Does 529 Contribution Reduce Taxable Income? Yes, in many states, contributing to a 529 plan can indeed lower your state taxable income, offering a valuable opportunity for tax savings and educational investment. Income-partners.net is here to guide you through the benefits of 529 plans, explore potential partnerships, and maximize your income through strategic savings. Let’s explore the power of tax-advantaged educational investments, strategic financial planning, and smart savings strategies.

1. Understanding 529 Plans and Their Tax Advantages

529 plans are designed to encourage saving for future education expenses, offering several tax benefits that can significantly impact your financial planning.

1.1. Federal Tax Benefits of 529 Plans

While there’s no federal income tax deduction for contributions to a 529 plan, the earnings grow federally tax-free. Moreover, these earnings are not subject to federal income tax when you take withdrawals for qualified education expenses. This includes up to $10,000 in K-12 tuition expenses and student loan payments.

1.2. State Tax Benefits for 529 Plans

Many states offer an income tax deduction or credit for 529 plan contributions when reporting income for state tax purposes. The income-partners.net platform details that, in most cases, you need to contribute to your own state’s plan to receive the tax benefit. This can provide substantial savings, depending on your state’s specific regulations and your contribution amount.

1.3. Key Insights from University Research

According to research from the University of Texas at Austin’s McCombs School of Business, strategic financial planning, including utilizing 529 plans, can significantly improve long-term financial outcomes for families.

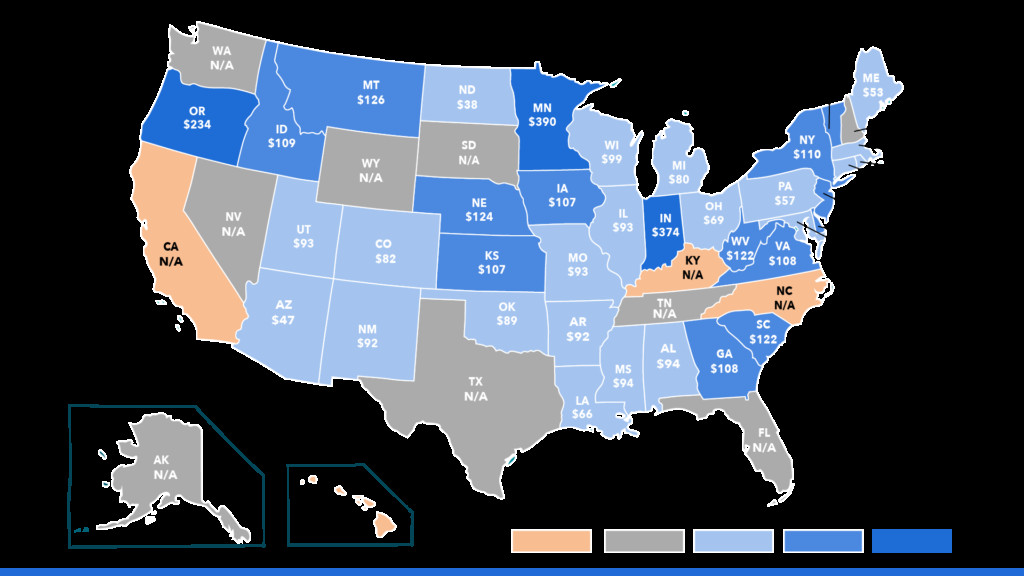

2. State-Specific Tax Benefits for 529 Contributions

Navigating the complex landscape of state tax benefits for 529 plans requires a detailed understanding of each state’s specific rules and regulations.

2.1. States Offering Income Tax Benefits

Most states with income taxes allow either a deduction from income or a state tax credit for 529 plan contributions. As highlighted by income-partners.net, nine tax parity states offer a state income tax benefit for contributions to any 529 plan, not just in-state plans. These states include Arizona, Arkansas, Kansas, Maine, Minnesota, Missouri, Montana, Ohio, and Pennsylvania.

2.2. States with Unique Tax Credit Systems

Several states, including Indiana, Oregon, Utah, and Vermont, offer a state income tax credit for 529 plan contributions. Unlike deductions, which reduce your taxable income, tax credits directly reduce the amount of tax you owe.

2.3. States Without Contribution Deductions

Four states—California, Hawaii, Kentucky, and North Carolina—currently have a state income tax but do not offer a contribution deduction for 529 plans.

3. Maximizing Your Tax Savings Through 529 Plans

To make the most of the tax advantages offered by 529 plans, it’s essential to understand the specific rules and limits set by your state.

3.1. Understanding Contribution Limits

While no annual contribution limits exist for 529 plans, most states limit the total contributions that qualify for an income tax credit or deduction. For example, New York residents can deduct up to $5,000 annually ($10,000 if married filing jointly).

3.2. Strategic Timing of Contributions

Most states require 529 plan contributions by December 31 to qualify for a state income tax benefit. However, some states offer a grace period, allowing contributions made in the following year to be applied to the prior tax year.

3.3. Leveraging the “Loophole”

Taxpayers can contribute to a 529 plan, immediately take a qualified distribution to pay for college or K-12 tuition, and still qualify for the state income tax benefit. However, some states, like Montana and Wisconsin, block this loophole by imposing time limits.

4. Who Can Claim the 529 Plan State Income Tax Benefit?

Understanding who is eligible to claim the state income tax benefit is crucial for effective financial planning.

4.1. Eligibility Criteria

States typically offer state income tax benefits to taxpayers who contribute to a 529 plan, including grandparents or other loved ones. However, some states only permit the account owner (or the account owner’s spouse) to claim the benefit.

4.2. Impact on Beneficiary’s Age

Eligible taxpayers may continue to claim a 529 plan state income tax benefit each year they contribute, regardless of the beneficiary’s age. This allows families to contribute throughout the child’s education years.

4.3. Grandparents and 529 Plans

Grandparents can significantly contribute to a grandchild’s education by utilizing 529 plans. This not only provides financial support but also offers potential tax benefits.

Grandparents giving gift to child

Grandparents giving gift to child

5. Choosing the Right 529 Plan: Beyond Tax Benefits

While state income tax benefits are a significant consideration, they shouldn’t be the only factor when choosing a 529 plan.

5.1. Assessing Fees and Performance

Attributes such as fees and investment performance must be considered before enrolling in a 529 plan. In some cases, the better investment performance of another state’s 529 plan can outweigh the benefits of a state income tax deduction.

5.2. Evaluating Plan Flexibility

Consider the flexibility of the 529 plan, including the ability to change beneficiaries and the range of investment options available.

5.3. Long-Term Growth Potential

Focus on the long-term growth potential of the 529 plan, ensuring it aligns with your financial goals and risk tolerance.

6. Real-World Examples of 529 Plan Tax Savings

Examining practical scenarios can illustrate the potential tax savings from 529 plan contributions.

6.1. Example 1: New York Residents

A married couple in New York contributing $10,000 annually to a 529 plan can deduct the full amount from their state income, resulting in significant tax savings.

6.2. Example 2: Tax Parity States

Residents of tax parity states like Pennsylvania can deduct contributions to any 529 plan, even those outside their state, providing greater flexibility and potential tax benefits.

6.3. Example 3: Indiana Residents

Indiana residents benefit from a state income tax credit, directly reducing their tax liability based on their 529 plan contributions.

7. Strategic Partnerships and Increased Income with Income-Partners.net

Income-partners.net offers unique opportunities to explore strategic partnerships that can further enhance your income and financial planning strategies.

7.1. Connecting with Financial Experts

Income-partners.net connects you with financial experts who can provide personalized advice on maximizing 529 plan benefits and other financial strategies.

7.2. Exploring Investment Opportunities

Discover investment opportunities that align with your financial goals, helping you grow your income and secure your financial future.

7.3. Building Strategic Alliances

Form strategic alliances with like-minded individuals and organizations to create synergistic financial opportunities.

8. The Role of Financial Planning in Maximizing 529 Plan Benefits

Financial planning is essential to maximize the tax benefits of 529 plans and ensure they align with your overall financial goals.

8.1. Setting Clear Financial Goals

Define your financial goals, including education savings targets, to guide your 529 plan contributions and investment strategies.

8.2. Consulting with Financial Advisors

Consult with financial advisors to develop a comprehensive financial plan that incorporates 529 plans and other tax-advantaged investment vehicles.

8.3. Regularly Reviewing Your Plan

Regularly review your financial plan and 529 plan performance to make necessary adjustments and ensure you stay on track to meet your goals.

9. Overcoming Challenges in Managing 529 Plans

Managing 529 plans can present several challenges, but with the right strategies, these can be effectively addressed.

9.1. Navigating State Regulations

Stay informed about the specific regulations and limits set by your state for 529 plan contributions and tax benefits. Income-partners.net offers resources to help you stay updated on these changes.

9.2. Balancing Investment Risk

Carefully balance investment risk within your 529 plan to ensure long-term growth while minimizing potential losses.

9.3. Addressing Unexpected Expenses

Plan for unexpected expenses and ensure you have sufficient funds outside your 529 plan to cover emergencies without jeopardizing your education savings.

10. Future Trends in 529 Plans and Education Savings

Staying informed about future trends in 529 plans and education savings can help you make informed decisions and maximize your financial benefits.

10.1. Potential Legislative Changes

Monitor potential legislative changes that may impact 529 plan benefits and regulations.

10.2. Innovative Investment Options

Explore innovative investment options within 529 plans to enhance growth potential and diversification.

10.3. Expanding Qualified Expenses

Stay updated on any expansions to the list of qualified education expenses that can be covered by 529 plans.

11. Integrating 529 Plans with Other Investment Strategies

To optimize your financial outcomes, it’s crucial to integrate 529 plans with your broader investment strategy.

11.1. Diversification

Ensure that your 529 plan aligns with your overall asset allocation strategy, contributing to a well-diversified portfolio.

11.2. Retirement Planning

Consider how 529 plans fit into your retirement planning strategy, ensuring they don’t detract from your retirement savings goals.

11.3. Estate Planning

Incorporate 529 plans into your estate planning to efficiently transfer wealth and support future generations’ education.

12. Leveraging Income-Partners.Net for Financial Success

Income-partners.net serves as a valuable resource for individuals seeking to maximize their financial opportunities through strategic partnerships and informed financial planning.

12.1. Access to Expert Advice

Benefit from access to expert financial advice and guidance through income-partners.net, helping you make informed decisions about 529 plans and other investments.

12.2. Networking Opportunities

Connect with other like-minded individuals and organizations through income-partners.net, fostering valuable partnerships and collaborations.

12.3. Comprehensive Resources

Utilize the comprehensive resources available on income-partners.net to stay informed about the latest trends and strategies in financial planning and investment.

13. Success Stories: How 529 Plans Have Impacted Families

Real-life success stories provide compelling evidence of the impact 529 plans can have on families’ financial futures.

13.1. The Smith Family

The Smith family utilized a 529 plan to save for their children’s college education, resulting in significant tax savings and reduced student loan debt.

13.2. The Johnson Family

The Johnson family leveraged a 529 plan to pay for their child’s K-12 tuition, taking advantage of state tax benefits and reducing their overall tax burden.

13.3. The Garcia Family

The Garcia family combined 529 plan savings with strategic financial planning to secure their children’s educational future and achieve their financial goals.

14. Common Mistakes to Avoid with 529 Plans

Avoiding common mistakes can help you maximize the benefits of your 529 plan and ensure you stay on track to meet your financial goals.

14.1. Not Starting Early

Starting early is crucial to maximizing the growth potential of your 529 plan. Don’t delay in establishing a plan and making regular contributions.

14.2. Ignoring Fees

Pay attention to the fees associated with your 529 plan and choose a plan with low fees to minimize costs and maximize returns.

14.3. Not Diversifying Investments

Diversify your investments within your 529 plan to reduce risk and enhance long-term growth potential.

15. The Importance of Early Planning and Consistent Contributions

Early planning and consistent contributions are key to unlocking the full potential of 529 plans.

15.1. Time Value of Money

Understand the time value of money and start saving early to take advantage of compounding returns.

15.2. Automate Contributions

Automate your 529 plan contributions to ensure consistency and avoid missing opportunities to save.

15.3. Adjust Contributions Over Time

Adjust your contributions over time as your income increases and your financial goals evolve.

16. Innovative Strategies for Maximizing 529 Plan Growth

Exploring innovative strategies can help you maximize the growth potential of your 529 plan and achieve your financial objectives.

16.1. Utilizing Ugma/Utma Transfers

Transfer funds from UGMA/UTMA accounts to 529 plans to take advantage of tax benefits and secure funds for education.

16.2. Incorporating 529 Plans into Estate Planning

Incorporate 529 plans into your estate planning to efficiently transfer wealth and support future generations’ education.

16.3. Leveraging Gift Tax Exclusions

Leverage gift tax exclusions to make tax-free contributions to 529 plans and maximize your savings potential.

17. Building a Financial Legacy Through Education Savings

Education savings through 529 plans can contribute to building a lasting financial legacy for future generations.

17.1. Breaking the Cycle of Debt

Help future generations avoid the burden of student loan debt by providing them with a strong foundation of education savings.

17.2. Promoting Financial Literacy

Promote financial literacy among family members by involving them in the 529 plan savings process.

17.3. Creating Opportunities

Create opportunities for future generations to pursue their educational and career aspirations by providing them with the resources they need to succeed.

18. How to Evaluate the Performance of Your 529 Plan

Regularly evaluating the performance of your 529 plan is crucial to ensuring it aligns with your financial goals.

18.1. Tracking Investment Returns

Monitor the investment returns of your 529 plan and compare them to benchmarks to assess performance.

18.2. Reviewing Asset Allocation

Review your asset allocation to ensure it aligns with your risk tolerance and financial goals.

18.3. Making Adjustments as Needed

Make adjustments to your investment strategy and contribution levels as needed to stay on track to meet your education savings goals.

19. The Future of 529 Plans: What to Expect

Staying informed about the future of 529 plans can help you make informed decisions and maximize your financial benefits.

19.1. Potential Legislative Changes

Monitor potential legislative changes that may impact 529 plan benefits and regulations.

19.2. Expanding Qualified Expenses

Stay updated on any expansions to the list of qualified education expenses that can be covered by 529 plans.

19.3. Innovative Investment Options

Explore innovative investment options within 529 plans to enhance growth potential and diversification.

20. Connecting with Partners for Financial Growth on Income-Partners.Net

Income-partners.net provides a platform for connecting with partners who can help you achieve your financial goals and maximize the benefits of 529 plans.

20.1. Finding Financial Advisors

Connect with experienced financial advisors who can provide personalized advice and guidance on 529 plans and other investments.

20.2. Networking with Other Investors

Network with other investors to share insights, strategies, and opportunities for financial growth.

20.3. Building Strategic Alliances

Form strategic alliances with like-minded individuals and organizations to create synergistic financial opportunities.

By understanding the intricacies of 529 plans and their tax benefits, leveraging strategic partnerships through income-partners.net, and implementing sound financial planning strategies, you can secure your financial future and provide valuable opportunities for future generations.

21. Understanding the Tax Implications of 529 Plan Withdrawals

While contributions to 529 plans can offer state tax benefits, it’s equally important to understand the tax implications of withdrawals.

21.1. Qualified vs. Non-Qualified Withdrawals

Distinguish between qualified withdrawals, which are tax-free when used for eligible education expenses, and non-qualified withdrawals, which may be subject to income tax and a 10% penalty on the earnings portion.

21.2. Eligible Education Expenses

Familiarize yourself with the range of eligible education expenses that qualify for tax-free withdrawals, including tuition, fees, books, supplies, and room and board.

21.3. Documentation and Record-Keeping

Maintain thorough documentation and records of all contributions, withdrawals, and eligible education expenses to ensure compliance with tax regulations.

22. Integrating 529 Plans with Estate Planning Strategies

Effectively integrating 529 plans with your estate planning strategy can provide additional tax benefits and ensure your assets are distributed according to your wishes.

22.1. Gifting Strategies

Utilize gifting strategies to make tax-free contributions to 529 plans, reducing your estate tax liability while supporting future generations’ education.

22.2. Control and Ownership

Consider the control and ownership of 529 plans within your estate plan, ensuring your assets are managed and distributed according to your wishes.

22.3. Beneficiary Designations

Review and update beneficiary designations regularly to ensure your 529 plans are aligned with your estate planning goals.

23. Addressing Common Misconceptions About 529 Plans

Addressing common misconceptions about 529 plans can help individuals make informed decisions and maximize the benefits of these valuable savings vehicles.

23.1. Impact on Financial Aid

Understand the impact of 529 plans on financial aid eligibility and how to strategically manage your assets to minimize any potential negative effects.

23.2. Investment Options

Explore the wide range of investment options available within 529 plans and choose investments that align with your risk tolerance and financial goals.

23.3. Flexibility and Control

Recognize the flexibility and control you have over your 529 plan, including the ability to change beneficiaries and investment options as needed.

24. Partnering with Financial Professionals for 529 Plan Success

Collaborating with experienced financial professionals can provide valuable insights and guidance to maximize the benefits of your 529 plan.

24.1. Tax Planning Strategies

Work with tax professionals to develop tax-efficient strategies for contributing to and withdrawing from 529 plans.

24.2. Investment Management

Partner with investment advisors to manage your 529 plan assets and optimize returns based on your risk tolerance and financial goals.

24.3. Financial Planning

Collaborate with financial planners to integrate 529 plans into your overall financial plan and ensure they align with your long-term objectives.

25. Leveraging Income-Partners.Net to Find 529 Plan Experts

Income-partners.net offers a valuable platform for connecting with financial professionals who can provide expert guidance on 529 plans and other financial matters.

25.1. Access to a Network of Professionals

Access a network of experienced financial advisors, tax professionals, and investment managers through income-partners.net.

25.2. Verified Credentials

Ensure you’re working with qualified professionals by verifying their credentials and experience on income-partners.net.

25.3. Customized Solutions

Find professionals who can provide customized solutions tailored to your specific financial needs and goals on income-partners.net.

Alt text: A couple discussing financial planning, highlighting the importance of expert advice and strategic savings strategies.

26. Case Studies: Real-Life Examples of 529 Plan Success Stories

Exploring real-life case studies can provide valuable insights into how 529 plans have helped families achieve their education savings goals.

26.1. The Davis Family

The Davis family utilized a 529 plan to save for their children’s college education, resulting in significant tax savings and reduced student loan debt.

26.2. The Garcia Family

The Garcia family leveraged a 529 plan to pay for their child’s K-12 tuition, taking advantage of state tax benefits and reducing their overall tax burden.

26.3. The Lee Family

The Lee family combined 529 plan savings with strategic financial planning to secure their children’s educational future and achieve their financial goals.

27. Maximizing the Benefits of 529 Plans for Different Educational Needs

529 plans can be utilized for a wide range of educational needs, including K-12 tuition, college expenses, and vocational training.

27.1. K-12 Tuition

Utilize 529 plans to pay for K-12 tuition expenses at private or religious schools, taking advantage of state tax benefits and reducing your overall tax burden.

27.2. College Expenses

Utilize 529 plans to pay for college tuition, fees, books, supplies, and room and board, ensuring your children have the resources they need to succeed in higher education.

27.3. Vocational Training

Utilize 529 plans to pay for vocational training programs, providing individuals with the skills and knowledge they need to pursue their career aspirations.

28. Integrating 529 Plans with Other Savings and Investment Vehicles

Effectively integrating 529 plans with other savings and investment vehicles can help you achieve your overall financial goals.

28.1. Retirement Savings

Coordinate your 529 plan contributions with your retirement savings strategy, ensuring you’re adequately preparing for both education and retirement expenses.

28.2. Emergency Funds

Maintain an adequate emergency fund to cover unexpected expenses, allowing you to avoid withdrawing from your 529 plan and potentially incurring penalties.

28.3. Investment Portfolios

Integrate 529 plans into your overall investment portfolio, diversifying your assets and optimizing returns based on your risk tolerance and financial goals.

29. Exploring the Impact of State Residency on 529 Plan Benefits

Your state of residency can significantly impact the tax benefits and investment options available to you through 529 plans.

29.1. State Tax Deductions

Understand the state tax deductions and credits available to you based on your residency and choose a 529 plan that maximizes your tax savings.

29.2. In-State vs. Out-of-State Plans

Compare in-state and out-of-state 529 plans, considering factors such as fees, investment options, and historical performance.

29.3. Tax Parity States

If you reside in a tax parity state, explore the benefits of contributing to any 529 plan, regardless of its location, to maximize your tax savings and investment opportunities.

30. Future Trends in Education Savings and the Role of 529 Plans

Staying informed about future trends in education savings can help you make informed decisions and maximize the benefits of 529 plans.

30.1. Legislative Changes

Monitor potential legislative changes that may impact 529 plan benefits and regulations.

30.2. Expanding Qualified Expenses

Stay updated on any expansions to the list of qualified education expenses that can be covered by 529 plans.

30.3. Innovative Investment Options

Explore innovative investment options within 529 plans to enhance growth potential and diversification.

Ready to unlock the full potential of 529 plans and build a brighter financial future? Visit income-partners.net today to connect with financial experts, explore partnership opportunities, and start your journey towards education savings success! Address: 1 University Station, Austin, TX 78712, United States. Phone: +1 (512) 471-3434. Website: income-partners.net.

FAQ: 529 Plan Contribution and Taxable Income

1. Do 529 contributions reduce federal taxable income?

No, contributions to a 529 plan are not deductible on your federal income tax return. However, the earnings grow federally tax-free, and withdrawals for qualified education expenses are also tax-free.

2. Do 529 contributions reduce state taxable income?

Yes, many states offer a state income tax deduction or credit for contributions to a 529 plan. The specific rules and limits vary by state, so check with your state’s tax agency for details.

3. Which states allow tax deductions for 529 contributions?

More than 30 states, including Washington, D.C., offer a state income tax deduction or credit for contributions to a 529 plan. However, the specific rules and limits vary by state.

4. Can you deduct out-of-state 529 contributions?

In most cases, you’ll need to contribute to your own state’s plan to receive the state tax benefit. However, nine tax parity states offer a state income tax benefit for contributions to any 529 plan, not just in-state plans.

5. Are 529 contributions pre-tax or post-tax?

529 contributions are made with post-tax dollars. While there is no federal income tax deduction for contributions, many states offer a state income tax deduction or credit.

6. Are 529 contributions tax-deductible for grandparents?

Yes, some states allow grandparents or other loved ones who contribute to a 529 plan to claim a state income tax benefit. However, some states only permit the account holder to deduct contributions.

7. What are qualified education expenses for 529 plans?

Qualified education expenses include tuition, fees, books, supplies, and equipment required for enrollment or attendance at an eligible educational institution. They can also include room and board if the beneficiary is enrolled at least half-time.

8. What happens if I use 529 plan funds for non-qualified expenses?

If you use 529 plan funds for non-qualified expenses, the earnings portion of the withdrawal will be subject to income tax and a 10% penalty.

9. How do I report 529 plan contributions and withdrawals on my tax return?

You’ll need to report 529 plan contributions and withdrawals on your state tax return if you’re claiming a state income tax deduction or credit. You’ll also need to report any non-qualified withdrawals on your federal income tax return.

10. Can I change the beneficiary of a 529 plan?

Yes, you can change the beneficiary of a 529 plan to another eligible family member, such as a sibling, parent, or niece/nephew, without incurring any tax penalties.