Are Ira Distributions Considered Investment Income? The straightforward answer is no, IRA distributions are generally not considered investment income for the purposes of the 3.8% Net Investment Income Tax (NIIT). However, distributions can indirectly trigger the tax if your overall income exceeds certain thresholds, so understanding this nuance is crucial for effective financial planning and maximizing your income potential, and at income-partners.net, we provide the resources and connections to help you navigate these complexities and optimize your financial strategies. By leveraging our platform, you can connect with partners who can provide expert guidance, ensuring you’re well-informed and making the best decisions for your financial future. Unlock partnership potential to maximize tax efficiency, strategic wealth growth, and retirement income security.

1. Decoding Investment Income and IRA Distributions

What exactly constitutes investment income and how do IRA distributions fit into the picture? Investment income generally includes earnings from investments such as dividends, interest, rents, royalties, and capital gains. IRA distributions, on the other hand, are funds withdrawn from Individual Retirement Accounts (IRAs), which are retirement savings plans offering tax advantages.

1.1. Defining Investment Income

Investment income encompasses various forms of earnings derived from investments. These can include:

- Dividends: Payments made by companies to their shareholders from profits.

- Interest: Earnings from savings accounts, bonds, and other interest-bearing investments.

- Rents: Income received from renting out properties.

- Royalties: Payments received for the use of intellectual property, such as copyrights or patents.

- Capital Gains: Profits earned from selling investments, such as stocks or real estate, for a higher price than their purchase price.

These types of income are typically subject to taxes, and understanding their implications is vital for financial planning.

1.2. IRA Distributions Explained

IRA distributions are withdrawals from retirement accounts such as traditional IRAs, Roth IRAs, and Simplified Employee Pension (SEP) IRAs. The tax treatment of these distributions varies depending on the type of IRA:

- Traditional IRA: Distributions are typically taxed as ordinary income in retirement. Contributions may be tax-deductible, providing an upfront tax benefit.

- Roth IRA: Qualified distributions are tax-free in retirement, provided certain conditions are met. Contributions are made with after-tax dollars, so there’s no upfront tax deduction.

- SEP IRA: Commonly used by self-employed individuals and small business owners, contributions are tax-deductible, and distributions are taxed as ordinary income in retirement.

The timing and amount of IRA distributions can have significant tax implications, making it essential to plan these withdrawals strategically.

2. The 3.8% Net Investment Income Tax (NIIT)

What is the NIIT, and why does it matter for those with IRAs? The Net Investment Income Tax (NIIT) is a 3.8% tax on certain investment income for individuals, estates, and trusts that exceed specific income thresholds.

2.1. Understanding the NIIT Thresholds

The NIIT applies to individuals with modified adjusted gross income (MAGI) above certain thresholds:

- Single: $200,000

- Married Filing Jointly: $250,000

- Married Filing Separately: $125,000

If your MAGI exceeds these thresholds, the NIIT is applied to the lesser of your net investment income or the amount by which your MAGI exceeds the threshold.

2.2. What Counts as Net Investment Income for NIIT?

For the purposes of the NIIT, net investment income includes:

- Interest

- Dividends

- Capital Gains

- Rental and Royalty Income

- Income from businesses involved in trading financial instruments or commodities

However, certain items are excluded from net investment income, such as wages, self-employment income, and distributions from qualified retirement plans, including 401(k)s and IRAs.

3. Are IRA Distributions Considered Investment Income?

Are IRA distributions directly subject to the NIIT? Generally, no, IRA distributions are not considered investment income for the purpose of the NIIT, according to IRC Section 1411(c)(5). This means that withdrawals from your traditional, Roth, or SEP IRA accounts are not directly taxed under the NIIT.

3.1. The Indirect Impact of IRA Distributions on NIIT

How can IRA distributions indirectly trigger the NIIT? Even though IRA distributions themselves are not subject to the NIIT, they can increase your MAGI, potentially pushing you over the income thresholds and triggering the tax on other investment income. This is a critical consideration for retirees and high-income individuals.

3.2. Case Study: How IRA Distributions Can Trigger NIIT

Let’s consider a scenario to illustrate how this works:

Scenario:

- Sarah, a single retiree, has $180,000 of income from Social Security and a part-time job.

- She also has $30,000 in capital gains from selling stock.

- Sarah plans to take a $20,000 distribution from her traditional IRA.

Without the IRA distribution:

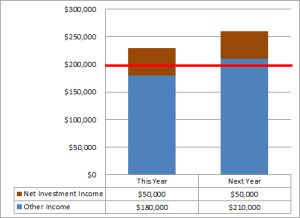

- Sarah’s MAGI would be $210,000 ($180,000 + $30,000).

- Since this is above the $200,000 threshold for single filers, she would be subject to the NIIT.

- The amount subject to NIIT would be the lesser of her net investment income ($30,000) or the amount by which her MAGI exceeds the threshold ($210,000 – $200,000 = $10,000).

- Thus, $10,000 would be subject to the 3.8% NIIT, resulting in a tax of $380.

With the IRA distribution:

- Sarah’s MAGI would increase to $230,000 ($180,000 + $30,000 + $20,000).

- The amount subject to NIIT would now be the lesser of her net investment income ($30,000) or the amount by which her MAGI exceeds the threshold ($230,000 – $200,000 = $30,000).

- In this case, $30,000 would be subject to the 3.8% NIIT, resulting in a tax of $1,140.

As you can see, the IRA distribution significantly increased the amount subject to the NIIT, resulting in a higher tax liability.

4. Strategies to Manage NIIT and IRA Distributions

What strategies can you use to manage the impact of IRA distributions on the NIIT? Several strategies can help minimize the impact of IRA distributions on your NIIT liability.

4.1. Tax Planning and Income Management

Effective tax planning involves managing your income and deductions to stay below the NIIT thresholds or minimize the amount of investment income subject to the tax. This can include:

- Timing IRA Distributions: Strategically plan when and how much to withdraw from your IRAs to avoid spiking your income in a single year.

- Tax-Loss Harvesting: Selling investments at a loss to offset capital gains and reduce your net investment income.

- Bunching Deductions: Strategically timing deductions, such as charitable contributions or medical expenses, to exceed the standard deduction in a given year.

- Controlling the timing of capital gains: Deferring or accelerating the realization of capital gains can help manage your income levels.

4.2. Roth IRA Conversions

Consider Roth IRA conversions to manage future tax liabilities. Converting traditional IRA assets to a Roth IRA can result in tax-free distributions in retirement, potentially reducing your exposure to the NIIT. However, the conversion itself is a taxable event, so it’s important to carefully evaluate the tax implications.

4.3. Investing in Tax-Advantaged Accounts

Utilize tax-advantaged investment accounts to minimize taxable investment income. Contributing to 401(k)s, health savings accounts (HSAs), and other tax-deferred or tax-free accounts can help reduce your overall taxable income.

4.4. Consulting with a Financial Advisor

Work with a qualified financial advisor to develop a comprehensive tax and retirement plan. A financial advisor can help you assess your specific situation, identify potential tax-saving opportunities, and create a strategy to optimize your income and investments. At income-partners.net, you can find experienced professionals who can guide you through these complexities.

5. Real-World Examples of NIIT Planning

How do these strategies work in practice? Let’s explore some real-world examples of how individuals have successfully managed the NIIT and IRA distributions.

5.1. Case Study 1: Minimizing NIIT with Roth Conversions

Scenario:

- John, a married retiree, has $230,000 in combined income from Social Security and pensions.

- He also has $50,000 in a traditional IRA and $20,000 in capital gains.

- John is concerned about the NIIT and wants to minimize his tax liability.

Strategy:

- John decides to convert $20,000 from his traditional IRA to a Roth IRA.

- This increases his MAGI to $250,000, which is exactly at the threshold for married couples filing jointly.

- The NIIT is calculated on the lesser of his net investment income ($20,000) or the amount by which his MAGI exceeds the threshold ($250,000 – $250,000 = $0).

- In this case, the NIIT is $0, as his MAGI does not exceed the threshold.

By strategically planning his Roth conversion, John was able to avoid the NIIT and reduce his overall tax liability.

5.2. Case Study 2: Using Tax-Loss Harvesting to Offset Capital Gains

Scenario:

- Maria, a single investor, has $190,000 in income from her job.

- She also has $40,000 in capital gains from selling stocks.

- Maria is close to the NIIT threshold and wants to reduce her exposure.

Strategy:

- Maria reviews her investment portfolio and identifies underperforming assets.

- She sells these assets at a loss of $10,000 through tax-loss harvesting.

- This reduces her net capital gains to $30,000, and her MAGI to $220,000 ($190,000 + $30,000).

- The amount subject to NIIT is the lesser of her net investment income ($30,000) or the amount by which her MAGI exceeds the threshold ($220,000 – $200,000 = $20,000).

- Thus, $20,000 is subject to the 3.8% NIIT, resulting in a tax of $760.

By utilizing tax-loss harvesting, Maria was able to reduce her capital gains and minimize her NIIT liability.

Tax-Loss Harvesting Diagram

Tax-Loss Harvesting Diagram

6. Partnering for Financial Success

Why is partnering with financial experts essential in managing NIIT and IRA distributions? Navigating the complexities of the NIIT and IRA distributions requires a deep understanding of tax laws and financial planning strategies. Partnering with experienced professionals can provide invaluable assistance in optimizing your financial outcomes.

6.1. Benefits of Partnering with Financial Advisors

Financial advisors offer a range of benefits, including:

- Personalized Financial Planning: Tailoring strategies to your specific financial situation and goals.

- Tax Optimization: Identifying opportunities to minimize your tax liability through strategic planning.

- Investment Management: Developing and managing your investment portfolio to maximize returns while minimizing risk.

- Retirement Planning: Creating a comprehensive retirement plan that addresses your income needs and tax considerations.

6.2. How Income-Partners.Net Facilitates Financial Partnerships

How can income-partners.net help you find the right financial partners? Income-partners.net serves as a platform connecting individuals with financial advisors, tax professionals, and other experts who can provide guidance and support. By using our platform, you can:

- Access a Network of Professionals: Connect with a diverse range of financial experts.

- Find Specialists: Locate advisors with expertise in tax planning, retirement planning, and investment management.

- Read Reviews and Testimonials: Gain insights into the experiences of other clients.

- Get Personalized Recommendations: Receive tailored recommendations based on your specific needs and preferences.

By leveraging income-partners.net, you can find the right partners to help you navigate the complexities of the NIIT and IRA distributions, ensuring your financial success.

7. Current Trends and Opportunities

What are the latest trends and opportunities in managing NIIT and IRA distributions? Staying informed about current trends and opportunities is essential for effective financial planning.

7.1. Legislative Updates

Tax laws are subject to change, so it’s important to stay updated on any legislative updates that may impact the NIIT and IRA distributions. Consulting with a tax professional can help you understand how these changes affect your financial situation and what steps you can take to adapt.

7.2. Innovative Financial Products

Explore innovative financial products that can help you manage your income and minimize your tax liability. These may include:

- Qualified Longevity Annuity Contracts (QLACs): Deferred annuity contracts that can reduce your required minimum distributions (RMDs) from IRAs and lower your taxable income.

- Charitable Remainder Trusts (CRTs): Irrevocable trusts that allow you to donate assets to charity, receive income for a set period, and potentially reduce your capital gains taxes.

- Opportunity Zone Investments: Investments in designated low-income communities that offer potential tax benefits, such as deferral or elimination of capital gains taxes.

7.3. Educational Resources

Take advantage of educational resources to enhance your understanding of financial planning concepts and strategies. This can include attending seminars, reading books and articles, and participating in online courses.

8. FAQs About IRA Distributions and Investment Income

What are some common questions about IRA distributions and investment income? Here are some frequently asked questions to clarify key concepts.

8.1. Are Roth IRA Distributions Taxable?

- Question: Are distributions from a Roth IRA taxable?

- Answer: Qualified distributions from a Roth IRA are generally tax-free at the federal level, provided certain conditions are met. These conditions typically include being at least 59 ½ years old and having held the account for at least five years.

8.2. Can I Avoid NIIT by Keeping My Income Below the Threshold?

- Question: Can I avoid the NIIT by keeping my income below the threshold?

- Answer: Yes, if your modified adjusted gross income (MAGI) is below the specified thresholds ($200,000 for single filers, $250,000 for married couples filing jointly), you will not be subject to the NIIT.

8.3. What Happens if I Withdraw from My IRA Before Age 59 ½?

- Question: What happens if I withdraw from my IRA before age 59 ½?

- Answer: Generally, withdrawals from traditional IRAs before age 59 ½ are subject to a 10% early withdrawal penalty, in addition to being taxed as ordinary income. However, there are exceptions for certain circumstances, such as qualified higher education expenses or first-time home purchases.

8.4. How Do I Calculate My Modified Adjusted Gross Income (MAGI) for NIIT Purposes?

- Question: How do I calculate my modified adjusted gross income (MAGI) for NIIT purposes?

- Answer: For most taxpayers, MAGI is the same as adjusted gross income (AGI). However, certain deductions and exclusions may need to be added back to AGI to calculate MAGI for NIIT purposes. Consult with a tax professional for guidance.

8.5. Can I Deduct Investment Expenses to Reduce My Net Investment Income?

- Question: Can I deduct investment expenses to reduce my net investment income?

- Answer: Yes, you can deduct certain investment expenses, such as investment advisory fees and custodial fees, to reduce your net investment income. However, these deductions are subject to limitations, and you should consult with a tax professional for guidance.

8.6. What Should I Do If I Receive an IRS Notice About the NIIT?

- Question: What should I do if I receive an IRS notice about the NIIT?

- Answer: If you receive an IRS notice about the NIIT, it’s important to review the notice carefully and respond promptly. If you disagree with the IRS’s assessment, you may need to provide documentation to support your position. Consult with a tax professional for assistance.

8.7. Is There a Limit to How Much I Can Convert to a Roth IRA?

- Question: Is there a limit to how much I can convert to a Roth IRA?

- Answer: No, there is no annual limit to how much you can convert from a traditional IRA to a Roth IRA. However, the conversion is a taxable event, and you should carefully evaluate the tax implications before proceeding.

8.8. How Does Tax-Loss Harvesting Work?

- Question: How does tax-loss harvesting work?

- Answer: Tax-loss harvesting involves selling investments at a loss to offset capital gains. This can help reduce your overall tax liability. However, there are rules and limitations to be aware of, such as the wash-sale rule, which prohibits you from repurchasing the same or substantially similar investment within 30 days of selling it at a loss.

8.9. Can I Contribute to Both a Traditional IRA and a Roth IRA in the Same Year?

- Question: Can I contribute to both a traditional IRA and a Roth IRA in the same year?

- Answer: Yes, you can contribute to both a traditional IRA and a Roth IRA in the same year, as long as your total contributions do not exceed the annual contribution limit. However, your ability to deduct contributions to a traditional IRA may be limited if you are also covered by a retirement plan at work.

8.10. How Often Should I Review My Tax and Retirement Plan?

- Question: How often should I review my tax and retirement plan?

- Answer: It’s a good idea to review your tax and retirement plan at least annually, or more frequently if there have been significant changes in your financial situation or tax laws. Regular reviews can help you identify potential opportunities to optimize your plan and ensure that it continues to meet your needs.

9. Conclusion: Navigating IRA Distributions and Investment Income

Navigating the complexities of IRA distributions and investment income requires careful planning and expert guidance, so while IRA distributions are not directly considered investment income for the NIIT, they can indirectly trigger the tax if your overall income exceeds certain thresholds. By partnering with experienced professionals and staying informed about current trends and opportunities, you can minimize your tax liability and achieve your financial goals.

At income-partners.net, we are committed to providing you with the resources and connections you need to succeed. Whether you’re seeking a financial advisor, a tax professional, or other experts, our platform can help you find the right partners to guide you on your journey. Visit income-partners.net today to explore the opportunities and start building your financial future.

Let income-partners.net be your guide to financial success, providing the connections and expertise you need to navigate the complexities of IRA distributions and investment income.

Are you ready to take control of your financial future and optimize your tax strategies? Visit income-partners.net today to connect with experienced professionals and start building your path to financial success. Find the partners you need to navigate the complexities of NIIT and IRA distributions, ensuring you make informed decisions and maximize your financial well-being.