Does A 529 Plan Reduce My Taxable Income? Absolutely, a 529 plan can indeed reduce your taxable income, particularly at the state level, offering a smart way to save for education while potentially lowering your tax burden. At income-partners.net, we help you navigate these financial strategies to maximize your savings and investment opportunities through strategic partnerships. Discover how these education savings plans can benefit you with the right resources, planning tools, and potential collaborative ventures that can elevate your financial health. Explore the advantages of tax-advantaged savings, investment growth, and strategic financial planning for long-term success.

1. Understanding 529 Plans and Their Tax Advantages

529 plans are specifically designed to encourage saving for future education expenses. While they don’t offer a federal income tax deduction, the tax benefits at the state level can be significant. Let’s explore how these plans work and why they are attractive.

A 529 plan is an investment account that offers tax advantages when used for qualified education expenses. These plans are typically sponsored by states, state agencies, or educational institutions. According to the University of Texas at Austin’s McCombs School of Business, strategic financial planning, including 529 plans, can significantly enhance long-term financial security.

1.1. Types of 529 Plans

There are two main types of 529 plans:

-

529 Savings Plans: These plans allow you to invest in a variety of mutual funds or other investments. The earnings grow tax-free, and withdrawals are also tax-free if used for qualified education expenses.

-

529 Prepaid Tuition Plans: These plans allow you to purchase tuition credits at today’s prices for use at participating colleges in the future. They are often state-sponsored and may have residency requirements.

1.2. Federal vs. State Tax Benefits

While there is no federal income tax deduction for contributions to a 529 plan, the federal government does offer other tax advantages:

- Tax-Free Growth: Earnings in a 529 plan grow tax-free.

- Tax-Free Withdrawals: Withdrawals for qualified education expenses are tax-free.

Many states offer additional tax benefits for 529 plan contributions, such as state income tax deductions or credits. These benefits can significantly reduce your state taxable income.

2. State Income Tax Benefits for 529 Plan Contributions

Many states provide state income tax benefits for contributions to a 529 plan, allowing residents to deduct a portion or all of their contributions from their state taxable income. These benefits vary widely by state.

According to a study by the College Savings Plans Network, state tax incentives can significantly boost participation in 529 plans, encouraging more families to save for education.

2.1. States with Income Tax Deductions

Over 30 states offer an income tax deduction for contributions to a 529 plan. The specifics vary, including:

- Deduction Limits: Some states have annual limits on the amount you can deduct.

- Residency Requirements: Most states require you to contribute to their own state’s 529 plan to be eligible for the deduction.

- Contributor Eligibility: Some states allow anyone to claim the deduction, while others restrict it to the account owner.

Here’s a detailed look at how various states handle these deductions:

| State | Deduction Type | Deduction Limit | Notes |

|---|---|---|---|

| Arizona | Income Tax Deduction | Up to $2,000 (single) / $4,000 (married filing jointly) | Available for contributions to any 529 plan. |

| Arkansas | Income Tax Deduction | Up to $4,000 per taxpayer | Available for contributions to any 529 plan. |

| Colorado | Income Tax Deduction | Up to $20,700 per beneficiary | Unlimited if under age 19. |

| Connecticut | Income Tax Deduction | Up to $5,000 (single) / $10,000 (married filing jointly) | |

| Indiana | Income Tax Credit | 20% of contributions, up to $1,000 credit | |

| Iowa | Income Tax Deduction | Up to $3,474 per beneficiary | |

| Kansas | Income Tax Deduction | Up to $3,000 per beneficiary | Available for contributions to any 529 plan. |

| Maine | Income Tax Deduction | Up to $250 (single) / $500 (married filing jointly) | Available for contributions to any 529 plan. |

| Maryland | Income Tax Deduction | Up to $2,500 per beneficiary | |

| Massachusetts | Income Tax Deduction | Up to $1,000 (single) / $2,000 (married filing jointly) | |

| Michigan | Income Tax Deduction | Limited Deduction | Benefits are based on annual contributions net of distributions. |

| Minnesota | Income Tax Deduction/Credit | Varies by AGI | Taxpayers are eligible for either a deduction or credit depending on their adjusted gross income. Available for contributions to any 529 plan. |

| Missouri | Income Tax Deduction | Up to $8,000 (single) / $16,000 (married filing jointly) | Available for contributions to any 529 plan. |

| Montana | Income Tax Credit | Up to $3,000 per taxpayer | Available for contributions to any 529 plan. |

| Nebraska | Income Tax Deduction | Up to $10,000 (single) / $5,000 (married filing jointly) | |

| New Hampshire | No Income Tax | N/A | |

| New Mexico | Income Tax Deduction | Full Deduction | |

| New York | Income Tax Deduction | Up to $5,000 (single) / $10,000 (married filing jointly) | |

| North Dakota | Income Tax Deduction | Up to $5,000 (single) / $10,000 (married filing jointly) | |

| Ohio | Income Tax Deduction | Up to $4,000 per beneficiary | Available for contributions to any 529 plan. |

| Oklahoma | Income Tax Deduction | Up to $10,000 (single) / $20,000 (married filing jointly) | |

| Oregon | Income Tax Credit | Varies, based on income | |

| Pennsylvania | Income Tax Deduction | Up to $16,000 per beneficiary | Available for contributions to any 529 plan. |

| Rhode Island | Income Tax Deduction | Up to $1,000 (single) / $2,000 (married filing jointly) | |

| South Carolina | Income Tax Deduction | Full Deduction | |

| Tennessee | No Income Tax | N/A | |

| Texas | No Income Tax | N/A | |

| Utah | Income Tax Credit | 4.95% of contributions, up to certain limits | |

| Vermont | Income Tax Credit | 10% of contributions, up to $250 | |

| Virginia | Income Tax Deduction | Up to $4,000 per account | |

| West Virginia | Income Tax Deduction | Full Deduction | |

| Wisconsin | Income Tax Deduction | Limited Deduction | State tax benefits based on annual contributions net of distributions. |

Note: Always consult a tax professional for personalized advice.

2.2. States with Tax Credits

A few states offer a tax credit rather than a deduction. A tax credit directly reduces your tax liability, providing a dollar-for-dollar reduction in the amount of tax you owe.

- Indiana: Offers a tax credit for 20% of contributions, up to a $1,000 credit.

- Oregon: Provides a tax credit based on income.

- Utah: Offers a tax credit equal to 4.95% of contributions, up to certain limits.

- Vermont: Provides a tax credit of 10% of contributions, up to $250.

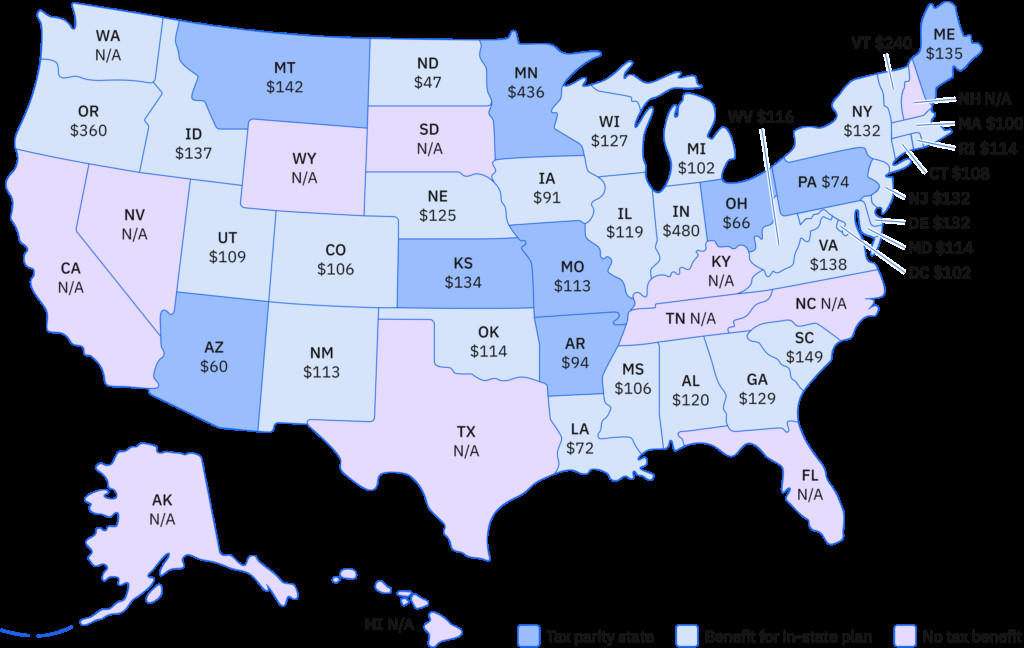

2.3. Tax Parity States

Nine states offer a state income tax benefit for contributions to any 529 plan, not just in-state plans. These states are known as “tax parity states” and include:

- Arizona

- Arkansas

- Kansas

- Maine

- Minnesota

- Missouri

- Montana

- Ohio

- Pennsylvania

This flexibility can be advantageous if another state’s 529 plan offers better investment options or lower fees.

529 Plan Contributions

529 Plan Contributions

3. How State Income Tax Deductions and Credits Work

The amount of state income tax benefit you can receive depends on the rules in your state. Generally, the benefit is based on the total amount of your 529 plan contributions during the tax year.

3.1. Contribution Limits

While 529 plans do not have annual contribution limits, most states limit the total contributions that qualify for an income tax credit or deduction. For instance, New York residents can deduct up to $5,000 for single filers and $10,000 for those married filing jointly.

3.2. Timing of Contributions

Most states require that 529 plan contributions be made by December 31 to qualify for a state income tax benefit in that tax year. However, some states offer a grace period, allowing contributions made in the following year to be applied to the prior tax year.

3.3. Special Cases and Loopholes

Some taxpayers attempt to exploit loopholes by contributing to a 529 plan, immediately taking a qualified distribution, and claiming the state income tax benefit. However, some states have implemented rules to prevent this. For example, Montana and Wisconsin impose time limits, while Michigan and Minnesota base state income tax benefits on annual contributions net of distributions.

3.4. K-12 Tuition and Graduate School

Parents saving for K-12 tuition and adults using a 529 plan to pay for graduate school may effectively receive an annual tuition discount by funneling payments through a 529 plan and claiming a state income tax benefit each year.

4. Who Is Eligible for a 529 Plan State Income Tax Benefit?

Eligibility for a 529 plan state income tax benefit typically extends to taxpayers who contribute to a 529 plan, including grandparents or other loved ones. However, in some states, only the 529 plan account owner (or the account owner’s spouse) may claim the benefit.

According to a report by Fidelity Investments, families with 529 plans tend to have higher overall savings rates, suggesting that these plans encourage a broader savings mindset.

4.1. Beneficiary’s Age

Eligible taxpayers can continue to claim a 529 plan state income tax benefit each year they contribute, regardless of the beneficiary’s age. There are no time limits on 529 plan accounts, so families can continue contributing throughout the child’s elementary school, middle school, high school, college years, and beyond.

4.2. Factors to Consider Beyond Tax Benefits

While state income tax benefits are a significant advantage, they should not be the only factor in choosing a 529 plan. Attributes such as fees and investment performance should also be considered. In some cases, the better investment performance of another state’s 529 plan can outweigh the benefits of a state income tax deduction.

5. Maximizing Your 529 Plan Benefits: A Strategic Approach

To truly maximize the benefits of a 529 plan, it’s essential to consider various factors and adopt a strategic approach. This involves understanding your state’s specific rules, optimizing contributions, and carefully evaluating investment options.

5.1. Understanding Your State’s Specific Rules

Each state has its own unique set of rules and regulations regarding 529 plans. It’s crucial to thoroughly understand these rules to maximize your benefits. Key aspects to consider include:

- Deduction or Credit Limits: Know the maximum amount you can deduct or the percentage you can claim as a credit.

- Residency Requirements: Determine whether you need to invest in your state’s plan to be eligible for the tax benefit.

- Contributor Eligibility: Clarify who can claim the tax benefit – is it limited to the account owner or can anyone contributing claim it?

- Carryover Provisions: Check if you can carry forward any unused deductions or credits to future tax years.

5.2. Optimizing Contributions

To take full advantage of state tax benefits, optimize your contributions based on your state’s rules. Consider these strategies:

- Front-Loading: If your state allows, consider front-loading contributions to maximize the tax benefit in a single year.

- Annual Contributions: If front-loading isn’t feasible or beneficial, make consistent annual contributions up to the deduction or credit limit.

- Gift Contributions: Encourage family members to contribute to the 529 plan, especially if they are also eligible for a state tax benefit.

5.3. Evaluating Investment Options

While state tax benefits are important, don’t overlook the investment aspect of 529 plans. Evaluate the investment options offered by different plans, considering factors such as:

- Expense Ratios: Look for plans with low expense ratios to minimize costs.

- Investment Performance: Review the historical performance of different investment options.

- Asset Allocation: Choose an asset allocation that aligns with your risk tolerance and time horizon.

- Age-Based Portfolios: Consider age-based portfolios that automatically adjust the asset allocation as the beneficiary gets closer to college age.

5.4. Coordinating with Other Savings Vehicles

529 plans are just one piece of the college savings puzzle. Coordinate your 529 plan with other savings vehicles, such as:

- Coverdell ESAs: These accounts offer tax-free growth and withdrawals for education expenses, but have lower contribution limits than 529 plans.

- Roth IRAs: While not specifically designed for education savings, Roth IRAs can be used for this purpose, offering tax-free growth and withdrawals (subject to certain rules).

- Taxable Investment Accounts: These accounts offer flexibility but do not provide the same tax advantages as 529 plans or Coverdell ESAs.

5.5. Estate Planning Considerations

529 plans can also be a valuable tool for estate planning. Contributions to a 529 plan are considered completed gifts, which can help reduce the size of your taxable estate. Additionally, the assets in a 529 plan are not subject to estate tax.

5.6. Professional Advice

Navigating the complexities of 529 plans and state tax benefits can be challenging. Consider seeking professional advice from a financial advisor or tax professional who can help you develop a customized savings strategy.

6. Real-Life Examples and Case Studies

To illustrate the practical benefits of 529 plans and state income tax deductions, let’s examine a few real-life examples and case studies.

6.1. Case Study 1: The Smith Family in New York

The Smith family lives in New York and has two children, ages 8 and 10. They contribute $5,000 per year to each child’s 529 plan. New York allows a state income tax deduction of up to $5,000 per taxpayer for contributions to a 529 plan.

- Tax Benefit: The Smiths can deduct $10,000 from their state taxable income each year ($5,000 for each child).

- Savings: Assuming a state income tax rate of 6%, this deduction saves them $600 per year in state income taxes.

- Long-Term Impact: Over 10 years, the Smiths save $6,000 in state income taxes, in addition to the tax-free growth and withdrawals of their 529 plans.

6.2. Case Study 2: The Johnson Family in Arizona

The Johnson family lives in Arizona, a tax parity state. They have one child, age 6, and contribute $4,000 per year to a 529 plan offered by another state that has lower fees and better investment options than Arizona’s plan.

- Tax Benefit: Arizona allows a state income tax deduction of up to $2,000 per taxpayer for contributions to any 529 plan.

- Savings: The Johnsons can deduct $2,000 from their state taxable income each year.

- Long-Term Impact: Assuming a state income tax rate of 4%, this deduction saves them $80 per year in state income taxes. While the tax savings are modest, they are also benefiting from lower fees and better investment performance in the out-of-state plan.

6.3. Example 3: The Patel Family in Indiana

The Patel family lives in Indiana, which offers a tax credit for contributions to a 529 plan. They have one child, age 4, and contribute $5,000 per year to Indiana’s 529 plan.

- Tax Benefit: Indiana offers a tax credit of 20% of contributions, up to a $1,000 credit.

- Savings: The Patels receive a tax credit of $1,000 each year, directly reducing their state income tax liability.

- Long-Term Impact: Over 14 years (until their child turns 18), the Patels receive a total of $14,000 in tax credits, significantly reducing their overall tax burden.

6.4. Success Story: Grandparents Saving for Grandchildren

John and Mary are grandparents who want to help their grandchildren pay for college. They live in a state that allows anyone to contribute to a 529 plan and claim a state income tax deduction. They contribute $10,000 per year to each of their two grandchildren’s 529 plans.

- Tax Benefit: John and Mary can deduct $20,000 from their state taxable income each year ($10,000 for each grandchild).

- Impact: This not only reduces their state income tax liability but also helps them reduce the size of their taxable estate, as contributions to a 529 plan are considered completed gifts.

- Legacy: John and Mary are able to provide significant financial support for their grandchildren’s education while also benefiting from tax savings and estate planning advantages.

7. Common Mistakes to Avoid with 529 Plans

While 529 plans offer numerous benefits, it’s important to avoid common mistakes that can undermine your savings strategy.

7.1. Not Starting Early Enough

One of the biggest mistakes is waiting too long to start saving. The earlier you start, the more time your investments have to grow tax-free. Even small contributions made early on can make a significant difference over time.

7.2. Overlooking State Tax Benefits

Many people are unaware of the state tax benefits offered by 529 plans. Failing to take advantage of these benefits can result in missed tax savings.

7.3. Choosing the Wrong Investment Options

Selecting inappropriate investment options can hinder your savings progress. It’s important to choose an asset allocation that aligns with your risk tolerance and time horizon. Avoid being too conservative, especially when saving for a young child, as this can limit potential growth.

7.4. Not Understanding Qualified Education Expenses

Withdrawing funds for non-qualified expenses can trigger taxes and penalties, negating the tax advantages of the 529 plan. Make sure you understand what expenses qualify for tax-free withdrawals, such as tuition, fees, books, and room and board.

7.5. Ignoring Fees and Expenses

Fees and expenses can eat into your investment returns. Pay attention to the expense ratios and other fees charged by different 529 plans, and choose a plan with reasonable costs.

7.6. Failing to Update Beneficiary Information

If the original beneficiary decides not to attend college or receives a full scholarship, you can change the beneficiary to another eligible family member. Failing to update the beneficiary information can limit your options and potentially result in taxable withdrawals.

7.7. Overfunding the Account

While there are no annual contribution limits to 529 plans, there are overall limits. Overfunding the account can result in gift tax implications. Be mindful of the overall contribution limits and coordinate with other family members who may be contributing to the same account.

7.8. Not Seeking Professional Advice

Navigating the complexities of 529 plans can be challenging. Don’t hesitate to seek professional advice from a financial advisor or tax professional who can help you develop a customized savings strategy.

8. The Future of 529 Plans: Trends and Updates

The landscape of 529 plans is constantly evolving, with new trends and updates emerging regularly. Staying informed about these changes can help you make the most of your 529 plan and adapt your savings strategy accordingly.

8.1. Expansion of Qualified Education Expenses

One notable trend is the expansion of qualified education expenses covered by 529 plans. In recent years, Congress has expanded the definition of qualified education expenses to include:

- K-12 Tuition: Up to $10,000 per year can be used for tuition at elementary and secondary schools.

- Student Loan Repayment: Up to $10,000 can be used to repay student loans.

These expansions have made 529 plans even more versatile and valuable for families saving for education.

8.2. Increased Awareness and Adoption

Awareness and adoption of 529 plans have been steadily increasing in recent years. As more families recognize the benefits of these plans, participation rates are likely to continue to rise.

8.3. Technological Innovations

Technological innovations are also playing a role in the evolution of 529 plans. Online platforms and mobile apps are making it easier than ever to open, manage, and contribute to 529 plans. These tools can help families stay on track with their savings goals and make informed investment decisions.

8.4. Legislative Changes

Legislative changes can also impact 529 plans. Congress and state legislatures may introduce new laws or regulations that affect contribution limits, tax benefits, and other aspects of these plans. Staying informed about these changes is crucial for maximizing your benefits.

8.5. Focus on Financial Literacy

There is a growing focus on financial literacy and the importance of saving for education. Many organizations and initiatives are working to educate families about 529 plans and other college savings options.

9. Partnering for Success: How Income-Partners.Net Can Help

At income-partners.net, we understand the importance of strategic financial planning and the role that 529 plans can play in achieving your education savings goals. We offer a range of resources and services to help you navigate the complexities of 529 plans and make informed decisions.

9.1. Expert Guidance

Our team of financial experts can provide personalized guidance on choosing the right 529 plan for your needs, optimizing contributions, and developing a comprehensive savings strategy.

9.2. Educational Resources

We offer a wealth of educational resources, including articles, guides, and webinars, to help you understand the ins and outs of 529 plans and state tax benefits.

9.3. Partner Network

Our partner network includes leading financial institutions and education providers, allowing us to offer a wide range of 529 plan options and related services.

9.4. Collaborative Ventures

We facilitate collaborative ventures between families, educators, and financial professionals to promote education savings and financial literacy.

9.5. Up-to-Date Information

We stay on top of the latest trends and updates in the 529 plan landscape, ensuring that our clients have access to the most accurate and relevant information.

10. Frequently Asked Questions (FAQs) About 529 Plans and Taxable Income

Here are some frequently asked questions about 529 plans and their impact on taxable income:

10.1. Do 529 Contributions Reduce State Taxable Income?

Yes, in many states, contributions to a 529 plan can reduce your state taxable income. The amount you can deduct or the credit you can claim varies by state.

10.2. Is There a Federal Tax Deduction for 529 Contributions?

No, there is no federal income tax deduction for contributions to a 529 plan. However, earnings grow tax-free, and withdrawals for qualified education expenses are also tax-free at the federal level.

10.3. Which States Allow Tax Deductions for 529 Contributions?

Over 30 states offer tax deductions or credits for contributions to a 529 plan. The specific rules vary by state.

10.4. Can I Deduct Out-of-State 529 Contributions?

In some states, known as tax parity states, you can deduct contributions to any 529 plan, regardless of whether it’s offered by your state or another state.

10.5. Are 529 Contributions Pre-Tax or Post-Tax?

529 contributions are made with post-tax dollars. However, the earnings grow tax-free, and withdrawals for qualified education expenses are also tax-free.

10.6. Are 529 Contributions Tax-Deductible for Grandparents?

In many states, grandparents can contribute to a 529 plan and claim a state income tax deduction or credit, even if they are not the account owner.

10.7. What Happens if I Withdraw Money for Non-Qualified Expenses?

If you withdraw money from a 529 plan for non-qualified expenses, the earnings portion of the withdrawal will be subject to federal and state income taxes, as well as a 10% penalty.

10.8. Can I Change the Beneficiary of a 529 Plan?

Yes, you can change the beneficiary of a 529 plan to another eligible family member without incurring taxes or penalties.

10.9. What Are Qualified Education Expenses?

Qualified education expenses include tuition, fees, books, supplies, and equipment required for enrollment or attendance at an eligible educational institution. In some cases, room and board may also qualify.

10.10. How Do I Open a 529 Plan?

You can open a 529 plan directly through a state-sponsored plan or through a financial institution that offers 529 plans.

Ready to explore how a 529 plan can benefit you? At income-partners.net, we invite you to delve deeper into strategic financial planning and discover the power of collaborative ventures. Contact us today at Address: 1 University Station, Austin, TX 78712, United States, Phone: +1 (512) 471-3434, or visit our website at income-partners.net to start building your future with confidence. Let’s connect and cultivate partnerships that drive financial success.