Are Rsus Taxed As Income? Yes, Restricted Stock Units (RSUs) are indeed taxed as income when they vest, not when they are granted, and understanding this is critical for effective financial planning. At income-partners.net, we’re here to guide you through the intricacies of RSU taxation, offering strategies to optimize your tax liabilities and maximize your wealth-building potential through strategic partnerships and income opportunities. This article will clarify how RSUs are taxed and show you how to make informed decisions, potentially leading to greater financial benefits and smarter tax planning.

1. What are Restricted Stock Units (RSUs)?

Restricted Stock Units (RSUs) are a form of equity compensation where an employee receives company shares after meeting certain vesting requirements. Unlike stock options, RSUs represent an actual grant of company stock, contingent on fulfilling specific conditions, such as staying with the company for a defined period. This makes them a popular incentive, especially in high-growth sectors like technology, aligning employee interests with the company’s long-term success. RSUs bridge the gap between performance and ownership, encouraging employees to contribute to the company’s growth while also providing them with a stake in its future.

1.1 How RSUs Work

RSUs are essentially a promise of company stock to be delivered at a future date, contingent upon the employee meeting specific vesting requirements, typically continued employment. The employee does not receive the shares immediately upon grant but rather earns them over time. This vesting schedule encourages employees to stay with the company, fostering stability and continuity. Once the vesting conditions are met, the shares are transferred to the employee, who then owns them outright and can sell them at their discretion. The value of RSUs is directly tied to the company’s stock price, providing employees with a tangible incentive to contribute to the company’s success. According to research from the University of Texas at Austin’s McCombs School of Business, in July 2025, RSUs can be a powerful tool for employee retention and motivation.

1.2 Key Features of RSUs

RSUs come with several key features that distinguish them from other forms of equity compensation.

- Vesting Schedule: RSUs vest according to a predetermined schedule, which specifies when the employee will receive the shares.

- Taxation: RSUs are taxed as ordinary income when they vest, based on the fair market value of the shares at that time.

- No upfront cost: Unlike stock options, employees do not need to purchase RSUs, making them a less risky form of compensation.

- Dividend equivalents: Some companies offer dividend equivalents, which provide employees with payments equal to the dividends paid on the underlying stock during the vesting period.

- Flexibility: RSUs can be customized to fit the company’s specific compensation goals and the employee’s individual circumstances.

Understanding these features is essential for employees to fully appreciate the value of their RSU grants and plan their finances accordingly.

2. Are RSUs Taxed as Income?

Yes, RSUs are taxed as ordinary income when they vest. When your RSUs vest, the fair market value of the shares at that time is considered part of your taxable income, which is subject to federal, state, and local income taxes, as well as Social Security and Medicare taxes. Unlike stock options, where taxation typically occurs upon exercise, RSUs are taxed upon vesting, regardless of whether you sell the shares immediately or not. The tax liability arises because the vested shares represent compensation for services rendered, making them subject to income tax.

2.1 Tax Implications at Vesting

When RSUs vest, the tax implications can be significant, especially for high-income earners. The fair market value of the shares at vesting is added to your taxable income for the year, which can potentially push you into a higher tax bracket. This means you could end up paying a higher percentage of your overall income in taxes. In addition to federal income tax, RSUs are also subject to state and local income taxes, as well as Social Security and Medicare taxes. It’s important to factor in all of these taxes when calculating your overall tax liability.

Consider a scenario where an employee receives 1,000 RSUs that vest when the company’s stock price is $50 per share. In this case, the employee would have $50,000 of additional taxable income, which could significantly increase their tax burden. It’s essential to understand these tax implications and plan accordingly to avoid any surprises come tax time.

2.2 Tax Implications When Selling Shares

In addition to the tax implications at vesting, there are also tax implications when you eventually sell the shares. If you sell the shares for more than their fair market value at vesting, you’ll realize a capital gain, which is subject to capital gains tax. The capital gains tax rate depends on how long you hold the shares before selling them. If you hold the shares for more than one year, you’ll be subject to long-term capital gains tax rates, which are generally lower than ordinary income tax rates. If you hold the shares for one year or less, you’ll be subject to short-term capital gains tax rates, which are the same as your ordinary income tax rates.

Conversely, if you sell the shares for less than their fair market value at vesting, you’ll realize a capital loss, which can be used to offset capital gains. If your capital losses exceed your capital gains, you can deduct up to $3,000 of capital losses per year against your ordinary income. It’s important to keep track of your cost basis (the fair market value at vesting) and your sale price to accurately calculate your capital gains or losses.

2.3 Understanding the Tax Form 1099-B

When you sell shares acquired through RSUs, you’ll receive a Form 1099-B from your brokerage firm, which reports the details of the sale to the IRS. This form includes information such as the date of the sale, the number of shares sold, the sale price, and your cost basis. It’s crucial to review this form carefully to ensure that the information is accurate. If you notice any discrepancies, contact your brokerage firm immediately to have them corrected. The Form 1099-B is essential for accurately reporting your capital gains or losses on your tax return.

3. Strategies to Optimize Taxes on RSUs

Managing the tax implications of RSUs requires careful planning and a proactive approach. Several strategies can help you optimize your tax liabilities and maximize the value of your RSU grants. These strategies include timing the sale of RSUs, charitable contributions, tax-loss harvesting, and diversification. By implementing these strategies, you can minimize the impact of taxes on your overall financial situation.

3.1 Timing the Sale of RSUs

One of the most effective strategies for optimizing taxes on RSUs is to carefully time the sale of your shares. Selling your shares immediately after they vest can minimize the risk of paying higher taxes on potential gains if the stock price increases. By selling immediately, you’ll only be subject to ordinary income tax on the fair market value of the shares at vesting. However, if you believe the company’s stock price will continue to rise, you may choose to hold onto the shares for a longer period.

If you hold the shares for more than one year before selling, any gains will be taxed at the long-term capital gains tax rates, which are generally lower than ordinary income tax rates. This can result in significant tax savings, especially if you’re in a high-income tax bracket. However, holding onto the shares also carries the risk of the stock price declining, which could result in a capital loss. It’s important to weigh the potential tax benefits against the risk of a stock price decline when deciding when to sell your RSU shares.

3.2 Charitable Contributions

Another strategy for optimizing taxes on RSUs is to donate some of the shares to charity after they vest but before selling. By donating appreciated shares, you can claim a charitable tax deduction for the fair market value of the donated shares, which can reduce your taxable income. This strategy is particularly beneficial if you’re charitably inclined and want to support a cause you believe in. Donating appreciated shares allows you to avoid paying capital gains tax on the appreciation while also receiving a tax deduction.

To qualify for a charitable tax deduction, you must donate the shares to a qualified charitable organization, such as a 501(c)(3) nonprofit. You’ll also need to itemize your deductions on your tax return to claim the deduction. The amount of your deduction may be limited based on your adjusted gross income (AGI). It’s important to consult with a tax advisor to determine the specific rules and limitations that apply to your situation.

3.3 Tax-Loss Harvesting

Tax-loss harvesting is a strategy that involves selling investments that have declined in value to generate capital losses, which can be used to offset capital gains. This strategy can be particularly useful if you have other investments that have appreciated in value and are subject to capital gains tax. By selling your losing investments, you can reduce your overall tax liability.

You can use capital losses to offset capital gains in the same year. If your capital losses exceed your capital gains, you can deduct up to $3,000 of capital losses per year against your ordinary income. Any excess capital losses can be carried forward to future years and used to offset capital gains in those years. Tax-loss harvesting can be a complex strategy, so it’s important to consult with a financial advisor to ensure that you’re implementing it effectively.

3.4 Diversification

Diversification is a risk management strategy that involves spreading your investments across a variety of asset classes, industries, and geographic regions. This strategy can help reduce the risk of your portfolio being overly concentrated in a single investment, such as your company’s stock. While RSUs can be a valuable form of compensation, they also tie a significant portion of your wealth to the success of your employer.

If your company’s stock price declines, both your job and your investment portfolio could suffer. By diversifying your investments, you can reduce the impact of a decline in your company’s stock price. Consider selling some of your RSU shares after they vest and reinvesting the proceeds in a diversified portfolio of stocks, bonds, and other assets. This can help you build a more resilient and balanced investment portfolio.

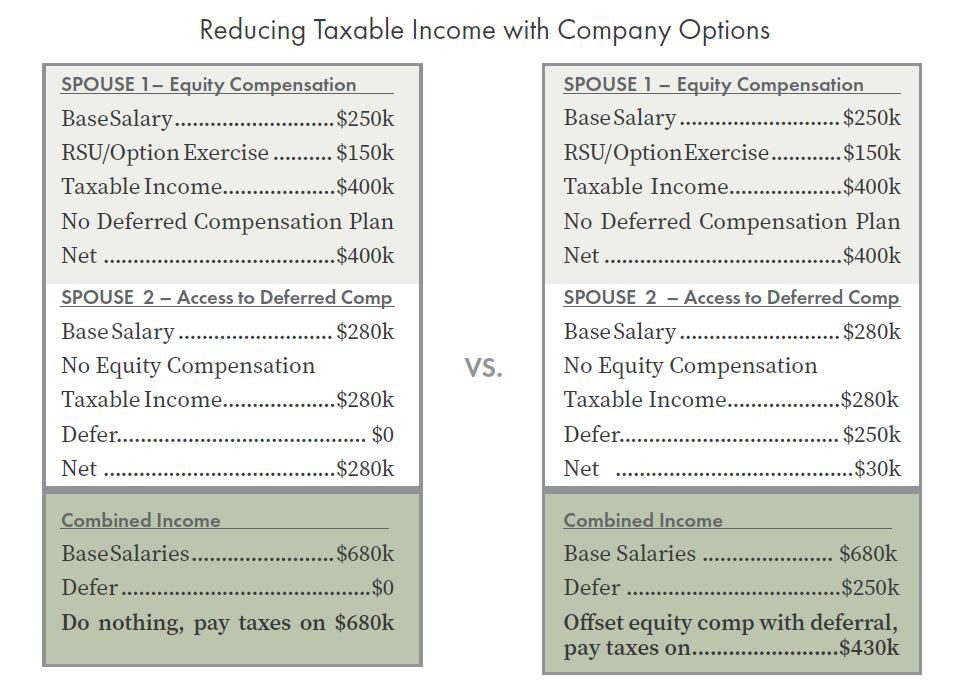

deferred comp

deferred comp

Deferred compensation plan example showing reduction in taxable income.

4. Understanding Capital Gains Tax

Capital gains tax is a tax on the profit you make from selling an asset, such as stocks, bonds, or real estate. The capital gains tax rate depends on how long you hold the asset before selling it. If you hold the asset for more than one year, the gain is considered a long-term capital gain and is taxed at a lower rate than ordinary income. If you hold the asset for one year or less, the gain is considered a short-term capital gain and is taxed at your ordinary income tax rate. Understanding the difference between short-term and long-term capital gains is crucial for tax planning.

4.1 Short-Term vs. Long-Term Capital Gains

The distinction between short-term and long-term capital gains is based on the holding period of the asset. If you hold an asset for more than one year before selling it, any profit you make is considered a long-term capital gain. Long-term capital gains are taxed at preferential rates, which are generally lower than ordinary income tax rates. The specific long-term capital gains tax rate depends on your income level.

If you hold an asset for one year or less before selling it, any profit you make is considered a short-term capital gain. Short-term capital gains are taxed at your ordinary income tax rate, which can be significantly higher than the long-term capital gains tax rates. This means that if you sell your RSU shares within one year of vesting, any profit you make will be taxed at your ordinary income tax rate.

4.2 Capital Gains Tax Rates

The capital gains tax rates vary depending on your income level and the holding period of the asset. For long-term capital gains, the tax rates are generally 0%, 15%, or 20%, depending on your taxable income. For high-income earners, there may also be an additional 3.8% net investment income tax (NIIT) on long-term capital gains.

Short-term capital gains are taxed at your ordinary income tax rate, which can range from 10% to 37%, depending on your taxable income. It’s important to be aware of the different capital gains tax rates when making investment decisions, as they can have a significant impact on your overall tax liability.

4.3 Minimizing Capital Gains Tax

There are several strategies you can use to minimize capital gains tax. One strategy is to hold your assets for more than one year before selling them, so that any profit you make is taxed at the lower long-term capital gains tax rates. Another strategy is to use tax-loss harvesting to offset capital gains with capital losses. You can also consider donating appreciated assets to charity, which allows you to avoid paying capital gains tax on the appreciation while also receiving a tax deduction.

Working with a financial advisor can help you develop a comprehensive tax plan that takes into account your individual circumstances and goals. A financial advisor can help you identify opportunities to minimize capital gains tax and maximize your overall wealth.

5. Common Mistakes to Avoid with RSU Taxation

RSU taxation can be complex, and it’s easy to make mistakes if you’re not careful. Some common mistakes to avoid include not understanding the tax implications at vesting, failing to plan for the tax liability, not tracking your cost basis, and not seeking professional advice. By being aware of these common mistakes, you can avoid costly errors and ensure that you’re managing your RSU taxation effectively.

5.1 Not Understanding the Tax Implications at Vesting

One of the most common mistakes people make with RSU taxation is not understanding the tax implications at vesting. Many employees are surprised to learn that RSUs are taxed as ordinary income when they vest, regardless of whether they sell the shares or not. This can result in a significant tax bill, especially if the fair market value of the shares is high.

It’s important to understand that when your RSUs vest, the fair market value of the shares is added to your taxable income for the year. This can potentially push you into a higher tax bracket, which means you’ll pay a higher percentage of your overall income in taxes. It’s crucial to factor in the tax implications of RSU vesting when planning your finances.

5.2 Failing to Plan for the Tax Liability

Another common mistake is failing to plan for the tax liability associated with RSU vesting. Many employees don’t realize how much their tax bill will increase when their RSUs vest, and they’re not prepared to pay the additional taxes. This can lead to financial stress and difficulty paying your taxes on time.

To avoid this mistake, it’s important to estimate your tax liability in advance and set aside enough money to pay your taxes when they’re due. You can use online tax calculators or consult with a tax advisor to estimate your tax liability. Consider adjusting your W-4 form to increase your tax withholding or making estimated tax payments throughout the year.

5.3 Not Tracking Your Cost Basis

Not tracking your cost basis is another common mistake that can lead to tax errors. Your cost basis is the fair market value of the shares when they vested. This is the amount you’ll use to calculate your capital gains or losses when you eventually sell the shares. If you don’t track your cost basis, you may not be able to accurately calculate your capital gains or losses, which could result in paying too much or too little in taxes.

Keep accurate records of when your RSUs vest and the fair market value of the shares at that time. Your brokerage firm should provide you with this information, but it’s always a good idea to keep your own records as well. When you sell your shares, you’ll need to report your cost basis on your tax return.

5.4 Not Seeking Professional Advice

Finally, not seeking professional advice is a common mistake that can have serious consequences. RSU taxation can be complex, and it’s easy to make mistakes if you’re not familiar with the rules. A tax advisor or financial planner can help you understand the tax implications of RSUs and develop a plan to minimize your tax liability.

A professional advisor can also help you with other aspects of financial planning, such as investment management, retirement planning, and estate planning. Working with a qualified advisor can give you peace of mind and help you achieve your financial goals.

6. RSU Taxation for Non-Residents

The taxation of RSUs for non-residents can be particularly complex. If you’re a non-resident alien working in the United States and receiving RSUs, the tax implications will depend on several factors, including your visa status, the length of time you’ve been in the United States, and any tax treaties between the United States and your home country. It’s essential to understand these factors to ensure that you’re complying with U.S. tax laws.

6.1 U.S. Tax Residency Rules

The first step in determining your RSU tax liability as a non-resident is to determine whether you meet the requirements to be considered a U.S. tax resident. The United States has two main tests for determining tax residency: the green card test and the substantial presence test.

The green card test is straightforward: if you have a green card (i.e., you’re a lawful permanent resident of the United States), you’re considered a U.S. tax resident. The substantial presence test is more complex and is based on the number of days you’ve been physically present in the United States over a three-year period. If you meet the substantial presence test, you’re considered a U.S. tax resident, unless you can claim a closer connection to a foreign country.

6.2 Tax Treaties

Tax treaties between the United States and other countries can affect the taxation of RSUs for non-residents. These treaties often provide special rules for determining which country has the right to tax certain types of income. For example, a tax treaty may provide that RSUs are only taxable in your home country, even if you’re working in the United States when they vest.

It’s important to review any tax treaties that may apply to your situation to determine how your RSUs will be taxed. You can find information about U.S. tax treaties on the IRS website or consult with a tax advisor who is familiar with international tax law.

6.3 Withholding and Reporting Requirements

Even if you’re a non-resident, your employer will likely be required to withhold U.S. taxes from your RSU income when they vest. This is because the IRS generally assumes that all income earned in the United States is subject to U.S. tax. However, you may be able to claim a refund of some or all of these taxes if you’re entitled to benefits under a tax treaty.

You’ll also need to file a U.S. tax return to report your RSU income and claim any deductions or credits you’re entitled to. Non-residents typically file Form 1040-NR, U.S. Nonresident Alien Income Tax Return. It’s important to file your tax return accurately and on time to avoid penalties and interest.

7. RSU Taxation and Estate Planning

RSUs can also have implications for estate planning. If you die before your RSUs vest, the unvested RSUs may be included in your estate, which could be subject to estate tax. The tax treatment of RSUs in your estate will depend on the terms of your company’s RSU plan and applicable tax laws. It’s important to consider the estate planning implications of RSUs when developing your overall estate plan.

7.1 Including RSUs in Your Estate Plan

When creating or updating your estate plan, be sure to include your RSUs as part of your assets. This will ensure that your RSUs are properly managed and distributed according to your wishes after your death. You should also review your company’s RSU plan to understand what happens to your unvested RSUs if you die before they vest.

Some RSU plans provide that unvested RSUs will be forfeited if the employee dies before they vest. Others may allow the unvested RSUs to vest immediately upon the employee’s death and be distributed to their beneficiaries. Understanding the terms of your RSU plan is crucial for effective estate planning.

7.2 Estate Tax Implications

RSUs that are included in your estate may be subject to estate tax. The federal estate tax is a tax on the transfer of property at death. The estate tax rate can be as high as 40%, and the estate tax exemption is currently $12.92 million per individual (in 2023). This means that if your estate is worth more than $12.92 million, it may be subject to estate tax.

The value of your RSUs for estate tax purposes is typically the fair market value of the shares at the date of your death. However, the IRS may scrutinize the valuation of RSUs, especially if they’re not publicly traded. It’s important to work with a qualified appraiser to determine the fair market value of your RSUs for estate tax purposes.

7.3 Strategies to Minimize Estate Tax

There are several strategies you can use to minimize estate tax on your RSUs. One strategy is to make lifetime gifts of your RSUs to your beneficiaries. Gifts are generally not subject to estate tax, as long as they’re made more than three years before your death. However, gifts may be subject to gift tax, which is a tax on the transfer of property during your lifetime.

Another strategy is to create a trust to hold your RSUs. A trust can provide a way to manage and distribute your RSUs after your death while also minimizing estate tax. There are many different types of trusts, and the best type of trust for your situation will depend on your individual circumstances and goals.

8. Real-Life Examples of RSU Tax Strategies

To illustrate how these tax strategies work in practice, let’s look at some real-life examples. These examples are for illustrative purposes only and should not be considered tax advice. Consult with a qualified tax advisor before making any decisions about your RSU taxation.

8.1 Example 1: Timing the Sale of RSUs

Sarah is a software engineer at a tech company. She receives 1,000 RSUs that vest when the company’s stock price is $100 per share. Sarah expects her income to be lower in the following year due to a planned sabbatical.

- Strategy: Sarah sells her shares immediately after they vest, recognizing $100,000 of ordinary income.

- Outcome: By selling immediately, Sarah avoids the risk of the stock price declining and potentially owing more in taxes if she held the shares for a longer period. This strategy also benefits Sarah by allowing her to shift the income to a lower tax bracket year.

8.2 Example 2: Charitable Contributions

John is a senior executive at a financial services firm. He receives 5,000 RSUs that vest when the company’s stock price is $50 per share. John is charitably inclined and wants to support a local nonprofit organization.

- Strategy: John donates 1,000 of his shares to the nonprofit organization after they vest.

- Outcome: John claims a charitable tax deduction for the fair market value of the donated shares, which reduces his taxable income. He also avoids paying capital gains tax on the appreciation of the donated shares.

8.3 Example 3: Tax-Loss Harvesting

Maria is a marketing manager at a consumer goods company. She receives 2,000 RSUs that vest when the company’s stock price is $25 per share. Maria also has other investments in her portfolio, some of which have declined in value.

- Strategy: Maria sells some of her losing investments to generate capital losses, which she uses to offset the capital gains from selling her RSU shares.

- Outcome: Maria reduces her overall tax liability by using tax-loss harvesting to offset capital gains with capital losses.

9. Staying Compliant with IRS Regulations

Navigating the complexities of RSU taxation requires staying compliant with IRS regulations. This includes accurately reporting your RSU income, keeping detailed records, and understanding the deadlines for filing your tax return and paying your taxes. By staying compliant with IRS regulations, you can avoid penalties and interest and ensure that you’re managing your RSU taxation effectively.

9.1 Reporting RSU Income

When your RSUs vest, your employer will report the income to you and the IRS on Form W-2, Wage and Tax Statement. The amount reported on your W-2 will be the fair market value of the shares at the time they vested. Be sure to review your W-2 carefully to ensure that the information is accurate.

When you sell your RSU shares, your brokerage firm will report the sale to you and the IRS on Form 1099-B, Proceeds from Broker and Barter Exchange Transactions. This form will include information such as the date of the sale, the number of shares sold, the sale price, and your cost basis. Review this form carefully to ensure that the information is accurate.

9.2 Recordkeeping Requirements

Keeping detailed records is essential for managing your RSU taxation effectively. You should keep records of when your RSUs were granted, when they vested, and the fair market value of the shares at vesting. You should also keep records of when you sold your shares, the sale price, and any expenses related to the sale.

These records will be helpful when preparing your tax return and calculating your capital gains or losses. They may also be needed if the IRS audits your tax return. Store your records in a safe place and keep them for at least three years after filing your tax return.

9.3 Filing Deadlines

The deadline for filing your federal income tax return is generally April 15 of each year. If you need more time to file, you can request an automatic extension of six months by filing Form 4868, Application for Automatic Extension of Time to File U.S. Individual Income Tax Return. However, an extension to file is not an extension to pay your taxes. You must still pay your taxes by the original due date to avoid penalties and interest.

If you’re self-employed or have other income that is not subject to withholding, you may need to make estimated tax payments throughout the year. The deadlines for making estimated tax payments are generally April 15, June 15, September 15, and January 15 of the following year.

10. How Income-Partners.Net Can Help You Maximize Your Income

At income-partners.net, we understand the complexities of navigating the financial landscape, especially when it comes to equity compensation like RSUs. We provide a comprehensive platform designed to help you maximize your income through strategic partnerships and informed financial decisions. Our services are tailored to address the unique challenges faced by entrepreneurs, business owners, investors, and marketing professionals in the United States, particularly in thriving hubs like Austin, Texas.

10.1 Strategic Partnership Opportunities

One of the key ways we help you maximize your income is through strategic partnership opportunities. We connect you with like-minded individuals and businesses who share your vision and goals. Whether you’re an entrepreneur looking for a co-founder, an investor seeking promising projects, or a marketing professional aiming to expand your reach, our platform offers a diverse network of potential partners.

10.2 Expert Insights and Resources

In addition to partnership opportunities, we provide expert insights and resources to help you make informed financial decisions. Our team of experienced financial professionals offers guidance on a wide range of topics, including RSU taxation, investment management, retirement planning, and estate planning.

We also offer a variety of educational resources, such as articles, webinars, and workshops, designed to help you stay up-to-date on the latest financial trends and strategies. With our expert insights and resources, you can make confident decisions that will help you achieve your financial goals.

10.3 Personalized Support

We understand that everyone’s financial situation is unique. That’s why we offer personalized support to help you address your specific needs and challenges. Our team of financial professionals will work with you one-on-one to develop a customized financial plan that takes into account your individual circumstances, goals, and risk tolerance.

Whether you need help with RSU taxation, investment management, retirement planning, or any other aspect of your financial life, we’re here to provide the support you need to succeed.

RSUs can be a valuable form of compensation, but it’s important to understand the tax implications and plan accordingly. By implementing the strategies discussed in this article and working with a qualified tax advisor or financial planner, you can minimize your tax liability and maximize the value of your RSU grants. At income-partners.net, we’re committed to providing you with the resources and support you need to navigate the complexities of RSU taxation and achieve your financial goals.

Address: 1 University Station, Austin, TX 78712, United States.

Phone: +1 (512) 471-3434.

Website: income-partners.net.

Ready to unlock your income potential? Explore strategic partnerships, gain expert insights, and connect with valuable resources at income-partners.net today. Let us help you build a secure and prosperous financial future. Discover how to find the right partners, build strong relationships, and immediately start profitable collaborations by visiting income-partners.net.

Frequently Asked Questions (FAQs) About RSU Taxation

1. Are RSUs taxed when granted or when they vest?

RSUs are taxed when they vest, not when they are granted. The fair market value of the shares at the time of vesting is considered ordinary income and is subject to federal, state, and local income taxes, as well as Social Security and Medicare taxes.

2. How are RSUs taxed when they vest?

When RSUs vest, the fair market value of the shares at that time is added to your taxable income for the year. This can potentially push you into a higher tax bracket, which means you’ll pay a higher percentage of your overall income in taxes.

3. What is the difference between short-term and long-term capital gains tax rates for RSUs?

If you hold your RSU shares for one year or less after vesting, any profit from selling them is taxed at your ordinary income tax rate (short-term capital gains). If you hold them for more than a year, the profit is taxed at the lower long-term capital gains tax rate.

4. What is the cost basis of RSU shares?

The cost basis of your RSU shares is the fair market value of the shares when they vested. This is the amount you’ll use to calculate your capital gains or losses when you eventually sell the shares.

5. How can I reduce the tax burden on my RSUs?

Strategies to reduce the tax burden on RSUs include timing the sale of shares, donating shares to charity, tax-loss harvesting, and diversification.

6. Are RSUs subject to Social Security and Medicare taxes?

Yes, RSUs are subject to Social Security and Medicare taxes when they vest, as they are considered ordinary income.

7. What happens to RSUs if I leave my company before they vest?

If you leave your company before your RSUs vest, you typically forfeit them. However, some companies may have provisions in their RSU plans that allow for accelerated vesting in certain circumstances, such as a layoff or termination without cause.

8. Can I defer the taxation of my RSUs?

In some cases, you may be able to defer the taxation of your RSUs by participating in a deferred compensation plan offered by your employer. This allows you to defer receiving part of your income until a later date, potentially lowering your current tax bracket.

9. Do I need to report my RSU income on my tax return?

Yes, you need to report your RSU income on your tax return. Your employer will report the income to you and the IRS on Form W-2.

10. Where can I find more information about RSU taxation?

You can find more information about RSU taxation on the IRS website or consult with a qualified tax advisor or financial planner. Additionally, income-partners.net offers resources and support to help you navigate the complexities of RSU taxation and make informed financial decisions.