Do I Need To Report Cash Income? Yes, you absolutely need to report cash income. As a freelancer, independent contractor, or small business owner, understanding your tax obligations is essential for financial health and peace of mind. At income-partners.net, we guide you through the nuances of reporting cash income, ensuring you stay compliant and maximize your income potential through strategic partnerships. Let’s explore the process of reporting cash earnings, managing self-employment taxes, and leveraging business deductions to optimize your financial strategy and explore lucrative partnership opportunities.

1. Understanding the Obligation to Report Cash Income

The IRS requires all income, including cash payments, to be reported, regardless of whether you receive a 1099 form. Reporting all income ensures compliance and helps you avoid penalties. Let’s delve deeper into why this is so important.

1.1. The IRS Stance on Cash Income

The IRS considers cash payments as taxable income, just like any other form of payment. It’s crucial to understand that receiving payment in cash does not exempt you from your tax obligations. According to the IRS, all income is subject to tax unless specifically excluded by law.

1.2. Why Reporting Cash Income Matters

Reporting cash income is vital for several reasons:

- Compliance: It ensures you are following tax laws and regulations.

- Avoiding Penalties: Failure to report income can lead to significant penalties, including fines and interest.

- Building Financial Credibility: Accurate income reporting helps in building a reliable financial history, which is essential for loans, mortgages, and other financial products.

- Accessing Opportunities: Demonstrating a history of reliable income can open doors to various partnership and investment opportunities, highlighting the benefits available on income-partners.net.

1.3. Real-World Consequences of Non-Reporting

Failing to report cash income can lead to serious legal and financial repercussions. The IRS has sophisticated methods for detecting unreported income, including data matching and audits. Penalties for non-compliance can include:

- Accuracy-Related Penalties: These can be as high as 20% of the underpaid tax.

- Fraud Penalties: In severe cases, civil fraud penalties can amount to 75% of the underpaid tax.

- Criminal Charges: Intentional failure to report income can result in criminal charges, including imprisonment.

1.4. Legal Framework Supporting Reporting

The legal basis for reporting all income, including cash, is rooted in the Internal Revenue Code. Section 61 of the IRC defines gross income as “all income from whatever source derived,” which includes cash payments. The Supreme Court has consistently upheld this broad definition of income, reinforcing the obligation to report all earnings.

2. Identifying Income Types That Need Reporting

Knowing what types of income to report is as important as knowing why. Here’s a breakdown of the income types you should always include.

2.1. Self-Employment Income

Self-employment income includes any money you earn as an independent contractor, freelancer, or small business owner. This encompasses payments for services, goods, and any other form of compensation you receive.

2.2. Gig Economy Earnings

With the rise of the gig economy, many individuals earn income through platforms like Uber, Airbnb, and TaskRabbit. All earnings from these sources, whether paid in cash or electronically, are taxable and must be reported.

2.3. Tips and Gratuities

Tips and gratuities are a significant part of income for many service industry workers. The IRS requires that all tips, including those received in cash, be reported as income. Maintaining a daily log of tips can help ensure accurate reporting.

2.4. Rental Income

If you own rental property, the income you receive from rent payments is taxable. This includes cash payments from tenants. Keep detailed records of all rental income and expenses to accurately report your earnings and claim any eligible deductions.

2.5. Bartering Income

Bartering, which involves exchanging goods or services without using money, also results in taxable income. The fair market value of the goods or services you receive in a barter transaction is considered income and must be reported.

2.6. Interest and Dividends

Interest earned from savings accounts and dividends received from investments are taxable income. Financial institutions typically report this income to the IRS on Form 1099-INT or 1099-DIV, making it easy to track and report.

2.7. Other Miscellaneous Income

Various other forms of income may need to be reported, such as royalties, prizes, and awards. Any income that is not specifically excluded by the IRS should be included on your tax return.

3. Methods for Tracking Cash Income Effectively

Tracking cash income might seem daunting, but with the right methods, it can be straightforward.

3.1. Maintaining a Detailed Cash Log

Keeping a detailed cash log is one of the most effective ways to track your cash income. This log should include:

- Date: The date you received the payment.

- Source: The name of the client or customer.

- Description: A brief description of the service or product provided.

- Amount: The amount of cash received.

This log can be kept in a physical notebook or using digital tools like spreadsheets or accounting software.

3.2. Using Spreadsheet Software

Spreadsheet software like Microsoft Excel or Google Sheets can be used to create a digital cash log. These tools allow you to easily organize and analyze your income data. You can create columns for date, source, description, and amount, and use formulas to calculate totals and subtotals.

3.3. Leveraging Accounting Software

Accounting software like QuickBooks Self-Employed or FreshBooks can automate the process of tracking your cash income. These tools allow you to record transactions, categorize expenses, and generate reports, making it easier to manage your finances and prepare your tax return.

3.4. Mobile Apps for Tracking Income

Several mobile apps are designed specifically for tracking income and expenses. Apps like Keeper and Hurdlr allow you to record transactions on the go, track mileage, and generate tax reports. These apps can be particularly useful for freelancers and gig workers who need to track income from multiple sources.

3.5. Bank Deposits and Reconciliations

Regularly depositing cash into your bank account can help you track your income. By reconciling your bank statements with your cash log, you can ensure that all income is accounted for. This also provides a verifiable record of your earnings in case of an audit.

3.6. Staying Organized

According to research from the University of Texas at Austin’s McCombs School of Business, in July 2025, organized record-keeping significantly reduces stress during tax season. Implement these simple tips for staying organized:

- Keep all receipts and invoices in one place.

- Set aside time each week to record your cash income.

- Back up your digital records regularly.

3.7. Benefits of Consistent Tracking

Consistent and accurate tracking of your cash income offers numerous benefits:

- Accurate Tax Reporting: It ensures that you report the correct amount of income on your tax return.

- Informed Financial Decisions: It provides you with a clear picture of your income and expenses, allowing you to make informed financial decisions.

- Audit Preparedness: It prepares you for a potential IRS audit by providing verifiable records of your income.

- Identifying Trends: Detailed tracking helps identify income trends, allowing you to optimize your business strategies and explore new partnership opportunities on income-partners.net.

Tracking Cash Income with Excel Spreadsheet

Tracking Cash Income with Excel Spreadsheet

4. Reporting Cash Income on Your Tax Return

Reporting your cash income accurately on your tax return is crucial for compliance and avoiding penalties. Here’s how to do it.

4.1. Schedule C: Profit or Loss from Business

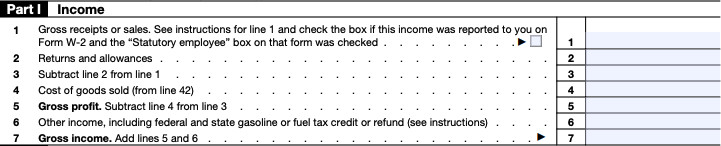

The primary form for reporting self-employment income, including cash income, is Schedule C (Form 1040), Profit or Loss from Business. This form is used to calculate your business’s profit or loss by subtracting your business expenses from your gross income.

4.2. Completing Line 1: Gross Receipts or Sales

On Line 1 of Schedule C, you will enter your gross receipts or sales. This includes all income you received from your business, including cash payments. Make sure to include all income, even if you didn’t receive a 1099 form.

4.3. Example of Reporting Cash Income

Let’s say you earned $10,000 from freelance work, including $2,000 in cash payments. On Line 1 of Schedule C, you would enter $10,000 as your gross receipts or sales. This reflects the total income you received from your business, regardless of the payment method.

4.4. Claiming Business Expenses

After reporting your gross income, you can deduct your business expenses to reduce your taxable income. Common business expenses include:

- Office Supplies: Expenses for pens, paper, and other office supplies.

- Home Office Deduction: A deduction for the portion of your home used exclusively for business.

- Travel Expenses: Costs for travel related to your business, including transportation, lodging, and meals.

- Advertising and Marketing: Expenses for advertising your business and marketing your products or services.

- Professional Fees: Fees paid to accountants, lawyers, and other professionals.

4.5. Calculating Net Profit or Loss

After deducting your business expenses from your gross income, you will arrive at your net profit or loss. This is the amount that will be subject to self-employment tax and income tax. Enter your net profit or loss on Line 31 of Schedule C.

4.6. Schedule SE: Self-Employment Tax

If your net profit from self-employment is $400 or more, you will also need to file Schedule SE (Form 1040), Self-Employment Tax. This form is used to calculate the amount of self-employment tax you owe, which includes Social Security and Medicare taxes.

4.7. Paying Estimated Taxes

As a self-employed individual, you are generally required to pay estimated taxes quarterly. This involves estimating your income and tax liability for the year and making payments to the IRS on a quarterly basis. Failing to pay estimated taxes can result in penalties.

4.8. Using Tax Software for Accuracy

Tax software like TurboTax or H&R Block can help you accurately report your cash income and calculate your tax liability. These tools guide you through the process of completing Schedule C and Schedule SE, and they can also help you identify eligible deductions and credits.

5. Strategies to Minimize Your Tax Liability Legally

Minimizing your tax liability is a smart financial strategy. Here’s how to do it legally and ethically.

5.1. Maximizing Deductible Business Expenses

One of the most effective ways to reduce your tax liability is by maximizing your deductible business expenses. Keep detailed records of all your expenses and make sure to claim every deduction you are eligible for.

5.2. Home Office Deduction

If you use a portion of your home exclusively and regularly for business, you may be able to claim the home office deduction. This deduction allows you to deduct expenses related to your home, such as rent, mortgage interest, utilities, and insurance, based on the percentage of your home used for business.

5.3. Vehicle Expenses

If you use your vehicle for business purposes, you can deduct your vehicle expenses. You can choose to deduct your actual expenses, such as gas, oil, and repairs, or you can use the standard mileage rate, which is set by the IRS each year.

5.4. Health Insurance Deduction

Self-employed individuals can deduct the amount they paid for health insurance premiums. This deduction is available even if you don’t itemize your deductions.

5.5. Retirement Contributions

Contributing to a retirement plan, such as a SEP IRA or a Solo 401(k), can help you reduce your tax liability. Contributions to these plans are tax-deductible, which can lower your taxable income.

5.6. Qualified Business Income (QBI) Deduction

The QBI deduction allows eligible self-employed individuals to deduct up to 20% of their qualified business income. This deduction can significantly reduce your tax liability.

5.7. Education and Training Expenses

Expenses for education and training that improve your skills or help you maintain your professional license can be deductible. These expenses can include tuition, books, and other related costs.

5.8. Strategic Timing of Income and Expenses

You may be able to reduce your tax liability by strategically timing your income and expenses. For example, you can defer income to a later year or accelerate expenses to the current year, depending on your tax situation.

5.9. Seeking Professional Advice

A tax professional can provide personalized advice on how to minimize your tax liability based on your specific circumstances. They can help you identify eligible deductions and credits, and they can also help you navigate complex tax laws and regulations.

5.10. Financial Planning

According to Harvard Business Review, effective financial planning is key to long-term financial health and tax optimization. Here’s how to plan for your financial future:

- Set financial goals.

- Create a budget and stick to it.

- Review your financial plan regularly.

6. Consequences of Not Reporting Cash Income

Failing to report cash income can lead to severe consequences. It’s crucial to understand these risks to ensure compliance.

6.1. IRS Audits

The IRS conducts audits to verify the accuracy of tax returns. If you fail to report cash income, you are at risk of being audited. The IRS uses various methods to detect unreported income, including data matching and statistical analysis.

6.2. Penalties for Underreporting Income

If the IRS determines that you have underreported your income, you may be subject to penalties. These penalties can include:

- Accuracy-Related Penalty: This penalty is typically 20% of the underpaid tax.

- Fraud Penalty: If the IRS determines that you intentionally failed to report income, you may be subject to a fraud penalty, which can be as high as 75% of the underpaid tax.

- Late Filing Penalty: If you fail to file your tax return on time, you may be subject to a late filing penalty, which is typically 5% of the unpaid tax for each month or part of a month that your return is late, up to a maximum of 25%.

- Late Payment Penalty: If you fail to pay your taxes on time, you may be subject to a late payment penalty, which is typically 0.5% of the unpaid tax for each month or part of a month that your payment is late, up to a maximum of 25%.

6.3. Interest Charges

In addition to penalties, the IRS charges interest on underpaid taxes. The interest rate is determined quarterly and is typically based on the federal short-term rate plus 3 percentage points.

6.4. Criminal Charges

In severe cases, failing to report cash income can result in criminal charges. Tax evasion is a federal crime that can result in imprisonment and significant fines.

6.5. Impact on Credit and Financial Standing

Failing to comply with tax laws can negatively impact your credit and financial standing. Tax liens and unpaid tax debts can appear on your credit report, making it difficult to obtain loans, mortgages, and other financial products.

6.6. State Tax Consequences

In addition to federal tax consequences, failing to report cash income can also result in state tax consequences. Many states have their own income tax laws, and failing to comply with these laws can result in penalties and interest charges.

6.7. Statute of Limitations

The IRS generally has three years from the date you file your tax return to audit it. However, if you substantially underreport your income, the IRS has six years to audit your return. In cases of fraud, there is no statute of limitations, meaning the IRS can audit your return at any time.

6.8. Importance of Voluntary Disclosure

If you have failed to report cash income in the past, it is important to take steps to correct the error. You can file an amended tax return to report the unreported income and pay any additional taxes and interest owed. In some cases, you may be able to avoid penalties by making a voluntary disclosure to the IRS.

7. Navigating 1099 Forms and Cash Income Reporting

Understanding how 1099 forms interact with cash income is crucial for accurate tax reporting.

7.1. What is a 1099 Form?

A 1099 form is an information return that reports income paid to independent contractors, freelancers, and other non-employees. There are several types of 1099 forms, including:

- 1099-NEC: Reports non-employee compensation, such as payments for services performed as an independent contractor.

- 1099-MISC: Reports miscellaneous income, such as rent, royalties, and prizes.

- 1099-K: Reports payments processed through third-party payment networks, such as PayPal and credit card processors.

7.2. When You Receive a 1099 Form

You will typically receive a 1099 form if you were paid $600 or more during the tax year. The payer is required to send you a copy of the form by January 31 of the following year.

7.3. What to Do If You Don’t Receive a 1099 Form

Even if you don’t receive a 1099 form, you are still required to report all of your income, including cash payments. The IRS requires you to report all income, regardless of whether you receive an information return.

7.4. Reconciling 1099 Forms with Your Records

When preparing your tax return, it is important to reconcile your 1099 forms with your own records. Make sure that the income reported on the 1099 forms matches the income you have recorded in your cash log or accounting software.

7.5. Reporting Income Not on a 1099 Form

If you have income that is not reported on a 1099 form, you will still need to report it on your tax return. Include this income in your gross receipts or sales on Schedule C.

7.6. Handling Discrepancies

If you find a discrepancy between the income reported on a 1099 form and your own records, contact the payer to request a corrected form. If you are unable to resolve the discrepancy, you should report the income based on your own records and include an explanation with your tax return.

7.7. Avoiding Common Mistakes

Common mistakes to avoid when reporting income on 1099 forms include:

- Failing to report all income.

- Incorrectly reporting income.

- Claiming ineligible deductions.

- Failing to keep adequate records.

7.8. Resources for Understanding 1099 Forms

The IRS provides numerous resources for understanding 1099 forms and reporting income. These resources include publications, FAQs, and online tools. You can also consult with a tax professional for assistance.

8. Utilizing Income-Partners.net for Partnership Opportunities

Now that you understand your tax obligations, let’s explore how income-partners.net can help you grow your income through strategic partnerships.

8.1. Finding Strategic Partners

income-partners.net is designed to connect you with potential partners who can help you expand your business and increase your revenue. Whether you’re looking for a marketing partner, a distributor, or an investor, you can find them on our platform.

8.2. Types of Partnerships Available

We offer a variety of partnership opportunities to suit your needs, including:

- Joint Ventures: Collaborate with another business on a specific project or venture.

- Strategic Alliances: Form a long-term partnership with another business to achieve common goals.

- Distribution Partnerships: Partner with a distributor to expand your reach and sell your products or services to a wider audience.

- Referral Partnerships: Partner with other businesses to refer customers to each other.

8.3. Benefits of Partnering

Partnering with other businesses can offer numerous benefits, including:

- Increased Revenue: Expand your reach and generate more sales.

- Access to New Markets: Enter new markets and reach new customers.

- Shared Resources: Share resources and reduce costs.

- Increased Expertise: Access new skills and expertise.

- Enhanced Brand Awareness: Increase your brand awareness and build your reputation.

8.4. How to Get Started on Income-Partners.net

Getting started on income-partners.net is easy. Simply create an account, complete your profile, and start browsing partnership opportunities. You can also use our search filters to find partners who match your specific criteria.

8.5. Building Successful Partnerships

To build successful partnerships, it is important to:

- Define Your Goals: Clearly define your goals and objectives for the partnership.

- Find the Right Partner: Choose a partner who shares your values and has complementary skills and expertise.

- Establish Clear Roles and Responsibilities: Clearly define the roles and responsibilities of each partner.

- Communicate Effectively: Communicate regularly and openly with your partner.

- Monitor and Evaluate Progress: Monitor and evaluate the progress of the partnership and make adjustments as needed.

8.6. Success Stories

Many businesses have successfully increased their income through strategic partnerships facilitated by platforms like income-partners.net. These success stories highlight the potential for growth and revenue generation through collaboration.

8.7. Maximizing Your Partnership Potential

To maximize your partnership potential on income-partners.net, it is important to:

- Create a Compelling Profile: Showcase your skills, expertise, and accomplishments.

- Be Proactive: Reach out to potential partners and initiate conversations.

- Be Open to New Ideas: Be open to new ideas and opportunities.

- Be Patient: Building successful partnerships takes time and effort.

- Provide Value: Focus on providing value to your partners and building mutually beneficial relationships.

Strategic Business Partnerships for Increased Revenue

Strategic Business Partnerships for Increased Revenue

9. Keeping Accurate Records for Tax Purposes

Accurate record-keeping is essential for tax compliance and financial management. Here’s how to maintain thorough records.

9.1. Importance of Record-Keeping

Keeping accurate records is crucial for several reasons:

- Accurate Tax Reporting: It ensures that you report the correct amount of income and expenses on your tax return.

- Audit Preparedness: It prepares you for a potential IRS audit by providing verifiable records of your income and expenses.

- Informed Financial Decisions: It provides you with a clear picture of your financial situation, allowing you to make informed decisions.

- Business Management: Detailed records help you track your business performance, identify trends, and make strategic decisions.

9.2. Types of Records to Keep

You should keep records of all income and expenses related to your business, including:

- Income Records: Cash logs, bank statements, 1099 forms, invoices, and receipts.

- Expense Records: Receipts, invoices, bank statements, credit card statements, and mileage logs.

- Asset Records: Records of purchases and sales of assets, such as equipment and vehicles.

- Liability Records: Records of debts and loans.

9.3. How Long to Keep Records

The IRS recommends that you keep your tax records for at least three years from the date you filed your return or two years from the date you paid the tax, whichever is later. However, you may need to keep records for longer if you filed an amended return or if you are claiming a loss.

9.4. Best Practices for Record-Keeping

To maintain accurate records, follow these best practices:

- Keep Records Organized: Organize your records in a systematic way, such as by date, category, or client.

- Store Records Securely: Store your records in a safe and secure location, such as a locked filing cabinet or a password-protected computer.

- Back Up Records Regularly: Back up your digital records regularly to protect against data loss.

- Use Accounting Software: Use accounting software to automate the process of tracking your income and expenses.

- Scan and Digitize Records: Scan and digitize your paper records to create electronic copies.

- Reconcile Records Regularly: Reconcile your records with your bank statements and credit card statements on a regular basis.

9.5. Using Technology for Efficient Record-Keeping

Technology can help you streamline the process of record-keeping and improve accuracy. Consider using these tools:

- Accounting Software: QuickBooks, FreshBooks, and Xero.

- Expense Tracking Apps: Keeper, Expensify, and Shoeboxed.

- Document Scanning Apps: CamScanner and Adobe Scan.

- Cloud Storage: Google Drive, Dropbox, and OneDrive.

9.6. Addressing Common Record-Keeping Challenges

Common record-keeping challenges include:

- Losing Receipts

- Forgetting to Record Transactions

- Mixing Business and Personal Expenses

- Falling Behind on Record-Keeping

To overcome these challenges, make record-keeping a regular habit, use technology to automate the process, and seek help from a professional if needed.

9.7. Resources for Record-Keeping Guidance

The IRS provides numerous resources for record-keeping guidance, including publications, FAQs, and online tools. You can also consult with a tax professional for assistance.

10. Frequently Asked Questions (FAQs) About Reporting Cash Income

Here are some frequently asked questions about reporting cash income to help clarify any remaining doubts.

10.1. Do I need to report cash income if I don’t receive a 1099 form?

Yes, you must report all income, including cash, regardless of whether you receive a 1099 form.

10.2. What form do I use to report cash income?

You report cash income on Schedule C (Form 1040), Profit or Loss from Business.

10.3. What happens if I don’t report my cash income?

Failing to report cash income can result in penalties, interest charges, and even criminal charges.

10.4. How should I track my cash income?

Maintain a detailed cash log, use spreadsheet software, or leverage accounting software to track your cash income effectively.

10.5. Can I deduct business expenses to reduce my tax liability?

Yes, you can deduct eligible business expenses to reduce your taxable income.

10.6. What is the home office deduction?

The home office deduction allows you to deduct expenses related to the portion of your home used exclusively and regularly for business.

10.7. How can income-partners.net help me increase my income?

income-partners.net connects you with potential partners who can help you expand your business and increase your revenue.

10.8. What are the benefits of partnering with other businesses?

Partnering can increase revenue, provide access to new markets, share resources, and enhance brand awareness.

10.9. How long should I keep my tax records?

The IRS recommends keeping your tax records for at least three years from the date you filed your return or two years from the date you paid the tax, whichever is later.

10.10. Where can I find more information about reporting cash income?

The IRS provides numerous resources, including publications, FAQs, and online tools. You can also consult with a tax professional.

In conclusion, reporting cash income is a crucial part of being a responsible freelancer, independent contractor, or business owner. By understanding your obligations, tracking your income effectively, and leveraging resources like income-partners.net, you can ensure compliance, minimize your tax liability, and maximize your income potential through strategic partnerships.

Ready to take your income to the next level? Visit income-partners.net today to discover partnership opportunities, learn strategies for building successful relationships, and connect with potential partners who can help you achieve your business goals. Don’t miss out on the chance to grow your income and build a thriving business with the support of a strong network of partners.