Can We File Income Tax Return For Assessment Year 2023-24? Absolutely, filing your income tax return for Assessment Year 2023-24 is a key part of managing your financial responsibilities, and at income-partners.net, we aim to simplify this process, making it more accessible and beneficial for you by guiding you through potential partnerships that could optimize your income tax strategies. Explore income tax solutions and financial partnerships to help you navigate the tax season efficiently. Maximize your tax benefits with strategic alliances and smart tax planning.

1. Understanding the Basics of Income Tax Return Filing

Yes, you can file an income tax return for the assessment year 2023-24, but understanding the basics is crucial. Filing an Income Tax Return (ITR) is reporting your income, deductions, and exemptions to the government. This process ensures compliance with tax laws and is essential for financial planning. Understanding the financial year (FY) and assessment year (AY) is vital. The FY is when you earn income, while the AY is when you file the return. For instance, income earned from April 1, 2022, to March 31, 2023 (FY 2022-23), is reported in AY 2023-24. Missing the deadline can lead to penalties and interest, as detailed under Section 234A and Section 234F of the Income Tax Act. Accurate filing also allows you to carry forward losses, which can reduce future tax liabilities.

Key points to remember:

- Understand the difference between Financial Year and Assessment Year.

- Be aware of the due dates to avoid penalties.

- Accurately report income, deductions, and exemptions.

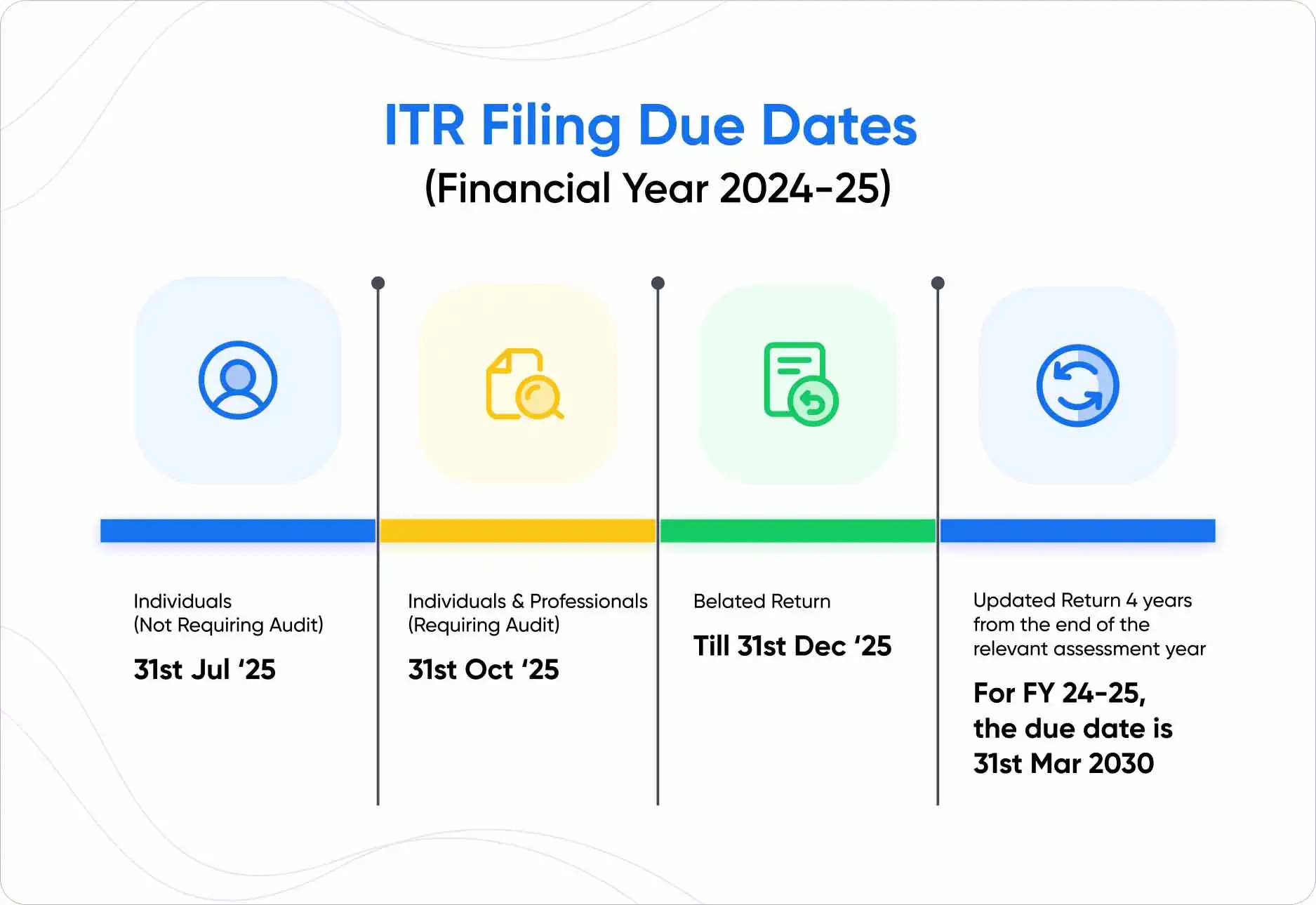

2. Key Dates and Deadlines for Filing ITR

Yes, filing by the set deadlines is essential. The last date to file ITR is generally July 31st of the assessment year for individuals and non-audit cases. However, for businesses requiring an audit, the deadline extends to October 31st. Taxpayers involved in international or specified domestic transactions needing transfer pricing reports have until November 30th. For the Financial Year 2022-23 (Assessment Year 2023-24), the original deadline was July 31, 2023, but there are provisions for belated returns and updated returns. Belated returns can be filed after the original deadline but before December 31st of the assessment year, subject to penalties and interest. Updated returns, introduced to correct errors or omissions, can be filed within two years from the end of the assessment year.

| Type of Return | Due Date for FY 2022-23 (AY 2023-24) | Notes |

|---|---|---|

| Original ITR | July 31, 2023 | For individuals and non-audit cases |

| Audit Cases | October 31, 2023 | For businesses requiring audit |

| Transfer Pricing Cases | November 30, 2023 | International/specified domestic transactions |

| Belated Return | December 31, 2023 | Subject to penalties and interest |

| Updated Return | March 31, 2026 | Within two years from the end of AY |

2.1 Consequences of Missing the Deadline

Yes, missing the ITR filing deadline has consequences. Missing the deadline results in interest under Section 234A at 1% per month on the outstanding tax amount. Additionally, Section 234F imposes a late fee, which can be ₹5,000 if your income exceeds ₹5 lakh and ₹1,000 if your income is below ₹5 lakh. Furthermore, missing the deadline means you cannot carry forward losses to offset future income, which can significantly impact your tax liability in subsequent years. For businesses, it can also lead to complications in loan approvals and other financial transactions.

Penalties for Late Filing:

- Interest: 1% per month on the unpaid tax amount (Section 234A).

- Late Fee: ₹5,000 for income above ₹5 lakh, ₹1,000 for income below ₹5 lakh (Section 234F).

- Loss of Benefits: Inability to carry forward losses.

Calendar reminders for income tax return due dates

Calendar reminders for income tax return due dates

3. Eligibility Criteria for Filing ITR

Yes, knowing the eligibility criteria is important. You are eligible to file an ITR if your gross total income exceeds the basic exemption limit. This limit varies based on your age. For FY 2022-23 (AY 2023-24), the basic exemption limit was ₹2.5 lakh for individuals below 60 years, ₹3 lakh for senior citizens (60-80 years), and ₹5 lakh for super senior citizens (above 80 years). Filing is also mandatory if you want to claim a refund, carry forward losses, or have invested in foreign assets. Non-residents with income in India are also required to file ITR.

Who Should File ITR?

- Individuals with gross total income exceeding the basic exemption limit.

- Those seeking a tax refund.

- Individuals wanting to carry forward losses.

- Residents with assets or financial interest in entities outside India.

- Non-residents with income in India.

4. Types of ITR Forms and Their Applicability

Yes, selecting the correct ITR form is essential. The Income Tax Department has prescribed different ITR forms based on the nature of income and the category of the taxpayer. Each form caters to specific types of income and taxpayer categories.

- ITR-1 (Sahaj): For resident individuals with income from salary, one house property, other sources (interest, dividends), and agricultural income up to ₹5,000.

- ITR-2: For individuals and HUFs not eligible for ITR-1, having income from salary, more than one house property, capital gains, and foreign income.

- ITR-3: For individuals and firms having income from business or profession.

- ITR-4 (Sugam): For resident individuals, HUFs, and firms (other than LLPs) with presumptive income from business or profession.

- ITR-5: For firms, LLPs, AOPs, and BOIs.

- ITR-6: For companies not claiming exemption under Section 11.

- ITR-7: For persons including companies required to furnish returns under Sections 139(4A), 139(4B), 139(4C), or 139(4D).

ITR Form Applicability:

| ITR Form | Applicability | Income Sources |

|---|---|---|

| ITR-1 (Sahaj) | Resident individuals | Salary, one house property, other sources, agri income up to ₹5,000 |

| ITR-2 | Individuals and HUFs | Salary, more than one house property, capital gains, foreign income |

| ITR-3 | Individuals and firms | Business or profession income |

| ITR-4 (Sugam) | Resident individuals, HUFs, and firms | Presumptive income from business/profession |

| ITR-5 | Firms, LLPs, AOPs, and BOIs | All income sources |

| ITR-6 | Companies | All income sources, not claiming Section 11 exemption |

| ITR-7 | Persons under Sections 139(4A), 139(4B), 139(4C), 139(4D) | All income sources |

5. Step-by-Step Guide to Filing ITR Online

Yes, filing ITR online is a straightforward process. Filing ITR online is convenient and efficient. Here’s a step-by-step guide to help you through the process:

- Register/Login: Visit the official income tax e-filing portal and register if you are a new user. Existing users can log in using their PAN, Aadhaar, or User ID.

- Download the Correct ITR Form: Choose and download the appropriate ITR form based on your income sources.

- Fill in the Details: Fill out all the required details accurately. This includes personal information, income details, deductions, and tax payments.

- Verify the Details: Double-check all the entered information to avoid errors.

- Upload the Form: Upload the filled-out ITR form in XML or JSON format, depending on the form type.

- e-Verify: e-Verify your return using Aadhaar OTP, Net Banking, Demat Account, or Electronic Verification Code (EVC). E-verification is mandatory for processing the return.

- Acknowledgment: After successful e-verification, you will receive an acknowledgment receipt (ITR-V).

Steps to File ITR Online:

| Step | Action | Details |

|---|---|---|

| 1 | Register/Login | Use PAN, Aadhaar, or User ID |

| 2 | Download ITR Form | Choose the correct form based on income sources |

| 3 | Fill Details | Accurately enter all required information |

| 4 | Verify Details | Double-check for errors |

| 5 | Upload Form | In XML or JSON format |

| 6 | e-Verify | Use Aadhaar OTP, Net Banking, Demat Account, or EVC |

| 7 | Acknowledgment | Receive ITR-V receipt |

5.1 Documents Required for Filing ITR

Yes, having the necessary documents is crucial for accurate filing. Several documents are essential for filing your ITR accurately. These include:

- PAN Card: Essential for identification.

- Aadhaar Card: Used for verification and linking with PAN.

- Form 16: Issued by your employer, detailing the tax deducted at source (TDS).

- Salary Slips: For detailed salary breakup.

- Bank Statements: For interest income and transactions.

- Form 26AS: Shows the tax credits in your account.

- Investment Proofs: For claiming deductions under Section 80C, 80D, etc.

- Home Loan Statement: For claiming deductions on home loan interest.

- Capital Gains Statement: If you have income from the sale of property, shares, or mutual funds.

Essential Documents:

| Document | Purpose | Relevance |

|---|---|---|

| PAN Card | Identification | Mandatory |

| Aadhaar Card | Verification | Linking with PAN |

| Form 16 | TDS Details | Issued by employer |

| Salary Slips | Salary Breakup | Detailed income information |

| Bank Statements | Interest Income | Tracking interest earned |

| Form 26AS | Tax Credits | Shows tax credits in your account |

| Investment Proofs | Deduction Claims | Under Section 80C, 80D, etc. |

| Home Loan Statement | Home Loan Interest Deduction | Claiming interest deductions |

| Capital Gains Statement | Capital Gains Income | Income from sale of assets |

6. Understanding Deductions and Exemptions

Yes, understanding deductions and exemptions can significantly reduce your tax liability. Deductions and exemptions are crucial for minimizing your tax liability. Section 80C allows deductions for investments in instruments like EPF, PPF, LIC, and NSC, up to ₹1.5 lakh. Section 80D provides deductions for health insurance premiums. HRA (House Rent Allowance) exemption can be claimed if you live in a rented property. Other deductions include those under Section 80E for education loan interest and Section 80G for donations. Understanding these provisions and planning your investments and expenses accordingly can substantially lower your taxable income.

Key Deductions and Exemptions:

- Section 80C: Investments in EPF, PPF, LIC, NSC (up to ₹1.5 lakh).

- Section 80D: Health insurance premiums.

- HRA Exemption: House Rent Allowance for rented accommodation.

- Section 80E: Interest on education loan.

- Section 80G: Donations to charitable institutions.

6.1 Common Mistakes to Avoid While Filing ITR

Yes, avoiding common mistakes ensures accurate filing and reduces the risk of notices from the Income Tax Department. Common mistakes can lead to errors and potential notices from the Income Tax Department. Some of these include:

- Incorrect Personal Information: Ensure your PAN, Aadhaar, and contact details are accurate.

- Wrong ITR Form: Selecting the wrong form can lead to rejection of your return.

- Misreporting Income: Accurately report all sources of income, including interest and capital gains.

- Incorrect Deduction Claims: Ensure you have valid proofs for all deductions claimed.

- Failure to Verify Return: e-Verification is mandatory to complete the filing process.

- Not Reporting Exempt Income: Report all exempt income to reconcile with your Form 26AS.

Common Mistakes to Avoid:

| Mistake | Impact | Prevention |

|---|---|---|

| Incorrect Personal Information | Return processing delays | Double-check PAN, Aadhaar, and contact details |

| Wrong ITR Form | Rejection of return | Select the correct form based on income sources |

| Misreporting Income | Notices from IT Department | Accurately report all income sources |

| Incorrect Deduction Claims | Disallowance of deductions | Have valid proofs for all deductions |

| Failure to Verify Return | Return not processed | e-Verify the return using available methods |

| Not Reporting Exempt Income | Discrepancies with Form 26AS | Report all exempt income |

7. What if You Missed the ITR Filing Deadline?

Yes, you can still file a belated return, but it comes with penalties. If you missed the original deadline, you can file a belated return. A belated return can be filed until December 31st of the assessment year. However, it comes with penalties and interest. You will be charged interest under Section 234A at 1% per month on the outstanding tax amount. Additionally, a late fee under Section 234F will be applicable. Moreover, you cannot carry forward losses if you file a belated return.

Belated Return:

- Deadline: December 31st of the assessment year.

- Interest: 1% per month on the outstanding tax amount (Section 234A).

- Late Fee: As per Section 234F.

- Loss of Benefits: Cannot carry forward losses.

7.1 Updated Return: An Opportunity to Correct Errors

Yes, an updated return allows you to rectify mistakes or omissions in your original return. An updated return provides an opportunity to correct errors or omissions in your original return. Introduced to facilitate voluntary compliance, it allows taxpayers to update their income details and pay additional taxes, if any. You can file an updated return within two years from the end of the assessment year. However, it comes with additional tax implications. If filed within 12 months from the end of the assessment year, you need to pay an additional 25% on the tax and interest. If filed after 12 months, the additional amount increases to 50%.

Updated Return:

- Deadline: Within two years from the end of the assessment year.

- Additional Tax: 25% if filed within 12 months, 50% if filed after 12 months.

- Purpose: To correct errors or omissions.

8. Tax Planning Strategies for Individuals and Businesses

Yes, effective tax planning can help minimize your tax liability legally. Effective tax planning involves strategies to minimize your tax liability while staying compliant with tax laws. For individuals, this includes investing in tax-saving instruments under Section 80C, claiming HRA exemption, and utilizing deductions under Section 80D and 80G. For businesses, it involves optimizing operational expenses, claiming depreciation, and utilizing available tax incentives and rebates. According to a study by the University of Texas at Austin’s McCombs School of Business, strategic tax planning can reduce a company’s effective tax rate by up to 5%. Therefore, both individuals and businesses should seek professional advice to optimize their tax planning strategies.

Tax Planning Strategies:

| Category | Strategy | Benefits |

|---|---|---|

| Individuals | Investments under Section 80C | Reduces taxable income up to ₹1.5 lakh |

| HRA Exemption | Reduces tax on rental income | |

| Deductions under Section 80D and 80G | Reduces taxable income through health insurance and donations | |

| Businesses | Optimizing Operational Expenses | Reduces taxable income |

| Claiming Depreciation | Reduces tax liability on assets | |

| Utilizing Tax Incentives and Rebates | Reduces overall tax burden |

9. Understanding Advance Tax and Its Implications

Yes, understanding advance tax is essential to avoid interest penalties. Advance tax is the income tax you pay in advance during the financial year, rather than as a lump sum at the end. If your estimated tax liability for a financial year exceeds ₹10,000, you are required to pay advance tax. It is paid in installments as per the due dates prescribed by the Income Tax Department. Failing to pay advance tax or paying less than the required amount can lead to interest under Section 234B and 234C. For FY 2022-23, the due dates and percentages of advance tax to be paid were:

| Due Date | Percentage of Advance Tax to be Paid |

|---|---|

| June 15 | 15% |

| September 15 | 45% |

| December 15 | 75% |

| March 15 | 100% |

Advance Tax:

- Applicability: Estimated tax liability exceeds ₹10,000.

- Installments: Paid in installments as per prescribed due dates.

- Consequences of Non-Payment: Interest under Section 234B and 234C.

10. Seeking Professional Help for ITR Filing

Yes, seeking professional help ensures accurate filing and optimized tax planning. Filing ITR can be complex, especially for individuals and businesses with multiple income sources and deductions. Consulting a tax professional can ensure accurate filing, optimized tax planning, and compliance with tax laws. Tax professionals can provide personalized advice based on your specific financial situation and help you navigate complex tax provisions. They can also assist in identifying eligible deductions and exemptions, reducing your tax liability. According to a survey by the National Association of Tax Professionals, taxpayers who use a professional tax preparer are more likely to claim all eligible deductions and credits, resulting in significant tax savings.

Benefits of Seeking Professional Help:

- Accurate Filing: Ensures accurate reporting of income and deductions.

- Optimized Tax Planning: Personalized advice based on your financial situation.

- Compliance with Tax Laws: Avoids penalties and notices from the Income Tax Department.

- Identification of Deductions and Exemptions: Maximizes tax savings.

11. Tax Implications of Partnership Firms

Yes, partnership firms have specific tax implications. Partnership firms are taxed differently from individual taxpayers. The firm is assessed as a separate entity, and its income is taxed at a flat rate. Partners are also taxed on their share of the firm’s income. The Income Tax Act provides specific provisions for the taxation of partnership firms, including deductions for salary and interest paid to partners, subject to certain conditions. Understanding these provisions is crucial for effective tax planning for partnership firms. According to the Harvard Business Review, a well-structured partnership agreement that addresses tax implications can significantly enhance the firm’s profitability and sustainability.

Tax Implications for Partnership Firms:

- Taxation as a Separate Entity: The firm is taxed at a flat rate.

- Taxation of Partners: Partners are taxed on their share of the firm’s income.

- Deductions for Salary and Interest: Subject to specific conditions.

- Importance of Partnership Agreement: Addressing tax implications in the agreement is crucial.

12. Frequently Asked Questions (FAQs) about ITR Filing

Here are some frequently asked questions about Income Tax Return (ITR) filing to clarify common doubts and provide helpful insights.

12.1 What is the last date to file ITR for AY 2023-24?

The last date to file ITR for individuals and non-audit cases was July 31, 2023. However, belated returns could be filed until December 31, 2023, with applicable penalties.

12.2 What happens if I miss the ITR filing deadline?

If you miss the ITR filing deadline, you will be liable to pay interest under Section 234A and a late fee under Section 234F. Additionally, you will not be able to carry forward losses.

12.3 Can I file ITR online?

Yes, you can file ITR online through the official income tax e-filing portal. This method is convenient and efficient.

12.4 What documents do I need to file ITR?

You need documents such as PAN card, Aadhaar card, Form 16, salary slips, bank statements, Form 26AS, investment proofs, home loan statement, and capital gains statement.

12.5 How can I claim deductions under Section 80C?

You can claim deductions under Section 80C by investing in instruments like EPF, PPF, LIC, and NSC, up to a maximum of ₹1.5 lakh.

12.6 What is advance tax, and who is required to pay it?

Advance tax is the income tax you pay in advance during the financial year. If your estimated tax liability exceeds ₹10,000, you are required to pay advance tax.

12.7 Can I revise my ITR if I made a mistake?

Yes, you can file an updated return to correct errors or omissions in your original return, within two years from the end of the assessment year, with additional tax implications.

12.8 Is it mandatory to e-verify my ITR?

Yes, e-verification is mandatory for processing your ITR. You can use Aadhaar OTP, Net Banking, Demat Account, or Electronic Verification Code (EVC) for e-verification.

12.9 What are the different types of ITR forms, and which one should I use?

The different types of ITR forms include ITR-1, ITR-2, ITR-3, ITR-4, ITR-5, ITR-6, and ITR-7. The form you should use depends on your income sources and taxpayer category.

12.10 How can a tax professional help with ITR filing?

A tax professional can ensure accurate filing, optimized tax planning, and compliance with tax laws. They can provide personalized advice based on your specific financial situation and help you navigate complex tax provisions.

13. Why Partnering with Income-Partners.Net Can Simplify Your Tax Journey

Navigating the complexities of income tax returns can be daunting, but you don’t have to do it alone. At income-partners.net, we understand the challenges faced by individuals and businesses in managing their tax obligations. Our platform offers a wealth of information, strategies, and opportunities to connect with partners who can help streamline your tax processes, optimize your financial planning, and unlock new avenues for income growth.

13.1 Access to Expert Resources and Guidance

Income-partners.net provides access to a diverse range of resources, including articles, guides, and expert insights on tax planning, compliance, and optimization. Whether you’re looking to understand the latest tax laws, identify eligible deductions, or develop a comprehensive tax strategy, our platform has you covered.

13.2 Strategic Partnerships for Enhanced Financial Outcomes

We believe that collaboration is key to success. That’s why income-partners.net is designed to connect you with strategic partners who can complement your skills, resources, and expertise. By joining forces with the right partners, you can:

- Expand your reach and market share: Access new customer segments and geographic regions through established partner networks.

- Diversify your income streams: Explore new business ventures and revenue models through collaborative projects.

- Optimize your tax strategies: Work with financial experts to identify tax-saving opportunities and ensure compliance.

13.3 Real-World Success Stories

Don’t just take our word for it. Here are a few examples of how partnerships facilitated through income-partners.net have led to tangible results:

- Case Study 1: A small business owner partnered with a marketing agency to increase brand awareness and drive sales. As a result, they experienced a 30% increase in revenue and were able to invest more in tax-efficient retirement plans.

- Case Study 2: A freelance consultant collaborated with a financial advisor to develop a personalized tax strategy. By maximizing deductions and optimizing investment decisions, they reduced their tax liability by 20% and secured their financial future.

- Case Study 3: A tech startup partnered with a venture capital firm to secure funding for expansion. With the additional capital, they were able to hire a dedicated tax team, ensuring compliance and maximizing tax benefits.

These are just a few examples of the countless success stories that have emerged from partnerships forged on income-partners.net.

13.4 Call to Action

Ready to unlock the power of collaboration and take control of your financial future? Visit income-partners.net today to:

- Explore a diverse range of partnership opportunities: Discover potential collaborators who align with your goals and values.

- Access expert resources and guidance: Learn from industry leaders and gain valuable insights into tax planning, financial management, and business growth.

- Connect with a supportive community: Network with like-minded individuals and build lasting relationships that can propel your success.

Don’t let tax season be a source of stress and anxiety. Partner with income-partners.net and experience the benefits of collaboration, knowledge, and strategic financial planning. Your journey to financial success starts here.

By understanding the various aspects of ITR filing, staying informed about the latest updates, and seeking professional help when needed, you can manage your tax obligations effectively and optimize your financial planning.

Address: 1 University Station, Austin, TX 78712, United States

Phone: +1 (512) 471-3434

Website: income-partners.net