Are you wondering, “Do I Need Critical Illness And Income Protection insurance?” Absolutely, you should explore these options! At income-partners.net, we believe that securing your financial future involves considering comprehensive protection against life’s uncertainties through strategic income partnership. Discover how these protections can safeguard your revenue streams and partnerships, bolstering your overall financial health and providing peace of mind. Let’s delve into how these plans ensure financial stability, strategic partnerships and revenue protection.

1. Understanding the Basics: Critical Illness Cover and Income Protection

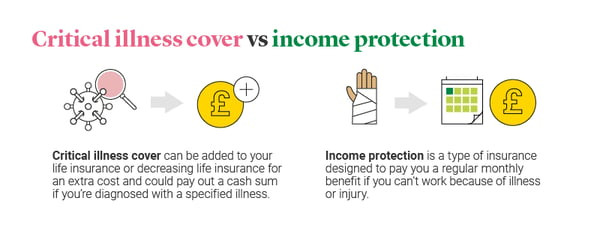

Critical illness cover and income protection are two distinct types of insurance designed to protect your finances, but they work in different ways. Understanding their core functions will help you assess whether you need them.

- Critical Illness Cover: This insurance provides a one-off, tax-free lump sum if you are diagnosed with a critical illness covered by the policy.

- Income Protection: This insurance pays out a regular monthly income if you are unable to work due to illness or injury, resulting in a loss of earnings.

Comparing income protection with critical illness cover

Comparing income protection with critical illness cover

2. Income Protection: Safeguarding Your Earnings

2.1. How Income Protection Works

Income protection insurance is designed to replace a portion of your income if you can’t work because of illness or injury. It ensures that you continue to receive a regular income until you can return to work, retire, or the policy ends.

According to research from the University of Texas at Austin’s McCombs School of Business, strategic partnerships are crucial for sustained income. By ensuring personal financial stability through income protection, you are better positioned to manage and nurture these partnerships.

2.2. Advantages of Income Protection

- Covers a Broad Range of Illnesses and Injuries: Income protection covers a wide variety of conditions that prevent you from working, offering comprehensive coverage.

- Regular Monthly Payments: Provides a steady income stream to cover essential expenses.

- Tax-Free Benefits: Payments are typically tax-free, maximizing the financial relief.

- Multiple Claims Possible: You can make multiple claims during the policy term if different illnesses or injuries occur.

2.3. Disadvantages of Income Protection

- Doesn’t Cover Unemployment: It doesn’t pay out if you become unemployed for reasons other than illness or injury.

- May Exclude Pre-existing Conditions: Policies might exclude pre-existing medical conditions.

- Doesn’t Cover Your Full Income: Typically, it only covers a portion of your income (e.g., 50-70%).

2.4. Who Needs Income Protection?

- Self-Employed Individuals: If you’re self-employed, you likely don’t have access to sick pay, making income protection essential.

- Entrepreneurs and Business Owners: Protecting your income ensures you can continue to meet personal and business obligations, even when you’re unable to work.

- Those with Limited Sick Pay: If your employer offers limited sick pay, income protection can bridge the gap.

- Individuals with Financial Commitments: If you have significant financial responsibilities, such as a mortgage or dependents, income protection ensures these needs are met.

2.5. Real-World Example

Consider an Austin-based marketing consultant who relies on their income to manage their business and personal expenses. If they become ill and can’t work for several months, income protection ensures they can continue to pay their mortgage, cover business costs, and support their family without depleting their savings or disrupting strategic partnerships.

3. Critical Illness Cover: Financial Security During Severe Illness

3.1. How Critical Illness Cover Works

Critical illness cover pays out a lump sum if you are diagnosed with a specified critical illness. This lump sum can be used to cover medical expenses, mortgage payments, lifestyle adjustments, or any other financial needs.

3.2. Advantages of Critical Illness Cover

- Lump Sum Payment: Provides immediate access to a significant amount of money.

- Covers Major Illnesses: Typically includes coverage for cancer, heart attack, stroke, and other serious conditions.

- Flexibility in Use: The payout can be used for any purpose, offering flexibility in managing your finances.

- Can Be Added to Life Insurance: Often available as an add-on to life insurance policies.

3.3. Disadvantages of Critical Illness Cover

- Not All Illnesses Are Covered: Coverage is limited to the specific illnesses listed in the policy.

- Requires Survival Period: Payouts usually require surviving a certain period (e.g., 14 days) after diagnosis.

- Ends After Payout: Once a claim is made, the policy ends.

3.4. Who Needs Critical Illness Cover?

- Individuals with a Family History of Critical Illness: If you have a family history of cancer, heart disease, or other critical illnesses, this cover can provide financial security.

- Those Seeking Financial Security: Provides peace of mind knowing that a lump sum will be available to manage expenses if a critical illness occurs.

- Individuals with Significant Financial Commitments: Helps cover large expenses like mortgage payments or medical bills.

- Entrepreneurs and Business Owners: Offers a financial cushion to manage business and personal expenses during a health crisis.

3.5. Real-World Example

Imagine a tech entrepreneur in Austin who is diagnosed with a severe form of cancer. Critical illness cover would provide a lump sum that they could use to pay for specialized treatment, hire help for their business, and ensure their family’s financial stability while they focus on recovery.

4. Detailed Comparison: Income Protection vs. Critical Illness Cover

To make an informed decision, it’s important to understand the key differences between income protection and critical illness cover.

4.1. Coverage Scope

- Income Protection: Covers a broad range of illnesses and injuries that prevent you from working.

- Critical Illness Cover: Covers only specific critical illnesses listed in the policy.

4.2. Payout Structure

- Income Protection: Pays a regular monthly income.

- Critical Illness Cover: Pays a one-time lump sum.

4.3. Purpose of Payout

- Income Protection: Designed to replace lost income and cover ongoing expenses.

- Critical Illness Cover: Designed to cover medical expenses, debt, and other immediate financial needs.

4.4. Claim Trigger

- Income Protection: Triggered by the inability to work due to illness or injury.

- Critical Illness Cover: Triggered by the diagnosis of a specified critical illness.

4.5. Policy Duration

- Income Protection: Pays out until you can return to work, retire, or the policy ends.

- Critical Illness Cover: Pays out once, and the policy terminates.

Comparison of Critical Illness Cover vs Income Protection

Comparison of Critical Illness Cover vs Income Protection

5. Why Both? The Power of Combined Protection

For many, the ideal solution involves having both income protection and critical illness cover. They serve different but equally important purposes.

5.1. Comprehensive Coverage

- Income Protection: Ensures you can meet ongoing expenses if you’re unable to work.

- Critical Illness Cover: Provides a financial cushion to deal with the immediate and long-term costs associated with a severe illness.

5.2. Strategic Financial Planning

Having both types of cover allows for more robust financial planning. You can address both short-term income replacement and long-term medical and lifestyle adjustments.

5.3. Peace of Mind

Knowing you have comprehensive coverage reduces stress and provides peace of mind, allowing you to focus on your health and business partnerships.

6. Factors to Consider When Choosing Coverage

6.1. Age and Health

Younger individuals may prioritize income protection due to the higher likelihood of injuries, while older individuals might lean towards critical illness cover due to the increased risk of serious illnesses.

6.2. Financial Situation

Assess your income, expenses, debts, and savings to determine the level of coverage you need. Consider how long you could manage without income and the potential costs of treating a critical illness.

6.3. Occupation

High-risk occupations may benefit more from income protection, while those with a family history of critical illness may find critical illness cover more valuable.

6.4. Policy Terms and Conditions

Carefully review the policy terms, including what is covered, exclusions, waiting periods, and payout conditions. Ensure the policy meets your specific needs and circumstances.

7. The Role of Strategic Partnerships in Financial Security

Strategic partnerships can play a crucial role in mitigating financial risks and enhancing overall financial security.

7.1. Business Continuity

Partnerships can ensure business continuity if you are unable to work due to illness or injury. Partners can step in to manage operations, maintaining revenue streams and protecting your business interests.

7.2. Diversification of Income

Collaborating with multiple partners diversifies your income sources, reducing reliance on a single stream. This diversification can help offset potential losses due to illness or injury.

7.3. Resource Sharing

Partnerships allow for the sharing of resources, such as equipment, staff, and expertise. This can reduce costs and improve efficiency, enhancing financial stability.

7.4. Mutual Support

In times of crisis, partners can provide mutual support, both financially and emotionally. This support can be invaluable in managing the challenges associated with illness or injury.

8. How to Find the Right Coverage

8.1. Consult a Financial Advisor

A financial advisor can assess your needs, compare different policies, and recommend the most suitable coverage options.

8.2. Compare Policies

Use online comparison tools to research and compare policies from different providers. Pay attention to coverage, premiums, terms, and conditions.

8.3. Read Reviews and Testimonials

Check customer reviews and testimonials to gauge the experiences of other policyholders. This can provide valuable insights into the quality of service and claims process.

8.4. Understand the Fine Print

Carefully read the policy documents to understand what is covered, what is excluded, and the conditions for making a claim.

9. Optimizing Your Financial Strategy with Income-Partners.net

At income-partners.net, we understand the importance of strategic partnerships in securing your financial future. Our platform offers resources and connections to help you build robust partnerships that complement your insurance coverage.

9.1. Identifying Synergistic Partners

Use our platform to identify potential partners whose skills and resources align with your business goals. Synergistic partnerships can create new revenue streams and enhance your financial stability.

9.2. Building Strong Relationships

We provide tools and strategies for building strong, mutually beneficial relationships with your partners. Strong relationships are essential for long-term success and financial security.

9.3. Risk Mitigation through Collaboration

Collaborate with your partners to identify and mitigate potential risks. By sharing resources and expertise, you can reduce the impact of unexpected events on your finances.

9.4. Leveraging Technology for Efficiency

Utilize our technology platform to streamline communication, manage projects, and track performance. Efficient collaboration can improve productivity and enhance your financial outcomes.

Address: 1 University Station, Austin, TX 78712, United States.

Phone: +1 (512) 471-3434.

Website: income-partners.net.

10. Case Studies: Success Stories of Combined Protection

10.1. The Entrepreneur’s Safeguard

An Austin-based tech entrepreneur invested in both income protection and critical illness cover. When diagnosed with a serious heart condition, the critical illness payout covered immediate medical expenses and allowed him to hire a temporary CEO to manage his company. Income protection ensured his personal income was maintained, preventing financial strain during his recovery.

10.2. The Freelancer’s Safety Net

A freelance marketing consultant in the USA purchased income protection to safeguard against potential injuries or illnesses. When a car accident left her unable to work for several months, income protection provided a steady income stream, allowing her to focus on recovery without worrying about financial obligations.

10.3. The Business Owner’s Resilience

A small business owner with multiple strategic partnerships had both income protection and critical illness cover. After being diagnosed with cancer, the critical illness payout enabled him to seek specialized treatment and maintain his business operations. Income protection ensured his family’s financial needs were met, allowing him to concentrate on his health and recovery.

11. Staying Informed: Trends in Insurance and Partnership

11.1. Telemedicine and Insurance

The rise of telemedicine is impacting insurance by providing easier access to healthcare and faster diagnoses. Some insurance policies now include telemedicine services, enhancing the value of coverage.

11.2. Personalized Insurance Products

Insurers are increasingly offering personalized products tailored to individual needs and circumstances. This trend allows you to customize your coverage to match your specific risks and financial goals.

11.3. Growth of Partnership Ecosystems

Businesses are forming larger and more diverse partnership ecosystems to drive innovation and growth. These ecosystems provide access to a broader range of resources and expertise, enhancing financial resilience.

11.4. Digital Platforms for Partnership Management

Digital platforms like income-partners.net are streamlining the process of finding, building, and managing partnerships. These platforms offer tools for communication, project management, and performance tracking, improving the efficiency and effectiveness of collaborations.

12. The Future of Financial Security: Integrating Insurance and Partnerships

The future of financial security involves a holistic approach that integrates insurance coverage with strategic partnerships.

12.1. Proactive Risk Management

By combining insurance with strong partnerships, you can proactively manage financial risks and build a more resilient financial foundation.

12.2. Enhanced Business Opportunities

Strategic partnerships can create new business opportunities and revenue streams, offsetting potential losses due to illness or injury.

12.3. Greater Financial Independence

Comprehensive insurance coverage and robust partnerships provide greater financial independence, allowing you to pursue your goals with confidence and peace of mind.

12.4. Community Support

Partnerships can foster a sense of community and mutual support, providing emotional and practical assistance during challenging times.

13. The Bottom Line: Is It Worth It?

Investing in both income protection and critical illness cover can provide significant financial security and peace of mind. While the costs may seem daunting, the benefits of protecting your income and assets during a health crisis are invaluable.

13.1. Protecting Your Income

Income protection ensures you can continue to meet your financial obligations if you are unable to work due to illness or injury.

13.2. Safeguarding Your Assets

Critical illness cover provides a lump sum to cover medical expenses and other costs associated with severe illness, protecting your assets and financial stability.

13.3. Building a Resilient Financial Future

By combining insurance coverage with strategic partnerships, you can build a resilient financial future that withstands unexpected events and supports your long-term goals.

14. Call to Action: Secure Your Future Today

Don’t wait until it’s too late to protect your income and assets. Explore your options for income protection and critical illness cover today. Visit income-partners.net to discover strategic partnership opportunities that can further enhance your financial security.

14.1. Take the First Step

Contact a financial advisor to discuss your needs and find the right coverage options.

14.2. Explore Partnership Opportunities

Visit income-partners.net to connect with potential partners and build a stronger financial foundation.

14.3. Secure Your Future

Invest in your financial security today and enjoy peace of mind knowing you are prepared for whatever the future may hold.

Thinking woman deciding between critical illness and income protection

Thinking woman deciding between critical illness and income protection

15. FAQs: Addressing Your Concerns About Income Protection and Critical Illness Cover

15.1. What Exactly is Income Protection Insurance?

Income protection insurance replaces a portion of your income if you can’t work due to illness or injury, ensuring financial stability during recovery.

15.2. How Does Critical Illness Cover Work?

Critical illness cover provides a one-time, tax-free lump sum if diagnosed with a covered critical illness, helping manage medical and living expenses.

15.3. Is Income Protection Taxable?

No, income protection benefits are typically tax-free, maximizing the financial relief provided.

15.4. What Critical Illnesses Are Commonly Covered?

Commonly covered critical illnesses include cancer, heart attack, stroke, and other serious conditions.

15.5. Can I Have Both Income Protection and Critical Illness Cover?

Yes, having both provides comprehensive financial security by addressing both short-term income replacement and long-term medical costs.

15.6. Who Should Consider Income Protection?

Self-employed individuals, entrepreneurs, and those with limited sick pay should consider income protection.

15.7. What Are the Key Benefits of Critical Illness Cover?

The key benefits include a lump sum payment, coverage for major illnesses, and flexibility in how the payout is used.

15.8. How Do Strategic Partnerships Enhance Financial Security?

Strategic partnerships ensure business continuity, diversify income, share resources, and provide mutual support during crises.

15.9. Where Can I Find Reliable Insurance Coverage?

Consult a financial advisor, compare policies online, and read customer reviews to find reliable insurance coverage.

15.10. How Does income-partners.net Support Financial Security?

income-partners.net offers resources and connections to build robust partnerships, complementing insurance coverage for enhanced financial stability.

By understanding the nuances of income protection and critical illness cover, and by leveraging the power of strategic partnerships, you can build a solid foundation for financial security and peace of mind. Visit income-partners.net today to take the next step towards a more secure future.