Do Corporations Pay Federal And State Income Taxes? Yes, corporations generally pay both federal and state income taxes, making strategic partnerships essential for optimizing financial strategies and boosting revenue. At income-partners.net, we help businesses navigate these complexities by connecting them with partners who can provide expert financial guidance. By exploring innovative collaborations and strategic alliances, businesses can effectively manage their tax obligations while maximizing profitability.

1. What Federal Income Taxes Do Corporations Pay?

Yes, corporations in the United States are subject to federal income taxes. The federal corporate income tax is currently levied at a flat rate of 21 percent. This tax applies to the taxable income of corporations, which is the gross income less allowable deductions.

The federal corporate income tax is a significant source of revenue for the U.S. government. It funds various public services and programs. Corporations calculate their taxable income by subtracting business expenses, such as wages, rent, and cost of goods sold, from their gross income. Understanding the federal corporate income tax is crucial for financial planning and compliance.

2. Which States Levy Corporate Income Taxes?

Forty-four states and the District of Columbia impose taxes on corporate income. These state corporate income taxes vary widely, with top marginal rates ranging from 2.5 percent in North Carolina to 11.5 percent in New Jersey.

State Corporate Income Tax Rates

State Corporate Income Tax Rates

The diversity in state corporate tax rates reflects different economic policies and priorities. Businesses often consider these variations when making decisions about where to locate or expand their operations. States with lower tax rates may attract more businesses, fostering economic growth and job creation.

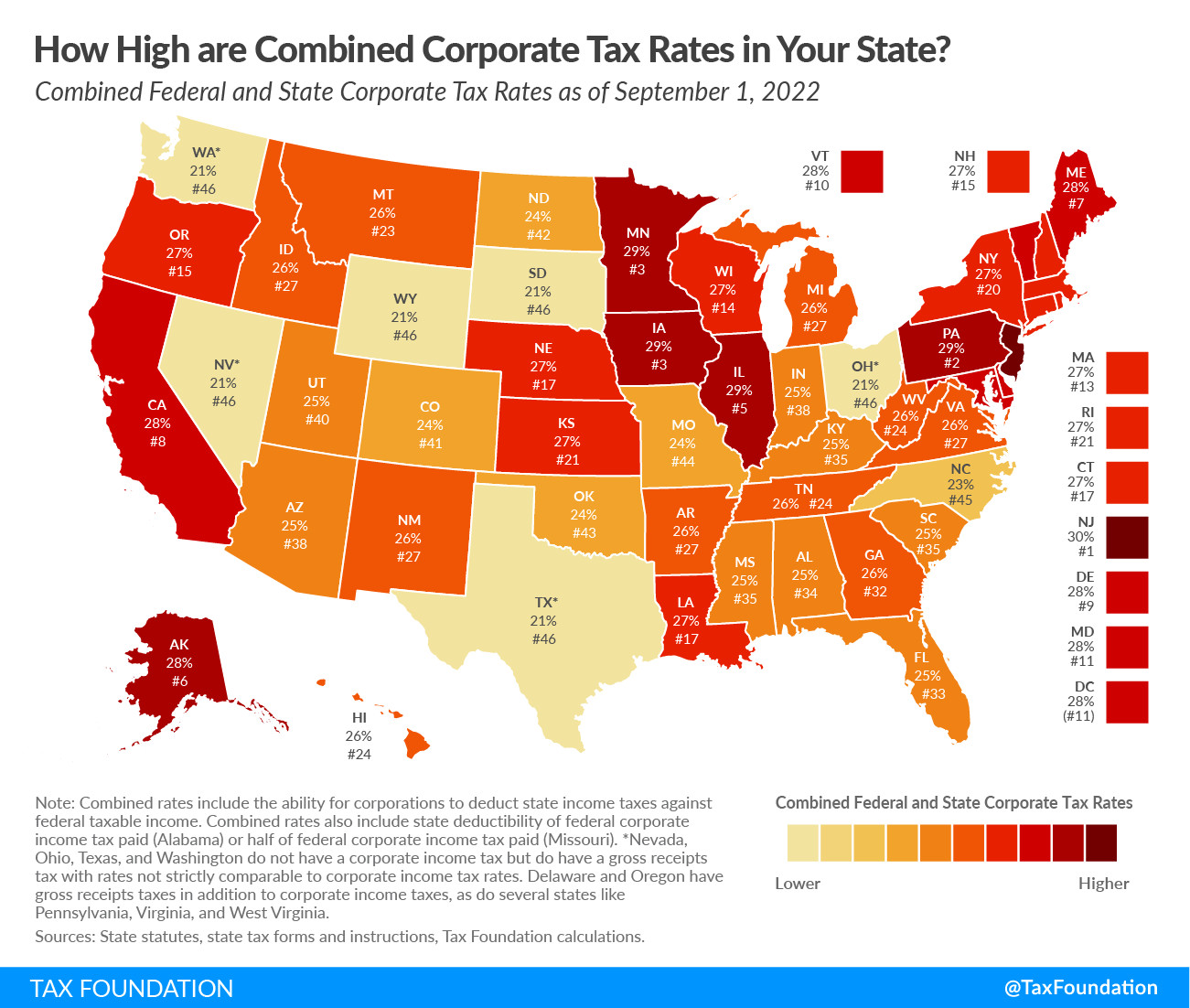

3. Which States Have the Highest Combined Corporate Tax Rates?

New Jersey has the highest combined state and federal corporate tax rate, totaling 30.1 percent. States like Alaska, California, Illinois, Iowa, Maine, Minnesota, and Pennsylvania also face combined corporate tax rates at or above 28 percent.

High combined tax rates can impact a corporation’s profitability and competitiveness. Businesses in these states may need to implement more aggressive tax planning strategies to mitigate the effects of higher taxes. Strategic partnerships, as facilitated by income-partners.net, can provide access to expert advice and resources for managing these tax burdens effectively.

4. Which States Do Not Impose Corporate Income Taxes?

Six states—Ohio, Nevada, South Dakota, Texas, Washington, and Wyoming—do not impose a state corporate income tax. These states rely on other forms of taxation, such as gross receipts taxes, to generate revenue.

The absence of a corporate income tax can be a significant advantage for businesses operating in these states. It can lead to lower overall tax burdens and increased profitability. This favorable tax environment can attract businesses and stimulate economic development.

5. What Are Gross Receipts Taxes?

In Nevada, Ohio, Texas, and Washington, corporations are subject to gross receipts taxes instead of corporate income taxes. Gross receipts taxes are levied on a company’s total gross revenue, without deductions for expenses.

Gross receipts taxes can have different economic effects compared to corporate income taxes. They can impact businesses with low profit margins more heavily, as the tax is applied to total revenue rather than profit. Understanding the nuances of gross receipts taxes is essential for businesses operating in these states.

6. Can Corporations Deduct State Income Taxes on Federal Returns?

Yes, corporations can deduct state corporate income taxes paid against their federal taxable income. This deduction lowers the effective federal corporate income tax rate, providing some relief from the combined tax burden.

For example, a corporation in Rhode Island, which has a 7 percent flat corporate income tax rate, can deduct this amount from its federal taxable income. This reduces their federal rate from 21 percent to 19.53 percent, resulting in a combined rate of 26.53 percent. This deduction is a valuable tool for managing overall tax liabilities.

7. Do Any States Allow Deduction of Federal Income Taxes on State Returns?

Yes, Alabama allows full deductibility of federal corporate income tax liability against state liability, while Missouri permits a 50 percent deduction of federal corporate income tax liability. This further lowers the effective corporate income tax rate for corporations in these states.

These deductions are unique and provide a significant tax advantage to corporations operating in Alabama and Missouri. They can result in substantial savings and improve a company’s financial performance. Such tax benefits highlight the importance of understanding state-specific tax laws and regulations.

8. Why Are Corporate Taxes Economically Damaging?

Corporate taxes are often considered economically damaging because they can reduce investment, hinder job creation, and decrease overall economic growth. These taxes can also lead to tax avoidance strategies, which further erode the tax base.

According to research from the University of Texas at Austin’s McCombs School of Business, corporate taxes can distort economic decision-making and create inefficiencies. Lowering corporate tax rates or reforming the tax system can increase competitiveness and promote economic growth. This benefits both companies and workers, fostering a more vibrant and prosperous economy.

9. How Can States Increase Competitiveness Through Tax Reform?

States can increase competitiveness by reforming their corporate tax systems. This includes lowering tax rates, simplifying tax structures, and offering targeted tax incentives. These reforms can attract businesses, encourage investment, and stimulate economic growth.

Tax reform is a key tool for states looking to improve their business climate and attract new companies. By creating a more favorable tax environment, states can enhance their competitiveness and foster long-term economic prosperity. This, in turn, leads to job creation, increased innovation, and a higher standard of living for residents.

10. What Role Do Strategic Partnerships Play in Tax Optimization?

Strategic partnerships play a crucial role in tax optimization by providing access to expert financial advice, innovative tax planning strategies, and resources for managing complex tax obligations. Collaborating with the right partners can help businesses navigate the intricacies of federal and state tax laws, identify opportunities for tax savings, and ensure compliance.

Income-partners.net facilitates these strategic partnerships, connecting businesses with experienced professionals who can offer tailored solutions for their specific needs. By leveraging the expertise of these partners, businesses can optimize their tax strategies, reduce their tax burdens, and improve their overall financial performance. These alliances can also foster innovation and growth, as businesses collaborate to develop new and effective approaches to tax management.

11. What Are the Key Considerations for Businesses When Planning for Federal and State Income Taxes?

When planning for federal and state income taxes, businesses should consider several key factors: understanding the applicable tax laws and regulations, accurately calculating taxable income, identifying available deductions and credits, and developing a comprehensive tax strategy. It is also essential to stay informed about changes in tax laws and regulations, as these can impact a company’s tax liabilities.

Partnering with tax professionals can provide valuable assistance in navigating these complexities and ensuring compliance. These experts can offer insights into the latest tax developments, help businesses identify potential tax savings opportunities, and develop strategies for minimizing their tax burdens. Effective tax planning is crucial for maintaining financial stability and achieving long-term success.

12. How Do Federal and State Income Taxes Impact Small Businesses Differently Than Large Corporations?

Federal and state income taxes can impact small businesses and large corporations differently due to variations in resources, tax planning capabilities, and access to tax incentives. Small businesses often face challenges in navigating complex tax laws and may lack the resources to engage in sophisticated tax planning strategies.

Large corporations, on the other hand, typically have dedicated tax departments and access to a wider range of tax planning tools and resources. This allows them to take advantage of various tax incentives and minimize their tax liabilities more effectively. As a result, small businesses may bear a disproportionately higher tax burden compared to large corporations. Addressing these disparities is essential for promoting a level playing field and supporting the growth of small businesses.

13. What Are Some Common Tax Deductions Available to Corporations?

Corporations can take advantage of various tax deductions to reduce their taxable income. Common deductions include business expenses such as wages, rent, utilities, and cost of goods sold. Other deductions may include depreciation, amortization, and charitable contributions.

Additionally, corporations can deduct state and local taxes paid, as well as certain business losses. Taking advantage of these deductions can significantly lower a corporation’s tax liability and improve its financial performance. It is essential for businesses to maintain accurate records and documentation to support their deductions and ensure compliance with tax laws.

14. How Can Businesses Stay Compliant with Federal and State Income Tax Laws?

Staying compliant with federal and state income tax laws requires careful attention to detail, accurate record-keeping, and a thorough understanding of tax regulations. Businesses should establish robust accounting systems, maintain detailed records of all financial transactions, and regularly review their tax positions to ensure compliance.

Partnering with tax professionals can provide valuable assistance in navigating the complexities of tax laws and regulations. These experts can help businesses develop effective compliance strategies, identify potential risks, and ensure that they meet all their tax obligations. Regular audits and reviews can also help identify and correct any errors or omissions, further enhancing compliance.

15. What Are the Potential Penalties for Non-Compliance with Federal and State Income Tax Laws?

Non-compliance with federal and state income tax laws can result in significant penalties, including monetary fines, interest charges, and even criminal prosecution. The severity of the penalties depends on the nature and extent of the non-compliance.

Failure to file tax returns on time or accurately report income can result in penalties. Engaging in fraudulent activities, such as tax evasion or misrepresentation of financial information, can lead to more severe consequences, including imprisonment. Businesses should take compliance seriously and seek professional guidance to avoid these penalties.

16. How Do Changes in Federal Tax Laws Impact State Income Tax Policies?

Changes in federal tax laws can have a ripple effect on state income tax policies. Many states link their tax systems to the federal tax code, meaning that changes at the federal level can automatically impact state tax laws.

For example, changes in federal tax rates, deductions, or credits can affect the amount of taxable income that states use to calculate their own taxes. States may need to adjust their tax policies to align with federal changes or to mitigate any unintended consequences. This interconnectedness highlights the importance of monitoring both federal and state tax developments.

17. What Are the Long-Term Trends in Corporate Income Taxation?

Long-term trends in corporate income taxation include a global movement towards lower tax rates and greater tax competition among countries. Many countries have reduced their corporate tax rates to attract businesses and investment.

Additionally, there is increasing scrutiny of multinational corporations and their tax avoidance strategies. Governments are working together to combat tax evasion and ensure that companies pay their fair share of taxes. These trends are likely to continue shaping the corporate tax landscape in the years to come.

18. How Can Businesses Use Tax Credits to Reduce Their Tax Liabilities?

Tax credits are powerful tools that businesses can use to reduce their tax liabilities. Tax credits directly reduce the amount of tax owed, providing a dollar-for-dollar reduction in tax liability. Various tax credits are available at both the federal and state levels, including credits for research and development, renewable energy, and job creation.

Businesses should carefully review available tax credits and take advantage of those for which they are eligible. Claiming tax credits can significantly lower a company’s tax burden and improve its financial performance. It is essential to maintain accurate records and documentation to support claims for tax credits.

19. What Role Do Tax Treaties Play in Corporate Income Taxation?

Tax treaties are agreements between countries that aim to prevent double taxation and promote cross-border investment. These treaties establish rules for determining which country has the right to tax certain types of income, such as dividends, interest, and royalties.

Tax treaties can provide significant benefits to multinational corporations by reducing their overall tax burden and simplifying cross-border transactions. Businesses should understand the provisions of applicable tax treaties and take advantage of their benefits. Partnering with tax professionals who specialize in international taxation can provide valuable assistance in navigating these complexities.

20. How Does the Location of a Corporation’s Headquarters Impact Its Federal and State Income Tax Liabilities?

The location of a corporation’s headquarters can significantly impact its federal and state income tax liabilities. Different states have different tax rates, rules, and incentives, which can affect a company’s overall tax burden.

States with lower tax rates and more favorable tax climates may attract corporations looking to minimize their tax liabilities. Additionally, some states offer tax incentives, such as credits and exemptions, to encourage businesses to locate or expand within their borders. Businesses should carefully consider these factors when choosing a location for their headquarters.

21. How Can Corporations Utilize Transfer Pricing Strategies to Optimize Their Income Tax Liabilities?

Corporations can use transfer pricing strategies to optimize their income tax liabilities by strategically allocating profits among different subsidiaries or branches located in different tax jurisdictions. Transfer pricing involves setting the prices for goods, services, and intellectual property transferred between related entities.

By setting transfer prices that shift profits to lower-tax jurisdictions, corporations can reduce their overall tax burden. However, transfer pricing is subject to scrutiny by tax authorities, and businesses must ensure that their transfer prices are arm’s length, meaning that they reflect the prices that would be agreed upon between unrelated parties.

22. What is the Difference Between Tax Avoidance and Tax Evasion, and Why is it Important to Distinguish Between the Two?

Tax avoidance and tax evasion are two distinct concepts, and it is important to distinguish between them. Tax avoidance involves using legal means to minimize tax liabilities, such as taking advantage of deductions, credits, and other tax incentives. Tax evasion, on the other hand, involves illegal means to avoid paying taxes, such as underreporting income or overstating expenses.

Tax avoidance is generally considered legal and acceptable, while tax evasion is illegal and can result in severe penalties. Businesses should engage in tax planning to minimize their tax liabilities through legal means, but they should avoid engaging in any activities that could be construed as tax evasion.

23. How Can Strategic Alliances Help Corporations Navigate Complex Tax Regulations?

Strategic alliances can be invaluable for corporations seeking to navigate complex tax regulations. These alliances, facilitated by platforms like income-partners.net, connect businesses with experts who can provide tailored guidance and support. These experts can help businesses understand their tax obligations, identify potential tax savings opportunities, and ensure compliance with all applicable laws and regulations.

Moreover, strategic alliances can provide access to innovative tax planning strategies and resources that may not be available to businesses operating in isolation. By collaborating with other organizations and leveraging their expertise, corporations can optimize their tax positions and achieve their financial goals.

24. What Emerging Trends in the Business World Might Impact Future Corporate Tax Liabilities?

Several emerging trends in the business world are likely to impact future corporate tax liabilities. These include the rise of the digital economy, the increasing globalization of business operations, and the growing focus on environmental, social, and governance (ESG) factors.

The digital economy presents challenges for tax authorities, as it can be difficult to determine where value is created and how to allocate profits among different jurisdictions. Globalization also creates complexities, as businesses operate across borders and engage in cross-border transactions. ESG factors are becoming increasingly important, and governments may introduce tax incentives to encourage sustainable business practices.

25. What Is The Role Of A Certified Public Accountant (CPA) In Corporate Tax Planning And Compliance?

A Certified Public Accountant (CPA) plays a crucial role in corporate tax planning and compliance. CPAs are licensed professionals who have met rigorous education, examination, and experience requirements. They possess the knowledge and expertise to help businesses navigate complex tax laws and regulations.

CPAs can assist with tax planning, tax preparation, tax compliance, and tax representation. They can help businesses minimize their tax liabilities, ensure compliance with all applicable laws, and represent them before tax authorities in the event of an audit or dispute. Hiring a CPA is a wise investment for any business looking to optimize its tax position and avoid costly penalties.

In conclusion, corporations face significant federal and state income tax obligations, making strategic partnerships essential. income-partners.net offers a platform to connect with experts who can provide invaluable guidance on tax optimization and financial growth. By leveraging these partnerships, businesses can effectively manage their tax liabilities, enhance their competitiveness, and achieve long-term success. Explore the opportunities at income-partners.net today and unlock your business’s full potential through strategic collaborations and innovative financial solutions.