Are Pensions Considered Provisional Income when calculating taxes on Social Security benefits? Yes, pensions are considered provisional income when determining the taxability of your Social Security benefits. At income-partners.net, we understand the complexities of retirement income and offer strategies to maximize your earnings through strategic partnerships. Exploring partnership opportunities can lead to significant income growth and financial security in retirement, offering solutions tailored to your unique situation.

1. Understanding Provisional Income and Its Components

Provisional income, also known as combined income, is a crucial calculation used by the Social Security Administration (SSA) to determine whether your Social Security benefits are subject to federal income tax. Understanding this calculation is essential for retirement planning and minimizing your tax burden.

So, what exactly makes up provisional income?

- Adjusted Gross Income (AGI): This includes your wages, salaries, self-employment income, interest, dividends, and distributions from retirement accounts such as 401(k)s and traditional IRAs, but excludes any Social Security benefits you receive. According to the IRS, AGI is your gross income minus certain deductions, like contributions to traditional IRAs, student loan interest payments, and self-employment tax.

- Nontaxable Interest: This includes interest from municipal bonds, which are exempt from federal income tax. Municipal bonds are debt securities issued by state and local governments to fund public projects.

- One-Half of Social Security Benefits: You must add one-half of the total Social Security benefits you received during the year, as reported on Form SSA-1099.

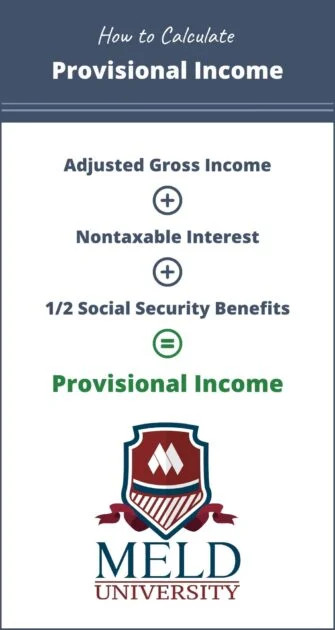

Formula for Provisional Income:

Provisional Income = AGI (excluding Social Security) + Nontaxable Interest + (1/2 * Social Security Benefits) An infographic explaining the provisional income calculation, showing AGI, nontaxable interest, and half of Social Security benefits being added together.

An infographic explaining the provisional income calculation, showing AGI, nontaxable interest, and half of Social Security benefits being added together.

2. Are Pensions Included in Provisional Income Calculations?

Yes, pensions are generally included in the Adjusted Gross Income (AGI) portion of the provisional income calculation. Pensions, whether from private companies, government entities, or other retirement plans, are considered taxable income when received. This means that distributions from pensions are added to your other sources of income, such as wages, salaries, dividends, and interest, to determine your AGI.

However, it’s important to distinguish between different types of retirement accounts and their tax implications:

- Taxable Pensions: Distributions from traditional pension plans, 401(k)s, and traditional IRAs are typically fully taxable as ordinary income. These distributions are included in your AGI and, consequently, impact your provisional income.

- Nontaxable Pensions: Certain types of pensions or retirement accounts may be nontaxable. For example, distributions from Roth IRAs are generally tax-free in retirement, provided certain conditions are met (e.g., the account has been open for at least five years, and you are age 59 1/2 or older). While the distributions themselves aren’t taxed, they can still indirectly affect your provisional income by increasing your overall income level.

3. How Provisional Income Affects the Taxation of Social Security Benefits

The level of your provisional income determines whether a portion of your Social Security benefits will be subject to federal income tax. The thresholds are as follows:

For Individuals:

- Provisional Income Below $25,000: None of your Social Security benefits are taxable.

- Provisional Income Between $25,000 and $34,000: Up to 50% of your Social Security benefits may be taxable.

- Provisional Income Above $34,000: Up to 85% of your Social Security benefits may be taxable.

For Married Couples Filing Jointly:

- Provisional Income Below $32,000: None of your Social Security benefits are taxable.

- Provisional Income Between $32,000 and $44,000: Up to 50% of your Social Security benefits may be taxable.

- Provisional Income Above $44,000: Up to 85% of your Social Security benefits may be taxable.

It’s crucial to note that these thresholds are not indexed to inflation, meaning they have not been adjusted to keep pace with the rising cost of living. This can lead to more retirees being subject to taxes on their Social Security benefits over time.

4. Examples of How Pensions Impact Provisional Income

Let’s illustrate how pension income can impact your provisional income and the taxation of your Social Security benefits with a couple of examples.

Example 1: Single Individual

-

Scenario: John is a single retiree with the following income:

- Pension Income: $30,000

- Social Security Benefits: $20,000

- Nontaxable Interest: $1,000

-

Provisional Income Calculation:

- AGI (excluding Social Security): $30,000 + $1,000 = $31,000

- One-Half of Social Security Benefits: $20,000 / 2 = $10,000

- Provisional Income: $31,000 + $10,000 = $41,000

-

Taxation of Social Security Benefits: Since John’s provisional income is above $34,000, up to 85% of his Social Security benefits may be taxable.

Example 2: Married Couple Filing Jointly

-

Scenario: Mary and Tom are a married couple filing jointly with the following income:

- Mary’s Pension Income: $25,000

- Tom’s Social Security Benefits: $18,000

- Nontaxable Interest: $500

-

Provisional Income Calculation:

- AGI (excluding Social Security): $25,000 + $500 = $25,500

- One-Half of Social Security Benefits: $18,000 / 2 = $9,000

- Provisional Income: $25,500 + $9,000 = $34,500

-

Taxation of Social Security Benefits: Since Mary and Tom’s provisional income is between $32,000 and $44,000, up to 50% of their Social Security benefits may be taxable.

5. Strategies to Minimize the Impact of Pensions on Social Security Taxes

Given that pension income can increase your provisional income and potentially subject your Social Security benefits to taxation, it’s essential to explore strategies to minimize this impact.

Here are some strategies to consider:

5.1. Roth IRA Conversions

Converting traditional IRA or 401(k) assets to a Roth IRA can be a powerful tax planning strategy. While you’ll pay income taxes on the converted amount in the year of conversion, future distributions from the Roth IRA will be tax-free, provided certain conditions are met. This can help reduce your taxable income in retirement and, consequently, your provisional income.

- Example: If you anticipate being in a higher tax bracket in retirement, converting a portion of your traditional IRA to a Roth IRA now could save you significant taxes in the long run.

5.2. Tax-Advantaged Investments

Consider investing in tax-advantaged accounts, such as municipal bonds, which offer interest that is exempt from federal income tax. This can help reduce your AGI and provisional income.

- Example: Investing in municipal bonds instead of taxable corporate bonds can lower your taxable income and potentially reduce the amount of Social Security benefits subject to tax.

5.3. Delaying Social Security Benefits

Delaying your Social Security benefits can increase your monthly benefit amount. While this won’t directly reduce your provisional income, it can provide you with more income in later years, potentially allowing you to draw less from taxable retirement accounts and keep your AGI lower.

- Example: If you delay claiming Social Security from age 62 to age 70, your monthly benefit will be significantly higher, providing you with a larger income stream and potentially reducing your reliance on taxable pension income.

5.4. Strategic Retirement Account Withdrawals

Carefully plan your withdrawals from retirement accounts to minimize your tax burden. Consider spreading out withdrawals over multiple years to avoid pushing yourself into a higher tax bracket.

- Example: Instead of taking a large lump-sum distribution from your 401(k), consider taking smaller, annual withdrawals to keep your income within a desired range.

5.5. Working with a Financial Advisor

A qualified financial advisor can help you develop a comprehensive retirement plan that takes into account your specific financial situation, tax liabilities, and goals. They can provide personalized advice on how to minimize the impact of pensions on your Social Security taxes and optimize your retirement income.

- Example: A financial advisor can analyze your income sources, tax bracket, and retirement goals to create a customized plan that minimizes taxes and maximizes your retirement income.

6. Understanding the Provisional Income Thresholds

The provisional income thresholds determine the extent to which your Social Security benefits are taxed. As previously mentioned, these thresholds are:

- Individuals: $25,000 – $34,000 (up to 50% taxable), Above $34,000 (up to 85% taxable)

- Married Couples Filing Jointly: $32,000 – $44,000 (up to 50% taxable), Above $44,000 (up to 85% taxable)

It’s important to understand that these thresholds are not adjusted for inflation. This means that as wages and investment income rise over time, more retirees will likely find themselves subject to taxes on their Social Security benefits.

7. The Importance of Tax Planning in Retirement

Tax planning is an essential component of retirement planning. Without a comprehensive tax strategy, you may end up paying more taxes than necessary, reducing your overall retirement income and potentially jeopardizing your financial security.

Here are some key reasons why tax planning is important in retirement:

- Minimizing Taxes: A well-designed tax plan can help you minimize your tax liabilities, allowing you to keep more of your hard-earned money.

- Maximizing Income: By reducing your tax burden, you can increase your overall retirement income and improve your standard of living.

- Protecting Assets: Tax planning can help you protect your assets from unnecessary taxation, ensuring that your wealth lasts throughout your retirement years.

- Ensuring Financial Security: By optimizing your tax strategy, you can enhance your financial security and reduce the risk of outliving your savings.

According to a study by the Employee Benefit Research Institute, retirees who engage in comprehensive financial planning, including tax planning, tend to have higher levels of wealth and greater financial security than those who do not.

8. Finding Partnership Opportunities to Increase Income

Beyond managing your pension and Social Security benefits, exploring partnership opportunities can significantly boost your income. At income-partners.net, we specialize in connecting individuals and businesses to create mutually beneficial partnerships.

8.1. Types of Partnerships

- Strategic Alliances: Partnering with another business to expand market reach or offer complementary services.

- Joint Ventures: Collaborating on a specific project, sharing resources and profits.

- Affiliate Marketing: Earning commissions by promoting another company’s products or services.

- Licensing Agreements: Granting another party the right to use your intellectual property for a fee.

8.2. Benefits of Partnerships

- Increased Revenue: Accessing new markets and customer bases.

- Reduced Costs: Sharing resources and expenses.

- Enhanced Expertise: Leveraging the skills and knowledge of your partner.

- Improved Innovation: Collaborating on new products and services.

8.3. How Income-Partners.Net Can Help

At income-partners.net, we provide a platform for finding and connecting with potential partners. Our services include:

- Partner Matching: Identifying businesses and individuals with complementary skills and goals.

- Networking Events: Facilitating connections and building relationships.

- Educational Resources: Providing insights and strategies for successful partnerships.

- Deal Structuring: Assisting with the negotiation and drafting of partnership agreements.

Address: 1 University Station, Austin, TX 78712, United States.

Phone: +1 (512) 471-3434.

Website: income-partners.net.

9. Case Studies: Successful Partnerships

To illustrate the power of partnerships, let’s examine a couple of real-world examples.

9.1. Starbucks and Spotify

In 2015, Starbucks and Spotify formed a partnership to integrate Spotify’s music platform into Starbucks’ loyalty program. This allowed Starbucks customers to influence the music played in stores and earn rewards for streaming music on Spotify.

- Results: The partnership increased customer engagement, drove loyalty program sign-ups, and provided Starbucks with valuable data on customer music preferences.

9.2. GoPro and Red Bull

GoPro and Red Bull partnered to create and distribute extreme sports content. GoPro’s cameras captured stunning footage of Red Bull’s athletes and events, which was then shared across both companies’ marketing channels.

- Results: The partnership elevated both brands’ image, expanded their reach to new audiences, and created a wealth of engaging content.

10. Key Takeaways for Maximizing Retirement Income

- Understand Provisional Income: Be aware of how your income sources, including pensions and Social Security benefits, impact your provisional income.

- Implement Tax Planning Strategies: Utilize Roth IRA conversions, tax-advantaged investments, and strategic retirement account withdrawals to minimize your tax burden.

- Seek Professional Advice: Consult with a financial advisor to develop a comprehensive retirement plan that addresses your specific needs and goals.

- Explore Partnership Opportunities: Consider partnering with other businesses or individuals to increase your income and expand your opportunities.

By taking a proactive approach to managing your income and taxes, you can maximize your retirement income and enjoy a financially secure future.

FAQ: Provisional Income and Social Security Benefits

1. What is provisional income, and why is it important?

Provisional income, also known as combined income, is used to determine if your Social Security benefits are taxable. It includes your adjusted gross income (AGI), nontaxable interest, and one-half of your Social Security benefits. Understanding provisional income is crucial for retirement tax planning.

2. Are pensions considered part of provisional income?

Yes, most pension income is included in the adjusted gross income (AGI) portion of your provisional income calculation. This includes distributions from traditional pensions, 401(k)s, and traditional IRAs.

3. How do Roth IRA distributions affect provisional income?

Distributions from Roth IRAs are generally tax-free, so they don’t directly increase your AGI. However, they can indirectly affect your provisional income by increasing your overall income level.

4. What are the provisional income thresholds for taxing Social Security benefits?

For individuals, the thresholds are $25,000 to $34,000 (up to 50% of benefits may be taxable) and above $34,000 (up to 85% may be taxable). For married couples filing jointly, the thresholds are $32,000 to $44,000 (up to 50% may be taxable) and above $44,000 (up to 85% may be taxable).

5. Can I reduce my provisional income to avoid taxes on my Social Security benefits?

Yes, you can reduce your provisional income by using strategies such as Roth IRA conversions, investing in tax-advantaged accounts, and carefully planning your retirement account withdrawals.

6. How does delaying Social Security benefits impact provisional income?

Delaying Social Security benefits does not directly reduce your provisional income, but it increases your monthly benefit amount. This can potentially allow you to draw less from taxable retirement accounts and keep your AGI lower.

7. Are the provisional income thresholds adjusted for inflation?

No, the provisional income thresholds are not adjusted for inflation, which means that more retirees may become subject to taxes on their Social Security benefits over time.

8. Should I consult a financial advisor about managing my provisional income?

Yes, consulting a qualified financial advisor can provide personalized advice on how to minimize the impact of pensions on your Social Security taxes and optimize your retirement income.

9. What types of partnership opportunities can help increase my retirement income?

Strategic alliances, joint ventures, affiliate marketing, and licensing agreements are all potential partnership opportunities that can help increase your retirement income.

10. How can income-partners.net help me find partnership opportunities?

Income-partners.net provides a platform for finding and connecting with potential partners. Our services include partner matching, networking events, educational resources, and deal structuring assistance.

At income-partners.net, we believe that strategic partnerships are essential for achieving financial success. Explore our resources and connect with potential partners today to unlock new opportunities and maximize your income potential!