Are Scholarships Considered Unearned Income? Yes, scholarships are generally considered unearned income to the extent they exceed qualified education expenses, potentially affecting students’ tax obligations, especially with the kiddie tax rules. Understanding this distinction is crucial for students and their families to navigate financial aid and tax planning effectively, and at income-partners.net, we provide the expertise you need to optimize your partnership strategies for increased income. Let’s delve into the specifics to help you reduce your taxable income and boost your partnership potential, exploring options such as strategic collaborations and revenue-sharing arrangements.

1. What Qualifies As a Taxable Scholarship?

In general, scholarships are excluded from gross income under Sec. 117 if they are used for qualified tuition and related expenses. But what happens when scholarships are used for expenses that go beyond that? Let’s explore.

Qualified Tuition and Related Expenses

The IRS defines qualified tuition and related expenses as the costs for:

- Tuition

- Fees

- Books

- Supplies

- Equipment required for enrollment or attendance at an educational institution

Scholarship funds used for these specific items are typically tax-free, promoting access to education and helping students focus on their studies rather than worrying about immediate tax implications.

Non-Qualified Expenses and Tax Implications

Any portion of a scholarship used for non-qualified expenses is considered taxable income. These typically include:

- Room and Board: Housing and meals, even if living on campus, are not considered qualified educational expenses.

- Travel: Expenses for traveling to and from school.

- Incidental Expenses: Costs that aren’t required for enrollment or attendance, such as optional textbooks or personal items.

When scholarships cover these non-qualified expenses, the amount spent is considered unearned income, which could be subject to federal income tax.

Example:

Imagine a student receives a $20,000 scholarship. $15,000 covers tuition and required fees, while the remaining $5,000 is allocated for room and board. In this case, the $15,000 used for tuition and fees is tax-free. However, the $5,000 used for room and board is considered taxable unearned income.

The Quid Pro Quo Exception: Scholarships Requiring Service

The IRS provides exceptions for scholarships that require students to perform certain services, such as participating in athletic programs or musical ensembles. Scholarships that require students to provide a service that is a quid pro quo are generally not included in gross income.

Considerations for Service-Based Scholarships

- Rev. Rul. 77-263: This IRS ruling is based on the U.S. Supreme Court’s decision in Bingler v. Johnson, which held that compensation exists if there is a quid pro quo relationship between the parties.

- Heidel Case: A Tax Court case involving a student who would continue to receive a scholarship even if the student did not participate in the sport because of injury or lack of desire.

- IRS Stance: Currently, the IRS has chosen not to press the issue.

Tax Form 1098-T: Tuition Statement

Every eligible educational institution is required to file a Form 1098-T for each enrolled student who has a reportable transaction. This form helps students determine the amount of qualified tuition and related expenses paid during the year, as well as the amount of scholarships or grants received.

- Box 1: Reports the amounts received as payment for qualified tuition and related expenses.

- Box 5: Reports all scholarships or grants administered by the institution.

Using Form 1098-T, students can calculate the amount of their scholarship that exceeds qualified tuition and may be considered taxable income.

Strategic Insight

While the IRS currently has a lenient approach towards these arrangements, it’s worth bearing in mind that a court might view the holding in Bingler as not applicable, especially in the case of large athletic programs where student-athletes receive full tuition, room and board, and additional funds for their participation. In such cases, a court could find that the funds the student-athlete received were earned income that must be included in gross income rather than nontaxable scholarship payments.

2. What is the Kiddie Tax and How Does it Relate to Scholarships?

The “kiddie tax” applies to unearned income for children, taxing it at estate and trust tax rates, which can be higher than the child’s individual tax rate. The Tax Cuts and Jobs Act (TCJA) changed the kiddie tax, potentially increasing the tax liability on taxable scholarship income.

Understanding Earned vs. Unearned Income

- Earned Income: Includes wages, salaries, professional fees, and other amounts received as compensation for personal services.

- Unearned Income: Includes income from dividends, interest, royalties, capital gains, and taxable scholarship income not reported on Form W-2.

Key Aspects of the Kiddie Tax

- History: Introduced in 1986, it initially applied to children under 14. Over time, it has expanded to include some college students up to age 23.

- TCJA Impact: The Tax Cuts and Jobs Act (TCJA) changed the tax rate for the kiddie tax. Instead of being taxed at the parent’s top marginal tax rate, the child’s unearned income is now taxed at rates applicable to estates and trusts, potentially increasing the tax liability.

- Form 8615: This form is used to calculate the kiddie tax. Under the TCJA, it no longer requires the child to include taxable income of the parent or other qualifying children.

When Does the Kiddie Tax Apply?

The kiddie tax applies if the child:

- Is under 18 years old; or is 18 and their earned income is less than half of their support; or is between 19 and 23, a full-time student, and their earned income is less than half of their support.

- Has at least one living parent.

- Is not married and filing a joint return.

- Has unearned income exceeding $2,100 (in 2018).

Scholarships, though taxable in some cases, are not counted toward the child’s own support when determining eligibility for the kiddie tax.

Tax Rate Implications

The kiddie tax uses the modified estate and trust tax rates, which can climb quickly:

- Up to $2,600: Taxed at 10%

- $2,601 to $9,300: Taxed at 24%

- $9,301 to $12,750: Taxed at 35%

- Over $12,750: Taxed at 37%

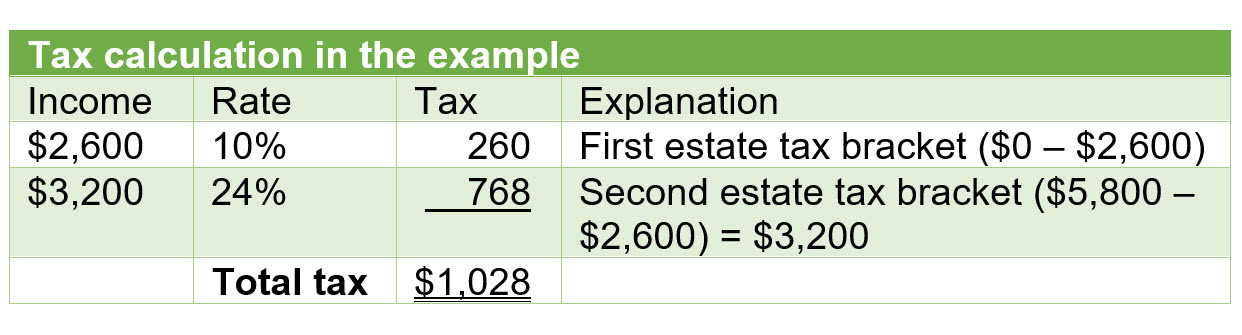

Example: Kiddie Tax Impact on Scholarship Income

Consider a full-time student who receives a $50,000 scholarship to attend a private liberal arts school. Qualified tuition and fees are $32,000, while room and board and other unqualified expenses total $18,000. Here’s how the kiddie tax could apply:

- The $32,000 used for qualified tuition and fees is tax-free.

- The $18,000 used for room and board is considered unearned income.

- The student’s gross income is $18,000.

- The standard deduction for a dependent is $12,200 (the lesser of the maximum standard deduction for a single individual or the student’s earned income for standard deduction purposes, which includes any taxable scholarship amount, plus $350).

- Taxable income is $5,800.

- The $5,800 is taxed using the modified estate and trust tax tables.

Strategic Insight

The TCJA changes have made the kiddie tax more complex, potentially increasing the tax liability for students with taxable scholarship income. While the new rules may benefit those with parents in higher tax brackets, they can be unfavorable for those with parents in lower tax brackets and a larger amount of unearned income.

3. How Can You Minimize the Taxable Portion of Scholarships?

Students can reduce their tax liability from scholarships by documenting all qualified education expenses, adjusting scholarship amounts, and strategically managing other sources of unearned income.

Documenting Qualified Education Expenses

Students should keep detailed records of all expenses that qualify as tuition and related expenses. This includes:

- Tuition statements

- Receipts for required books and supplies

- Any other mandatory fees

Adjusting Scholarship Amounts

When possible, students can work with the educational institution to adjust the amount of the scholarship allocated to qualified tuition and related expenses. This can help minimize the portion of the scholarship considered taxable income.

Strategic Planning for Unearned Income

For students affected by the kiddie tax, it’s essential to manage and reduce all sources of unearned income. Strategies include:

- Shifting Income to Nontaxable Accounts: Contribute to tax-advantaged accounts, such as Roth IRAs.

- Deferring Income: Defer income to a period when the student is no longer subject to the kiddie tax.

- Recognizing Losses: Offset unearned income with capital losses or other deductible expenses.

Leveraging Partnerships for Tax Optimization

Partnering with other entities can provide avenues for reducing taxable income. Consider these strategies:

- Strategic Alliances: Collaborate with companies that offer tax-advantaged benefits, such as educational assistance programs.

- Joint Ventures: Engage in ventures that allow for the deferral or reduction of taxable income.

Tax Planning Resources

Consulting with a tax professional can provide personalized strategies for minimizing the tax impact of scholarships and unearned income. Income-partners.net provides resources and expertise to help students and families navigate these complex issues.

Real-World Example:

A student receives a $40,000 scholarship. Qualified tuition and fees are $25,000, and room and board are $15,000. By meticulously documenting $2,000 in additional required books and equipment, the student can reduce the taxable portion of the scholarship to $13,000.

Strategic Insight

Maximizing qualified education expenses and strategically managing unearned income can significantly reduce the tax liability for students receiving scholarships. Partnering with experts can provide additional opportunities for tax optimization.

4. How Does Form 1098-T Assist in Calculating Taxable Scholarship Income?

Form 1098-T, issued by educational institutions, provides key information for calculating taxable scholarship income, though it may not always capture the full picture due to certain exceptions and reporting limitations.

Understanding Form 1098-T

Form 1098-T, Tuition Statement, is an informational form that eligible educational institutions are required to file for each student enrolled who has a reportable transaction. This form helps students and their families determine the amount of qualified tuition and related expenses paid during the year, as well as the amount of scholarships or grants received.

- Box 1: Payments Received for Qualified Tuition and Related Expenses: This box reports the amounts received as payment for qualified tuition and related expenses less any reimbursements or refunds made during the calendar year.

- Box 5: Scholarships or Grants: This box includes the total amount of scholarships or grants administered and processed by the institution during the calendar year. This includes payments received directly by the institution, or checks endorsed by the student.

Limitations of Form 1098-T

While Form 1098-T is a valuable tool, it has several limitations that can make calculating taxable scholarship income more challenging:

- Exceptions to Filing: Educational institutions are not required to file Form 1098-T in certain situations, such as when courses are taken for no academic credit, for nonresident alien students, or when qualified tuition is paid in full by scholarships or waivers.

- Incomplete Scholarship Information: The form may not include all scholarships received by the student, particularly if the student receives funds directly and the institution is unaware of them.

- Timing Differences: The amounts reported on Form 1098-T may not align perfectly with the student’s tax year due to timing differences in when payments are received and when expenses are incurred.

Calculating Taxable Scholarship Income Using Form 1098-T

In an ideal scenario, where the educational institution accurately completes Form 1098-T, the amount of taxable scholarship income can be calculated by subtracting the amount reported in Box 1 (qualified tuition and related expenses) from the amount reported in Box 5 (scholarships or grants).

Example:

A student receives Form 1098-T with the following information:

- Box 1 (Qualified Tuition and Related Expenses): $15,000

- Box 5 (Scholarships or Grants): $20,000

In this case, the taxable scholarship income would be $5,000 ($20,000 – $15,000).

When Form 1098-T Is Insufficient

When Form 1098-T does not provide a complete picture, students may need to gather additional information to accurately calculate their taxable scholarship income. This can include:

- Student Account Details: Obtain a detailed statement from the college or university showing all charges (tuition, fees, room and board, books) and financial aid received.

- Records of Additional Expenses: Compile receipts for any qualified education expenses not billed through the educational institution, such as required textbooks purchased separately.

- Information on Outside Scholarships: Keep records of any scholarships received directly from outside organizations, which may not be reported to the institution.

Strategic Insight

While Form 1098-T is a helpful starting point, students should not rely on it exclusively for calculating their taxable scholarship income. Gathering additional documentation and consulting with a tax professional can ensure accuracy and help minimize potential tax liabilities.

Tax calculation in the example

Tax calculation in the example

Image alt: Kiddie tax example with tax calculation.

5. What Strategies Can Reduce Unearned Income from Scholarships?

Strategies to reduce unearned income from scholarships include identifying additional qualified education expenses, coordinating scholarship amounts with tuition costs, and managing other sources of unearned income.

Identifying Additional Qualified Education Expenses

Students can reduce the taxable portion of their scholarships by identifying additional expenses that qualify as tuition and related expenses. According to IRS regulations, allowable expenses must be required of all students in the course and cannot be considered incidental.

Examples of Qualified Expenses

- Required Textbooks and Supplies: If a textbook is listed as required on the course syllabus, its cost qualifies as an educational expense.

- Mandatory Equipment: Equipment required for enrollment or attendance at the institution.

- Lab Fees and Other Mandatory Fees: Fees required for specific courses or programs.

Non-Qualified Expenses to Avoid

- Optional Textbooks: Textbooks listed as optional on the syllabus do not qualify.

- Incidental Expenses: Costs associated with room and board, travel, and personal items.

- Equipment Not Required: Equipment that is not mandatory for enrollment or attendance.

Strategic Insight

Understanding the distinction between qualified and non-qualified expenses is key to minimizing taxable scholarship income.

Coordinating Scholarship Amounts with Tuition Costs

Students can work with their educational institution to coordinate the amount of the scholarship with the actual cost of tuition and related expenses. If the scholarship exceeds these costs, students can request a reduction in the scholarship amount or allocate the excess funds to future semesters.

Managing Other Sources of Unearned Income

Since unearned income may come from other sources, taxpayers affected by the kiddie tax should seek ways to reduce their overall unearned income. This can be achieved through various strategies, including:

- Shifting Income to Nontaxable Accounts: Contributing to retirement accounts like Roth IRAs.

- Deferring Income to Future Years: Delaying the receipt of income to a period when the taxpayer is not subject to the kiddie tax.

- Recognizing Losses: Offsetting unearned income with capital losses or other deductible expenses.

Strategic Insight

Reducing overall unearned income is essential for minimizing the impact of the kiddie tax. Partnering with financial advisors can provide personalized strategies for managing unearned income.

6. What Are the Recent Changes to the Kiddie Tax and How Do They Impact Students?

Recent changes to the kiddie tax, particularly those introduced by the Tax Cuts and Jobs Act (TCJA), have significantly altered how unearned income is taxed for children, including students receiving scholarships.

Overview of the Kiddie Tax Changes Under TCJA

Before the TCJA, the kiddie tax applied to the unearned income of children under age 18, taxing it at their parents’ marginal tax rate. The TCJA changed this by taxing the child’s unearned income at the rates used for trusts and estates. This change was designed to simplify the tax process by removing the need to consider the parents’ tax situation.

How the New Rules Work

Under the TCJA, the unearned income of a child is taxed as follows:

- The first $1,100 (in 2020) is tax-free.

- The next $1,100 is taxed at the child’s tax rate.

- Any amount over $2,200 is taxed at trust and estate tax rates, which can be higher than the child’s individual income tax rates.

Impact on Scholarship Income

The changes to the kiddie tax can significantly impact students receiving scholarships that cover non-qualified expenses, such as room and board. Since these amounts are considered unearned income, they are subject to the kiddie tax rules.

Example: Kiddie Tax Before and After TCJA

Before TCJA:

- Child with $5,000 of unearned income.

- Parents in the 37% tax bracket.

- The child’s unearned income would be taxed at 37%.

After TCJA:

- Child with $5,000 of unearned income.

- The first $2,200 is taxed at the child’s rate or is tax-free, and the remaining $2,800 is taxed at trust and estate rates, which could range from 10% to 37%, depending on the income level.

Strategic Insight

The TCJA changes to the kiddie tax may result in higher tax liabilities for some students, particularly those with significant unearned income and parents in lower tax brackets.

7. How Does the Source of Scholarship Funding Affect Its Taxability?

The source of scholarship funding—whether from private, institutional, or government entities—generally does not affect its taxability, as the primary determinant is whether the funds are used for qualified education expenses.

Scholarship Funding Sources

- Private Scholarships: These are awarded by private organizations, foundations, or individuals.

- Institutional Scholarships: These are provided directly by colleges or universities.

- Government Scholarships: These are funded by federal, state, or local government entities.

IRS Guidelines

The IRS focuses on the purpose for which the scholarship funds are used, not the source of the funding. As long as the funds are used for qualified education expenses, they are generally tax-free, regardless of whether the scholarship comes from a private donor, the university itself, or a government agency.

Taxability Factors

- Qualified Education Expenses: If the scholarship funds are used for tuition, fees, books, supplies, and equipment required for enrollment or attendance, they are generally tax-free.

- Non-Qualified Expenses: If the funds are used for room and board, travel, or other non-qualified expenses, they are considered taxable income.

- Service Requirements: Scholarships that require the student to perform services as a condition of receiving the funds may be treated differently, depending on the nature of the service and whether it is considered compensation.

Specific Scholarship Types and Taxability

- ROTC Scholarships: These scholarships often cover tuition and fees and may also provide a stipend for living expenses. The portion used for tuition and fees is generally tax-free, while the stipend may be taxable.

- Athletic Scholarships: These scholarships typically cover tuition, fees, room and board, and other expenses. The portion used for tuition and fees is generally tax-free, while the portion used for room and board may be taxable.

- Merit-Based Scholarships: These scholarships are awarded based on academic achievement or other merit criteria. The taxability depends on whether the funds are used for qualified education expenses.

- Need-Based Scholarships: These scholarships are awarded based on financial need. The taxability depends on whether the funds are used for qualified education expenses.

Strategic Insight

The source of scholarship funding does not typically affect its taxability. The critical factor is how the funds are used. Consulting with a tax advisor can help students understand the specific tax implications of their scholarships.

8. How Do State Tax Laws Impact the Taxability of Scholarships?

State tax laws can influence the taxability of scholarships, potentially differing from federal guidelines, which can add complexity to tax planning for students and families.

State Tax Conformity

Many states conform to federal tax laws, meaning they follow the same rules for determining taxable income, including the taxability of scholarships. However, some states may have their own unique rules or may offer additional deductions or credits related to education expenses.

States with Unique Tax Laws

- California: California generally conforms to federal tax law but may have some differences in deductions and credits.

- New York: New York also generally conforms but offers its own set of deductions and credits, including those related to education.

- Pennsylvania: Pennsylvania does not tax scholarship income, regardless of whether it is used for qualified education expenses.

- New Jersey: New Jersey generally follows federal guidelines but may have specific provisions related to education tax benefits.

Impact on Tax Planning

The differences in state tax laws can significantly impact tax planning for students and families. It is essential to understand both federal and state tax rules to accurately calculate taxable income and take advantage of available tax benefits.

Example: Pennsylvania vs. Federal Tax Law

- Federal Law: A student receives a $10,000 scholarship, with $6,000 used for tuition and $4,000 for room and board. Under federal law, $4,000 is taxable income.

- Pennsylvania State Law: The same student would not have any taxable income from the scholarship, as Pennsylvania does not tax scholarship income.

Strategic Insight

State tax laws can significantly impact the taxability of scholarships. Students should consult with a tax advisor to understand the specific rules in their state and to optimize their tax planning strategies.

9. Are There Any Specific Types of Scholarships That Are Always Tax-Free?

Certain types of scholarships are generally tax-free if they meet specific criteria, primarily related to the use of funds for qualified education expenses and the recipient’s status as a degree candidate.

General Rule for Tax-Free Scholarships

To be considered tax-free, a scholarship must meet the following criteria:

- Qualified Education Expenses: The scholarship must be used for tuition, fees, books, supplies, and equipment required for enrollment or attendance at an eligible educational institution.

- Degree Candidate: The recipient must be a candidate for a degree at the educational institution.

- No Service Requirement: The scholarship should not require the student to perform services as a condition of receiving the funds (unless the service is part of a comprehensive student work-learning-service program).

Specific Scholarship Types

- Tuition-Specific Scholarships: Scholarships that are specifically designated for tuition and mandatory fees are generally tax-free if the student uses the funds accordingly.

- Federal Government Scholarships: Certain scholarships funded by the federal government, such as those through the National Health Service Corps Scholarship Program or the Armed Forces Health Professions Scholarship and Financial Assistance Program, may have special tax considerations.

- Qualified Tuition Reductions: Qualified tuition reductions for graduate students who perform teaching or research activities for an eligible educational institution are tax-free.

- Veteran’s Education Benefits: Payments received through the Department of Veterans Affairs that are used to pay for education or training, such as funds received under the GI Bill, are not included in income.

Scholarships with Potential Tax Implications

- Room and Board Scholarships: Scholarships that cover room and board expenses are generally taxable, as these are not considered qualified education expenses.

- Travel Scholarships: Scholarships that cover travel expenses are also generally taxable.

- Scholarships Requiring Service: Scholarships that require the student to perform services may be considered taxable income, depending on the nature and extent of the service requirement.

Strategic Insight

While certain types of scholarships are generally tax-free if they meet specific criteria, it is essential to understand the specific terms and conditions of each scholarship to determine its taxability. Consulting with a tax advisor can provide clarity and help students avoid potential tax liabilities.

10. What Records Should Students Keep to Substantiate Scholarship Expenses for Tax Purposes?

Maintaining thorough records of scholarship expenses is crucial for students to substantiate their claims for tax purposes, ensuring they can accurately report and potentially reduce their taxable income.

Essential Records to Keep

- Scholarship Award Letters: Keep copies of all scholarship award letters, which detail the amount of the scholarship, the terms and conditions, and any restrictions on how the funds can be used.

- Tuition Bills and Statements: Save all tuition bills and statements from the educational institution, which show the amount of tuition and fees charged for each academic period.

- Receipts for Books and Supplies: Keep receipts for all books, supplies, and equipment purchased for courses, ensuring that the items are required for enrollment or attendance.

- Form 1098-T: Retain copies of Form 1098-T, Tuition Statement, received from the educational institution, which reports the amount of qualified tuition and related expenses paid, as well as the amount of scholarships or grants received.

- Bank Statements: Save bank statements that show the deposit of scholarship funds and the payment of qualified education expenses.

- Course Syllabi: Keep copies of course syllabi, which list required textbooks and materials, as these can help substantiate the expenses.

- Records of Other Expenses: Maintain records of any other expenses that may qualify as education expenses, such as lab fees or mandatory equipment costs.

How to Organize Records

- Digital Copies: Scan and save digital copies of all documents in a secure location, such as a cloud storage service or an encrypted hard drive.

- Physical Files: Create physical files for each tax year, storing all relevant documents in a well-organized manner.

- Spreadsheets: Use spreadsheets to track scholarship funds received and expenses paid, categorizing the expenses as qualified or non-qualified.

Strategic Insight

Maintaining thorough and organized records is essential for substantiating scholarship expenses and accurately reporting taxable income. Consulting with a tax advisor can provide guidance on record-keeping best practices and ensure compliance with tax laws.

At income-partners.net, we understand the complexities of financial aid and tax planning. We offer strategies to leverage partnerships for income growth and provide resources to navigate the tax implications of scholarships. Connect with us today to explore opportunities for financial empowerment through strategic alliances and expert guidance. Address: 1 University Station, Austin, TX 78712, United States. Phone: +1 (512) 471-3434. Website: income-partners.net.

Ready to explore partnership opportunities that boost your income? Visit income-partners.net now and discover how strategic collaborations can transform your financial future. Don’t miss out—unlock your potential today

Frequently Asked Questions (FAQ)

1. Are all scholarships considered taxable income?

No, not all scholarships are taxable. Scholarships used for qualified education expenses like tuition and fees are generally tax-free.

2. What are qualified education expenses?

Qualified education expenses include tuition, fees, books, supplies, and equipment required for enrollment or attendance at an educational institution.

3. What happens if my scholarship covers room and board?

Scholarship funds used for room and board are generally considered taxable income.

4. How does the kiddie tax affect scholarship income?

The kiddie tax can affect the tax liability on unearned income, including taxable scholarship income, for children under certain age and dependency criteria.

5. What is Form 1098-T and how does it relate to scholarships?

Form 1098-T reports the amount of qualified tuition and related expenses paid and the amount of scholarships or grants received during the year, helping students calculate their taxable scholarship income.

6. Can I reduce the amount of taxable scholarship income?

Yes, you can reduce taxable scholarship income by documenting additional qualified education expenses and managing other sources of unearned income.

7. Does the source of scholarship funding affect its taxability?

No, the source of scholarship funding does not typically affect its taxability; the key factor is how the funds are used.

8. What records should I keep to substantiate scholarship expenses for tax purposes?

Keep scholarship award letters, tuition bills, receipts for books and supplies, Form 1098-T, and bank statements to substantiate your scholarship expenses.

9. Are there any scholarships that are always tax-free?

Scholarships specifically designated for tuition and mandatory fees are generally tax-free if the student uses the funds accordingly and meets other criteria.

10. How do state tax laws impact the taxability of scholarships?

State tax laws can differ from federal guidelines, potentially affecting the taxability of scholarships, so it’s essential to understand both federal and state rules.