Do You Have To Report Cash Income On Taxes? Absolutely, reporting all income, including cash, is a must for compliance and to avoid penalties, and income-partners.net can help you navigate these financial waters. Freelancers and independent contractors should include cash payments as part of their self-employment income on Schedule C, and by claiming business write-offs, you can significantly reduce your taxable income. Let income-partners.net guide you through the process, offering resources to help you understand self-employment tax, optimize your financial strategy, and connect with valuable partnership opportunities, ensuring you are well-informed and positioned for financial success.

1. Understanding the Obligation to Report Cash Income

Do you have to report cash income on taxes? Yes, you absolutely must report all cash income on your taxes. It’s a common misconception that if you don’t receive a 1099 form, you’re off the hook, but the IRS considers cash payments as part of your taxable self-employment income. Reporting all income, including cash, ensures compliance, helps avoid penalties, and allows you to claim eligible business write-offs to reduce your taxable income.

Even if you are a freelancer or independent contractor getting paid in cash, you’re still required to report it. The IRS doesn’t differentiate between income types; all earnings are subject to taxation. According to the IRS, failing to report income can lead to significant penalties, including fines and interest on the unpaid taxes.

1.1. The Importance of Reporting All Income

The significance of reporting every dollar you earn, regardless of how you receive it, cannot be overstated. Honesty and accuracy in tax reporting are essential for several reasons:

- Legal Compliance: It ensures you are meeting your legal obligations as a taxpayer.

- Avoiding Penalties: It helps you avoid penalties, fines, and legal issues with the IRS.

- Financial Transparency: It provides a clear and transparent financial record, which is crucial for future financial planning and creditworthiness.

- Eligibility for Benefits: Accurate income reporting can affect your eligibility for certain government benefits and programs.

1.2. Real-World Consequences of Non-Compliance

Non-compliance with tax laws can lead to serious repercussions. For example, underreporting income can result in an audit, where the IRS scrutinizes your financial records. If discrepancies are found, you may be required to pay back taxes, penalties, and interest. In severe cases, tax evasion can lead to criminal charges. According to a study by the Tax Policy Center, the “tax gap” (the difference between taxes owed and taxes paid) is substantial, with unreported income being a significant contributor.

1.3. How Income-Partners.Net Can Help

Income-partners.net offers resources and expertise to help you stay compliant with tax laws while optimizing your income. We provide:

- Educational Materials: Clear and concise guides on tax regulations and reporting requirements.

- Financial Tools: Calculators and templates to help you track your income and expenses accurately.

- Partnership Opportunities: Connections with businesses and professionals who can provide further financial guidance and support.

By leveraging the resources at income-partners.net, you can ensure you are reporting your cash income correctly, minimizing your tax liability, and maximizing your financial opportunities.

2. Identifying Tax Forms for Reporting Income

Do you have to report cash income on taxes? Yes, and you will typically report it on Schedule C as part of your self-employment income. Unlike traditional employees who receive a W-2 form, self-employed individuals, including freelancers and small business owners, often receive Form 1099-NEC for payments of $600 or more. However, even without a 1099-NEC, you are still required to report all income, including cash, to the IRS.

Navigating the world of tax forms can be daunting, especially for self-employed individuals. Understanding which forms to use and how to fill them out accurately is crucial for compliance and minimizing tax liabilities.

2.1. Understanding Form 1099-NEC

Form 1099-NEC (Nonemployee Compensation) is used to report payments made to independent contractors, freelancers, and other self-employed individuals. If you receive $600 or more from a client or payer during the tax year, they are required to send you a 1099-NEC. This form includes:

- Payer Information: The name, address, and Taxpayer Identification Number (TIN) of the entity that paid you.

- Recipient Information: Your name, address, and TIN.

- Total Payments: The total amount of compensation you received for your services.

However, it’s important to note that even if you don’t receive a 1099-NEC, you are still obligated to report all income you earned.

2.2. Schedule C: Profit or Loss From Business

Schedule C is the form used to report the income and expenses from your business or self-employment. It is attached to your individual income tax return (Form 1040). Key sections of Schedule C include:

- Income: This section is where you report your gross receipts or sales, including all cash income.

- Expenses: You can deduct various business expenses to reduce your taxable income. Common deductions include:

- Advertising

- Car and truck expenses

- Contract labor

- Depreciation

- Home office

- Insurance

- Legal and professional fees

- Office expenses

- Supplies

- Travel

- Net Profit or Loss: This is your total income minus your total expenses. This amount is then transferred to your Form 1040.

2.3. Additional Relevant Tax Forms

Depending on your specific situation, you may need to use other tax forms as well:

- Schedule SE (Self-Employment Tax): Used to calculate the self-employment tax you owe on your net profit from Schedule C.

- Form 8829 (Expenses for Business Use of Your Home): Used to calculate the deductible expenses for the business use of your home.

- Form 4562 (Depreciation and Amortization): Used to claim depreciation expenses for business assets.

2.4. Maximizing Financial Opportunities with Income-Partners.Net

Income-partners.net provides a suite of resources to help you navigate these tax forms and optimize your financial strategy:

- Detailed Guides: Step-by-step instructions on how to fill out each form accurately.

- Expense Tracking Tools: Templates and software recommendations to help you keep track of your business expenses.

- Professional Network: Access to a network of financial advisors and tax professionals who can provide personalized guidance.

- Partnership Opportunities: Connections with businesses and individuals who can help you grow your income and expand your business.

By leveraging these resources, you can confidently manage your tax obligations and focus on maximizing your financial potential.

3. What To Do With Self-Employment Income Not Reported On a 1099

Do you have to report cash income on taxes? Yes, even if you don’t receive a 1099 form. The IRS requires you to report all self-employment income, including cash, regardless of whether it’s reported on a 1099-NEC or not. Failing to report this income can lead to penalties and interest.

Many freelancers and independent contractors mistakenly believe that if they don’t receive a 1099 form, they don’t need to report the income. However, the IRS has made it clear that all income, including cash, must be reported.

3.1. The IRS Stance on Unreported Income

The IRS expects you to report all income you earn, whether or not you receive a 1099 form. The 1099-NEC is simply an informational document that helps the IRS track income. Even if you don’t receive this form, you are still responsible for accurately reporting your earnings. According to IRS Publication 334, “Tax Guide for Small Business,” you must report all income from whatever source derived, including cash, property, and services.

3.2. Why Report Income Even Without a 1099?

There are several compelling reasons to report all income, even if you don’t receive a 1099 form:

- Legal Compliance: It ensures you are meeting your legal obligations as a taxpayer.

- Avoiding Penalties: It helps you avoid penalties, fines, and legal issues with the IRS.

- Building a Financial Record: It provides a clear and transparent financial record, which is crucial for future financial planning and creditworthiness.

- Qualifying for Loans: Lenders often require proof of income when you apply for loans. Reporting all income can help you qualify for better loan terms.

3.3. Best Practices for Tracking Unreported Income

To accurately report income that is not reported on a 1099, it’s essential to keep detailed records of all your earnings. Here are some best practices:

- Maintain a Detailed Ledger: Keep a log of all cash income, including the date, source, and amount.

- Use Accounting Software: Consider using accounting software like QuickBooks or FreshBooks to track your income and expenses.

- Keep Bank Statements: Regularly review your bank statements to ensure all deposits are accounted for.

- Save Receipts: Save receipts for all business-related expenses to maximize your deductions.

3.4. Income-Partners.Net: Your Resource for Financial Success

Income-partners.net offers a comprehensive suite of resources to help you manage and report your income effectively:

- Income Tracking Tools: Templates and software recommendations to help you keep track of all income sources.

- Expert Financial Advice: Access to a network of financial advisors and tax professionals who can provide personalized guidance.

- Partnership Opportunities: Connections with businesses and individuals who can help you grow your income and expand your business.

By utilizing the resources available at income-partners.net, you can confidently navigate the complexities of self-employment income reporting, ensuring you are compliant with tax laws and maximizing your financial opportunities.

4. Keeping Track of Your Cash Income

Do you have to report cash income on taxes? Yes, and keeping accurate records of your cash income is essential for tax compliance. Without proper tracking, it’s easy to forget the exact amounts you’ve earned, leading to potential underreporting.

Tracking cash income can be challenging, especially for those who receive frequent cash payments. However, with the right strategies and tools, you can maintain accurate records and simplify the tax reporting process.

4.1. Why Tracking Cash Income Is Crucial

Accurate tracking of cash income is essential for several reasons:

- Tax Compliance: It ensures you report all income to the IRS, avoiding potential penalties and fines.

- Financial Planning: It provides a clear picture of your earnings, helping you make informed financial decisions.

- Business Management: It allows you to monitor the performance of your business and identify areas for improvement.

- Audit Preparedness: In the event of an IRS audit, detailed records of your cash income will be invaluable.

4.2. Effective Methods for Tracking Cash Income

Here are some effective methods for tracking cash income:

- Maintain a Cash Log: Keep a detailed log of all cash payments, including the date, source, amount, and purpose of the payment.

- Use a Spreadsheet: Create a spreadsheet to record your cash income. Include columns for the date, source, amount, and any relevant notes.

- Utilize Accounting Software: Use accounting software like QuickBooks or FreshBooks to track your income and expenses. These programs offer features for recording cash transactions and generating financial reports.

- Mobile Apps: There are several mobile apps designed to help you track your income and expenses on the go. These apps allow you to enter cash transactions quickly and easily.

- Bank Deposits: Deposit cash payments into your business bank account regularly. This creates a record of your cash income and makes it easier to reconcile your records.

4.3. Tips for Accurate Record-Keeping

To ensure your cash income records are accurate, follow these tips:

- Record Transactions Immediately: Don’t wait until the end of the day or week to record your cash income. Record each transaction as soon as it occurs to minimize the risk of forgetting.

- Be Detailed: Include as much detail as possible in your records. Note the date, source, amount, and purpose of each payment.

- Reconcile Regularly: Reconcile your cash income records with your bank statements and other financial documents regularly. This will help you identify and correct any discrepancies.

- Keep Supporting Documentation: Save receipts and other supporting documentation for all cash transactions. This will provide additional evidence in the event of an audit.

4.4. How Income-Partners.Net Supports Accurate Tracking

Income-partners.net is committed to helping you maintain accurate records of your cash income and optimize your financial strategy. Our resources include:

- Tracking Templates: Downloadable templates for tracking your cash income in a spreadsheet or log.

- Software Recommendations: Reviews and recommendations of accounting software and mobile apps that can help you manage your finances.

- Expert Advice: Access to a network of financial advisors and tax professionals who can provide personalized guidance on record-keeping and tax compliance.

- Partnership Opportunities: Connections with businesses and individuals who can help you grow your income and expand your business.

By leveraging the tools and resources available at income-partners.net, you can confidently track your cash income, ensure tax compliance, and make informed financial decisions.

5. Reporting Cash Income

Do you have to report cash income on taxes? Yes, and reporting it correctly involves including it with your gross receipts on Schedule C. This form calculates your business’s profit or loss, and accurately reporting cash income is crucial for determining your taxable income.

Reporting cash income accurately is a critical part of tax compliance for self-employed individuals. The process involves including your cash income with your other earnings on the appropriate tax forms and accurately calculating your taxable income.

5.1. Key Steps in Reporting Cash Income

Here are the key steps involved in reporting cash income:

- Calculate Total Cash Income: Add up all the cash payments you received during the tax year. Use your cash log, spreadsheet, or accounting software to ensure you have an accurate total.

- Complete Schedule C: Fill out Schedule C, “Profit or Loss From Business (Sole Proprietorship),” to report your business income and expenses.

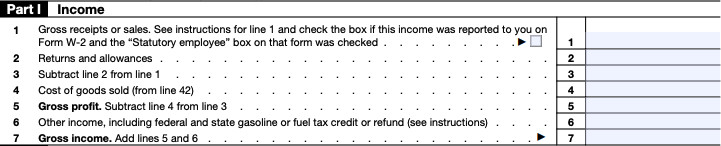

- Report Gross Receipts: On line 1 of Schedule C, enter your total gross receipts or sales. This should include all income you received from your business, including cash payments.

- Deduct Business Expenses: Deduct any eligible business expenses from your gross receipts to calculate your net profit or loss. Common business expenses include:

- Advertising

- Car and truck expenses

- Contract labor

- Depreciation

- Home office

- Insurance

- Legal and professional fees

- Office expenses

- Supplies

- Travel

- Transfer Net Profit or Loss: Transfer the net profit or loss from Schedule C to your individual income tax return (Form 1040).

How to Report Cash Income Without a 1099 | Part I of Schedule C for self-employment income

How to Report Cash Income Without a 1099 | Part I of Schedule C for self-employment income

5.2. Common Mistakes to Avoid

When reporting cash income, it’s essential to avoid common mistakes that can lead to errors and potential penalties. Here are some mistakes to watch out for:

- Underreporting Income: Failing to report all cash income is a common mistake. Be sure to include all payments you received, regardless of the amount or source.

- Incorrectly Classifying Expenses: Make sure you correctly classify your business expenses. Deductible expenses must be ordinary and necessary for your business.

- Missing Deductions: Don’t miss out on eligible deductions. Review the list of common business expenses and make sure you’re claiming all the deductions you’re entitled to.

- Math Errors: Double-check your calculations to ensure your numbers are accurate. Math errors can lead to incorrect tax liabilities and potential penalties.

5.3. Pro Tips for Accurate Reporting

To ensure you report your cash income accurately, follow these pro tips:

- Keep Detailed Records: Maintain detailed records of all cash payments and business expenses. This will make it easier to complete your tax forms accurately.

- Reconcile Regularly: Reconcile your cash income records with your bank statements and other financial documents regularly. This will help you identify and correct any discrepancies.

- Seek Professional Advice: If you’re unsure about how to report your cash income or claim business expenses, seek advice from a qualified tax professional.

5.4. Income-Partners.Net: Your Partner in Tax Compliance

Income-partners.net is dedicated to providing the resources and support you need to confidently report your cash income and optimize your tax strategy. Our offerings include:

- Detailed Guides: Step-by-step guides on how to complete Schedule C and other relevant tax forms.

- Expense Tracking Tools: Templates and software recommendations to help you keep track of your business expenses.

- Professional Network: Access to a network of financial advisors and tax professionals who can provide personalized guidance.

- Partnership Opportunities: Connections with businesses and individuals who can help you grow your income and expand your business.

By leveraging these resources, you can ensure you are reporting your cash income correctly, minimizing your tax liability, and maximizing your financial opportunities.

6. Lowering Your Tax Bill After Reporting Cash Income

Do you have to report cash income on taxes? Yes, but you can also lower your tax bill by claiming all eligible business write-offs. By deducting legitimate business expenses, you reduce your taxable income, which means you pay less in taxes.

Reporting cash income may seem daunting, but there are legal and effective ways to lower your tax bill. Claiming business write-offs is a key strategy for reducing your taxable income and paying less to the IRS.

6.1. Understanding Business Write-Offs

Business write-offs, also known as tax deductions, are expenses you incur while running your business that can be deducted from your gross income. By deducting these expenses, you reduce your taxable income, which ultimately lowers your tax bill. According to the IRS, business expenses must be both ordinary and necessary to be deductible.

6.2. Common Business Write-Offs

Here are some common business write-offs that self-employed individuals can claim:

- Home Office Deduction: If you use a portion of your home exclusively and regularly for business, you may be able to deduct expenses related to that space, such as rent, mortgage interest, utilities, and insurance.

- Car and Truck Expenses: You can deduct the actual expenses of operating your vehicle for business purposes, such as gas, oil, repairs, and insurance, or take the standard mileage rate.

- Supplies: You can deduct the cost of supplies you use in your business, such as office supplies, tools, and materials.

- Advertising: You can deduct the cost of advertising your business, such as online ads, print ads, and business cards.

- Contract Labor: If you hire independent contractors for your business, you can deduct the payments you make to them.

- Education: You can deduct expenses for education that maintains or improves your skills in your current business, but not education that qualifies you for a new business.

- Insurance: You can deduct the cost of business insurance, such as liability insurance, property insurance, and workers’ compensation insurance.

- Legal and Professional Fees: You can deduct fees you pay to attorneys, accountants, and other professionals for services related to your business.

Sign up for tax university- Keepertax

Sign up for tax university- Keepertax

6.3. Strategies for Maximizing Write-Offs

To maximize your business write-offs, follow these strategies:

- Keep Detailed Records: Maintain detailed records of all your business expenses, including receipts, invoices, and bank statements.

- Track Expenses Regularly: Track your expenses regularly throughout the year. This will make it easier to identify all your eligible write-offs when it’s time to file your taxes.

- Consult a Tax Professional: Work with a qualified tax professional who can help you identify all the write-offs you’re entitled to and ensure you’re claiming them correctly.

- Use Accounting Software: Use accounting software like QuickBooks or FreshBooks to track your income and expenses. These programs can help you categorize your expenses and generate reports for tax time.

6.4. Income-Partners.Net: Your Partner in Tax Optimization

Income-partners.net is committed to helping you optimize your tax strategy and lower your tax bill. Our resources include:

- Write-Off Guides: Detailed guides on common business write-offs and how to claim them.

- Expense Tracking Tools: Templates and software recommendations to help you keep track of your business expenses.

- Professional Network: Access to a network of financial advisors and tax professionals who can provide personalized guidance.

- Partnership Opportunities: Connections with businesses and individuals who can help you grow your income and expand your business.

By leveraging these resources, you can ensure you are claiming all the business write-offs you’re entitled to, lowering your tax bill, and maximizing your financial opportunities.

7. Consequences of Not Reporting Cash Income

Do you have to report cash income on taxes? Yes, absolutely, and failing to do so can lead to significant penalties and legal issues. The IRS takes unreported income seriously, and the consequences of non-compliance can be severe.

While it may be tempting to avoid reporting cash income, the consequences of doing so far outweigh any perceived benefits. The IRS has the authority to impose penalties, fines, and even criminal charges for failing to report income accurately.

7.1. Potential Penalties and Fines

If you fail to report all your cash income, you may be subject to the following penalties and fines:

- Accuracy-Related Penalty: This penalty applies if you understate your income due to negligence or intentional disregard of the rules. The penalty is typically 20% of the underpayment.

- Failure-to-File Penalty: This penalty applies if you don’t file your tax return by the due date (including extensions). The penalty is typically 5% of the unpaid taxes for each month or part of a month that your return is late, up to a maximum of 25%.

- Failure-to-Pay Penalty: This penalty applies if you don’t pay your taxes by the due date. The penalty is typically 0.5% of the unpaid taxes for each month or part of a month that the taxes remain unpaid, up to a maximum of 25%.

- Interest: The IRS charges interest on underpayments of taxes. The interest rate is determined quarterly and is typically based on the federal short-term rate plus 3 percentage points.

7.2. Risk of an IRS Audit

Failing to report all your cash income can increase your risk of an IRS audit. The IRS uses various methods to identify taxpayers who may be underreporting their income, including:

- Data Matching: The IRS compares the information reported on your tax return with information reported by third parties, such as banks, employers, and other businesses.

- Statistical Analysis: The IRS uses statistical models to identify tax returns that are likely to contain errors or underreported income.

- Informant Tips: The IRS receives tips from individuals who suspect that someone is not reporting their income accurately.

If your tax return is selected for an audit, the IRS will review your financial records and may request additional information to verify your income and expenses. If the IRS finds that you have underreported your income, you may be required to pay back taxes, penalties, and interest.

7.3. Criminal Charges for Tax Evasion

In severe cases, failing to report cash income can lead to criminal charges for tax evasion. Tax evasion is the intentional attempt to avoid paying taxes. Examples of tax evasion include:

- Underreporting income

- Hiding assets

- Filing a false tax return

If you are convicted of tax evasion, you may be subject to fines, imprisonment, and a criminal record.

7.4. Income-Partners.Net: Your Ally in Tax Compliance

Income-partners.net is dedicated to helping you stay compliant with tax laws and avoid the consequences of not reporting cash income. Our resources include:

- Tax Compliance Guides: Detailed guides on how to report your income accurately and avoid common mistakes.

- Professional Network: Access to a network of financial advisors and tax professionals who can provide personalized guidance.

- Partnership Opportunities: Connections with businesses and individuals who can help you grow your income and expand your business.

By leveraging these resources, you can ensure you are reporting your cash income correctly, minimizing your risk of penalties and fines, and staying on the right side of the law.

8. Addressing Concerns About Past Years’ Unreported Income

Do you have to report cash income on taxes? Yes, even if it’s from previous years. If you discover that you failed to report cash income in past years, it’s essential to take corrective action to mitigate potential penalties and legal issues.

Discovering that you’ve failed to report cash income in previous years can be stressful, but it’s important to address the issue proactively. The IRS has procedures in place to allow taxpayers to correct past errors and come into compliance with tax laws.

8.1. The Importance of Correcting Past Errors

Correcting past errors is essential for several reasons:

- Avoiding Penalties: The IRS may impose penalties for underreporting income in previous years. By correcting your errors, you can potentially reduce or eliminate these penalties.

- Minimizing Interest: The IRS charges interest on underpayments of taxes. By correcting your errors promptly, you can minimize the amount of interest you owe.

- Reducing Audit Risk: Correcting your errors can reduce your risk of an IRS audit. The IRS is more likely to audit taxpayers who have a history of underreporting income.

- Maintaining Compliance: Correcting your errors demonstrates your commitment to complying with tax laws. This can help you avoid future legal issues.

8.2. Options for Correcting Past Errors

There are several options for correcting past errors on your tax return:

- Amended Return: You can file an amended tax return (Form 1040-X) to correct errors on a previously filed return. An amended return allows you to report additional income, claim additional deductions, or correct other mistakes.

- Voluntary Disclosure: If you have intentionally failed to report income in past years, you may be able to participate in the IRS’s Voluntary Disclosure Program. This program allows you to come forward voluntarily and disclose your unreported income in exchange for a reduced risk of criminal prosecution.

- Payment Plan: If you owe additional taxes, penalties, and interest as a result of correcting your errors, you may be able to set up a payment plan with the IRS. A payment plan allows you to pay your tax liability in installments over a period of time.

8.3. Steps to Take When Correcting Past Errors

Here are the steps you should take when correcting past errors on your tax return:

- Gather Your Records: Gather all the records you need to accurately determine the amount of unreported income and any additional deductions you may be entitled to.

- Consult a Tax Professional: Work with a qualified tax professional who can help you determine the best course of action and prepare your amended tax return or voluntary disclosure.

- File an Amended Return: If you choose to file an amended return, complete Form 1040-X and attach any supporting documentation.

- Submit Payment: If you owe additional taxes, penalties, and interest, submit payment with your amended return or set up a payment plan with the IRS.

8.4. Income-Partners.Net: Your Resource for Correcting Past Errors

Income-partners.net is dedicated to helping you correct past errors on your tax return and come into compliance with tax laws. Our resources include:

- Tax Resolution Guides: Detailed guides on how to file an amended tax return and participate in the IRS’s Voluntary Disclosure Program.

- Professional Network: Access to a network of financial advisors and tax professionals who can provide personalized guidance.

- Partnership Opportunities: Connections with businesses and individuals who can help you grow your income and expand your business.

By leveraging these resources, you can take proactive steps to correct past errors, minimize your risk of penalties and fines, and ensure you are in compliance with tax laws.

9. Frequently Asked Questions (FAQs) About Reporting Cash Income on Taxes

Do you have to report cash income on taxes? This is a common question, and here are some other frequently asked questions about reporting cash income on taxes to help clarify the process.

Understanding the nuances of reporting cash income on taxes can be challenging. Here are some frequently asked questions to provide clarity and guidance.

9.1. Common Questions and Answers

Q1: Do I have to report cash income if I don’t receive a 1099 form?

A: Yes, you must report all cash income, regardless of whether you receive a 1099 form. The IRS requires you to report all income, including cash, from any source.

Q2: What if I only earned a small amount of cash income?

A: You are still required to report all cash income, even if it’s a small amount. There is no minimum threshold for reporting income.

Q3: What form do I use to report cash income?

A: You report cash income on Schedule C, “Profit or Loss From Business (Sole Proprietorship),” which is attached to your individual income tax return (Form 1040).

Q4: Can I deduct business expenses to reduce my taxable cash income?

A: Yes, you can deduct ordinary and necessary business expenses from your gross cash income to calculate your net profit or loss.

Q5: What happens if I fail to report cash income?

A: Failing to report cash income can result in penalties, fines, and even criminal charges. The IRS takes unreported income seriously.

Q6: How far back can the IRS audit my tax return?

A: The IRS generally has three years from the date you filed your return to audit it. However, in cases of fraud or substantial underreporting of income, the IRS can audit your return for longer periods.

Q7: What should I do if I made a mistake on my tax return?

A: If you discover that you made a mistake on your tax return, you can file an amended tax return (Form 1040-X) to correct the error.

Q8: Can I get help with my taxes?

A: Yes, you can get help with your taxes from a qualified tax professional or through resources like income-partners.net.

Q9: What records should I keep to track my cash income?

A: You should keep a detailed log of all cash payments, including the date, source, amount, and purpose of the payment.

Q10: Is there a penalty for paying taxes late?

A: Yes, the IRS charges a penalty for failing to pay your taxes by the due date. The penalty is typically 0.5% of the unpaid taxes for each month or part of a month that the taxes remain unpaid, up to a maximum of 25%.

9.2. Income-Partners.Net: Your Go-To Resource for Tax Information

Income-partners.net offers a wealth of information and resources to help you navigate the complexities of reporting cash income on taxes. Our website provides:

- Detailed Guides: Step-by-step guides on how to report your income accurately and avoid common mistakes.

- Tax Tips: Practical tips for minimizing your tax liability and maximizing your deductions.

- Professional Network: Access to a network of financial advisors and tax professionals who can provide personalized guidance.

- Partnership Opportunities: Connections with businesses and individuals who can help you grow your income and expand your business.

By utilizing these resources, you can confidently manage your tax obligations, minimize your risk of penalties and fines, and maximize your financial opportunities.

10. Leveraging Income-Partners.Net for Your Financial Success

Do you have to report cash income on taxes? Yes, and income-partners.net is here to help you not only understand your tax obligations but also to find opportunities for growth and financial success.

Income-partners.net is more than just a resource for tax information; it’s a platform designed to connect you with opportunities, strategies, and professionals that can help you achieve your financial goals.

10.1. Exploring Partnership Opportunities

Income-partners.net offers a unique opportunity to connect with potential partners who can help you grow your income and expand your business. Whether you’re looking for:

- Strategic Alliances: Partnering with complementary businesses to reach new markets and customers.

- Joint Ventures: Collaborating on projects or ventures to share resources and expertise.

- Referral Partnerships: Exchanging referrals with other businesses to generate new leads and sales.

Income-partners.net can help you find the right partners to achieve your business objectives.

10.2. Accessing Expert Advice and Guidance

Income-partners.net provides access to a network of financial advisors, tax professionals, and business consultants who can provide personalized guidance on a wide range of financial topics. Whether you need help with:

- Tax Planning: Developing a tax strategy to minimize your tax liability and maximize your deductions.

- Financial Planning: Creating a financial plan to achieve your long-term financial goals.

- Business Consulting: Getting advice on how to start, grow, or manage your business effectively.

Income-partners.net can connect you with the experts you need to succeed.

10.3. Utilizing Educational Resources and Tools

Income-partners.net offers a variety of educational resources and tools to help you improve your financial literacy and make informed decisions. Our resources include:

- Articles and Guides: Detailed articles and guides on tax planning, financial management, and business growth.

- Calculators and Tools: Interactive calculators and tools to help you estimate your tax liability, track your expenses, and plan for your financial future.

- Webinars and Workshops: Live webinars and workshops on a variety of financial topics.

10.4. Call to Action: Start Your Journey to Financial Success Today

Ready to take control of your finances and achieve your business goals? Visit income-partners.net today to:

- Explore Partnership Opportunities: Connect with potential partners who can help you grow your income and expand your business.

- Access Expert Advice: Get personalized guidance from financial advisors, tax professionals, and business consultants.

- Utilize Educational Resources: Improve your financial literacy and make informed decisions.

Don’t wait any longer. Start your journey to financial success with income-partners.net today!

Understanding your tax obligations, especially when it comes to reporting cash income, is crucial for financial health and legal compliance. income-partners.net provides the resources, expertise, and connections you need to navigate the complexities of tax reporting, maximize your financial opportunities, and build a successful business.