Are Grants Unearned Income? Yes, in many cases, grants are considered unearned income, especially when they are used for purposes other than qualified education expenses. At income-partners.net, we aim to provide clarity on this topic, helping you understand the tax implications and explore strategies for financial success through strategic partnerships. Understanding these distinctions can save you headaches and help you better plan for the future. Let’s delve into this topic and see how it affects you and your potential income partnerships, financial strategies, and tax planning.

1. Decoding Unearned Income: What Does It Really Mean?

What exactly constitutes unearned income? Unearned income refers to income derived from sources other than wages, salaries, or active participation in a business. It’s essentially money you receive without directly working for it.

Think of it this way: if you’re not trading your time and effort for a paycheck, the resulting income is likely unearned. This category typically includes interest, dividends, capital gains, rental income, royalties, and, importantly for our discussion, certain types of grants and scholarships. The IRS categorizes unearned income distinctly from earned income, which is critical for tax purposes.

1.1. The IRS Perspective on Unearned vs. Earned Income

How does the IRS differentiate between earned and unearned income? The IRS defines earned income as compensation received for personal services rendered, such as wages, salaries, and self-employment income, as stated in Section 911(d)(2) of the Internal Revenue Code. Unearned income, on the other hand, includes income from investments, rents, royalties, and taxable portions of scholarships and grants. This distinction is crucial because different types of income are often taxed at different rates.

For example, if you’re a student receiving a scholarship that covers tuition and required fees, that portion is typically tax-free. However, if the scholarship also covers room and board, the amount allocated to those expenses may be considered taxable unearned income. According to IRS Publication 970, “Tax Benefits for Education,” scholarships used for expenses other than qualified tuition and related expenses are generally included in income.

1.2. Real-World Examples of Unearned Income

What are some practical examples of unearned income? To clarify, consider these scenarios:

- Dividends from Stocks: If you own shares of a company and receive dividend payments, this is unearned income.

- Interest from Savings Accounts: The interest you earn on your savings accounts is also classified as unearned income.

- Rental Income: If you own a property and rent it out, the rental income you receive is unearned.

- Royalties: Payments received for the use of your intellectual property, such as books or patents, are unearned income.

- Taxable Scholarship Income: As mentioned earlier, the portion of a scholarship used for non-qualified expenses is considered unearned income.

Understanding these examples can help you identify sources of unearned income in your own financial situation, allowing you to plan your taxes more effectively.

1.3. Unearned Income: What It Means for Partnerships

Can unearned income influence partnerships? Yes, it can, particularly in how partners manage their tax liabilities and plan for financial growth. For instance, a partnership might invest in assets that generate unearned income, like real estate or stocks. This income would then be distributed among the partners, affecting their individual tax obligations.

Moreover, understanding the nature of unearned income can help partners make informed decisions about how to structure their agreements. According to a study by the University of Texas at Austin’s McCombs School of Business in July 2025, partnerships that proactively address tax implications related to unearned income tend to have more sustainable financial outcomes. This proactive approach includes strategies for minimizing tax liabilities and maximizing after-tax returns for all partners involved.

2. Navigating the Nuances: Are Grants Considered Unearned Income?

Are all grants considered unearned income? Not necessarily. It largely depends on the grant’s purpose and how the funds are used. Grants intended for specific purposes, like covering tuition or research expenses, may not be considered taxable income if used accordingly. However, grants used for personal expenses or unrelated purposes are typically classified as unearned income and are subject to taxation.

The key lies in understanding the terms and conditions of the grant and how it aligns with IRS regulations. Let’s break this down further.

2.1. Grants as Income: Understanding the Tax Implications

How do grants become taxable income? When grants are used for non-qualified expenses, they become taxable income. According to Section 117 of the Internal Revenue Code, scholarships or grants used for tuition, fees, books, and required equipment are generally tax-free. However, if the grant covers expenses such as room and board, travel, or other personal costs, those amounts are considered taxable income.

This is particularly relevant for students receiving scholarships that exceed the cost of tuition and required expenses. The excess amount is often treated as unearned income and may be subject to the kiddie tax if the student is a qualifying child.

2.2. Qualified vs. Non-Qualified Expenses: What’s the Difference?

What differentiates qualified from non-qualified expenses? Qualified expenses are those directly related to your education, such as tuition, mandatory fees, and required books and equipment. Non-qualified expenses, on the other hand, include room and board, travel, and other personal expenses that are not directly tied to your education.

For example, if you receive a scholarship of $20,000 and your tuition is $15,000, the $5,000 difference is taxable if used for non-qualified expenses. It’s essential to keep detailed records of how grant funds are used to accurately report income and avoid potential tax issues.

2.3. Specific Types of Grants and Their Tax Status

What are the tax implications for different types of grants? Let’s examine some specific examples:

- Educational Grants: These are generally tax-free if used for qualified education expenses. This includes scholarships and fellowships.

- Research Grants: If a research grant covers expenses directly related to the research project, it may not be taxable. However, any portion used for personal expenses is taxable.

- Business Grants: Grants awarded to businesses are typically considered taxable income. However, there may be deductions available for expenses related to the grant.

- Disaster Relief Grants: These grants are often tax-free, as they are intended to help individuals recover from disasters.

- Government Grants: The tax status of government grants varies depending on the specific program and its purpose. Some may be taxable, while others are not.

It’s crucial to consult with a tax professional to determine the tax status of any grant you receive.

2.4. How Grants Affect Strategic Partnerships

How do grants impact strategic partnerships? Grants can play a pivotal role in fostering strategic partnerships, particularly in fields like research and development. For instance, two companies might collaborate on a research project funded by a grant. In such cases, it’s essential to clearly define how the grant funds will be used and how any resulting income will be distributed.

According to Harvard Business Review, successful partnerships often have detailed agreements outlining financial responsibilities and tax implications. This includes how grant funds are allocated, how expenses are tracked, and how any taxable income is reported. Clear communication and meticulous record-keeping are key to avoiding disputes and ensuring compliance with tax regulations.

Detailed tax record keeping

Detailed tax record keeping

3. The Kiddie Tax and Unearned Income: What You Need to Know

What is the kiddie tax, and how does it relate to unearned income? The kiddie tax is a set of rules that taxes the unearned income of children at the tax rates of trusts and estates, which are generally higher than individual rates. This tax applies to children under a certain age who have unearned income exceeding a certain threshold.

Originally introduced to prevent wealthy families from shifting income to their children to avoid higher tax rates, the kiddie tax has significant implications for students with taxable scholarship income.

3.1. Understanding the Kiddie Tax Rules

What are the specific rules of the kiddie tax? As of 2018, the kiddie tax applies to children who meet the following criteria, as outlined in Section 1(g)(2) of the Internal Revenue Code:

- The child is:

- Under the age of 18;

- Age 18 and has earned income that is less than half of their own support; or

- Ages 19 to 23, a full-time student, and has earned income that is less than half of their own support.

- Has at least one living parent.

- Is not married and filing a joint return with their spouse.

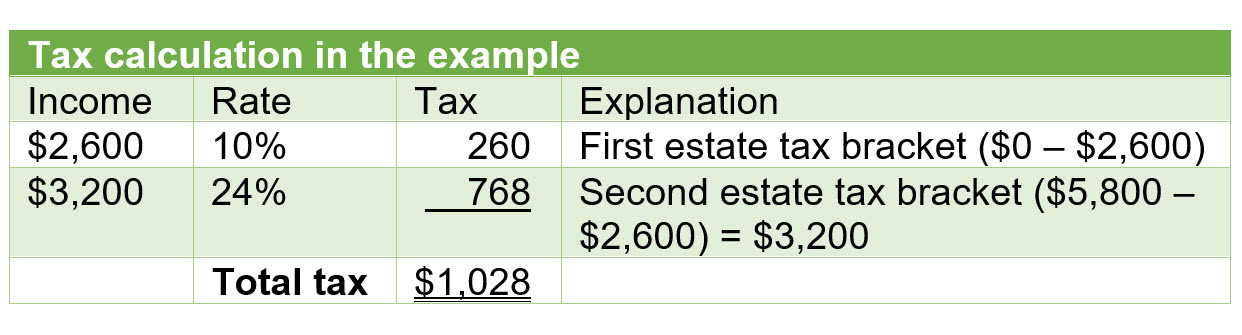

If a child meets these criteria and has unearned income exceeding twice the reduced standard deduction amount for a dependent (which was $2,100 in 2018), the kiddie tax applies. The first $1,050 of unearned income is offset by the standard deduction, the next $1,050 is taxed at the child’s rate, and any amount above $2,100 is taxed at the trust and estate tax rates.

3.2. How Scholarships and Grants Impact the Kiddie Tax

How do scholarships and grants affect the kiddie tax? If a student receives a scholarship or grant that covers non-qualified expenses, the taxable portion is considered unearned income and may be subject to the kiddie tax. This can be a significant issue for students whose scholarships exceed the cost of tuition and required expenses.

For example, consider a student who receives a $50,000 scholarship to cover tuition, room, and board. If the tuition is $32,000 and room and board are $18,000, the $18,000 used for room and board is taxable unearned income. If the student meets the criteria for the kiddie tax, this income will be taxed at the higher trust and estate tax rates.

3.3. Strategies to Minimize the Kiddie Tax

What strategies can minimize the kiddie tax? There are several strategies to consider:

- Maximize Qualified Expenses: Ensure that grant funds are used primarily for qualified education expenses such as tuition, fees, and required books and equipment.

- Reduce Unearned Income: Look for ways to reduce other sources of unearned income, such as shifting assets to tax-advantaged accounts or deferring income to a later year.

- Increase Earned Income: If possible, increase the child’s earned income to exceed half of their support, which would disqualify them from the kiddie tax.

- Consult a Tax Professional: Seek advice from a qualified tax professional who can help you navigate the complexities of the kiddie tax and develop a tailored strategy.

3.4. The Intersection of Kiddie Tax and Income Partnerships

How does the kiddie tax relate to income partnerships? While the kiddie tax primarily affects individual students, it can also have implications for families involved in income partnerships. For instance, if a child is a beneficiary of a family partnership that generates unearned income, that income may be subject to the kiddie tax.

According to Entrepreneur.com, families should carefully structure their partnerships to minimize the tax burden on all members, including children. This may involve strategies such as distributing income in a way that maximizes tax benefits or shifting assets to different types of accounts. Careful planning and professional advice are essential to navigating these complexities.

4. Strategies for Reducing Unearned Income from Grants

How can you reduce the amount of unearned income from grants? Students who find themselves in a situation where they have taxable scholarships can make adjustments in certain cases. Additional expenses, above those reported on Form 1098-T, should be considered by the taxpayer to reduce the taxable scholarship amount. The institution is only required to report on Form 1098-T qualified tuition and related expenses that are billed. However, additional expenses may qualify as qualified tuition and related expenses. To be allowable, the expenses must be required of all students in the course and cannot be considered incidental expenses.

4.1. Documenting Qualified Expenses

What steps can you take to document qualified expenses? To reduce taxable scholarship income, meticulous record-keeping is essential. Keep receipts and documentation for all qualified education expenses, including:

- Tuition bills

- Fee statements

- Textbook receipts

- Equipment invoices

Ensure that these expenses are required for enrollment or attendance at the educational institution. For example, a textbook that is listed as optional on the course syllabus would not qualify, but a course book that is listed as required would be. Additional expenses, such as required books or equipment that are not run through the educational institution’s billing software, may increase the qualified tuition and fees.

4.2. Maximizing Educational Tax Credits

How can educational tax credits help? Educational tax credits, such as the American Opportunity Tax Credit (AOTC) and the Lifetime Learning Credit (LLC), can help reduce your overall tax liability. The AOTC provides a credit of up to $2,500 per student for the first four years of college, while the LLC provides a credit of up to $2,000 per tax return for qualified education expenses.

To claim these credits, you must meet certain eligibility requirements and file Form 8863, Education Credits (American Opportunity and Lifetime Learning Credits), with your tax return. These credits can significantly reduce the tax burden associated with unearned income from grants.

4.3. Shifting Income to Tax-Advantaged Accounts

How can tax-advantaged accounts help reduce unearned income? Consider shifting income to tax-advantaged accounts such as 529 plans or Coverdell Education Savings Accounts. These accounts allow you to save for education expenses on a tax-free or tax-deferred basis.

Distributions from 529 plans used for qualified education expenses are tax-free, which can help reduce the amount of taxable unearned income. Similarly, Coverdell ESAs offer tax-free growth and withdrawals for qualified education expenses.

4.4. Deferring Income to Future Years

Is it possible to defer income to future years? In some cases, it may be possible to defer income to a future year when the student is no longer subject to the kiddie tax. This could involve delaying the receipt of grant funds or structuring payments in a way that minimizes the tax impact.

However, this strategy requires careful planning and coordination with the educational institution and any grant providers. Consult with a tax professional to determine if deferring income is a viable option for your situation.

5. The Role of Form 1098-T in Reporting Scholarship Income

What is Form 1098-T, and how does it relate to scholarship income? Every eligible educational institution is required to file a Form 1098-T, Tuition Statement, for each student that is enrolled and has a reportable transaction. However, some exceptions apply for courses taken for no academic credit, for nonresident alien students, and for students whose qualified tuition is paid in full by scholarships or waived.

This form is crucial for reporting scholarship income and determining the taxable amount.

5.1. Understanding What’s Reported on Form 1098-T

What information is included on Form 1098-T? On the Form 1098-T, the educational institution is to report amounts received as payment for qualified tuition and related expenses less reimbursements or refunds during the calendar year in box 1 and all scholarships or grants in box 5. The scholarships that are listed in box 5 include all scholarships the institution knows or should know about, regardless of whether the payment is received directly by the institution, or a check is endorsed by the student.

This form provides a summary of the payments you made for qualified tuition and related expenses, as well as the amount of any scholarships or grants you received.

5.2. Limitations of Form 1098-T

What are the limitations of Form 1098-T? From the Form 1098-T requirements, one can see that in many cases, in an ideal world, as long as the educational institution properly completes the Form 1098-T, any total scholarship amount received in excess of qualified tuition should be easily calculated by taking the scholarships listed in box 5 and subtracting qualified tuition payments as reported in box 1. However, it is not so straightforward. Form 1098-T has specific exceptions where the form does not need to be filed, such as when qualified tuition is paid in full. In many of the cases where scholarships end up being taxable, the tuition is paid in full and thereby a Form 1098-T is not required. In addition, the educational institution will most likely report any scholarship that is received by the institution, but there may be situations where the scholarship is received directly by the student and not reported to the institution. Both of these situations present a gap in the amount of taxable income that can be calculated from the Form 1098-T by the taxpayer and by the IRS.

While Form 1098-T is a valuable resource, it has certain limitations. For example, it may not include all qualified education expenses, such as required books or equipment purchased outside of the educational institution. Additionally, it may not accurately reflect the amount of scholarships or grants you received if the institution was not aware of all sources of funding.

5.3. Reconciling Form 1098-T with Your Records

How should you reconcile Form 1098-T with your own records? To ensure accuracy, it’s essential to reconcile Form 1098-T with your own records. Compare the amounts reported on the form with your tuition statements, scholarship documentation, and receipts for qualified education expenses.

If you find any discrepancies, contact the educational institution to request a corrected Form 1098-T. Keep detailed records of all payments and expenses to support your tax return.

5.4. Using Form 1098-T to Calculate Taxable Scholarship Income

How can you use Form 1098-T to calculate taxable scholarship income? In cases where a tax preparer believes a student might be in a taxable situation because of scholarships, a good starting point for making this calculation is Form 1098-T. However, details for the account the student has with the college/university may be needed in some situations. The account detail should show information for charges such as tuition, fees, room and board, and possibly other charges for items such as books. It will also present what the institution shows for financial aid, which includes grants and scholarships. In addition to Form 1098-T and the student’s account detail, a general inquiry for any other scholarships received or expenses paid may be necessary. However, the preparer should keep in mind that, generally, large scholarships are received directly by the institution.

To calculate the taxable portion of your scholarship, subtract the amount of qualified tuition and related expenses (reported in box 1) from the total amount of scholarships and grants (reported in box 5). The difference is the amount of taxable scholarship income that must be reported on your tax return.

6. Real-World Examples and Case Studies

How do these rules apply in real-world situations? Let’s explore some case studies to illustrate the concepts discussed.

6.1. Case Study 1: The Full-Ride Scholarship

Consider a student who receives a full-ride scholarship to a private university. The scholarship covers tuition, fees, room, and board, totaling $60,000 per year. The tuition and fees amount to $40,000, while room and board cost $20,000.

In this case, the $40,000 used for tuition and fees is tax-free. However, the $20,000 used for room and board is considered taxable unearned income. If the student is subject to the kiddie tax, this income will be taxed at the higher trust and estate tax rates.

To minimize the tax impact, the student could explore strategies such as documenting additional qualified education expenses or shifting assets to tax-advantaged accounts.

6.2. Case Study 2: The Research Grant

A graduate student receives a $30,000 research grant to fund their dissertation project. The grant covers research expenses, travel, and a stipend for living expenses. The student spends $15,000 on research-related expenses, $5,000 on travel, and $10,000 on living expenses.

In this scenario, the $15,000 used for research expenses may be tax-free if it is directly related to the research project. However, the $5,000 used for travel and the $10,000 used for living expenses are considered taxable unearned income.

The student should keep detailed records of all research-related expenses to justify the tax-free portion of the grant.

6.3. Case Study 3: The Business Grant

A small business owner receives a $50,000 grant to expand their operations. The grant is used to purchase new equipment, hire additional staff, and cover marketing expenses.

In this case, the entire $50,000 grant is considered taxable income. However, the business owner can deduct expenses related to the grant, such as the cost of new equipment, salaries, and marketing expenses.

The business owner should keep detailed records of all expenses to maximize their deductions and minimize their tax liability.

6.4. How Partnerships Can Learn from These Cases

What can partnerships learn from these case studies? These case studies highlight the importance of understanding the tax implications of grants and scholarships, particularly in the context of income partnerships. By carefully documenting expenses, maximizing deductions, and seeking professional advice, partnerships can minimize their tax liability and maximize their financial success.

According to a study by the American Institute of CPAs (AICPA), partnerships that proactively manage their tax obligations tend to be more profitable and sustainable. This includes developing strategies for minimizing unearned income and taking advantage of available tax credits and deductions.

7. Expert Tips for Navigating Grant Taxation

What are some expert tips for navigating grant taxation? To effectively manage grant taxation, consider the following tips from tax professionals and financial advisors.

7.1. Consult with a Tax Professional

Seek advice from a qualified tax professional who can help you navigate the complexities of grant taxation and develop a tailored strategy. A tax professional can assess your specific situation, identify potential tax issues, and recommend strategies for minimizing your tax liability.

7.2. Keep Detailed Records

Maintain meticulous records of all grant-related income and expenses. This includes tuition statements, scholarship documentation, receipts for qualified education expenses, and documentation of research-related expenses.

7.3. Understand the Grant Terms and Conditions

Carefully review the terms and conditions of your grant to understand how the funds can be used and what expenses are covered. This will help you determine the taxable portion of the grant and plan accordingly.

7.4. Explore Tax-Advantaged Savings Options

Consider using tax-advantaged savings options such as 529 plans or Coverdell ESAs to save for education expenses on a tax-free or tax-deferred basis.

7.5. Stay Informed About Tax Law Changes

Stay up-to-date on the latest tax law changes that may affect grant taxation. Tax laws are constantly evolving, so it’s essential to stay informed and adjust your strategies accordingly.

8. Resources and Tools for Further Research

What resources and tools are available for further research? To deepen your understanding of grant taxation and related topics, consider the following resources:

- IRS Publications: IRS Publication 970, Tax Benefits for Education, provides detailed information on tax benefits for education expenses, including scholarships and grants.

- AICPA: The American Institute of CPAs (AICPA) offers resources and guidance on tax planning and compliance.

- Tax Foundation: The Tax Foundation provides analysis and insights on tax policy issues.

- Financial Planning Association (FPA): The FPA offers resources and guidance on financial planning, including tax planning.

- income-partners.net: Explore income-partners.net for insights on strategic partnerships and income maximization.

9. FAQ: Addressing Common Questions About Grants and Unearned Income

Here are some frequently asked questions about grants and unearned income:

- Are all scholarships taxable?

- No, scholarships used for qualified education expenses such as tuition, fees, and required books are generally tax-free.

- What are qualified education expenses?

- Qualified education expenses include tuition, fees, and required books and equipment for enrollment or attendance at an educational institution.

- What is the kiddie tax?

- The kiddie tax is a set of rules that taxes the unearned income of children at the tax rates of trusts and estates.

- How does the kiddie tax affect scholarship income?

- If a student receives a scholarship that covers non-qualified expenses, the taxable portion is considered unearned income and may be subject to the kiddie tax.

- What is Form 1098-T?

- Form 1098-T, Tuition Statement, is a form that educational institutions are required to file for each student who is enrolled and has a reportable transaction.

- How can I reduce the amount of unearned income from grants?

- You can reduce unearned income by documenting qualified expenses, maximizing educational tax credits, shifting income to tax-advantaged accounts, and deferring income to future years.

- Is it possible to defer income to future years?

- In some cases, it may be possible to defer income to a future year when the student is no longer subject to the kiddie tax.

- What is the American Opportunity Tax Credit (AOTC)?

- The AOTC provides a credit of up to $2,500 per student for the first four years of college.

- What is the Lifetime Learning Credit (LLC)?

- The LLC provides a credit of up to $2,000 per tax return for qualified education expenses.

- Where can I find more information about grant taxation?

- You can find more information about grant taxation in IRS Publication 970, Tax Benefits for Education, and other resources from the IRS, AICPA, and other organizations.

10. Conclusion: Maximizing Opportunities While Minimizing Tax Burdens

How can individuals and partnerships maximize opportunities while minimizing tax burdens? Understanding the nuances of grant taxation is crucial for individuals and partnerships seeking to maximize opportunities while minimizing tax burdens. By carefully documenting expenses, exploring tax-advantaged savings options, and seeking professional advice, you can navigate the complexities of grant taxation and achieve your financial goals.

At income-partners.net, we’re dedicated to providing you with the insights and resources you need to succeed. Whether you’re a student seeking to minimize the tax impact of scholarship income or a business owner looking to expand your operations with grant funding, we’re here to help. Explore our website for more information on strategic partnerships and income maximization.

Ready to take the next step? Contact us at Address: 1 University Station, Austin, TX 78712, United States or Phone: +1 (512) 471-3434, or visit our website at income-partners.net to discover how we can help you achieve your financial goals. Explore the diverse partnership opportunities and effective relationship-building strategies available on income-partners.net. Uncover potential collaborations and begin constructing lucrative partnerships immediately.