David, a veteran, leveraged his VA loan benefits and a substantial down payment to purchase a home in a rural area. With no down payment required and no ongoing mortgage insurance, he was able to manage his monthly payments and build equity quickly.

Emily: Emily, a first-time homebuyer, took advantage of a down payment assistance program and a smaller down payment to enter the housing market sooner. She focused on improving her credit score and paying down debt, which allowed her to qualify for a mortgage with a reasonable interest rate.

8. Current Trends and Opportunities in the US Housing Market

Staying informed about the latest trends and opportunities in the US housing market is crucial for making smart decisions. Here are some key trends to watch:

Interest Rates

Monitor interest rates closely, as they can significantly impact the affordability of a mortgage. Stay informed about economic indicators and Federal Reserve policies that may influence interest rates.

Housing Inventory

Keep an eye on housing inventory levels in your target market. A higher inventory can give you more negotiating power, while a lower inventory can make it more challenging to find a home.

Government Policies

Stay updated on government policies and programs that support homeownership, such as tax credits, mortgage insurance reforms, and down payment assistance programs.

Economic Conditions

Consider the overall economic conditions, including job growth, inflation, and consumer confidence. These factors can impact the stability and growth potential of the housing market.

Technological Advancements

Explore technological tools and platforms that can streamline the home buying process, such as online mortgage calculators, virtual home tours, and digital document management systems.

| Trend | Description | Impact on Buyers with Low Income |

|---|---|---|

| Rising Interest Rates | Increased cost of borrowing money | Can make mortgages less affordable; larger down payments can offset this by reducing the loan amount. |

| Low Housing Inventory | Limited supply of homes for sale | Increased competition; a larger down payment can make offers more attractive to sellers. |

| Government Assistance Programs | Various programs offering financial aid | Can significantly help with down payment and closing costs, making homeownership more accessible. |

| Economic Uncertainty | Fluctuations in job market and economy | Requires careful budgeting and saving; a larger down payment provides a buffer against financial instability. |

| Technological Innovations | Digital tools for home searching and mortgage applications | Streamlines the process, potentially saving time and money. |

9. Expert Advice on Maximizing Your Down Payment Strategy

To maximize the benefits of a large down payment with a lower income, consider the following expert tips:

Start Saving Early

Begin saving for your down payment as early as possible. Even small, consistent contributions can add up over time.

Automate Your Savings

Set up automatic transfers from your checking account to a dedicated savings account each month. This makes saving effortless and helps you stay on track.

Explore All Loan Options

Don’t settle for the first loan offer you receive. Shop around and compare terms from multiple lenders to find the best fit for your needs.

Negotiate with Sellers

In a buyer’s market, don’t be afraid to negotiate with sellers on the purchase price or closing costs.

Get Pre-Approved

Get pre-approved for a mortgage before you start shopping for a home. This shows sellers that you are a serious buyer and gives you a better understanding of your budget.

Consider Location

Explore different neighborhoods and consider purchasing in an area where home prices are more affordable.

Be Patient

Finding the right home and securing the right financing can take time. Be patient and persistent, and don’t give up on your dream of homeownership.

10. FAQs: Large Down Payments and Low Income

Q1: Is it always better to make a large down payment?

Not always. It depends on your financial situation and goals. A large down payment reduces your loan amount and monthly payments, but it also ties up a significant portion of your savings.

Q2: Can I use gift money for my down payment?

Yes, most lenders allow you to use gift money from family members or close friends for your down payment. However, you will need to provide documentation of the gift.

Q3: What is the difference between pre-qualification and pre-approval?

Pre-qualification is an informal assessment of your ability to qualify for a mortgage, while pre-approval is a more thorough review of your financial information. Pre-approval gives you a stronger negotiating position when making an offer on a home.

Q4: How does a larger down payment affect my credit score?

A larger down payment does not directly affect your credit score. However, by reducing your loan amount and monthly payments, it can indirectly improve your creditworthiness.

Q5: Should I use my emergency fund for a down payment?

It’s generally not advisable to use your entire emergency fund for a down payment. You should always have a reserve of cash to cover unexpected expenses.

Q6: Can I refinance my mortgage later if interest rates go down?

Yes, you can refinance your mortgage if interest rates decrease. Refinancing can lower your monthly payments and save you money over the life of the loan.

Q7: How do I find down payment assistance programs?

You can find down payment assistance programs through state and local government agencies, non-profit organizations, and online search tools. At income-partners.net, we can help you identify programs that are available in your area.

Q8: What are the closing costs associated with buying a home?

Closing costs typically include appraisal fees, title insurance, lender fees, and taxes. These costs can range from 2% to 5% of the home’s purchase price.

Q9: How long does it take to save for a down payment?

The time it takes to save for a down payment depends on your income, expenses, and savings habits. By creating a detailed budget and setting realistic goals, you can accelerate your savings and achieve your homeownership dreams.

Q10: What are the tax benefits of owning a home?

Homeowners can often deduct mortgage interest and property taxes from their federal income taxes. These deductions can lower your overall tax liability and make homeownership more affordable.

Bottom Line: Your Path to Homeownership Starts Here

A large down payment can indeed offset low income, making homeownership a reachable goal. Strategic financial planning, exploring the right loan options, and leveraging resources like income-partners.net can pave your way to owning a home, even with a limited income.

At income-partners.net, we understand the challenges you face, and we are committed to providing the tools, resources, and partnerships you need to succeed. Explore our website at income-partners.net to discover partnership opportunities, educational resources, and personalized guidance that can help you achieve your financial goals.

Ready to take the next step? Contact us at +1 (512) 471-3434 or visit our office at 1 University Station, Austin, TX 78712, United States, to learn more about how we can help you navigate the path to homeownership. Let us help you find the right partnerships and strategies to make your dreams a reality.