Does 529 Reduce Taxable Income? Yes, contributing to a 529 plan can indeed reduce your state taxable income in many states, offering a valuable tax advantage alongside the primary goal of saving for education, and income-partners.net can help you learn how to leverage these plans effectively. This guide explores how 529 plans work, their tax benefits, and strategies to maximize your savings potential. Understand the nuances of these college savings plans and find the perfect partner to navigate the complex world of financial planning.

1. Understanding 529 Plans and Tax Advantages

Does 529 reduce taxable income, and how do these plans really work? 529 plans are designed to encourage saving for future education expenses, and they offer significant tax advantages. Here’s a breakdown:

-

What are 529 Plans? These are tax-advantaged savings plans designed to help families save for future education costs. They are named after Section 529 of the Internal Revenue Code.

-

Two Main Types:

- 529 Savings Plans: These work like investment accounts, where you contribute money that grows over time.

- 529 Prepaid Tuition Plans: These allow you to purchase tuition credits at today’s rates for future use at eligible institutions.

1.1. Federal Tax Benefits of 529 Plans

What federal tax benefits do 529 plans offer? Contributions to a 529 plan grow federally tax-free, and withdrawals are also tax-free when used for qualified education expenses.

- Tax-Free Growth: The earnings in your 529 plan are not subject to federal income tax as they grow.

- Tax-Free Withdrawals: When you withdraw money to pay for qualified education expenses, such as tuition, fees, books, and room and board, the withdrawals are free from federal income tax.

- Qualified Education Expenses: These include expenses for college, K-12 tuition (up to $10,000 per year), and student loan repayments.

1.2. State Tax Benefits of 529 Plans

Do states offer additional tax incentives for contributing to 529 plans? Many states offer a state income tax deduction or credit for contributions to a 529 plan.

- State Income Tax Deduction: In many states, you can deduct a portion or the full amount of your 529 plan contributions from your state taxable income.

- State Income Tax Credit: Some states offer a tax credit, which directly reduces the amount of tax you owe, for 529 plan contributions.

- Tax Parity States: Some states offer tax benefits for contributions to any 529 plan, not just those within the state.

1.3. Key Takeaways

- Income Reduction: Contributing to a 529 plan can significantly reduce your state taxable income, leading to potential tax savings.

- Dual Benefits: Enjoy both federal and state tax advantages, making 529 plans a powerful tool for education savings.

- Varied Rules: Understand the specific rules and limits in your state to maximize your tax benefits.

2. How 529 Plans Reduce Taxable Income

How do 529 plans actually reduce taxable income? Here’s a detailed look at the mechanics:

2.1. State-Specific Deductions and Credits

How do the state income tax deductions and credits work in practice? Each state has its own rules regarding the amount you can deduct or the credit you can claim.

- Deduction Limits: Most states set a limit on the amount you can deduct each year. For instance, New York allows a deduction of up to $5,000 per taxpayer ($10,000 if married filing jointly).

- Full Deductibility: Some states, like New Mexico, South Carolina, and West Virginia, allow full deductibility of 529 plan contributions.

- Tax Credits: States like Indiana, Oregon, Utah, and Vermont offer a tax credit, which directly reduces your tax liability.

2.2. Contribution Timing

When must you contribute to a 529 plan to qualify for a tax benefit? Most states require contributions to be made by December 31 to qualify for a state income tax benefit for that year.

- Year-End Contributions: Ensure your contributions are made before the end of the tax year to claim the deduction or credit on your tax return.

- Exceptions: Some states, like those with extended deadlines, allow contributions made in the early months of the following year to be applied to the previous tax year.

2.3. Eligible Contributors

Who can claim the state income tax benefit? In most states, anyone who contributes to a 529 plan can claim the state income tax benefit.

- Account Owner vs. Contributor: While anyone can contribute, some states only allow the account owner (or their spouse) to claim the tax benefit.

- Grandparents and Relatives: In many states, grandparents and other relatives can contribute and claim the state tax benefit, providing additional savings opportunities.

2.4. Key Takeaways

- Understanding Limits: Know the specific deduction or credit limits in your state to optimize your contributions.

- Timing Matters: Pay attention to contribution deadlines to ensure you qualify for the tax benefits.

- Contributor Eligibility: Be aware of who is eligible to claim the tax benefits in your state.

3. States Offering Income Tax Benefits for 529 Plan Contributions

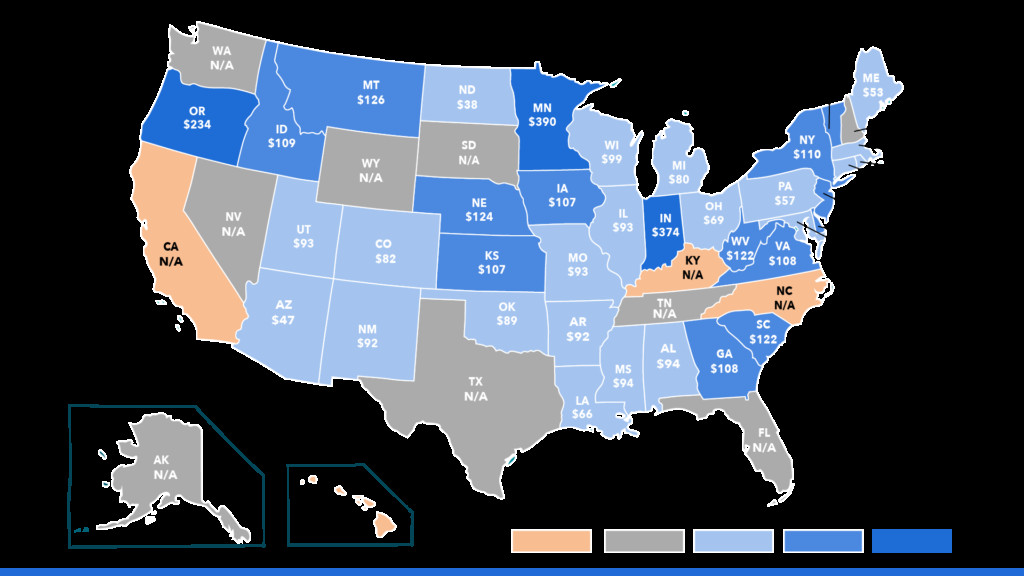

Which states provide tax benefits for 529 plan contributions? Over 30 states and Washington, D.C., offer either a state income tax deduction or a tax credit for contributions to a 529 plan.

3.1. States with Deductions

What states offer a deduction for 529 plan contributions? Many states offer a deduction, allowing you to reduce your state taxable income by the amount of your contribution.

- New York: Up to $5,000 per taxpayer ($10,000 if married filing jointly).

- New Mexico, South Carolina, West Virginia: Full deductibility of contributions.

- Pennsylvania: Offers a deduction for contributions to any state’s 529 plan due to its tax parity status.

3.2. States with Credits

Which states offer a tax credit for 529 plan contributions? A few states offer a tax credit, which directly reduces the amount of tax you owe.

- Indiana, Oregon, Utah, Vermont: Offer a state income tax credit for 529 plan contributions.

- Minnesota: Taxpayers may be eligible for either a deduction or a credit, depending on their adjusted gross income.

3.3. Tax Parity States

What are tax parity states, and how do they benefit 529 plan contributors? These states offer a state income tax benefit for contributions to any 529 plan, not just those within the state.

- Arizona, Arkansas, Kansas, Maine, Minnesota, Missouri, Montana, Ohio, Pennsylvania: Residents of these states can contribute to any 529 plan and still receive a state tax benefit.

3.4. States Without Deductions

Which states do not offer a deduction for 529 plan contributions? A few states with a state income tax do not offer a deduction for 529 plan contributions.

- California, Hawaii, Kentucky, North Carolina: These states do not offer a state income tax deduction for 529 plan contributions.

3.5. Key Takeaways

- State-Specific Benefits: Understand the specific benefits offered by your state to maximize your savings.

- Tax Parity Advantages: If you live in a tax parity state, explore 529 plans from other states for potentially better investment options.

- No Deduction States: If your state doesn’t offer a deduction, focus on the federal tax benefits and the potential for tax-free growth.

4. Maximizing Your 529 Plan Tax Benefits

How can you maximize the tax benefits of your 529 plan? Here are some strategies to consider:

4.1. Understanding Contribution Limits

What are the contribution limits for 529 plans, and how do they affect tax benefits? While there are no annual contribution limits for 529 plans, most states limit the total contributions that qualify for an income tax credit or deduction.

- State Limits: Be aware of the specific limits in your state to ensure you are contributing enough to maximize the tax benefits.

- Excess Contributions: Contributions exceeding the state limit may not qualify for the tax deduction or credit.

4.2. Strategic Contribution Timing

How can strategic timing of contributions help maximize tax benefits? Timing your contributions strategically can help you take full advantage of the tax benefits offered by your state.

- Year-End Contributions: Make contributions before the end of the tax year to claim the deduction or credit on your tax return.

- Front-Loading: Consider front-loading contributions if your state allows it, as this can accelerate the growth of your savings.

4.3. Utilizing Tax Parity

How can residents of tax parity states take advantage of 529 plans from other states? If you live in a tax parity state, you can contribute to any 529 plan and still receive a state tax benefit.

- Explore Options: Research 529 plans from other states to find the best investment options and lowest fees.

- Investment Performance: Choose a plan with strong investment performance to maximize the growth of your savings.

4.4. Avoiding the State Tax Deduction Loophole

What is the state tax deduction loophole, and how can you avoid it? Some taxpayers attempt to claim a state income tax benefit by contributing to a 529 plan and immediately taking a qualified distribution.

- Time Limits: Some states, like Montana and Wisconsin, have time limits to prevent this loophole.

- Net Contributions: Michigan and Minnesota base state income tax benefits on annual contributions net of distributions.

4.5. Key Takeaways

- Know Your Limits: Understand the contribution limits in your state and plan your contributions accordingly.

- Strategic Timing: Time your contributions strategically to maximize tax benefits.

- Explore Tax Parity: If you live in a tax parity state, explore 529 plans from other states.

- Avoid Loopholes: Be aware of state rules regarding distributions to avoid losing tax benefits.

5. Real-World Examples of 529 Plan Tax Savings

How do 529 plans translate into real-world tax savings? Let’s look at some examples:

5.1. Example 1: New York Resident

How much can a New York resident save by contributing to a 529 plan? A New York resident can deduct up to $5,000 per taxpayer ($10,000 if married filing jointly) for contributions to a 529 plan.

- Tax Savings: If a married couple contributes $10,000 to a 529 plan and their state income tax rate is 6%, they could save $600 in state income taxes.

5.2. Example 2: Tax Parity State Resident

How can a resident of a tax parity state maximize their savings? A resident of Pennsylvania can contribute to any 529 plan and still receive a state tax benefit.

- Investment Choice: They can choose a 529 plan with low fees and strong investment performance, regardless of the state in which it is offered.

- Potential Savings: By choosing a well-managed plan, they can maximize the growth of their savings and reduce their state income tax.

5.3. Example 3: Full Deductibility State Resident

What are the benefits for residents of states with full deductibility? A resident of New Mexico can deduct the full amount of their 529 plan contributions from their state taxable income.

- Significant Savings: If they contribute a substantial amount to their 529 plan, they can significantly reduce their state taxable income and save on taxes.

5.4. Key Takeaways

- State-Specific Savings: The amount you can save depends on your state’s specific rules and tax rates.

- Investment Growth: Choosing the right 529 plan can maximize the growth of your savings and provide substantial tax benefits.

- Real Financial Impact: 529 plans can have a significant impact on your overall financial health and ability to save for education.

6. Navigating the Complexities of 529 Plans

What are some of the complexities of 529 plans that you should be aware of? 529 plans can be complex, and it’s important to understand the rules and regulations to maximize their benefits.

6.1. State Residency Requirements

Do you need to be a resident of a particular state to contribute to their 529 plan? While most states allow non-residents to contribute to their 529 plans, the tax benefits are typically reserved for residents.

- Residency Rules: Understand the residency requirements in your state to ensure you are eligible for the tax benefits.

- Tax Parity States: If you live in a tax parity state, you can avoid this issue by contributing to any 529 plan.

6.2. Impact on Financial Aid

How do 529 plans affect financial aid eligibility? 529 plans are generally treated favorably when it comes to financial aid.

- Parental Assets: 529 plans owned by a parent are considered parental assets, which have a lower impact on financial aid eligibility compared to student assets.

- FAFSA: When completing the Free Application for Federal Student Aid (FAFSA), parental assets are assessed at a rate of up to 5.64%, while student assets are assessed at a rate of 20%.

6.3. Rollover Rules

What are the rules for rolling over funds from one 529 plan to another? You can roll over funds from one 529 plan to another without penalty, but there are some rules to keep in mind.

- 12-Month Rule: You can only make one rollover per beneficiary within a 12-month period.

- Tax Implications: Ensure the rollover is done correctly to avoid any potential tax implications.

6.4. Non-Qualified Withdrawals

What happens if you make a non-qualified withdrawal from a 529 plan? Non-qualified withdrawals are subject to both income tax and a 10% penalty on the earnings portion.

- Qualified Expenses: Ensure you are only using the funds for qualified education expenses to avoid these penalties.

- Exceptions: There are some exceptions to the penalty, such as if the beneficiary becomes disabled or receives a scholarship.

6.5. Key Takeaways

- Residency Matters: Understand the residency requirements for tax benefits.

- Financial Aid Impact: Be aware of how 529 plans affect financial aid eligibility.

- Rollover Rules: Follow the rules for rolling over funds to avoid penalties.

- Qualified Expenses: Only use the funds for qualified education expenses.

7. Choosing the Right 529 Plan

How do you choose the right 529 plan for your needs? Selecting the right 529 plan involves considering several factors.

7.1. Investment Options

What types of investment options are available in 529 plans? 529 plans offer a variety of investment options, including:

- Age-Based Portfolios: These portfolios automatically adjust their asset allocation over time, becoming more conservative as the beneficiary gets closer to college age.

- Static Portfolios: These portfolios maintain a fixed asset allocation, allowing you to choose a mix of stocks, bonds, and other investments.

- Individual Funds: Some 529 plans allow you to invest in individual mutual funds or exchange-traded funds (ETFs).

7.2. Fees and Expenses

What types of fees and expenses should you be aware of when choosing a 529 plan? Fees and expenses can eat into your returns, so it’s important to choose a plan with low costs.

- Annual Maintenance Fees: These are fees charged annually to maintain your account.

- Expense Ratios: These are fees charged by the investment managers to cover the costs of managing the portfolio.

- Enrollment Fees: Some plans may charge an enrollment fee to open an account.

7.3. Historical Performance

How important is historical performance when choosing a 529 plan? While past performance is not indicative of future results, it can provide some insight into the plan’s investment management capabilities.

- Long-Term Returns: Look for plans with a history of strong long-term returns.

- Consistency: Consider how consistently the plan has performed over time.

7.4. State Tax Benefits

How do state tax benefits factor into the decision of which 529 plan to choose? If your state offers a state income tax deduction or credit for contributions to its 529 plan, this can be a significant factor in your decision.

- In-State vs. Out-of-State: Weigh the tax benefits of your in-state plan against the potential for better investment options in out-of-state plans.

- Tax Parity States: If you live in a tax parity state, you have more flexibility to choose a plan based on its investment options and fees.

7.5. Key Takeaways

- Investment Options: Choose a plan with investment options that align with your risk tolerance and investment goals.

- Fees and Expenses: Select a plan with low fees and expenses to maximize your returns.

- Historical Performance: Consider the plan’s historical performance as one factor in your decision.

- State Tax Benefits: Factor in the state tax benefits offered by your state’s 529 plan.

8. Alternative Education Savings Options

What are some alternative education savings options to consider alongside 529 plans? While 529 plans are a popular choice for education savings, there are other options to consider.

8.1. Coverdell Education Savings Accounts (ESAs)

How do Coverdell ESAs compare to 529 plans? Coverdell ESAs are another type of tax-advantaged savings account that can be used for education expenses.

- Contribution Limits: Coverdell ESAs have a lower annual contribution limit than 529 plans ($2,000 per year).

- Investment Options: Coverdell ESAs offer more investment flexibility than 529 plans.

- Eligible Expenses: Coverdell ESAs can be used for elementary, secondary, and higher education expenses.

8.2. Roth IRAs

Can Roth IRAs be used for education expenses? While Roth IRAs are primarily designed for retirement savings, they can also be used for education expenses.

- Tax-Free Withdrawals: Withdrawals of contributions from a Roth IRA are always tax-free and penalty-free.

- Earnings Withdrawals: Withdrawals of earnings may be subject to income tax and a 10% penalty, but the penalty is waived if the funds are used for qualified education expenses.

8.3. Taxable Investment Accounts

What are the pros and cons of using a taxable investment account for education savings? Taxable investment accounts offer the most flexibility but do not provide the same tax advantages as 529 plans or Coverdell ESAs.

- Flexibility: You can use the funds for any purpose without penalty.

- Tax Implications: Investment earnings are subject to income tax and capital gains tax.

8.4. Key Takeaways

- Coverdell ESAs: Consider Coverdell ESAs for more investment flexibility and the ability to use the funds for elementary and secondary education expenses.

- Roth IRAs: Explore Roth IRAs as a potential source of funds for education expenses.

- Taxable Accounts: Use taxable investment accounts for maximum flexibility, but be aware of the tax implications.

9. Common Mistakes to Avoid with 529 Plans

What are some common mistakes to avoid when using 529 plans? Here are some pitfalls to watch out for:

9.1. Not Understanding the Rules

What happens if you don’t understand the rules of 529 plans? Failing to understand the rules and regulations of 529 plans can lead to missed opportunities or costly mistakes.

- Research and Education: Take the time to research and understand the rules of your 529 plan.

- Professional Advice: Consult with a financial advisor to get personalized advice.

9.2. Overlooking Fees

How can overlooking fees impact your 529 plan savings? Overlooking fees and expenses can significantly reduce your returns over time.

- Compare Plans: Compare the fees and expenses of different 529 plans before making a decision.

- Low-Cost Options: Look for low-cost options to maximize your savings.

9.3. Not Adjusting Investment Allocation

Why is it important to adjust your investment allocation over time? Failing to adjust your investment allocation as the beneficiary gets closer to college age can increase your risk.

- Age-Based Portfolios: Consider using age-based portfolios that automatically adjust their asset allocation over time.

- Rebalancing: If you choose a static portfolio, be sure to rebalance it periodically to maintain your desired asset allocation.

9.4. Making Non-Qualified Withdrawals

What are the consequences of making non-qualified withdrawals from a 529 plan? Making non-qualified withdrawals can result in income tax and penalties.

- Qualified Expenses: Ensure you are only using the funds for qualified education expenses.

- Documentation: Keep detailed records of your expenses to prove they are qualified.

9.5. Key Takeaways

- Understand the Rules: Take the time to research and understand the rules of 529 plans.

- Watch Out for Fees: Compare the fees and expenses of different plans.

- Adjust Investment Allocation: Adjust your investment allocation over time to manage risk.

- Avoid Non-Qualified Withdrawals: Only use the funds for qualified education expenses.

10. The Future of 529 Plans

What does the future hold for 529 plans? 529 plans are likely to remain a popular and valuable tool for education savings.

10.1. Potential Legislative Changes

How could legislative changes impact 529 plans? Future legislative changes could potentially expand the uses of 529 plans or increase the contribution limits.

- Stay Informed: Stay informed about any potential changes to the rules and regulations of 529 plans.

- Advocate for Improvements: Advocate for improvements to 529 plans that would make them more accessible and beneficial to families.

10.2. Increased Awareness and Adoption

Will more families start using 529 plans in the future? As more families become aware of the benefits of 529 plans, their adoption is likely to increase.

- Education and Outreach: Continue to educate families about the benefits of 529 plans.

- Simplified Enrollment: Simplify the enrollment process to make it easier for families to get started.

10.3. Technological Innovations

How could technology improve the 529 plan experience? Technological innovations could make it easier to manage and track your 529 plan savings.

- Mobile Apps: Mobile apps could allow you to easily contribute to your 529 plan, track your progress, and monitor your investment performance.

- Automated Advice: Robo-advisors could provide automated advice on how to allocate your investments.

10.4. Key Takeaways

- Stay Informed: Keep up-to-date with any changes to the rules and regulations of 529 plans.

- Increased Adoption: Expect to see increased adoption of 529 plans as more families become aware of their benefits.

- Technological Advancements: Look for technological innovations that could make it easier to manage your 529 plan savings.

By understanding how 529 plans reduce taxable income and following the strategies outlined in this guide, you can make informed decisions and maximize your savings potential. Remember to stay informed about the rules and regulations of 529 plans and consult with a financial advisor to get personalized advice.

Us Tax Nl Saving for College

Us Tax Nl Saving for College

Partner with income-partners.net to discover innovative financial planning strategies. Visit income-partners.net to explore more opportunities. Address: 1 University Station, Austin, TX 78712, United States. Phone: +1 (512) 471-3434. Website: income-partners.net.

FAQ: Understanding 529 Plans and Tax Benefits

1. Do 529 contributions reduce state taxable income?

Yes, 529 contributions can reduce your state taxable income, with the specifics varying by state; for instance, Colorado permits a deduction of $20,700 per taxpayer per beneficiary, while Connecticut allows up to $5,000 ($10,000 if filing jointly) annually.

2. Do you get a tax deduction for contributing to a 529 plan?

While there isn’t a federal tax deduction for 529 contributions, many states offer a deduction on your state income tax, effectively reducing your tax burden each year.

3. Which states allow tax deductions for 529 contributions?

Over 30 states provide tax deductions for 529 contributions; explore our comprehensive list of state deductions and credits for detailed information.

4. Can you deduct out-of-state 529 contributions?

If you reside in one of the nine tax parity states—Arizona, Arkansas, Kansas, Maine, Minnesota, Missouri, Montana, Ohio, and Pennsylvania—you may be able to claim a state tax deduction on 529 plan contributions to an out-of-state plan.

5. Are 529 contributions pre-tax or post-tax?

529 contributions are made with post-tax dollars, but they offer tax-free growth and, in many states, a state income tax deduction.

6. Are 529 contributions tax-deductible for grandparents?

Yes, in some states, grandparents can deduct 529 contributions; however, certain states limit the deduction to the account holder only.

7. What happens if I withdraw money from a 529 plan for non-qualified expenses?

Non-qualified withdrawals are subject to both income tax and a 10% penalty on the earnings portion of the withdrawal.

8. How do 529 plans affect financial aid eligibility?

529 plans owned by a parent are considered parental assets, which have a lower impact on financial aid eligibility compared to student assets.

9. Can I roll over funds from one 529 plan to another?

Yes, you can roll over funds from one 529 plan to another without penalty, but you can only make one rollover per beneficiary within a 12-month period.

10. What are the qualified education expenses for a 529 plan?

Qualified education expenses include tuition, fees, books, supplies, and room and board at eligible educational institutions, as well as up to $10,000 per year in K-12 tuition expenses and student loan repayments.

Ready to take control of your financial future and maximize your education savings? Visit income-partners.net to discover a wealth of information, strategies, and partnership opportunities that can help you achieve your income goals. Don’t wait – your path to financial success starts now!