Are income-driven repayment plans forgiven after 20 years? Yes, generally, income-driven repayment (IDR) plans offer loan forgiveness after a specified period, typically 20 to 25 years, depending on the specific plan and loan type, explore options at income-partners.net. IDR plans are designed to make student loan repayment more affordable by basing monthly payments on your income and family size, not just the amount you owe, by understanding IDR plans, you can explore partnership opportunities that align with financial wellness. Consider exploring loan repayment partnerships, debt relief strategies, and financial stability initiatives.

1. Understanding Income-Driven Repayment (IDR) Plans

Income-Driven Repayment (IDR) plans are federal student loan repayment options that calculate your monthly payments based on your income and family size. These plans offer a pathway to loan forgiveness after a set period, typically 20 to 25 years. Millions of borrowers are taking advantage of IDR plans.

Here’s a detailed look at IDR plans:

- Affordability: IDR plans are designed to make student loan repayment more manageable by aligning monthly payments with your income.

- Eligibility: These plans are available to borrowers with federal student loans, including Direct Loans and FFEL loans.

- Loan Forgiveness: After making qualifying payments for 20 or 25 years, the remaining loan balance is forgiven. The exact timeframe depends on the specific IDR plan.

For individuals seeking financial stability and exploring partnership opportunities, understanding IDR plans is crucial. Income-partners.net can provide insights into how these plans can impact your financial planning and potential business ventures.

1.1. What are the main types of IDR plans available?

There are four main types of IDR plans: SAVE, PAYE, IBR, and ICR, each with its own eligibility requirements and terms.

- SAVE (Saving on A Valuable Education): This plan, replacing REPAYE, offers the most significant payment reduction for many borrowers.

- PAYE (Pay As You Earn): PAYE caps monthly payments at 10% of discretionary income and offers forgiveness after 20 years.

- IBR (Income-Based Repayment): IBR has different terms depending on when you took out your loans, with forgiveness after 20 or 25 years.

- ICR (Income Contingent Repayment): ICR calculates payments based on income and family size, with forgiveness after 25 years.

1.2. Who is eligible for Income-Driven Repayment (IDR) Plans?

Eligibility for IDR plans generally includes borrowers with federal student loans, but specific requirements vary by plan. Borrowers with Direct Loans, including Direct Subsidized Loans, Direct Unsubsidized Loans, Direct PLUS Loans (for graduate or professional students), and Direct Consolidation Loans, are typically eligible. FFEL (Federal Family Education Loan) Program loans may also qualify if consolidated into a Direct Consolidation Loan. However, Parent PLUS Loans and defaulted loans have specific eligibility criteria. The income requirements and family size considerations also play a significant role in determining eligibility, ensuring that the plans are accessible to those who need them most.

2. The SAVE Plan and Loan Forgiveness

The SAVE (Saving on A Valuable Education) Plan is the newest IDR plan, replacing the REPAYE plan, and offers potentially faster loan forgiveness for borrowers with smaller loan balances.

2.1. How does the SAVE plan affect loan forgiveness timelines?

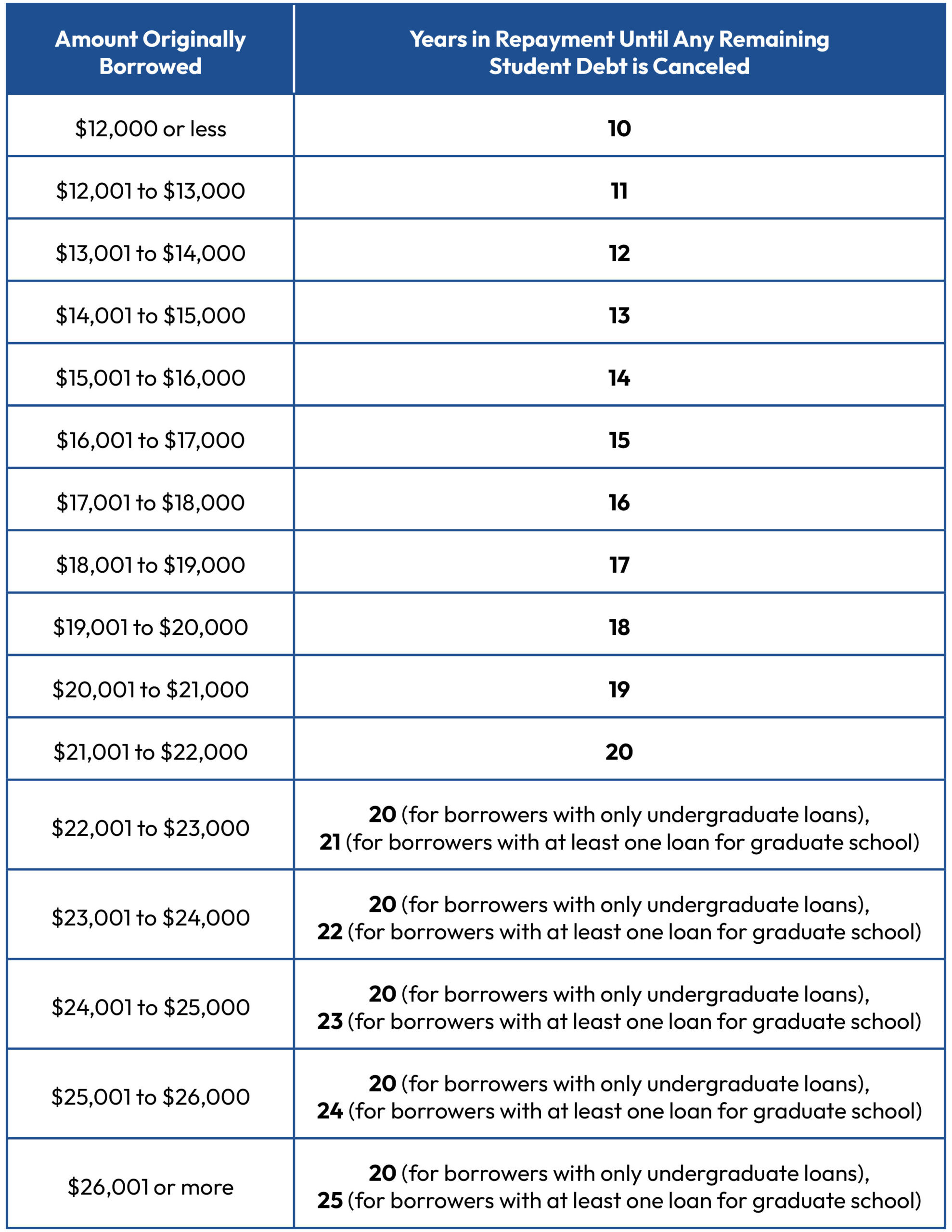

Under the SAVE plan, borrowers who originally borrowed $12,000 or less may be eligible for loan forgiveness after just 10 years of payments. This is a significant change from the standard 20 to 25 years under other IDR plans. For every $1,000 borrowed above $12,000, the repayment period increases by one year, up to a maximum of 20 or 25 years depending on whether the loans were for undergraduate or graduate study.

SAVE Plan Repayment Chart

SAVE Plan Repayment Chart

2.2. What are the specific forgiveness timelines under the SAVE plan?

The forgiveness timelines under the SAVE plan are as follows:

- 10 years: For those who borrowed $12,000 or less.

- Less than 20 years: For those who borrowed less than $21,000 and only have undergraduate loans.

- 20 years: For those with undergraduate loans and borrowed more than $21,000.

- Less than 25 years: For those with any graduate school loans and borrowed less than $26,000.

- 25 years: For those with any graduate school loans and borrowed more than $26,000.

2.3. How to Apply for the SAVE Plan

Applying for the SAVE plan involves several key steps to ensure eligibility and maximize benefits. First, gather all necessary documents, including your most recent tax return, proof of income (such as pay stubs), and information on your federal student loans. Next, visit the Federal Student Aid website (studentaid.gov) and complete the IDR application. You will need to provide your income and family size, which will be used to calculate your monthly payment.

During the application process, select the SAVE plan as your preferred repayment option. The application will guide you through the necessary steps and provide information on any additional documentation required. Once you submit your application, it will be reviewed by your loan servicer, who will notify you of your eligibility and monthly payment amount.

It’s important to recertify your income and family size annually to ensure your payments remain accurate and to continue your eligibility for the SAVE plan. This can be done through the Federal Student Aid website. If your income changes significantly, you should update your information as soon as possible to avoid any discrepancies in your payments and potential issues with loan forgiveness.

Regularly check your loan servicer’s website for any updates or changes to the SAVE plan and ensure you are meeting all requirements to stay on track for loan forgiveness. By following these steps and staying informed, you can effectively manage your student loans and take full advantage of the SAVE plan’s benefits.

3. PAYE, IBR, and ICR Plans: Forgiveness After 20 or 25 Years

While the SAVE plan offers potentially faster forgiveness, the PAYE, IBR, and ICR plans still provide loan forgiveness after 20 or 25 years of qualifying payments.

3.1. What are the forgiveness timelines for PAYE, IBR, and ICR plans?

The forgiveness timelines for these plans are as follows:

- PAYE: 20 years of payments.

- IBR: 20 years for new borrowers on or after July 1, 2014; 25 years for borrowers before that date.

- ICR: 25 years of payments.

3.2. How do these plans compare to the SAVE plan?

The SAVE plan generally offers lower monthly payments and potentially faster forgiveness for borrowers with smaller loan balances. However, PAYE, IBR, and ICR may be more suitable for borrowers with higher incomes or larger loan balances. The best plan depends on your individual financial situation.

For strategic financial planning, it’s essential to evaluate the nuances of each IDR plan. Consider collaborating with financial advisors through platforms like income-partners.net to explore optimal financial strategies.

3.3. Determining the Best IDR Plan for Your Situation

Choosing the right Income-Driven Repayment (IDR) plan requires careful consideration of several factors, including your income, loan balance, family size, and loan type. First, assess your current financial situation by calculating your discretionary income, which is the difference between your adjusted gross income and 150% of the poverty guideline for your family size. This will help you estimate your monthly payments under each IDR plan.

Next, consider the loan forgiveness timelines for each plan. The SAVE plan offers forgiveness after 10 years for those who borrowed $12,000 or less, while PAYE offers forgiveness after 20 years, and IBR and ICR offer forgiveness after 20 or 25 years, depending on the loan origination date. Evaluate which timeline aligns best with your long-term financial goals.

Also, compare the monthly payment amounts under each plan. The SAVE plan generally offers the lowest monthly payments, while PAYE and IBR cap payments at a percentage of your discretionary income. ICR payments can be higher, especially as your income increases. Use online calculators provided by the Department of Education or your loan servicer to estimate your payments under each plan.

Finally, consider the potential tax implications of loan forgiveness. While loan forgiveness is currently tax-free through 2025, any amount forgiven after that may be considered taxable income. Consult with a tax professional to understand the potential impact on your tax liability. By carefully evaluating these factors and comparing the terms of each IDR plan, you can make an informed decision that best suits your financial needs and goals.

4. One-Time IDR Account Adjustment

The Department of Education has announced a one-time IDR account adjustment to help borrowers receive credit toward forgiveness through IDR or PSLF.

4.1. What is the one-time IDR account adjustment?

This adjustment is designed to address historical issues with loan servicing and payment tracking. It provides borrowers with credit toward IDR loan forgiveness for past periods of forbearance, deferment, and repayment, regardless of the repayment plan.

4.2. How does the IDR account adjustment affect loan forgiveness?

The one-time account adjustment can help borrowers reach loan forgiveness faster by counting periods that previously didn’t qualify toward the required 20 or 25 years of payments. Millions of borrowers are expected to benefit from this adjustment.

4.3. Understanding the Benefits of the One-Time IDR Account Adjustment

The One-Time IDR Account Adjustment is a comprehensive initiative by the U.S. Department of Education to address historical inaccuracies in the counting of payments toward income-driven repayment (IDR) plan forgiveness. This adjustment offers several key benefits to borrowers.

First, it provides a more accurate count of qualifying payments for IDR forgiveness. Many borrowers have experienced issues with their payments not being properly credited due to servicing errors or administrative issues. The adjustment reviews loan histories to ensure all eligible payments are accurately counted, bringing borrowers closer to forgiveness.

Second, the adjustment addresses long-standing issues with forbearance steering. In the past, loan servicers often placed borrowers in forbearance instead of IDR plans, which delayed their progress toward forgiveness. The adjustment credits borrowers for certain periods of forbearance, helping to rectify this issue.

Third, the adjustment simplifies the path to forgiveness for many borrowers. By providing a more accurate and comprehensive count of qualifying payments, it reduces the burden on borrowers to track and verify their payment history. This streamlined process makes it easier for borrowers to achieve loan forgiveness and gain financial relief.

Overall, the One-Time IDR Account Adjustment is a significant step toward ensuring fairness and accuracy in the student loan system, providing much-needed relief and a clearer path to forgiveness for millions of borrowers.

5. Do You Need to Apply for IDR Loan Forgiveness?

No, you do not need to apply for IDR loan forgiveness. It is automatically granted after you make your last qualifying IDR payment.

5.1. What steps should you take to ensure you receive IDR loan forgiveness?

To ensure you receive IDR loan forgiveness, you should:

- Make sure you are enrolled in an IDR plan.

- Certify your income and family size annually.

- Keep detailed records of your payments.

- Contact your loan servicer if you believe you are eligible for forgiveness but haven’t received it.

5.2. Addressing Potential Issues with IDR Loan Forgiveness

While IDR loan forgiveness is designed to be automatic, there can be issues that arise, which may delay or prevent borrowers from receiving the forgiveness they are entitled to. One common issue is inaccurate payment tracking. Loan servicers sometimes make errors in recording qualifying payments, leading to an undercount of the payments made toward the required 20 or 25 years. To address this, borrowers should keep detailed records of all payments, including dates, amounts, and confirmation numbers, and regularly review their loan statements to ensure accuracy.

Another issue is failure to recertify income and family size annually. IDR plans require borrowers to update their income and family size each year to ensure their payments are calculated correctly. Failure to recertify can lead to increased payments or removal from the IDR plan, delaying or preventing loan forgiveness. Borrowers should set reminders to recertify annually and promptly provide any required documentation to their loan servicer.

Changes in loan servicer can also cause confusion and errors in payment tracking. When loans are transferred between servicers, payment histories may not be accurately transferred, leading to discrepancies in the count of qualifying payments. Borrowers should maintain copies of their payment records and proactively contact their new servicer to verify their payment history and ensure all payments are properly credited.

Additionally, some borrowers may encounter issues related to eligible loan types. Not all federal student loans are eligible for IDR plans, and consolidating loans can sometimes affect eligibility. Borrowers should verify that their loans are eligible for IDR and understand the implications of consolidation on their path to forgiveness.

If borrowers encounter any of these issues, they should contact their loan servicer immediately to resolve the problem. If the issue cannot be resolved with the servicer, borrowers can file a complaint with the Federal Student Aid (FSA) Ombudsman, who can help mediate disputes and ensure fair treatment. By proactively addressing potential issues and advocating for their rights, borrowers can increase their chances of successfully receiving IDR loan forgiveness.

6. Tax Implications of IDR Loan Forgiveness

Through the end of 2025, there are no federal tax consequences for having your student loans forgiven through an IDR plan.

6.1. Will you have to pay taxes on any loan balance that is forgiven under the IDR plan?

Unless the law changes, there may be federal tax consequences for any amount of your student loan debt that is forgiven through IDR beginning in 2026. However, some states may still tax forgiven student loan debt.

6.2. How can you prepare for potential tax implications?

To prepare for potential tax implications, you should:

- Speak with a tax professional for personalized advice.

- Understand the tax laws in your state.

- Set aside funds to cover potential tax liabilities.

6.3. Navigating the Tax Implications of Loan Forgiveness

While the prospect of loan forgiveness is exciting, it’s essential to understand the potential tax implications that may arise. In general, when a debt is forgiven, the forgiven amount is often considered taxable income by the IRS. This means that the amount of your student loan debt that is forgiven under an IDR plan could be subject to federal income tax in the year the forgiveness occurs.

However, there are exceptions and special rules that may apply. For example, the American Rescue Plan Act of 2021 included a provision that made student loan forgiveness tax-free at the federal level through December 31, 2025. This means that if your loans are forgiven before this date, you will not owe federal income tax on the forgiven amount.

It’s important to note that while federal tax rules may provide temporary relief, state tax laws can vary. Some states may consider forgiven student loan debt as taxable income, while others may not. You should consult with a tax advisor in your state to understand the specific state tax implications of loan forgiveness.

To prepare for potential tax liabilities, consider setting aside funds in advance. You can estimate the potential tax amount by multiplying the forgiven loan amount by your estimated tax rate for the year of forgiveness. Another strategy is to adjust your tax withholdings or make estimated tax payments throughout the year to spread out the tax burden.

Additionally, stay informed about any changes in tax laws or regulations that could affect the tax treatment of loan forgiveness. The IRS and other government agencies provide resources and guidance on tax-related matters, so be sure to stay updated on the latest developments.

By understanding the tax implications of loan forgiveness and taking proactive steps to prepare, you can navigate this aspect of loan repayment with confidence and minimize any potential financial surprises.

7. Seeking Expert Advice and Resources

Navigating student loan repayment and forgiveness can be complex. Seeking expert advice and utilizing available resources can help you make informed decisions.

7.1. Who can you consult for advice on IDR plans and loan forgiveness?

You can consult with:

- Financial advisors: Professionals who can provide personalized financial advice.

- Student loan counselors: Experts who specialize in student loan repayment options.

- Tax professionals: Advisors who can help you understand the tax implications of loan forgiveness.

7.2. Where can you find reliable information about IDR plans?

Reliable sources of information include:

- The U.S. Department of Education’s website: Provides comprehensive information about federal student loans and repayment plans.

- Student loan servicer websites: Offer details about your specific loans and repayment options.

- Nonprofit organizations: Provide unbiased information and resources for student loan borrowers.

7.3. Leveraging Expert Guidance and Resources for IDR Plans

Navigating the complexities of Income-Driven Repayment (IDR) plans can be overwhelming, and seeking expert guidance and utilizing available resources is essential for making informed decisions and optimizing your repayment strategy. One valuable resource is consulting with a certified financial planner (CFP) who specializes in student loan repayment. A CFP can assess your financial situation, evaluate your eligibility for different IDR plans, and help you choose the plan that best aligns with your goals and circumstances.

Student loan counseling agencies are another excellent source of guidance. These agencies provide free or low-cost counseling services to help borrowers understand their repayment options, navigate the application process, and resolve any issues with their loans. Counselors can also assist with budgeting, debt management, and planning for loan forgiveness.

In addition to professional advice, there are numerous online resources available to help you learn about IDR plans and manage your student loans. The U.S. Department of Education’s website (studentaid.gov) is a comprehensive source of information about federal student loans, repayment plans, and loan forgiveness programs. The website provides tools and calculators to estimate your monthly payments under different IDR plans and track your progress toward loan forgiveness.

Nonprofit organizations, such as the Institute of Student Loan Advisors (TISLA) and the National Consumer Law Center (NCLC), also offer valuable resources and advocacy for student loan borrowers. These organizations provide educational materials, legal assistance, and policy advocacy to help borrowers navigate the student loan system and protect their rights.

When seeking expert guidance, it’s important to choose reputable and trustworthy sources. Be wary of companies that charge excessive fees or make unrealistic promises about loan forgiveness. Always verify the credentials and qualifications of any advisor or agency you work with, and be sure to do your own research to make informed decisions.

By leveraging expert guidance and utilizing available resources, you can navigate the complexities of IDR plans with confidence and achieve your goals of affordable repayment and loan forgiveness.

8. Real-Life Examples of IDR Loan Forgiveness

Hearing real-life stories can provide inspiration and clarity about the possibilities of IDR loan forgiveness.

8.1. Can you share success stories of borrowers who have received loan forgiveness through IDR plans?

- Sarah: A teacher with $60,000 in student loans had her remaining balance forgiven after 20 years of payments under the PAYE plan.

- John: A social worker with $40,000 in student loans received forgiveness after 10 years under the SAVE plan due to his low original loan balance.

- Emily: A nurse practitioner with $80,000 in student loans is on track for forgiveness after 25 years under the ICR plan.

8.2. What lessons can be learned from these stories?

These stories highlight the importance of:

- Enrolling in the right IDR plan for your financial situation.

- Making consistent, qualifying payments.

- Staying informed about changes to IDR programs.

8.3. Learning from Success: Real Stories of IDR Loan Forgiveness

Hearing real-life success stories of borrowers who have achieved loan forgiveness through Income-Driven Repayment (IDR) plans can provide inspiration, motivation, and valuable insights into the process. These stories illustrate the transformative impact of IDR plans and the importance of perseverance and informed decision-making.

One such story is that of Maria, a public school teacher who struggled with student loan debt for many years. Maria had borrowed $80,000 to pursue her teaching degree, and the standard repayment plan left her with unaffordable monthly payments. She enrolled in the Pay As You Earn (PAYE) plan, which reduced her monthly payments based on her income. After 20 years of making qualifying payments under the PAYE plan, Maria’s remaining loan balance was forgiven. She describes the experience as life-changing, allowing her to finally achieve financial stability and pursue her dreams without the burden of student loan debt.

Another inspiring story is that of David, a social worker who dedicated his career to serving underserved communities. David had borrowed $60,000 in student loans, and his low income made it challenging to keep up with his loan payments. He enrolled in the Income-Based Repayment (IBR) plan, which provided him with affordable monthly payments based on his income and family size. After 25 years of making qualifying payments under the IBR plan, David’s remaining loan balance was forgiven. He emphasizes the importance of seeking out IDR plans and staying informed about the eligibility requirements and application process.

These success stories underscore the power of IDR plans to provide relief and opportunity to borrowers who are struggling with student loan debt. They also highlight the importance of making informed decisions, staying on top of your loan repayment, and seeking out expert advice when needed. By learning from these real-life examples, you can gain valuable insights into how to navigate the IDR process and achieve your own loan forgiveness goals.

9. Recent Changes and Updates to IDR Plans

The landscape of IDR plans is constantly evolving. Staying informed about recent changes and updates is crucial.

9.1. What are the latest updates to IDR programs?

Recent updates include the implementation of the SAVE plan, the one-time IDR account adjustment, and ongoing discussions about potential changes to tax laws related to loan forgiveness.

9.2. How do these changes affect borrowers?

These changes can provide significant benefits to borrowers, such as lower monthly payments, faster loan forgiveness, and a more accurate count of qualifying payments.

9.3. Staying Informed: Navigating Recent Changes to IDR Plans

The landscape of Income-Driven Repayment (IDR) plans is constantly evolving, with new regulations, policy changes, and program updates being introduced regularly. Staying informed about these changes is essential for borrowers to make informed decisions and optimize their repayment strategy. One significant recent change is the implementation of the Saving on A Valuable Education (SAVE) plan, which replaces the Revised Pay As You Earn (REPAYE) plan. The SAVE plan offers several key benefits, including lower monthly payments, a more generous income calculation, and a faster path to loan forgiveness for borrowers with smaller loan balances.

Another important recent update is the One-Time IDR Account Adjustment, which aims to correct historical inaccuracies in the counting of payments toward IDR plan forgiveness. This adjustment provides borrowers with credit for past periods of forbearance, deferment, and repayment, regardless of the repayment plan they were enrolled in at the time.

In addition to these specific program changes, there are also ongoing discussions and debates about broader student loan policy reforms, such as proposals to expand loan forgiveness, simplify the IDR application process, and address the root causes of student loan debt. These potential reforms could have significant implications for borrowers in the future, so it’s important to stay informed about the latest developments and advocate for policies that support student loan borrowers.

To stay informed about recent changes and updates to IDR plans, borrowers should regularly check the U.S. Department of Education’s website (studentaid.gov) for official announcements and guidance. They should also sign up for email updates from their loan servicer and follow reputable news sources and advocacy organizations that cover student loan issues.

By staying informed and engaged, borrowers can navigate the evolving landscape of IDR plans with confidence and make informed decisions that align with their financial goals and circumstances.

10. Is IDR Right for You?

Deciding whether an IDR plan is the right choice depends on your individual circumstances.

10.1. How can you determine if an IDR plan is the right choice for you?

Consider your:

- Income and family size.

- Loan balance.

- Long-term financial goals.

10.2. What are the pros and cons of enrolling in an IDR plan?

Pros:

- Lower monthly payments.

- Potential for loan forgiveness.

- Protection against default.

Cons:

- Longer repayment period.

- Potential tax implications.

- May pay more interest over time.

10.3. Evaluating Your Options: Is an IDR Plan the Right Choice for You?

Deciding whether an Income-Driven Repayment (IDR) plan is the right choice for you is a significant decision that requires careful consideration of your financial situation, goals, and priorities. There are several factors to evaluate when determining if an IDR plan aligns with your needs.

First, assess your income and expenses. IDR plans are designed to make student loan payments more affordable by basing them on your income and family size. If your current income is low relative to your student loan debt, an IDR plan could significantly reduce your monthly payments and free up cash for other essential expenses.

Next, consider your long-term career prospects and earning potential. If you anticipate your income will increase substantially in the future, an IDR plan may not be the best option, as your monthly payments will also increase over time. In this case, a standard or graduated repayment plan might be more suitable.

Evaluate your risk tolerance and financial stability. IDR plans offer protection against default by providing affordable monthly payments that prevent your loans from becoming delinquent. If you are concerned about your ability to consistently make loan payments, an IDR plan can provide peace of mind and prevent long-term financial consequences.

Also, consider the potential for loan forgiveness. IDR plans offer loan forgiveness after a set period of qualifying payments, typically 20 or 25 years. If you are eligible for loan forgiveness, an IDR plan could significantly reduce your overall repayment burden and help you achieve financial freedom sooner.

Finally, seek out expert advice from a financial advisor or student loan counselor. These professionals can provide personalized guidance and help you evaluate your options based on your unique circumstances.

By carefully evaluating these factors and seeking out expert advice, you can make an informed decision about whether an IDR plan is the right choice for you and take control of your student loan repayment journey.

For tailored guidance on navigating IDR plans, consider exploring partnership opportunities with financial advisory services via income-partners.net.

FAQ: Income-Driven Repayment Plans and Forgiveness

1. What happens to my student loans after 20 years of income-driven repayment?

Generally, any remaining balance on your loans will be forgiven after 20 years of qualifying payments under certain IDR plans like PAYE. However, the specific timeline can vary based on the plan and loan type.

2. Are student loans really forgiven after 20 years?

Yes, under income-driven repayment (IDR) plans, any remaining loan balance can be forgiven after 20 or 25 years, depending on the plan and when the loans were taken out. The SAVE plan can offer forgiveness even sooner for those who originally borrowed $12,000 or less.

3. What is the income-driven repayment forgiveness 20-year plan?

The 20-year plan refers to IDR plans like PAYE, where borrowers can have their remaining loan balance forgiven after 20 years of qualifying payments. This is in contrast to plans like ICR, which require 25 years of payments for forgiveness.

4. What happens to my student loans after 25 years of income-driven repayment?

Under IDR plans like IBR (for older loans) and ICR, any remaining balance on your loans will be forgiven after 25 years of qualifying payments.

5. What is the SAVE plan for student loans?

The SAVE (Saving on A Valuable Education) plan is an income-driven repayment plan that replaces the REPAYE plan. It offers lower monthly payments and potentially faster loan forgiveness, especially for borrowers with smaller loan balances.

6. Do I need to apply for loan forgiveness under IDR?

No, loan forgiveness under IDR is generally automatic after you make your last qualifying payment. However, it’s essential to ensure you are enrolled in an eligible IDR plan and have certified your income annually.

7. Will I owe taxes on the amount of student loans forgiven under IDR?

Through the end of 2025, there are no federal tax consequences for student loan forgiveness under IDR plans. However, unless the law changes, there may be tax implications for loan amounts forgiven after 2025.

8. What is the one-time IDR account adjustment?

The one-time IDR account adjustment is a program by the Department of Education to correct past issues with loan servicing. It provides borrowers with credit toward IDR loan forgiveness for periods of forbearance, deferment, and repayment.

9. What are the pros and cons of income-driven repayment plans?

Pros include lower monthly payments and potential loan forgiveness. Cons include a longer repayment period, potential tax implications on forgiven amounts, and the possibility of paying more interest over time.

10. How do I enroll in an income-driven repayment plan?

To enroll in an IDR plan, you can visit the Federal Student Aid website (studentaid.gov) and complete the IDR application. You’ll need to provide information about your income, family size, and student loans.

Conclusion

Navigating the world of income-driven repayment plans can seem daunting, but understanding the details can lead to significant financial relief. Remember to explore all available options, stay informed about program updates, and seek expert advice when needed.

Ready to take control of your financial future? Visit income-partners.net to explore partnership opportunities, learn more about financial planning, and connect with professionals who can help you navigate student loan repayment and forgiveness. Discover strategies to build wealth, manage debt, and achieve financial independence. Start your journey to financial success today with income-partners.net.

Consider exploring partnerships with financial advisors and student loan experts through income-partners.net to optimize your financial strategies.