Are Ira Withdrawals Considered Earned Income? Yes and no. It’s a nuanced question with significant implications for your Social Security benefits and overall financial strategy. At income-partners.net, we provide clarity and strategic insights to help you navigate these complexities and maximize your income potential through strategic partnerships and informed financial decisions. This article explains the impact of IRA withdrawals on your ability to collect Social Security and how they affect the taxes you pay on those benefits.

Table of Contents

- Understanding the Basics: Earned Income and IRA Withdrawals

- IRA Withdrawals and Social Security Eligibility: What You Need to Know

- The Impact of IRA Withdrawals on Social Security Taxes: A Detailed Look

- Traditional vs. Roth IRA: Tax Implications for Social Security

- Navigating the Social Security Earnings Test with IRA Withdrawals

- Strategic Planning: Minimizing Taxes on Social Security Benefits

- Real-World Examples: How IRA Withdrawals Affect Retirees

- Expert Insights: Tips for Optimizing Your Retirement Income

- Common Misconceptions About IRA Withdrawals and Social Security

- Frequently Asked Questions (FAQ) About IRA Withdrawals and Earned Income

1. Understanding the Basics: Earned Income and IRA Withdrawals

What exactly constitutes “earned income,” and how do IRA withdrawals fit into this definition? Earned income refers to money you actively earn through employment, self-employment, or business activities. It’s the income you receive in exchange for your labor or services. This includes wages, salaries, tips, bonuses, and net earnings from self-employment. Earned income is a critical factor in determining eligibility for certain tax benefits and credits, as well as impacting Social Security benefits.

IRA withdrawals, on the other hand, represent distributions from your Individual Retirement Account (IRA). These withdrawals are generally considered taxable income but are not classified as earned income. According to the IRS, earned income is directly tied to your work, while IRA withdrawals are considered deferred income from previous earnings that were saved and invested.

An infographic explaining whether IRA distributions count as income for Social Security.

An infographic explaining whether IRA distributions count as income for Social Security.

Alternative text: IRA distributions and their impact on Social Security benefits illustrated in a clear infographic.

This distinction is vital when assessing how IRA withdrawals affect your Social Security benefits, particularly concerning the Social Security earnings test and the taxation of benefits. Because IRA withdrawals are not earned income, they don’t directly reduce your Social Security benefits under the earnings test. However, they can influence the amount of Social Security benefits that are subject to income tax, depending on the type of IRA (Traditional or Roth) and your overall income level. Understanding the nuances of earned income versus IRA withdrawals is the first step in strategically planning your retirement income to minimize taxes and maximize your benefits.

2. IRA Withdrawals and Social Security Eligibility: What You Need to Know

How do IRA withdrawals affect your eligibility to receive Social Security benefits? This is a crucial question for anyone planning their retirement income strategy. The Social Security Administration (SSA) has specific rules about how much earned income you can have while still receiving full Social Security benefits, especially if you claim benefits before your full retirement age (FRA). This is known as the Social Security earnings test.

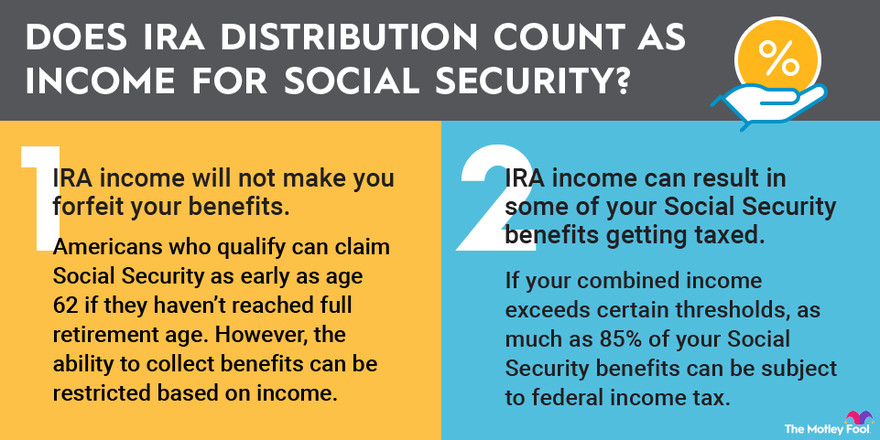

However, IRA withdrawals do not fall under the umbrella of earned income for the purposes of the Social Security earnings test. This means that withdrawing money from your IRA will not directly reduce your Social Security benefits, regardless of the amount you withdraw. The SSA focuses on income derived from active work, not from retirement savings.

If you’re considering early retirement and plan to supplement your Social Security benefits with IRA withdrawals, this is good news. You can access your retirement savings without fear of an immediate reduction in your Social Security payments. However, it’s essential to remember that while IRA withdrawals don’t directly affect your eligibility, they can indirectly impact your benefits through taxation, which we’ll explore in the next section.

3. The Impact of IRA Withdrawals on Social Security Taxes: A Detailed Look

Can IRA withdrawals cause your Social Security benefits to become taxable? The answer is a conditional yes. While IRA withdrawals don’t directly affect your eligibility to receive Social Security benefits, they can influence whether those benefits are subject to federal income tax. The IRS uses a formula that includes your adjusted gross income (AGI), non-taxable interest, and half of your Social Security benefits to determine your “combined income.”

Traditional IRA withdrawals are generally included in your AGI, which means they can increase your combined income. If your combined income exceeds certain thresholds, a portion of your Social Security benefits may become taxable. For example, for the 2024 tax year:

- Individuals with a combined income between $25,000 and $34,000 may have to pay income tax on up to 50% of their Social Security benefits.

- Individuals with a combined income above $34,000 may have to pay income tax on up to 85% of their Social Security benefits.

Married couples filing jointly have different thresholds:

- Combined income between $32,000 and $44,000 may result in up to 50% of Social Security benefits being taxable.

- Combined income above $44,000 may result in up to 85% of Social Security benefits being taxable.

This means that if you rely heavily on Traditional IRA withdrawals for retirement income, you may find a significant portion of your Social Security benefits being taxed. It’s crucial to estimate your combined income carefully to plan your withdrawals strategically and minimize your tax burden.

4. Traditional vs. Roth IRA: Tax Implications for Social Security

How do Traditional and Roth IRAs differ in their tax implications for Social Security benefits? Understanding the distinction between these two types of IRAs is crucial for effective retirement planning. The primary difference lies in when you pay taxes: Traditional IRAs offer tax deductions on contributions, but withdrawals are taxed in retirement. Roth IRAs, on the other hand, don’t provide upfront tax deductions, but qualified withdrawals in retirement are tax-free.

The implications for Social Security taxes are significant. Traditional IRA withdrawals, as mentioned earlier, are included in your adjusted gross income (AGI) and can increase your combined income, potentially leading to taxation of your Social Security benefits. Roth IRA withdrawals, however, are not included in your AGI. This means that taking withdrawals from a Roth IRA will not increase your combined income and will not cause your Social Security benefits to become taxable.

This makes Roth IRAs particularly attractive for retirees who want to minimize their tax burden and keep more of their Social Security benefits tax-free. If you anticipate being in a higher tax bracket in retirement, a Roth IRA can be a powerful tool for tax-efficient income planning. According to a study by the National Bureau of Economic Research, strategic Roth conversions during lower-income years can significantly reduce lifetime taxes and increase retirement income security.

5. Navigating the Social Security Earnings Test with IRA Withdrawals

How can you strategically use IRA withdrawals to navigate the Social Security earnings test? The Social Security earnings test can be a significant concern for individuals who claim Social Security benefits before their full retirement age (FRA) and continue to work. As previously discussed, the earnings test reduces your Social Security benefits if your earned income exceeds certain thresholds.

Since IRA withdrawals are not considered earned income, they do not directly affect the earnings test. This provides an opportunity to supplement your income with IRA withdrawals without reducing your Social Security benefits. For example, if you’re 63 years old and still working part-time, you can strategically withdraw funds from your IRA to cover living expenses without worrying about exceeding the earnings limit.

However, it’s important to remember that while IRA withdrawals don’t impact the earnings test, they can still affect the taxation of your Social Security benefits. Therefore, a balanced approach is necessary, considering both your earned income and your IRA withdrawals to optimize your overall financial situation.

6. Strategic Planning: Minimizing Taxes on Social Security Benefits

What are some effective strategies for minimizing taxes on your Social Security benefits when taking IRA withdrawals? Minimizing taxes on Social Security benefits requires careful planning and a strategic approach to retirement income. Here are some key strategies to consider:

- Roth Conversions: Converting Traditional IRA funds to a Roth IRA can be a powerful way to reduce future taxes. While you’ll pay taxes on the converted amount in the year of the conversion, future withdrawals will be tax-free, potentially reducing your combined income in retirement and preventing your Social Security benefits from being taxed.

- Tax-Efficient Withdrawal Strategies: Consider the order in which you withdraw funds from different accounts. Withdrawing from taxable accounts before tapping into your Traditional IRA can help keep your AGI lower in the early years of retirement.

- Managing Your AGI: Be mindful of how different income sources impact your AGI. Strategies like delaying Traditional IRA withdrawals and utilizing tax-advantaged accounts can help keep your AGI below the thresholds that trigger taxation of Social Security benefits.

- Consulting a Financial Advisor: A qualified financial advisor can help you develop a personalized retirement income plan that considers your specific circumstances and goals. They can provide tailored advice on how to optimize your IRA withdrawals and minimize your tax burden.

According to a study by Fidelity Investments, retirees who work with a financial advisor tend to have better retirement outcomes, including lower tax liabilities and more sustainable income streams.

7. Real-World Examples: How IRA Withdrawals Affect Retirees

Let’s look at a couple of real-world examples to illustrate how IRA withdrawals can affect retirees’ Social Security benefits:

- Example 1: John, Age 64

John retires at 64 and claims Social Security benefits. He also withdraws $30,000 annually from his Traditional IRA. His combined income exceeds the threshold, causing a portion of his Social Security benefits to be taxed. - Example 2: Mary, Age 63

Mary retires at 63 and claims Social Security benefits. She withdraws $30,000 annually from her Roth IRA. Because Roth IRA withdrawals are tax-free and not included in her AGI, her Social Security benefits remain untaxed.

These examples highlight the importance of understanding the tax implications of different types of IRA withdrawals. Depending on your individual circumstances, the right strategy can significantly impact your tax liability and overall retirement income.

8. Expert Insights: Tips for Optimizing Your Retirement Income

What are some expert tips for optimizing your retirement income and minimizing the impact of IRA withdrawals on Social Security benefits? Here are some valuable insights from financial experts:

- Plan Ahead: Start planning your retirement income strategy well in advance of retirement. This will give you time to make informed decisions about your IRA contributions, conversions, and withdrawals.

- Consider Your Tax Bracket: Evaluate your current and future tax brackets to determine the most tax-efficient way to manage your retirement income.

- Diversify Your Income Streams: Relying solely on Social Security and IRA withdrawals can be risky. Consider diversifying your income streams with other assets, such as real estate or investments.

- Stay Informed: Keep up-to-date with the latest tax laws and regulations. Retirement planning is an ongoing process, and it’s important to stay informed about changes that could affect your financial situation.

“Retirement planning is not a one-time event; it’s a continuous process that requires ongoing monitoring and adjustments,” says certified financial planner Sophia Bera of Gen Y Planning. “Regularly reviewing your retirement income strategy with a financial advisor can help you stay on track and achieve your financial goals.”

9. Common Misconceptions About IRA Withdrawals and Social Security

What are some common misconceptions about IRA withdrawals and Social Security? It’s easy to get confused about the complex rules surrounding retirement income. Here are a few common misconceptions:

- Misconception 1: IRA Withdrawals Reduce Social Security Benefits: While Traditional IRA withdrawals can impact the taxation of your Social Security benefits, they do not directly reduce the amount you receive each month.

- Misconception 2: All IRA Withdrawals Are Taxed the Same: The tax implications of IRA withdrawals depend on the type of IRA (Traditional or Roth) and your overall income level.

- Misconception 3: You Can Avoid Taxes on Social Security Completely: While it’s possible to minimize taxes on Social Security benefits, completely avoiding them is difficult, especially if you have significant income from other sources.

Understanding these common misconceptions can help you make more informed decisions about your retirement income strategy.

10. Frequently Asked Questions (FAQ) About IRA Withdrawals and Earned Income

Here are some frequently asked questions about IRA withdrawals and earned income, designed to provide quick and clear answers:

Q1: Do withdrawals from my IRA affect Social Security benefits?

Withdrawing from a traditional IRA won’t affect your ability to claim Social Security, but it’s considered taxable income, potentially taxing your Social Security benefits.

Q2: Is withdrawal from an IRA considered earned income?

No, IRA withdrawals are generally considered taxable income, but they are not classified as earned income. Earned income comes from employment, self-employment, or active business participation.

Q3: What income counts toward the Social Security earnings limit?

The Social Security earnings test only considers earned income, such as wages, salaries, tips, bonuses, and net earnings from self-employment.

Q4: Do IRA withdrawals count as income for Medicare?

Yes, traditional IRA withdrawals typically count as income for calculating Medicare premiums. Higher income can lead to higher Medicare Part B and Part D premiums.

Q5: What income does not count against Social Security?

Roth IRA distributions have no effect on Social Security benefits, including the earnings test or taxation of benefits. Unearned income like interest or dividends also doesn’t affect your ability to collect Social Security but can increase the taxation of benefits.

Q6: Can I avoid paying taxes on my Social Security benefits if I only take withdrawals from my Roth IRA?

Yes, withdrawals from a Roth IRA are tax-free and do not count toward your combined income, so they won’t cause your Social Security benefits to be taxed.

Q7: How does converting a Traditional IRA to a Roth IRA affect my Social Security benefits?

Converting a Traditional IRA to a Roth IRA can help reduce future taxes on your Social Security benefits, as Roth withdrawals are tax-free and not included in your AGI. However, you’ll need to pay taxes on the converted amount in the year of the conversion.

Q8: Is it better to delay Social Security and take IRA withdrawals, or claim Social Security early and minimize IRA withdrawals?

The best approach depends on your individual circumstances, including your health, life expectancy, and financial needs. Delaying Social Security can result in higher monthly benefits, while taking withdrawals from your IRA can provide immediate income. Consult with a financial advisor to determine the best strategy for you.

Q9: Can I recharacterize an IRA contribution to avoid taxes on my Social Security benefits?

The ability to recharacterize IRA contributions (i.e., changing a Traditional IRA contribution to a Roth IRA contribution or vice versa) was eliminated by the Tax Cuts and Jobs Act of 2017, starting in 2018.

Q10: What are the age requirements for withdrawing from an IRA without penalty?

Generally, you can withdraw from an IRA without penalty after age 59 1/2. However, there are exceptions, such as for qualified education expenses, first-time home purchases, or in cases of disability or death.

Navigating the complexities of IRA withdrawals and Social Security can be challenging. At income-partners.net, we provide comprehensive resources and expert guidance to help you make informed decisions about your retirement income strategy. By understanding the nuances of earned income, Social Security eligibility, and tax implications, you can optimize your retirement income and achieve your financial goals. Visit income-partners.net today to discover how we can help you create a secure and prosperous retirement.

Address: 1 University Station, Austin, TX 78712, United States.

Phone: +1 (512) 471-3434.

Website: income-partners.net.