Yes, gains and losses are indeed reported on the income statement. At income-partners.net, we understand how crucial it is for entrepreneurs, investors, and business professionals like you to accurately track and report these figures for a clear financial overview. Knowing this, you can strategically identify potential collaborators, maximize your revenue streams, and make well-informed business choices to boost profitability and grow your business. Let’s explore how this reporting can influence your overall financial health, providing you with valuable insights and strategic advantages.

1. Understanding the Income Statement

The income statement, often referred to as the profit and loss (P&L) statement, is a financial report that summarizes a company’s financial performance over a specific period. The University of Texas at Austin’s McCombs School of Business emphasizes that a clear income statement is vital for assessing a company’s profitability and operational efficiency, offering insights into revenue, expenses, gains, and losses.

1.1. Key Components of an Income Statement

An income statement includes several key components that provide a comprehensive view of a company’s financial performance:

- Revenue: Represents the total income generated from the company’s primary business activities.

- Cost of Goods Sold (COGS): Includes the direct costs associated with producing goods or services.

- Gross Profit: Calculated by subtracting COGS from revenue, indicating the profit earned before operating expenses.

- Operating Expenses: Encompasses all costs incurred to keep the business running, such as salaries, rent, and utilities.

- Operating Income: Derived by subtracting operating expenses from gross profit, reflecting the profit earned from core business operations.

- Other Income and Expenses: Includes income and expenses not directly related to the company’s primary operations.

- Gains and Losses: Represents profits or losses from activities outside the company’s normal business operations.

- Income Tax Expense: The amount of income tax owed for the reported period.

- Net Income: The final profit after deducting all expenses, including income tax.

1.2. Significance of the Income Statement

The income statement is a critical tool for various stakeholders:

- Investors: Use it to evaluate a company’s profitability and potential for future earnings.

- Creditors: Assess a company’s ability to repay debts.

- Management: Monitors financial performance and makes strategic decisions.

- Analysts: Analyze trends and compare performance against industry benchmarks.

- Partners: Evaluate performance before getting into any partnerships with an outside entity

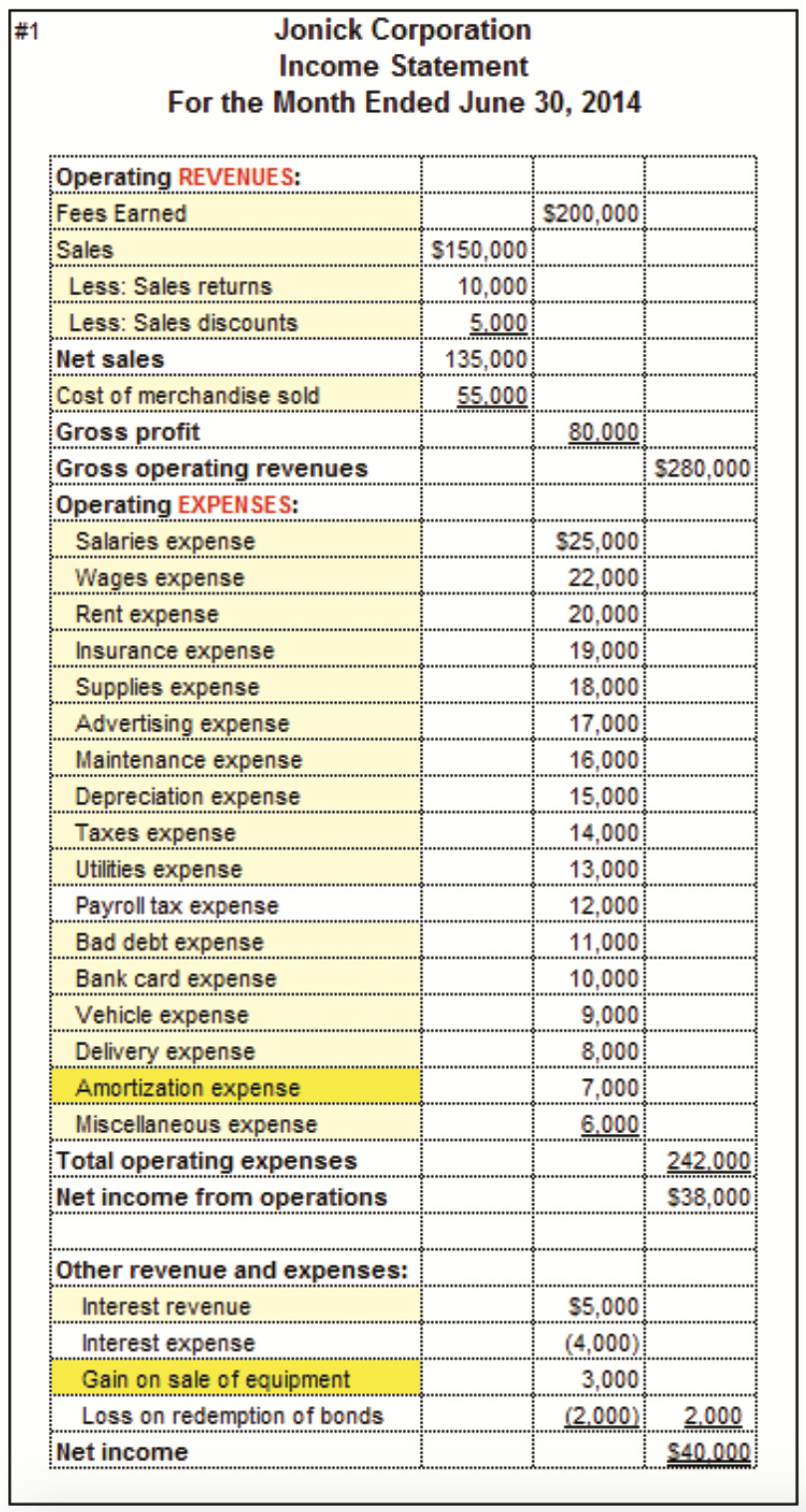

Screen Shot 2020-06-14 at 6.08.33 PM.png

Screen Shot 2020-06-14 at 6.08.33 PM.png

2. What are Gains?

Gains are increases in a company’s wealth resulting from transactions or events that are not part of its ordinary business activities. Harvard Business Review highlights that gains often come from non-recurring events, such as selling assets or investments.

2.1. Types of Gains

There are several types of gains that a company might report on its income statement:

- Gain on Sale of Assets: Occurs when a company sells an asset (e.g., property, equipment, or investments) for more than its book value.

- Gain on Investment: Results from an increase in the value of investments, such as stocks or bonds, when sold.

- Gain on Debt Restructuring: Arises when a company renegotiates its debt terms, resulting in a reduction of liabilities.

- Gain on Insurance Settlement: Occurs when a company receives insurance proceeds that exceed the book value of the damaged asset.

- Foreign Exchange Gain: Results from fluctuations in exchange rates that increase the value of foreign currency holdings.

2.2. Examples of Gains

Consider these scenarios to illustrate how gains are reported:

- Example 1: Sale of Equipment: A company sells a piece of equipment for $50,000. The equipment’s book value (original cost less accumulated depreciation) is $30,000. The company records a gain of $20,000 ($50,000 – $30,000) on the income statement.

- Example 2: Investment Appreciation: A company sells stocks for $75,000. The original purchase price was $60,000. The company reports a gain of $15,000 ($75,000 – $60,000) on the income statement.

- Example 3: Debt Restructuring: A company renegotiates its loan terms and reduces its debt by $25,000. The company records a gain of $25,000 on the income statement.

2.3. Reporting Gains on the Income Statement

Gains are typically reported in the “Other Income and Expenses” section of the income statement. This section includes items that are not part of the company’s core business operations. The gain is added to the company’s income, increasing its net income.

3. What are Losses?

Losses are decreases in a company’s wealth resulting from transactions or events that are not part of its ordinary business activities. Losses often stem from unexpected events or poor investment decisions, according to Entrepreneur.com.

3.1. Types of Losses

There are several types of losses that a company might report on its income statement:

- Loss on Sale of Assets: Occurs when a company sells an asset for less than its book value.

- Loss on Investment: Results from a decrease in the value of investments when sold.

- Impairment Loss: Arises when the value of an asset declines below its carrying value and is written down.

- Loss from Discontinued Operations: Occurs when a company sells or abandons a significant part of its business.

- Loss on Insurance Settlement: Results when insurance proceeds are less than the book value of the damaged asset.

- Foreign Exchange Loss: Results from fluctuations in exchange rates that decrease the value of foreign currency holdings.

3.2. Examples of Losses

Consider these examples to illustrate how losses are reported:

- Example 1: Sale of Land: A company sells land for $100,000. The land’s book value is $120,000. The company records a loss of $20,000 ($100,000 – $120,000) on the income statement.

- Example 2: Investment Decline: A company sells bonds for $40,000. The original purchase price was $50,000. The company reports a loss of $10,000 ($40,000 – $50,000) on the income statement.

- Example 3: Asset Impairment: A company determines that the value of its equipment has declined due to technological obsolescence. The company writes down the asset by $15,000, recording an impairment loss on the income statement.

3.3. Reporting Losses on the Income Statement

Losses are also reported in the “Other Income and Expenses” section of the income statement. The loss is subtracted from the company’s income, decreasing its net income.

4. Key Differences Between Gains and Losses

Understanding the distinction between gains and losses is crucial for accurate financial reporting and decision-making. Here’s a summary of the key differences:

| Feature | Gain | Loss |

|---|---|---|

| Definition | Increase in wealth from non-ordinary business activities | Decrease in wealth from non-ordinary business activities |

| Source | Sale of assets above book value, investment appreciation, debt reduction | Sale of assets below book value, investment decline, asset impairment |

| Impact | Increases net income | Decreases net income |

| Reporting | Reported in “Other Income and Expenses” section of income statement | Reported in “Other Income and Expenses” section of the income statement |

5. Impact on Financial Statements

Gains and losses significantly impact a company’s financial statements.

5.1. Income Statement Impact

Gains increase net income, making the company appear more profitable. This can positively influence investor confidence and stock prices. Conversely, losses decrease net income, potentially raising concerns among investors and creditors.

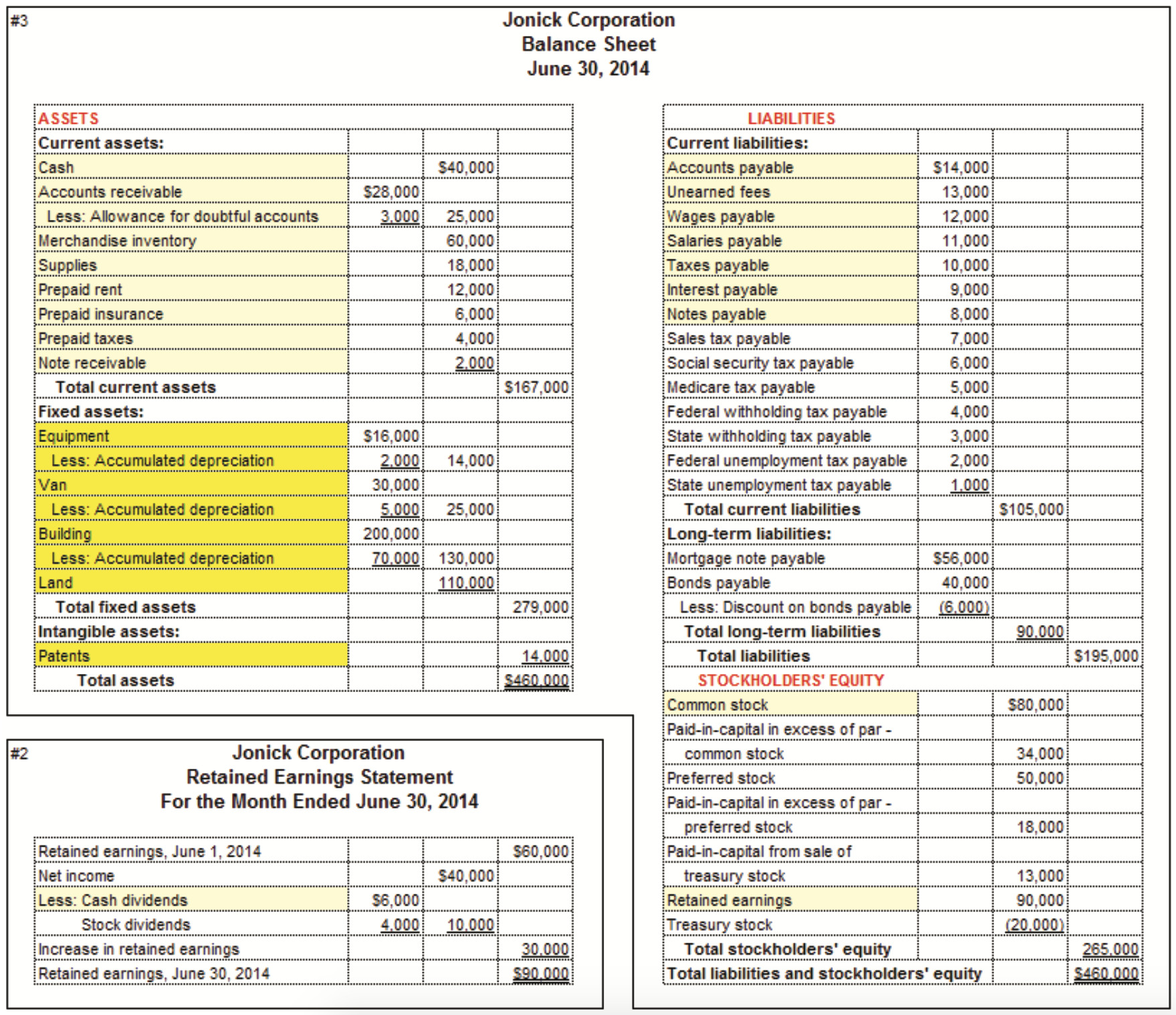

5.2. Balance Sheet Impact

Gains and losses can indirectly affect the balance sheet. For example, a gain from selling an asset increases the company’s retained earnings, which is part of the equity section of the balance sheet. A loss, on the other hand, decreases retained earnings.

5.3. Statement of Cash Flows Impact

Gains and losses can also impact the statement of cash flows. While gains and losses themselves are non-cash transactions, they can affect the cash flow from investing activities. For example, the cash received from selling an asset at a gain is reported as an inflow in the investing activities section.

6. Accounting Standards and Regulations

The reporting of gains and losses is governed by accounting standards and regulations.

6.1. Generally Accepted Accounting Principles (GAAP)

In the United States, companies must follow GAAP when preparing financial statements. GAAP provides guidelines on how to recognize, measure, and report gains and losses.

6.2. International Financial Reporting Standards (IFRS)

Companies in many other countries follow IFRS. IFRS also provides standards for reporting gains and losses, which may differ slightly from GAAP.

6.3. Tax Implications

Gains and losses have tax implications. Gains are usually taxable, while losses can often be used to offset taxable income. Understanding these tax implications is essential for effective financial planning.

7. Strategic Implications for Your Business

Understanding how gains and losses are reported can offer strategic advantages for your business.

7.1. Improved Financial Analysis

By accurately tracking and reporting gains and losses, you can gain a clearer understanding of your company’s financial performance. This enables you to make more informed decisions about investments, operations, and financing.

7.2. Enhanced Investor Relations

Transparent and accurate financial reporting builds trust with investors. Demonstrating a clear understanding of gains and losses can enhance investor confidence and attract capital.

7.3. Better Risk Management

Identifying the sources of gains and losses helps you assess risks and opportunities. This allows you to develop strategies to mitigate risks and capitalize on opportunities, leading to more sustainable growth.

7.4. Strategic Partnerships

Understanding your company’s financial strengths and weaknesses, as highlighted by gains and losses, can aid in forming strategic partnerships. income-partners.net can connect you with partners who complement your business, driving mutual growth and profitability.

8. Practical Examples for Businesses in Austin, TX

For businesses in Austin, TX, understanding the local economic landscape and industry-specific factors is crucial.

8.1. Technology Sector

In the tech sector, gains often come from successful product launches or strategic acquisitions. Losses can result from failed projects or market downturns. Accurately reporting these gains and losses helps tech companies attract investment and manage resources effectively.

8.2. Real Estate Sector

Real estate companies in Austin can experience gains from property sales and development projects. Losses might occur due to market fluctuations or unsuccessful investments. Proper reporting ensures compliance with regulations and helps in securing financing.

8.3. Small Businesses and Startups

Small businesses and startups need to carefully manage their finances to ensure sustainability. Reporting gains from successful marketing campaigns or cost-saving measures can boost morale and attract investors. Losses from unsuccessful ventures should be analyzed to prevent future occurrences.

9. Common Mistakes to Avoid

Several common mistakes can undermine the accuracy of financial reporting.

9.1. Misclassifying Gains and Losses

Incorrectly classifying gains and losses can distort the income statement and mislead stakeholders. Ensure that all gains and losses are properly identified and reported in the “Other Income and Expenses” section.

9.2. Failing to Recognize Impairment Losses

Ignoring impairment losses can overstate the value of assets on the balance sheet. Regularly assess assets for impairment and record any necessary write-downs.

9.3. Inadequate Documentation

Poor documentation can make it difficult to verify gains and losses. Maintain thorough records of all transactions and events that result in gains or losses.

9.4. Neglecting Tax Implications

Failing to consider the tax implications of gains and losses can lead to inaccurate tax planning. Consult with a tax professional to understand the tax consequences of your financial transactions.

10. How Income-Partners.Net Can Help

income-partners.net offers a range of resources and tools to help you navigate the complexities of financial reporting and strategic partnerships.

10.1. Expert Insights

Access expert insights on financial analysis, risk management, and strategic planning. Our articles, webinars, and workshops provide practical guidance to help you make informed decisions.

10.2. Partnership Opportunities

Connect with potential partners who can complement your business and drive growth. Our platform facilitates networking and collaboration, helping you find the right partners for your specific needs.

10.3. Customizable Solutions

Benefit from customizable solutions tailored to your industry and business goals. Our team of experts can help you develop financial strategies and partnership agreements that align with your objectives.

10.4. Comprehensive Resources

Explore our comprehensive library of resources, including templates, guides, and case studies. These resources provide valuable information and practical tools to support your financial and strategic initiatives.

11. Case Studies: Successful Partnerships

Examining successful partnerships can provide valuable insights and inspiration.

11.1. Technology Partnership

Two tech companies in Austin partnered to develop a new software solution. By combining their expertise and resources, they achieved significant gains in revenue and market share.

11.2. Real Estate Collaboration

A real estate developer and a construction company collaborated on a residential project. Their partnership resulted in a successful development with high returns on investment.

11.3. Startup Alliance

Two startups formed an alliance to share resources and expand their market reach. Their collaboration led to increased efficiency and significant gains in customer acquisition.

12. Future Trends in Financial Reporting

Staying informed about future trends in financial reporting is essential for maintaining a competitive edge.

12.1. Increased Automation

Automation is transforming financial reporting, making it more efficient and accurate. Embrace automation tools to streamline your processes and reduce errors.

12.2. Enhanced Data Analytics

Data analytics is playing a growing role in financial analysis. Use data analytics tools to gain deeper insights into your financial performance and identify opportunities for improvement.

12.3. Greater Transparency

Transparency is becoming increasingly important to stakeholders. Provide clear and accurate financial information to build trust and maintain a positive reputation.

12.4. Focus on Sustainability

Sustainability reporting is gaining traction. Incorporate sustainability metrics into your financial reports to demonstrate your commitment to environmental and social responsibility.

13. Practical Tips for Accurate Reporting

To ensure accurate reporting of gains and losses, consider these practical tips:

- Maintain Detailed Records: Keep thorough records of all transactions and events that result in gains or losses.

- Follow Accounting Standards: Adhere to GAAP or IFRS guidelines when preparing financial statements.

- Seek Professional Advice: Consult with a financial professional to ensure compliance and accuracy.

- Regularly Review Financial Statements: Review your financial statements regularly to identify any errors or discrepancies.

- Use Accounting Software: Implement accounting software to automate and streamline your financial reporting processes.

14. Maximizing Your Business Potential

By understanding and accurately reporting gains and losses, you can maximize your business potential.

14.1. Attract Investors

Transparent and accurate financial reporting attracts investors and increases your access to capital.

14.2. Improve Decision-Making

Informed decision-making leads to better outcomes and more sustainable growth.

14.3. Optimize Resource Allocation

Effective resource allocation enhances efficiency and profitability.

14.4. Build Strategic Partnerships

Strategic partnerships drive innovation and expand your market reach.

Screen Shot 2020-06-14 at 6.09.47 PM.png

Screen Shot 2020-06-14 at 6.09.47 PM.png

15. Partnering with Income-Partners.Net for Success

income-partners.net is your dedicated partner in achieving financial clarity and strategic growth. We provide the resources, tools, and expertise you need to navigate the complexities of financial reporting and build successful partnerships.

15.1. Personalized Support

Our team of experts offers personalized support to address your specific business needs.

15.2. Proven Strategies

We provide proven strategies and best practices to help you achieve your financial goals.

15.3. Collaborative Environment

Our platform fosters a collaborative environment where you can connect with partners and share insights.

15.4. Long-Term Growth

We are committed to helping you achieve long-term growth and success.

16. Expert Opinions on Gains and Losses

Industry experts emphasize the importance of understanding gains and losses for sound financial management.

16.1. Financial Analysts

Financial analysts highlight that accurately reporting gains and losses is crucial for evaluating a company’s financial health and making investment decisions.

16.2. Business Consultants

Business consultants advise companies to carefully analyze the sources of gains and losses to identify strengths and weaknesses.

16.3. Accounting Professionals

Accounting professionals stress the importance of following accounting standards and seeking expert advice to ensure accurate reporting.

16.4. Entrepreneurs

Entrepreneurs emphasize that understanding gains and losses is essential for making informed business decisions and managing risk.

17. Navigating Regulatory Changes

Staying up-to-date with regulatory changes is crucial for compliance.

17.1. Monitor Updates

Monitor updates from regulatory agencies, such as the Securities and Exchange Commission (SEC) and the Financial Accounting Standards Board (FASB).

17.2. Seek Legal Advice

Consult with legal professionals to ensure compliance with all applicable laws and regulations.

17.3. Implement Changes

Implement any necessary changes to your financial reporting processes to reflect new regulations.

17.4. Train Staff

Train your staff on the latest regulatory requirements and best practices.

18. Preparing for Future Economic Conditions

Preparing for future economic conditions is essential for business resilience.

18.1. Scenario Planning

Develop scenario plans to anticipate potential economic challenges and opportunities.

18.2. Risk Management

Implement risk management strategies to mitigate the impact of economic uncertainties.

18.3. Diversification

Diversify your business operations and investments to reduce your vulnerability to economic shocks.

18.4. Financial Reserves

Maintain adequate financial reserves to weather economic downturns.

19. Utilizing Technology for Financial Reporting

Technology plays a crucial role in modern financial reporting.

19.1. Accounting Software

Implement accounting software to automate and streamline your financial reporting processes.

19.2. Data Analytics Tools

Use data analytics tools to gain deeper insights into your financial performance.

19.3. Cloud Computing

Leverage cloud computing to enhance collaboration and accessibility.

19.4. Artificial Intelligence (AI)

Explore the potential of AI to improve the accuracy and efficiency of financial reporting.

20. Connecting with Partners on Income-Partners.Net

income-partners.net offers a unique platform to connect with partners who can help you achieve your financial goals.

20.1. Identify Potential Partners

Use our platform to identify potential partners who align with your business needs and goals.

20.2. Network and Collaborate

Network and collaborate with partners to share insights and resources.

20.3. Build Strategic Alliances

Build strategic alliances to drive innovation and expand your market reach.

20.4. Achieve Mutual Growth

Achieve mutual growth and success through collaborative partnerships.

FAQ: Gains and Losses on the Income Statement

Q1: What is the primary purpose of the income statement?

The primary purpose of the income statement is to report a company’s financial performance over a specific period by summarizing revenues, expenses, gains, and losses.

Q2: Where are gains and losses reported on the income statement?

Gains and losses are typically reported in the “Other Income and Expenses” section of the income statement.

Q3: What is the difference between a gain and a loss?

A gain is an increase in a company’s wealth from non-ordinary business activities, while a loss is a decrease in wealth from similar activities.

Q4: How do gains impact the income statement?

Gains increase net income on the income statement, making the company appear more profitable.

Q5: How do losses impact the income statement?

Losses decrease net income on the income statement, potentially raising concerns among investors and creditors.

Q6: Are gains and losses taxable?

Gains are usually taxable, while losses can often be used to offset taxable income.

Q7: What are some examples of gains?

Examples of gains include gain on sale of assets, gain on investment, and gain on debt restructuring.

Q8: What are some examples of losses?

Examples of losses include loss on sale of assets, loss on investment, and impairment loss.

Q9: Why is accurate reporting of gains and losses important?

Accurate reporting of gains and losses is crucial for improved financial analysis, enhanced investor relations, and better risk management.

Q10: How can income-partners.net help with financial reporting?

income-partners.net offers expert insights, partnership opportunities, customizable solutions, and comprehensive resources to help you navigate financial reporting complexities.

Ready to take your business to the next level? Visit income-partners.net today to explore partnership opportunities, discover proven strategies, and connect with experts who can help you achieve your financial goals. Don’t miss out on the chance to build strategic alliances, drive innovation, and achieve lasting success. Contact us at Address: 1 University Station, Austin, TX 78712, United States or Phone: +1 (512) 471-3434.