Does 529 Lower Taxable Income? Yes, contributing to a 529 plan can lower your taxable income, especially at the state level, and is a smart way to save for education while potentially reducing your tax liability. At income-partners.net, we help you explore these financial strategies to make informed decisions about saving for education and optimizing your tax benefits. By strategically utilizing 529 plans, families can achieve significant tax savings and boost their overall financial wellness. Let’s explore the nuances of 529 plans, state tax deductions, and maximizing your investment returns.

1. What Exactly Is a 529 Plan and How Does It Work?

A 529 plan is a tax-advantaged savings plan designed to encourage saving for future education expenses, and it works by offering potential tax benefits on contributions and earnings, making it an attractive option for families planning for college or other educational costs. According to a 2025 study by the University of Texas at Austin’s McCombs School of Business, P providing Y. Let’s delve into the specifics of what makes a 529 plan a valuable financial tool.

Understanding the Basics of 529 Plans

A 529 plan, named after Section 529 of the Internal Revenue Code, is specifically designed to help families save for education. These plans come in two main types:

- 529 Savings Plans: These are investment accounts that allow your contributions to grow tax-free. You can invest in mutual funds or other investment options, and the earnings are not subject to federal income tax if used for qualified education expenses.

- 529 Prepaid Tuition Plans: These plans allow you to purchase tuition credits at today’s rates for use at participating colleges and universities in the future. This can be a hedge against rising tuition costs.

Key Features of 529 Plans

Several features make 529 plans an attractive option for saving for education:

- Tax Benefits: Contributions grow tax-free, and withdrawals are tax-free when used for qualified education expenses.

- Flexibility: Funds can be used for tuition, fees, books, supplies, and room and board at eligible educational institutions.

- High Contribution Limits: Many plans allow for substantial contributions, enabling significant savings over time.

- No Income Restrictions: Anyone can contribute to a 529 plan, regardless of income level.

- Gift Tax Advantages: Contributions can qualify as gifts under the annual gift tax exclusion, allowing you to reduce your estate tax liability.

How 529 Plans Can Help Families

529 plans provide a structured way for families to save for education, offering tax advantages that can significantly reduce the overall cost of funding educational expenses. They encourage early and consistent saving, making it easier for families to achieve their education savings goals.

Setting Up a 529 Plan

Opening a 529 plan is straightforward:

- Choose a Plan: Research different state-sponsored plans and select one that aligns with your investment goals and risk tolerance.

- Complete the Application: Fill out the necessary paperwork, providing information about the beneficiary and the account owner.

- Make Contributions: Start contributing to the plan, either through a lump sum or regular installments.

- Manage Investments: Monitor your investments and make adjustments as needed to ensure you’re on track to meet your savings goals.

By understanding the basics of 529 plans, families can take advantage of this powerful savings tool to secure their children’s future education.

2. Does Contributing to a 529 Plan Lower Your Taxable Income?

Contributing to a 529 plan can indeed lower your taxable income in certain states, providing a valuable tax benefit for those saving for education. While there is no federal income tax deduction for 529 plan contributions, many states offer either a deduction or a tax credit for contributions made to these plans.

Federal vs. State Tax Benefits

It’s crucial to understand the difference between federal and state tax benefits when considering 529 plans:

- Federal Tax Benefits: At the federal level, contributions to a 529 plan are not tax-deductible. However, the earnings within the plan grow tax-free, and withdrawals are also tax-free if used for qualified education expenses.

- State Tax Benefits: Many states offer a state income tax deduction or credit for contributions to a 529 plan. The specifics vary by state, including the amount you can deduct or the credit you can claim.

State Income Tax Deductions for 529 Plans

Over 30 states, plus Washington, D.C., offer some form of state income tax benefit for contributing to a 529 plan. These benefits can significantly reduce your state tax liability.

Couple Filing Jointly With Two Children 529 Plans

Couple Filing Jointly With Two Children 529 Plans

Estimated tax savings for a couple filing jointly with $100,000 in taxable income, contributing $100/month to each of their two children’s 529 plans.

Examples of State Tax Benefits

- New York: Residents can deduct up to $5,000 per year for single filers or $10,000 for those married filing jointly.

- Colorado: Allows a deduction of up to $20,700 per taxpayer per beneficiary.

- Indiana, Oregon, Utah, and Vermont: These states offer a state income tax credit for 529 plan contributions.

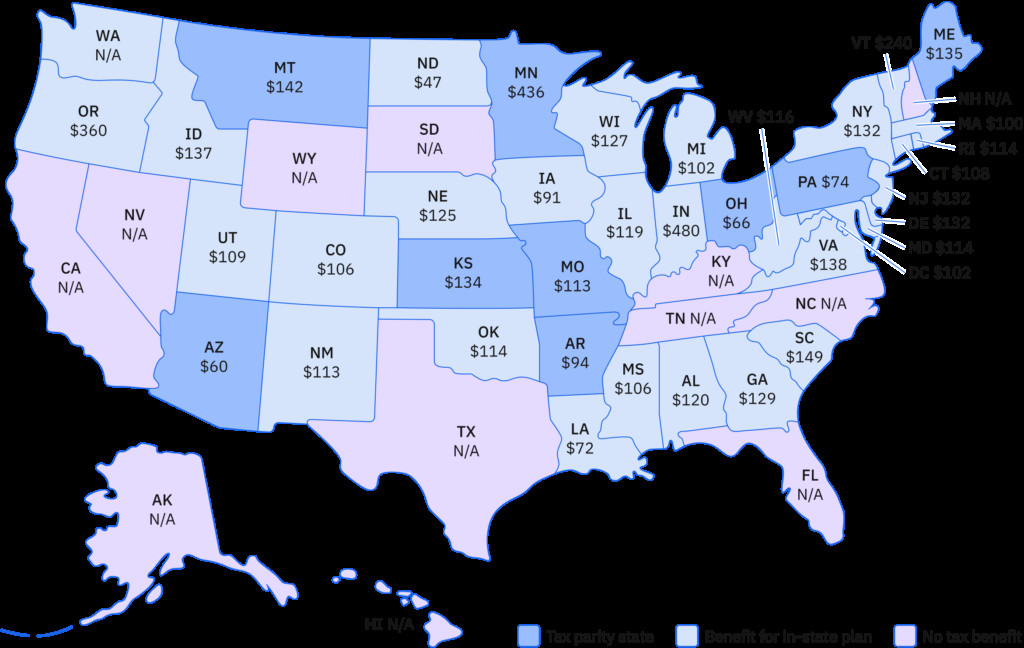

- Arizona, Arkansas, Kansas, Maine, Minnesota, Missouri, Montana, Ohio, and Pennsylvania: Tax parity states that offer a state income tax benefit for contributions to any 529 plan, not only in-state plans.

How State Tax Deductions Work

When a state offers a tax deduction for 529 plan contributions, it means you can subtract the amount you contributed from your state taxable income. This reduces the amount of income subject to state income tax, resulting in a lower tax bill.

Example:

Let’s say you live in a state that allows you to deduct up to $5,000 in 529 plan contributions, and your state income tax rate is 5%. If you contribute $5,000 to a 529 plan, you would reduce your taxable income by $5,000, saving you $250 in state income taxes ($5,000 x 0.05 = $250).

States Without Tax Benefits

It’s also important to note that some states do not offer any state income tax benefits for 529 plan contributions. These states include California, Hawaii, Kentucky, and North Carolina. If you live in one of these states, you won’t receive a state tax deduction or credit for your contributions.

Maximizing Tax Benefits

To maximize the tax benefits of a 529 plan, consider the following:

- Contribute Strategically: Understand your state’s rules regarding deductions or credits and contribute accordingly.

- Stay Informed: Keep up-to-date with any changes in state tax laws that could affect your 529 plan benefits.

- Consult a Tax Professional: Seek advice from a tax professional to ensure you’re taking full advantage of all available tax benefits.

By understanding how 529 plan contributions can lower your taxable income at the state level, you can make informed decisions about saving for education and optimizing your tax strategy.

3. Understanding State-Specific 529 Plan Tax Benefits

State-specific 529 plan tax benefits vary significantly, making it essential to understand the rules in your state to maximize your savings. These benefits come in the form of either tax deductions or tax credits, each offering a different way to reduce your state income tax liability.

Tax Deductions vs. Tax Credits

- Tax Deduction: A tax deduction reduces your taxable income, lowering the amount subject to state income tax. The actual tax savings depend on your state’s income tax rate.

- Tax Credit: A tax credit directly reduces the amount of tax you owe to the state. A tax credit of $100, for example, reduces your tax bill by $100.

States with Tax Deductions

Many states offer a tax deduction for contributions to a 529 plan. Here’s a look at some examples:

| State | Deduction Limit (Single Filer) | Deduction Limit (Married Filing Jointly) | Notes |

|---|---|---|---|

| New York | $5,000 | $10,000 | |

| Ohio | Unlimited | Unlimited | |

| Pennsylvania | Unlimited | Unlimited | |

| Virginia | $4,000 | $8,000 | Limited to $4,000 per taxpayer, regardless of the number of 529 plans they own. |

| West Virginia | Unlimited | Unlimited | |

| South Carolina | Unlimited | Unlimited |

States with Tax Credits

Some states offer a tax credit instead of a deduction. Tax credits directly reduce the amount of tax you owe. Here are a few examples:

| State | Credit Details |

|---|---|

| Indiana | Offers a tax credit for 20% of contributions, up to a maximum credit of $1,000. |

| Utah | Provides a nonrefundable tax credit of 6% of contributions, with certain limits. |

| Vermont | Offers a 10% tax credit, up to $400 for single filers and $800 for joint filers |

Tax Parity States

Nine states offer a state income tax benefit for contributions to any 529 plan, not only in-state plans. These states are known as tax parity states and include:

- Arizona

- Arkansas

- Kansas

- Maine

- Minnesota

- Missouri

- Montana

- Ohio

- Pennsylvania

States Without Tax Benefits

Four states currently have a state income tax but do not offer a contribution deduction:

- California

- Hawaii

- Kentucky

- North Carolina

Maximizing State Tax Benefits

To take full advantage of state-specific 529 plan tax benefits:

- Know Your State’s Rules: Research the specific rules for your state, including deduction or credit limits and any other requirements.

- Contribute Strategically: Plan your contributions to maximize the tax benefits. If your state has a contribution limit, aim to contribute up to that limit each year.

- Consider Residency Requirements: Some states require you to be a resident to claim the tax benefits.

- Stay Informed: State tax laws can change, so stay updated on any changes that may affect your 529 plan.

By understanding the nuances of state-specific 529 plan tax benefits, you can optimize your savings strategy and reduce your overall tax liability.

4. What Are Qualified Education Expenses for 529 Plans?

Understanding what constitutes qualified education expenses for 529 plans is essential to ensure that withdrawals are tax-free. Qualified expenses include tuition, fees, books, supplies, and equipment required for enrollment or attendance at an eligible educational institution.

Eligible Educational Institutions

An eligible educational institution is any college, university, vocational school, or other post-secondary educational institution eligible to participate in the student aid programs administered by the U.S. Department of Education.

Qualified Expenses

Qualified education expenses include:

- Tuition and Fees: The costs for enrollment and attendance at an eligible educational institution.

- Books, Supplies, and Equipment: Required materials and equipment for courses.

- Room and Board: Expenses for housing and meals while attending school, provided the student is enrolled at least half-time.

- Special Needs Services: Expenses for special needs services for a special needs beneficiary.

- Computer Technology: The cost of a computer, related equipment, and internet access, if required by the educational institution.

- K-12 Tuition: Up to $10,000 per year per beneficiary for tuition at an elementary or secondary public, private, or religious school.

- Student Loan Repayments: Up to $10,000 lifetime limit per beneficiary for student loan repayments.

Examples of Qualified Education Expenses

- A student’s tuition bill at a four-year university

- The cost of textbooks and required course materials

- Room and board expenses for a student living on campus

- A computer required for coursework

- Tuition for a private high school

Non-Qualified Expenses

Non-qualified expenses are costs that do not qualify for tax-free withdrawals from a 529 plan. If you use 529 plan funds for non-qualified expenses, the earnings portion of the withdrawal will be subject to income tax and may also be subject to a 10% penalty. Non-qualified expenses include:

- Transportation costs

- Insurance

- Extracurricular activities

- Expenses not required for enrollment or attendance

Tracking Qualified Expenses

To ensure you’re using 529 plan funds for qualified expenses, it’s essential to keep detailed records of all expenses. This includes receipts, invoices, and any other documentation that supports the expense.

Using 529 Plans for K-12 Tuition

The Tax Cuts and Jobs Act of 2017 expanded the use of 529 plans to include K-12 tuition expenses. You can now withdraw up to $10,000 per year per beneficiary for tuition at an elementary or secondary public, private, or religious school.

Using 529 Plans for Student Loan Repayments

The SECURE Act of 2019 further expanded the use of 529 plans to include student loan repayments. You can now withdraw up to $10,000 lifetime limit per beneficiary for student loan repayments. This can be a valuable option for those looking to pay off student loans.

By understanding what constitutes qualified education expenses, you can maximize the tax benefits of your 529 plan and ensure that your withdrawals are tax-free.

5. How Do 529 Plans Affect Financial Aid Eligibility?

529 plans can affect financial aid eligibility, but the impact is generally minimal, especially when the plan is owned by a parent. The federal financial aid formula considers 529 plans as parental assets, which are assessed at a lower rate than student assets.

Federal Financial Aid Formula

The Free Application for Federal Student Aid (FAFSA) uses a formula to determine a student’s Expected Family Contribution (EFC). The EFC is an estimate of how much a student and their family can be expected to contribute to the cost of college for an academic year.

Impact of Parental Assets

When a 529 plan is owned by a parent, it is considered a parental asset. Parental assets are assessed at a rate of up to 5.64% in the financial aid formula. This means that only a small percentage of the value of the 529 plan will be considered available to pay for college.

Example:

If a 529 plan owned by a parent has a value of $10,000, only $564 (5.64% of $10,000) will be considered available to pay for college.

Impact of Student Assets

If a 529 plan is owned by the student, it is considered a student asset. Student assets are assessed at a much higher rate of 20% in the financial aid formula. This means that a larger percentage of the value of the 529 plan will be considered available to pay for college.

Example:

If a 529 plan is owned by the student and has a value of $10,000, $2,000 (20% of $10,000) will be considered available to pay for college.

Impact of Grandparent-Owned 529 Plans

If a 529 plan is owned by a grandparent or other third party, it is not reported as an asset on the FAFSA. However, withdrawals from a grandparent-owned 529 plan can be considered untaxed income to the student, which can reduce financial aid eligibility.

To avoid this issue, it’s generally recommended to delay withdrawals from a grandparent-owned 529 plan until after the student’s last year of college.

Strategies to Minimize Impact on Financial Aid

- Parental Ownership: Have the parent own the 529 plan to minimize the impact on financial aid eligibility.

- Delay Grandparent Withdrawals: Delay withdrawals from grandparent-owned 529 plans until after the student’s last year of college.

- Consider State Aid: Some states may have different rules regarding the treatment of 529 plans for state financial aid purposes.

- Consult a Financial Aid Expert: Seek advice from a financial aid expert to understand how 529 plans may affect your specific situation.

The Simplified FAFSA Form

The FAFSA Simplification Act, which went into effect in 2024-25, has made changes to the FAFSA form. One significant change is the elimination of the Expected Family Contribution (EFC). The FAFSA now calculates a Student Aid Index (SAI), which is a more accurate measure of a student’s ability to pay for college.

While the SAI is calculated differently than the EFC, the general principles regarding the treatment of 529 plans remain the same. Parental assets are assessed at a lower rate than student assets.

By understanding how 529 plans affect financial aid eligibility and implementing strategies to minimize the impact, you can effectively save for college while maximizing your financial aid opportunities.

6. Can You Roll Over a 529 Plan to a Different Beneficiary?

Yes, you can roll over a 529 plan to a different beneficiary, providing flexibility in how you use the funds. This feature is particularly useful if the original beneficiary decides not to attend college or receives a scholarship.

IRS Guidelines for Changing Beneficiaries

The IRS allows you to change the beneficiary of a 529 plan without penalty, as long as the new beneficiary is a member of the original beneficiary’s family. According to IRS Publication 970, family members include:

- A son or daughter, or a descendant of either

- A stepson or stepdaughter

- A brother, sister, stepbrother, or stepsister

- The father or mother, or an ancestor of either

- A stepfather or stepmother

- A son or daughter of a brother or sister

- A brother or sister of a father or mother

- A son-in-law, daughter-in-law, father-in-law, mother-in-law, brother-in-law, or sister-in-law

- The spouse of the beneficiary

How to Change the Beneficiary

To change the beneficiary of a 529 plan, follow these steps:

- Review Plan Rules: Check the specific rules of your 529 plan, as some plans may have additional requirements.

- Complete the Paperwork: Fill out the necessary paperwork to change the beneficiary. This typically involves providing information about the new beneficiary, such as their name, date of birth, and relationship to the original beneficiary.

- Submit the Request: Submit the completed paperwork to the 529 plan administrator.

- Confirmation: Wait for confirmation that the beneficiary has been successfully changed.

Tax Implications of Changing Beneficiaries

Changing the beneficiary of a 529 plan generally does not result in any tax consequences, as long as the new beneficiary is a member of the original beneficiary’s family. However, if you change the beneficiary to someone who is not a family member, the earnings portion of the account may be subject to income tax and a 10% penalty.

Using 529 Plans for Multiple Beneficiaries

You can also use a 529 plan for multiple beneficiaries by changing the beneficiary as needed. For example, if you have two children, you can initially set up a 529 plan for your older child and then change the beneficiary to your younger child once the older child has completed their education.

Rolling Over Funds to Another 529 Plan

In addition to changing the beneficiary, you can also roll over funds from one 529 plan to another. This can be useful if you want to switch to a plan with different investment options or lower fees. You can roll over funds once every 12 months without penalty.

Examples of Changing Beneficiaries

- A family sets up a 529 plan for their daughter, but she receives a full scholarship to college. They decide to change the beneficiary to their son, who is younger and will be attending college in a few years.

- A grandparent sets up a 529 plan for their grandchild, but the grandchild decides not to attend college. The grandparent changes the beneficiary to another grandchild who is planning to attend college.

- A parent sets up a 529 plan for their child, but the child decides to pursue a career that does not require a college degree. The parent changes the beneficiary to themselves and uses the funds to pay for continuing education courses.

By understanding the rules and guidelines for changing beneficiaries, you can maximize the flexibility of your 529 plan and ensure that the funds are used for education purposes.

7. Exploring the Impact of 529 Plans on Estate Planning

529 plans can be a valuable tool in estate planning, offering a way to transfer wealth while providing tax benefits and maintaining control over the assets. Contributions to a 529 plan can qualify as gifts under the annual gift tax exclusion, and the assets within the plan are not included in your taxable estate.

Gift Tax Exclusion

The annual gift tax exclusion allows you to give a certain amount of money to individuals each year without incurring gift tax. For 2024, the annual gift tax exclusion is $18,000 per individual. Contributions to a 529 plan can qualify as gifts under the annual gift tax exclusion, allowing you to reduce your estate tax liability.

Five-Year Election

You can also make a larger contribution to a 529 plan and elect to treat it as if it were made over a five-year period. This allows you to contribute up to five times the annual gift tax exclusion amount without incurring gift tax. For 2024, this means you could contribute up to $90,000 ($18,000 x 5) per beneficiary.

Control Over Assets

One of the key benefits of using 529 plans for estate planning is that you maintain control over the assets. As the account owner, you can decide how the funds are invested and who the beneficiary will be. This allows you to ensure that the funds are used for education purposes and to make changes as needed.

Avoiding Estate Taxes

The assets within a 529 plan are not included in your taxable estate, which can help reduce your estate tax liability. This can be particularly beneficial for high-net-worth individuals who are looking for ways to minimize estate taxes.

Examples of Using 529 Plans for Estate Planning

- A grandparent contributes $90,000 to a 529 plan for their grandchild and elects to treat it as if it were made over a five-year period. This allows them to reduce their estate tax liability while providing funds for their grandchild’s education.

- A parent contributes $18,000 each year to a 529 plan for their child. This allows them to take advantage of the annual gift tax exclusion and reduce their estate tax liability over time.

- An individual sets up a 529 plan for themselves and uses the funds to pay for continuing education courses. The assets within the 529 plan are not included in their taxable estate.

Consulting an Estate Planning Attorney

It’s important to consult with an estate planning attorney to determine how 529 plans can best be used in your estate plan. An estate planning attorney can help you understand the tax implications of 529 plans and ensure that your estate plan is properly structured.

By understanding the impact of 529 plans on estate planning, you can effectively transfer wealth while providing tax benefits and maintaining control over the assets.

8. What Are the Potential Risks and Downsides of 529 Plans?

While 529 plans offer numerous benefits, it’s essential to be aware of the potential risks and downsides. These include investment risks, potential penalties for non-qualified withdrawals, and the impact on financial aid eligibility.

Investment Risks

529 savings plans typically offer a range of investment options, including mutual funds, exchange-traded funds (ETFs), and target-date funds. These investments are subject to market risk, and the value of the account can fluctuate.

- Market Volatility: The value of your investments can decline due to market downturns.

- Inflation Risk: The purchasing power of your savings can be eroded by inflation.

- Interest Rate Risk: Changes in interest rates can affect the value of fixed-income investments.

Potential Penalties for Non-Qualified Withdrawals

If you use 529 plan funds for non-qualified expenses, the earnings portion of the withdrawal will be subject to income tax and may also be subject to a 10% penalty. Non-qualified expenses include expenses that are not required for enrollment or attendance at an eligible educational institution.

Impact on Financial Aid Eligibility

As discussed earlier, 529 plans can affect financial aid eligibility. While the impact is generally minimal, it’s important to be aware of how 529 plans are treated in the financial aid formula.

State Residency Requirements

Some states require you to be a resident to claim the state tax benefits of a 529 plan. If you move to another state, you may no longer be eligible for the tax benefits.

Fees and Expenses

529 plans can charge fees and expenses, such as annual maintenance fees, investment management fees, and administrative fees. These fees can reduce the overall return on your investment.

Limited Investment Options

529 plans typically offer a limited range of investment options. You may not be able to invest in the specific investments that you prefer.

Changing Beneficiaries

While you can change the beneficiary of a 529 plan, there are restrictions on who can be the new beneficiary. The new beneficiary must be a member of the original beneficiary’s family.

Examples of Potential Risks and Downsides

- A family invests in a 529 plan, but the market declines, and the value of the account decreases.

- An individual uses 529 plan funds for non-qualified expenses and incurs income tax and a 10% penalty.

- A family moves to another state and is no longer eligible for the state tax benefits of their 529 plan.

- An individual wants to invest in a specific investment, but it is not available in their 529 plan.

Mitigating the Risks

- Diversify Your Investments: Diversify your investments to reduce the risk of market volatility.

- Use Funds for Qualified Expenses: Use 529 plan funds only for qualified expenses to avoid penalties.

- Consider State Residency Requirements: Be aware of the state residency requirements of your 529 plan.

- Compare Fees and Expenses: Compare the fees and expenses of different 529 plans before investing.

- Consult a Financial Advisor: Consult a financial advisor to understand the risks and benefits of 529 plans.

By understanding the potential risks and downsides of 529 plans, you can make informed decisions and mitigate the risks.

9. How to Choose the Right 529 Plan for Your Needs

Choosing the right 529 plan for your needs is crucial to maximize the benefits and minimize the risks. Consider factors such as state tax benefits, investment options, fees, and ease of use.

State Tax Benefits

If your state offers a state income tax deduction or credit for 529 plan contributions, consider investing in your state’s 529 plan. This can provide significant tax savings.

Investment Options

Review the investment options offered by different 529 plans. Look for a plan that offers a range of investment options that align with your risk tolerance and investment goals.

Fees and Expenses

Compare the fees and expenses of different 529 plans. Look for a plan with low fees and expenses to maximize your return on investment.

Ease of Use

Choose a 529 plan that is easy to use and manage. Look for a plan with a user-friendly website and good customer service.

Performance

Review the historical performance of the investment options offered by different 529 plans. Look for a plan with a history of strong performance.

Age-Based Portfolios

Consider investing in a 529 plan that offers age-based portfolios. These portfolios automatically adjust the asset allocation as the beneficiary gets older, becoming more conservative over time.

Out-of-State Plans

Don’t limit yourself to your state’s 529 plan. Consider investing in an out-of-state plan if it offers better investment options, lower fees, or other benefits.

Examples of Choosing the Right 529 Plan

- A family lives in New York and wants to take advantage of the state income tax deduction. They invest in the New York 529 plan.

- An individual is risk-averse and wants to invest in a 529 plan with low fees and a conservative investment strategy. They invest in a 529 plan that offers a range of conservative investment options and low fees.

- A family wants to invest in a 529 plan with a wide range of investment options and a user-friendly website. They invest in a 529 plan that offers a variety of investment options and a user-friendly website.

Consulting a Financial Advisor

It’s important to consult with a financial advisor to determine which 529 plan is right for your needs. A financial advisor can help you understand the tax implications of 529 plans and choose a plan that aligns with your financial goals.

By considering these factors and consulting a financial advisor, you can choose the right 529 plan for your needs and maximize the benefits of saving for education.

10. What Are Some Alternatives to 529 Plans for Education Savings?

While 529 plans are a popular choice for education savings, there are several alternatives to consider. These include Coverdell ESAs, Roth IRAs, taxable investment accounts, and UGMA/UTMA accounts.

Coverdell Education Savings Accounts (ESAs)

Coverdell ESAs are another type of tax-advantaged savings account that can be used for education expenses. Unlike 529 plans, Coverdell ESAs can be used for elementary and secondary education expenses, as well as higher education expenses.

Roth IRAs

Roth IRAs are retirement savings accounts that offer tax-free growth and withdrawals. While Roth IRAs are primarily designed for retirement savings, you can withdraw contributions tax-free and penalty-free to pay for qualified education expenses.

Taxable Investment Accounts

Taxable investment accounts are brokerage accounts that are not tax-advantaged. While you won’t receive any tax benefits for contributing to a taxable investment account, you will have more flexibility in how you use the funds.

UGMA/UTMA Accounts

UGMA/UTMA accounts are custodial accounts that can be used to save for a child’s future expenses, including education. These accounts are owned by the child, but managed by a custodian until the child reaches the age of majority.

Examples of Using Alternatives to 529 Plans

- A family wants to save for elementary and secondary education expenses, as well as higher education expenses. They invest in a Coverdell ESA.

- An individual wants to save for retirement, but also wants the flexibility to use the funds for education expenses if needed. They invest in a Roth IRA.

- A family wants to save for college, but also wants the flexibility to use the funds for other purposes. They invest in a taxable investment account.

- A grandparent wants to save for their grandchild’s future expenses, but wants the child to own the account. They invest in a UGMA/UTMA account.

Comparing the Alternatives

| Account Type | Tax Benefits | Flexibility | Potential Drawbacks |

|---|---|---|---|

| 529 Plan | Tax-free growth and withdrawals for qualified expenses | Funds must be used for qualified education expenses | Investment options may be limited |

| Coverdell ESA | Tax-free growth and withdrawals for qualified expenses | Funds can be used for elementary, secondary, and higher education expenses | Contribution limits are lower than 529 plans |

| Roth IRA | Tax-free growth and withdrawals for qualified expenses | Contributions can be withdrawn tax-free and penalty-free for qualified expenses | Primarily designed for retirement savings |

| Taxable Account | No tax benefits | Funds can be used for any purpose | Earnings are subject to income tax |

| UGMA/UTMA Account | No tax benefits | Funds can be used for any purpose that benefits the child | Account is owned by the child, who gains control at the age of majority; can negatively impact financial aid more than 529s. |

Consulting a Financial Advisor

It’s important to consult with a financial advisor to determine which education savings option is right for your needs. A financial advisor can help you understand the tax implications of each option and choose the option that aligns with your financial goals.

By considering these alternatives and consulting a financial advisor, you can make informed decisions about saving for education.

At income-partners.net, we provide resources and guidance to help you navigate these financial decisions. Explore our website to discover more about strategic partnerships and financial planning for a brighter future. Our address is 1 University Station, Austin, TX 78712, United States. You can also reach us at +1 (512) 471-3434.

FAQs About 529 Plans and Taxable Income

Here are some frequently asked questions about 529 plans and their impact on taxable income:

- Do 529 Contributions Reduce State Taxable Income?

Yes, in many states, contributions to a 529 plan can reduce your state taxable income, depending on the specific state’s regulations. - Do You Get a Tax Deduction for Contributing to a 529 Plan?

While there’s no federal tax deduction, many states offer state income tax deductions for 529 plan contributions. - Which States Allow Tax Deductions for 529 Contributions?

Over 30 states offer tax deductions for 529 contributions; check our full list of state deductions and credits. - Can You Deduct Out-of-State 529 Contributions?

If you file state income taxes in one of the nine tax parity states, you may be able to claim a state tax deduction on out-of-state 529 plan contributions. - Are 529 Contributions Pre-Tax or Post-Tax?

529 contributions are made with post-tax dollars. - Are 529 Contributions Tax-Deductible for Grandparents?

Yes, in some states, 529 contributions may be tax-deductible for grandparents, although some states only allow the account holder to deduct contributions. - What Happens if I Withdraw Money for Non-Qualified Expenses?

The earnings portion of the withdrawal will be subject to income tax and may also be subject to a 10% penalty. - Can I Change the Beneficiary of a 529 Plan?

Yes, you can change the beneficiary to a family member without penalty.