Do Dividends Count As Income For Social Security? The answer is crucial for anyone planning their retirement and aiming to maximize their income. At income-partners.net, we understand the importance of a well-rounded financial strategy, which is why we’re here to provide clarity on this topic. This guide breaks down how dividends interact with Social Security benefits, ensuring you’re well-prepared to make informed decisions. Maximize your retirement income with strategic financial partnerships, portfolio diversification, and long-term investment.

1. How Are Social Security Benefits Determined?

How are Social Security benefits determined? Your monthly Social Security benefits hinge primarily on two factors: your average earnings over your working life and the age at which you begin claiming benefits.

The Social Security Administration (SSA) calculates your benefits using a formula that considers your average indexed monthly earnings (AIME) over your 35 highest-earning years. It is important to note that dividends are not considered in this calculation. This calculation determines your primary insurance amount (PIA), which is the benefit you would receive if you start payouts at your full retirement age (FRA). Your full retirement age, the age at which you’re entitled to full Social Security benefits without reduction for early retirement or increase for delayed retirement, depends on your birth year:

- 1937 or before: Age 65

- 1938 to 1942: Age 65 and 2 months to age 65 and 10 months

- 1943 to 1954: Age 66

- 1955 to 1959: Age 66 and 2 months to age 66 and 10 months

- 1960 or later: Age 67

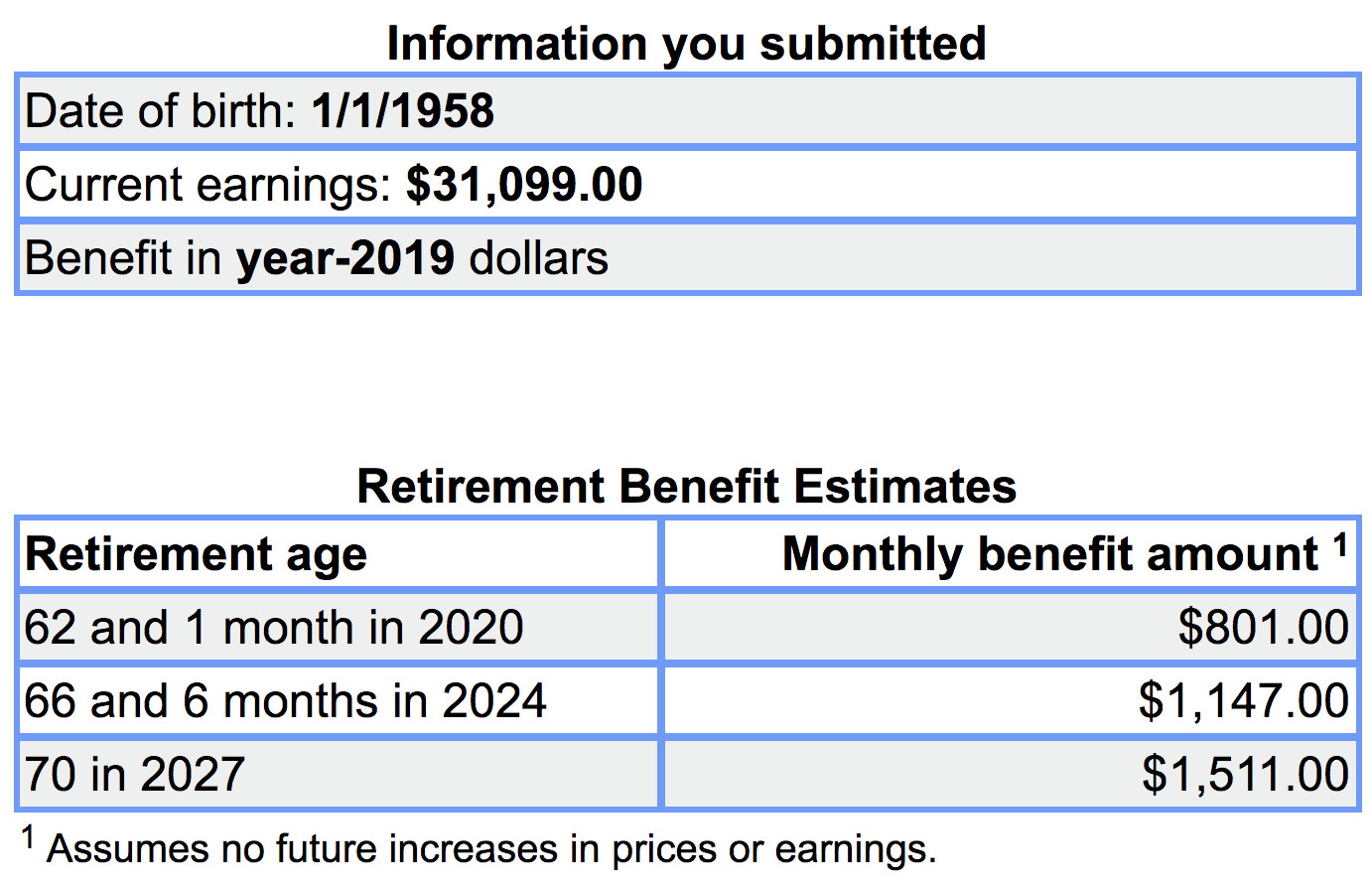

Claiming Social Security as early as age 62 results in a reduction in benefits, as much as 30%. Waiting longer to claim benefits increases your monthly income, up to age 70. For example, a person born on January 1, 1958, with a median U.S. income of $31,099, would receive $1,147 per month in benefits if they earned this median amount for 35 years and retired at their full retirement age (66 and 6 months) in 2024.

Social Security Benefits Calculator example

Social Security Benefits Calculator example

Delaying your benefits until age 70 increases your monthly payment, due to delayed retirement credits. Waiting beyond age 70 does not further increase your benefits.

For high earners, the maximum Social Security benefit at full retirement age was $2,861 per month in 2019, assuming work-related earnings were at or above the maximum cap on Social Security taxes ($132,900 in 2019).

In December 2018, retired workers and their dependents received an average monthly Social Security benefit of $1,461, or about $17,532 per year. Social Security payments were not designed to completely replace one’s working income, and even maximizing benefits does not generate princely sums.

According to the Social Security Administration, nearly nine out of ten individuals age 65 and older receive Social Security benefits, but such payments only represent about 33% of the income of the elderly. The average household run by someone who is at least 65 years old spends $49,542 per year, according the latest data from the U.S. Bureau of Labor Statistics. A couple maximizing benefits by delaying Social Security until age 70 would still only receive $36,264 per year, or 73% of what the average couple needs to cover retirement expenses.

The gap between what Social Security pays and what typical retirees spend is meant to be filled with other income sources, such as pensions and private savings, including dividends, stocks, and bonds.

2. How Do Dividends Affect Social Security Benefits?

How do dividends affect Social Security benefits? While receiving Social Security benefits, you can continue to work. If you begin taking benefits before your full retirement age, an earnings limit may reduce your benefits.

In 2019, the limit was $17,040 per year. Exceeding this limit reduces your annual benefit by $1 for every $2 of work-related income above the limit. This penalty disappears once you reach full retirement age, allowing you to earn as much as you want without losing benefits.

Earnings include income from wages or net earnings from self-employment, bonuses, commissions, and severance pay. They do not include investment income, pensions, capital gains, and inheritances. Dividends and capital gains will not negatively affect your Social Security benefits directly, even if you file earlier than your full retirement age.

However, dividends and capital gains can still affect your ultimate net Social Security benefits due to taxes. At the federal level, up to 85% of Social Security benefits are taxable, based on your combined income:

- Combined income = adjusted gross income + nontaxable interest + half of your Social Security benefits

The amount of your Social Security that is taxable depends on your combined income:

- Single filers with $25,000 to $34,000 combined income: up to 50% of benefits are taxable at federal level

- Married couple filing jointly with $32,000 to $44,000 combined income: up to 50% of benefits are taxable

- Single and married couples with combined incomes above $34,000 and $44,000, respectively: up to 85% of benefits are taxable

Adjusted gross income (AGI) is your total income minus deductions and certain expenses. Capital gains and dividends are included in your AGI figure, and thus count in your combined income calculation. No matter how capital gains and dividends are classified, they are still included in your AGI. Long-term capital gains, short-term capital gains, ordinary dividends, and qualified dividends are treated the same in this calculation, even though they can be taxed at different rates.

As a result, dividends can affect the net Social Security benefits you receive by potentially increasing the amount of your benefits that are taxable at the federal level. Qualified dividends enjoy tax advantages that make them an appealing source of income for many investors.

Qualified dividends are taxed at the long-term capital gains rate, which is lower than the marginal income tax rate. Following tax reform, the long-term capital gain rates look like this for different filers and taxable income levels:

Tax Rate examples for married couple

Tax Rate examples for married couple

A married couple could generate up to $78,750 of taxable income and avoid paying federal taxes on all of their qualified dividends. However, they could exceed the Social Security benefits combined income limit of $44,000 for couples.

In that case, 85% of their Social Security benefits would be classified as taxable income. However, the couple could claim a standard deduction of $24,400 to help reduce their taxable income. Assuming they do not have any other sources of income besides Social Security benefits and dividends, this couple’s overall effective tax rate in retirement, including the 0% tax rate on their qualified dividend income if their taxable income remains below $78,750, would be quite attractive.

Dividends increase your adjusted gross income and therefore have potential to reduce your net Social Security benefits after taxes, their attractive tax treatment and performance qualities still make them an appealing source of income. Required Minimum Distributions (RMDs) from retirement accounts, such as IRAs or 401(k)s, after age 70.5 are also included in your AGI and thus combined income calculations.

It is worth noting that 13 states tax Social Security benefits:

- Colorado

- Connecticut

- Kansas

- Minnesota

- Missouri

- Montana

- Nebraska

- New Mexico

- North Dakota

- Rhode Island

- Utah

- Vermont

- West Virginia

The way these states tax benefits varies wildly. Vermont uses the same rules as the federal government, while Connecticut will only tax benefits for individuals and married couples earning at least $50,000 or $60,000, respectively. If you live in one of these states make sure you check how your benefits will be taxed and what potential AGI limits should be kept in mind.

3. Intent To Understand Tax Implications Of Dividends

How can I understand the tax implications of dividends in relation to Social Security benefits? Understanding how dividends are taxed and how they affect your Social Security benefits is crucial for retirement planning.

| Tax Factor | Description |

|---|---|

| Qualified Dividends | These are taxed at lower long-term capital gains rates, which are generally more favorable than ordinary income tax rates. |

| Ordinary Dividends | These are taxed at your ordinary income tax rate, which can be higher than the rate for qualified dividends. |

| Adjusted Gross Income (AGI) | Dividends are included in your AGI, which is a critical figure used to determine the taxability of your Social Security benefits. A higher AGI can lead to a larger portion of your Social Security benefits being subject to federal income tax. |

| Combined Income | This includes your AGI, nontaxable interest, and half of your Social Security benefits. The IRS uses this figure to determine how much of your Social Security benefits are taxable. |

| Tax Thresholds | The IRS has specific income thresholds that determine the percentage of your Social Security benefits that may be taxable. For example, for single filers, up to 50% of benefits may be taxable if combined income is between $25,000 and $34,000, and up to 85% may be taxable if combined income is above $34,000. For married couples filing jointly, these thresholds are $32,000 to $44,000 and above $44,000, respectively. |

| State Taxes | Some states also tax Social Security benefits, which can further complicate your tax planning. The rules vary significantly by state, so it’s essential to know the specific regulations in your state of residence. |

| Tax-Advantaged Accounts | Investing in tax-advantaged accounts like 401(k)s or IRAs can change how dividends are taxed. For example, dividends earned within a traditional IRA are tax-deferred until withdrawal, while those in a Roth IRA may be tax-free. |

| Tax Planning Strategies | Strategies like tax-loss harvesting, asset location, and careful management of dividend income can help minimize your tax liability and maximize your after-tax income. |

| Professional Advice | Due to the complexity of tax laws, consulting with a tax professional is often advisable. They can provide personalized guidance based on your specific financial situation and help you navigate the intricacies of dividend taxation and Social Security benefits. |

| Tax Law Changes | Tax laws can change, so staying informed about the latest regulations is crucial. Regularly review your tax plan with a professional to ensure you’re taking advantage of all available opportunities and complying with current laws. |

| Estimated Taxes | If you receive significant dividend income, you may need to pay estimated taxes quarterly to avoid penalties. Planning for this in advance can help you manage your cash flow and avoid surprises at tax time. |

| Record Keeping | Maintaining accurate records of your dividend income, investment transactions, and other relevant financial information is essential for accurate tax reporting. |

4. Determine Impact Of Dividend On Social Security

How do I determine the impact of dividend income on my Social Security benefits? Determining the specific impact of dividend income on your Social Security benefits requires a comprehensive assessment of your overall financial situation and an understanding of the relevant tax rules.

Begin by calculating your adjusted gross income (AGI), which includes all sources of income, including dividends. Differentiate between qualified and ordinary dividends as they are taxed differently, with qualified dividends generally taxed at lower long-term capital gains rates. Calculate your combined income by adding your AGI, any nontaxable interest, and half of your Social Security benefits.

Check the IRS income thresholds for Social Security benefit taxation. For example, in 2023, single filers with a combined income between $25,000 and $34,000 may have up to 50% of their benefits taxed, while those with combined income above $34,000 may have up to 85% taxed. For married couples filing jointly, the thresholds are $32,000 and $44,000, respectively.

Determine the portion of your Social Security benefits that will be subject to federal income tax based on your combined income and the applicable IRS thresholds. Also, consider any state taxes on Social Security benefits. Some states do not tax these benefits, while others do, which can further affect your overall tax liability.

Evaluate how dividend income may push you into a higher tax bracket, which could increase the amount of taxes you pay on both your dividends and Social Security benefits. Explore strategies to minimize the impact of dividend income on your Social Security benefits, such as investing in tax-advantaged accounts (e.g., 401(k)s, IRAs) or using tax-loss harvesting to offset capital gains.

Use online calculators and tax software to estimate your tax liability, taking into account your dividend income and Social Security benefits. Given the complexity of tax laws, consulting with a tax professional is highly recommended. They can provide personalized advice based on your specific financial situation and help you navigate the intricacies of dividend taxation and Social Security benefits.

Stay informed about any changes to tax laws and regulations that could affect how dividend income impacts your Social Security benefits. Tax laws can change, so it’s essential to stay updated.

5. Can Dividends Reduce Social Security Benefits

Can dividends directly reduce Social Security benefits? Dividends do not directly reduce the amount of Social Security benefits you receive; however, they can indirectly affect the net amount you take home due to taxation.

| Aspect | Description |

|---|---|

| Direct Reduction | Dividends do not directly reduce your Social Security benefits. The Social Security Administration (SSA) does not subtract dividend income from your benefit amount. |

| Taxation of Benefits | Dividend income can increase your adjusted gross income (AGI), which is used to determine how much of your Social Security benefits are subject to federal income tax. Higher AGI can result in a larger portion of your benefits being taxed. |

| Combined Income | Your combined income (AGI + nontaxable interest + half of your Social Security benefits) is used to determine the taxability of your Social Security benefits. Dividend income contributes to AGI, and therefore can affect the combined income calculation. |

| Income Thresholds | The IRS has specific income thresholds that determine the percentage of your Social Security benefits that may be taxable. For example, for single filers, up to 50% of benefits may be taxable if combined income is between $25,000 and $34,000, and up to 85% may be taxable if combined income is above $34,000. For married couples filing jointly, these thresholds are $32,000 to $44,000 and above $44,000, respectively. |

| Example | Suppose a single filer has an AGI of $30,000, including $5,000 in dividend income, and receives $15,000 in Social Security benefits. Their combined income is $30,000 (AGI) + $0 (nontaxable interest) + $7,500 (half of Social Security benefits) = $37,500. Since this is above $34,000, up to 85% of their Social Security benefits could be taxable. |

| Net Effect | While the gross amount of your Social Security benefits remains unchanged, the net amount you receive after taxes can be reduced due to dividend income increasing your taxable income. |

| Tax Planning | Strategies to minimize the impact of dividend income on your Social Security benefits include investing in tax-advantaged accounts, tax-loss harvesting, and carefully managing your dividend income to stay below certain income thresholds. |

| Professional Advice | Consulting with a tax professional is recommended to assess your specific situation and develop a tax-efficient strategy. |

| State Taxes | Some states also tax Social Security benefits, which can further complicate your tax planning. |

| Earnings Limit | Keep in mind, if you are under the full retirement age and still working, there’s an earnings limit. Although dividends do not count towards this limit, exceeding the earnings limit will reduce your Social Security benefits. For 2023, this limit is $21,240, and for every $2 earned over this amount, $1 is deducted from Social Security benefits. |

| Full Retirement Age (FRA) | Once you reach full retirement age, you can earn as much as you like without any reduction in Social Security benefits. This is a key factor to consider when planning retirement and dividend income strategies. |

6. What Investment Income Affects Social Security

What types of investment income affect Social Security benefits? While most investment income doesn’t directly reduce your Social Security benefits, it can indirectly affect the net amount you receive due to taxation. Here’s a breakdown:

| Type of Investment Income | Affect on Social Security Benefits |

|---|---|

| Dividends | Dividends are included in your adjusted gross income (AGI), which is used to calculate your combined income. Your combined income (AGI + nontaxable interest + half of your Social Security benefits) determines the taxability of your Social Security benefits. Higher dividend income can increase your AGI, leading to a larger portion of your Social Security benefits being subject to federal income tax. Qualified dividends are taxed at lower long-term capital gains rates, while ordinary dividends are taxed at your ordinary income tax rate. Managing your dividend income can help optimize your tax situation. |

| Capital Gains | Like dividends, capital gains are included in your AGI and contribute to your combined income, affecting the taxability of your Social Security benefits. Strategies like tax-loss harvesting can help offset capital gains, reducing your overall tax liability. Long-term and short-term capital gains are treated the same for Social Security taxation purposes, although they are taxed at different rates. |

| Interest Income | Taxable interest income, such as from bonds, CDs, and savings accounts, is included in your AGI and contributes to your combined income. Nontaxable interest (e.g., from municipal bonds) does not directly affect the taxability of your Social Security benefits. |

| Rental Income | Net rental income (rental income minus expenses) is included in your AGI and contributes to your combined income, affecting the taxability of your Social Security benefits. Properly managing rental expenses can help minimize your tax liability. |

| Retirement Account Distributions | Distributions from tax-deferred retirement accounts, such as traditional 401(k)s and IRAs, are included in your AGI and contribute to your combined income, affecting the taxability of your Social Security benefits. Roth IRA distributions are generally tax-free and do not affect the taxability of your Social Security benefits. Timing your distributions and considering Roth conversions can help manage your tax liability. |

| Annuity Payments | The taxable portion of annuity payments is included in your AGI and contributes to your combined income, affecting the taxability of your Social Security benefits. The taxability of annuity payments depends on whether the annuity was purchased with pre-tax or after-tax dollars. |

| Investment Income Not Affecting Social Security | Income from municipal bonds, certain types of life insurance, and health savings accounts (HSAs) generally do not affect the taxability of your Social Security benefits. |

7. How To Minimize Taxes On Social Security

How can I minimize taxes on Social Security benefits when receiving dividend income? To minimize taxes on Social Security benefits while receiving dividend income, a strategic approach is essential.

| Strategy | Description |

|---|---|

| Tax-Advantaged Accounts | Maximize contributions to tax-advantaged accounts such as 401(k)s, traditional IRAs, and health savings accounts (HSAs). Contributions to these accounts reduce your adjusted gross income (AGI), potentially lowering your combined income and the amount of Social Security benefits subject to tax. |

| Roth Conversions | Consider converting funds from traditional IRAs or 401(k)s to Roth IRAs. While you’ll pay taxes on the converted amount in the year of conversion, future withdrawals (including earnings) from the Roth IRA are tax-free, potentially reducing your taxable income in retirement. |

| Tax-Loss Harvesting | Use tax-loss harvesting to offset capital gains. Selling investments at a loss can offset capital gains, reducing your overall AGI and potentially lowering the amount of Social Security benefits subject to tax. You can deduct up to $3,000 in net capital losses per year ($1,500 if married filing separately). |

| Asset Location | Strategically allocate different types of investments between taxable, tax-deferred, and tax-exempt accounts. Place high-dividend-paying stocks in tax-advantaged accounts to avoid or defer taxes on the dividend income. |

| Manage Dividend Income | Manage the timing and amount of dividend income to stay below certain income thresholds. Consider delaying the realization of dividend income, if possible, to years when your overall income is lower. |

| Municipal Bonds | Invest in municipal bonds, which offer tax-exempt interest income. Since this income is not included in your AGI, it does not affect the taxability of your Social Security benefits. |

| Qualified Dividends | Prioritize investments that generate qualified dividends, which are taxed at lower long-term capital gains rates. While they still increase your AGI, the lower tax rate can result in overall tax savings. |

| Itemized Deductions | Itemize deductions instead of taking the standard deduction if your itemized deductions exceed the standard deduction amount. Deductions such as medical expenses, state and local taxes (SALT), and charitable contributions can reduce your AGI. |

| Timing of Social Security Benefits | Consider delaying claiming Social Security benefits to increase your monthly benefit amount. While this won’t directly reduce the taxability of your benefits, it can provide a larger stream of income later in retirement, potentially allowing you to rely less on taxable investment income. |

| Monitor Tax Law Changes | Stay informed about changes to tax laws and regulations that could affect how dividend income and Social Security benefits are taxed. Tax laws can change, so it’s essential to stay updated. |

| Professional Advice | Consult with a tax professional who can assess your specific situation and develop a personalized tax-efficient strategy. A tax professional can help you navigate the complexities of dividend taxation and Social Security benefits and make informed decisions to minimize your tax liability. |

8. Maximizing Social Security With Passive Income

How can I maximize Social Security benefits while generating passive income from dividends? Maximizing Social Security benefits while generating passive income from dividends requires a strategic approach that balances income streams and minimizes tax liabilities.

| Strategy | Description |

|---|---|

| Delay Social Security Benefits | Delaying your Social Security benefits until age 70 maximizes your monthly benefit amount. For each year you delay beyond your full retirement age, your benefits increase by about 8%. This strategy ensures a larger, more secure income stream later in retirement. |

| Optimize Investment Allocation | Allocate investments strategically across taxable, tax-deferred, and tax-exempt accounts. Place high-dividend-paying stocks in tax-advantaged accounts to avoid or defer taxes on the dividend income. Consider using a mix of stocks, bonds, and real estate to diversify your income streams. |

| Tax-Efficient Dividend Strategies | Implement tax-efficient dividend strategies to minimize the impact of dividend income on your overall tax liability. Prioritize investments that generate qualified dividends, which are taxed at lower long-term capital gains rates. Use tax-loss harvesting to offset capital gains and reduce your AGI. |

| Manage Combined Income | Manage your combined income (AGI + nontaxable interest + half of your Social Security benefits) to stay below certain income thresholds. Keeping your combined income below these thresholds can minimize the amount of your Social Security benefits subject to federal income tax. |

| Use Tax-Advantaged Accounts | Maximize contributions to tax-advantaged accounts such as 401(k)s, traditional IRAs, and health savings accounts (HSAs). Contributions to these accounts reduce your AGI, potentially lowering your combined income and the amount of Social Security benefits subject to tax. Consider Roth conversions to create a tax-free income stream in retirement. |

| Consider Part-Time Work | Working part-time can provide additional income and help delay withdrawals from investment accounts. However, be mindful of the Social Security earnings limit if you claim benefits before your full retirement age. In 2023, this limit is $21,240, and for every $2 earned over this amount, $1 is deducted from Social Security benefits. |

| Strategic Withdrawals | Plan strategic withdrawals from investment accounts to supplement your Social Security benefits and dividend income. Prioritize withdrawals from taxable accounts before tapping into tax-deferred accounts. Consider the tax implications of each withdrawal and adjust your strategy accordingly. |

| Review and Adjust Regularly | Regularly review and adjust your financial plan to adapt to changing circumstances and tax laws. Tax laws can change, so it’s essential to stay updated. Consulting with a financial advisor or tax professional can help you navigate the complexities of retirement planning and make informed decisions. |

| Maximize Pension Benefits | If applicable, maximize your pension benefits by making informed decisions about when and how to receive them. Consider the impact of pension benefits on your overall income and tax situation. |

| Consider Long-Term Care Insurance | Purchase long-term care insurance to protect your retirement savings from unexpected healthcare costs. Long-term care expenses can significantly impact your financial security and reduce your ability to generate passive income. |

9. Retirement Income Strategies

What are effective retirement income strategies involving dividends and Social Security? Effective retirement income strategies involving dividends and Social Security require careful planning and a diversified approach to ensure financial security and minimize tax liabilities.

| Strategy | Description |

|---|---|

| Diversified Investment Portfolio | Construct a diversified investment portfolio that includes a mix of stocks, bonds, real estate, and other assets. Allocate a portion of your portfolio to dividend-paying stocks to generate a steady stream of passive income. Consider diversifying across different sectors and industries to reduce risk. |

| Dividend Reinvestment Plan (DRIP) | Enroll in a dividend reinvestment plan (DRIP) to automatically reinvest dividends back into the company’s stock. This can help accelerate the growth of your investment portfolio over time. DRIPs are a convenient way to compound your returns and increase your ownership in the company. |

| Tax-Efficient Investment Strategies | Implement tax-efficient investment strategies to minimize the impact of taxes on your investment returns. Prioritize investments that generate qualified dividends, which are taxed at lower long-term capital gains rates. Use tax-loss harvesting to offset capital gains and reduce your AGI. Consider investing in tax-exempt municipal bonds to generate tax-free income. |

| Delay Social Security Benefits | Delay claiming Social Security benefits until age 70 to maximize your monthly benefit amount. For each year you delay beyond your full retirement age, your benefits increase by about 8%. This strategy ensures a larger, more secure income stream later in retirement. |

| Strategic Withdrawals from Retirement Accounts | Plan strategic withdrawals from retirement accounts to supplement your Social Security benefits and dividend income. Prioritize withdrawals from taxable accounts before tapping into tax-deferred accounts. Consider the tax implications of each withdrawal and adjust your strategy accordingly. |

| Annuities for Guaranteed Income | Consider purchasing an annuity to provide a guaranteed stream of income in retirement. Annuities can offer a predictable income stream that supplements your Social Security benefits and dividend income. Be sure to carefully evaluate the terms and conditions of the annuity before purchasing. |

| Real Estate Investments | Invest in real estate to generate rental income and potential capital appreciation. Rental income can provide a steady stream of passive income in retirement. Consider the tax implications of real estate investments, such as depreciation and property taxes. |

| Part-Time Work or Consulting | Consider working part-time or consulting to supplement your retirement income. Part-time work can provide additional income and help delay withdrawals from investment accounts. However, be mindful of the Social Security earnings limit if you claim benefits before your full retirement age. |

| Downsize Your Home | Consider downsizing your home to reduce expenses and free up capital. Selling your home can provide a lump sum of cash that can be used to supplement your retirement income. Downsizing can also reduce your property taxes, maintenance costs, and utility bills. |

| Regular Financial Planning Reviews | Regularly review and adjust your financial plan to adapt to changing circumstances and tax laws. Tax laws can change, so it’s essential to stay updated. Consulting with a financial advisor or tax professional can help you navigate the complexities of retirement planning and make informed decisions. |

10. What Are The Social Security Earnings Limits

What are the Social Security earnings limits and how do they affect my benefits? The Social Security earnings limits determine how much you can earn from work while still receiving full Social Security benefits. These limits apply only if you are receiving benefits and are younger than your full retirement age (FRA).

| Aspect | Description |

|---|---|

| Earnings Limit | For 2023, if you are under your full retirement age, the earnings limit is $21,240. If you earn more than this amount, your Social Security benefits will be reduced. |

| Benefit Reduction | For every $2 you earn above the annual limit, $1 will be deducted from your Social Security benefits. |

| Year You Reach FRA | In the year you reach your full retirement age, a different earnings limit applies. For 2023, the limit is $56,520. For every $3 you earn above this limit, $1 will be deducted from your Social Security benefits. Only the earnings before the month you reach your FRA are counted. |

| No Limit at FRA | Once you reach your full retirement age, there is no limit on how much you can earn. You will receive your full Social Security benefits regardless of your earnings. |

| Full Retirement Age (FRA) | The full retirement age is 66 for people born from 1943 to 1954, and it gradually increases to 67 for those born in 1960 or later. |

| What Counts as Earnings? | Earnings include wages, salaries, net earnings from self-employment, bonuses, commissions, and vacation pay. |

| What Doesn’t Count as Earnings? | Earnings do not include investment income, such as dividends, interest, and capital gains. They also do not include pensions, annuities, or other retirement income. |

| Example | If you are 64 years old in 2023 and earn $30,000 from work, your earnings exceed the annual limit of $21,240 by $8,760. Your Social Security benefits will be reduced by $4,380 ($8,760 / 2). |

| Reporting Earnings | It is your responsibility to report your earnings to the Social Security Administration (SSA). The SSA will use this information to adjust your benefits accordingly. |

| Impact on Family Benefits | If you are receiving Social Security benefits as a spouse or dependent, your earnings can also affect the benefits of other family members. |

| Purpose of Earnings Limits | The earnings limits are designed to ensure that Social Security benefits are primarily intended to replace lost income due to retirement, disability, or death, rather than to supplement current earnings. |

| Review and Adjust Regularly | The Social Security Administration reviews and adjusts the earnings limits annually to reflect changes in the national average wage. It’s essential to stay informed about the current earnings limits and how they may affect your benefits. |

| Seek Professional Advice | If you have questions or concerns about how the earnings limits may affect your Social Security benefits, consulting with a financial advisor or Social Security expert is recommended |