Fixed income and bonds are often used interchangeably, but are they truly the same? Understanding the nuances between these terms is crucial for making informed investment decisions and partnering effectively. At income-partners.net, we help you navigate these financial concepts and connect with partners who can amplify your income.

Fixed income encompasses a broader category of investments that provide a return in the form of fixed periodic payments, while bonds are a specific type of fixed-income security. This distinction is key for investors looking to diversify their portfolios and businesses seeking strategic partnerships. Let’s delve into the details to clarify their similarities and differences, helping you unlock more opportunities for revenue generation and collaboration.

1. What Exactly is Fixed Income?

Fixed income refers to any type of investment that provides a return in the form of fixed, periodic payments. This means that investors receive a predetermined amount of money at regular intervals, such as monthly, quarterly, or annually.

1.1 What are the Primary Characteristics of Fixed Income Investments?

Fixed income investments are characterized by:

- Predictable Income Stream: Regular, predetermined payments.

- Lower Risk Profile: Generally less volatile than equities.

- Diversification Benefits: Can balance a portfolio’s overall risk.

- Principal Preservation: Aims to return the initial investment at maturity.

1.2 What are Some Common Types of Fixed Income Investments?

Beyond bonds, fixed income includes various instruments:

- Bonds: Debt securities issued by corporations or governments.

- Certificates of Deposit (CDs): Savings accounts with a fixed interest rate and maturity date.

- Money Market Funds: Investments in short-term debt securities.

- Preferred Stock: A hybrid security with characteristics of both stocks and bonds.

- Mortgage-Backed Securities (MBS): Investments backed by a pool of mortgages.

2. What are Bonds?

Bonds are debt instruments issued by corporations, municipalities, states, or national governments to raise capital. When you buy a bond, you are essentially lending money to the issuer, who promises to repay the principal amount (also known as face value or par value) on a specific maturity date, along with periodic interest payments (coupon payments).

2.1 What are the Key Features of Bonds?

Understanding the structure of a bond is essential:

- Issuer: The entity borrowing the money (e.g., corporation, government).

- Principal (Face Value): The amount repaid at maturity.

- Coupon Rate: The fixed interest rate paid on the principal.

- Maturity Date: The date when the principal is repaid.

- Credit Rating: An assessment of the issuer’s creditworthiness (e.g., AAA, BBB, BB).

2.2 How Do Bonds Work?

Bonds function as a loan agreement between the issuer and the investor. The issuer sells bonds to raise funds, and in return, the investor receives periodic interest payments and the repayment of the principal at maturity. The price of a bond can fluctuate in the secondary market based on factors such as interest rate movements and the issuer’s creditworthiness.

3. What is the Relationship Between Fixed Income and Bonds?

Here’s where things get clearer: bonds are a subset of fixed income. All bonds are fixed-income investments because they provide a fixed stream of income through coupon payments. However, not all fixed-income investments are bonds.

3.1 How Do Bonds Fit Within the Fixed Income Universe?

Bonds represent a significant portion of the fixed-income market, offering a wide range of options for investors with different risk tolerances and investment goals. They can be categorized based on the issuer (e.g., government bonds, corporate bonds), credit quality (e.g., investment-grade bonds, high-yield bonds), and maturity (e.g., short-term bonds, long-term bonds).

3.2 What Distinguishes Bonds from Other Fixed Income Investments?

While bonds share the characteristic of providing fixed income, they differ from other fixed-income investments in several ways:

- Issuance: Bonds are typically issued in larger denominations and traded on exchanges.

- Market Volatility: Bond prices can fluctuate more than some other fixed-income investments like CDs.

- Credit Risk: Bonds carry credit risk, which is the risk that the issuer may default on its obligations.

- Interest Rate Sensitivity: Bond prices are inversely related to interest rate movements.

4. What are the Different Types of Bonds?

Bonds come in various forms, each with unique characteristics and risk profiles. Understanding these differences is crucial for making informed investment decisions.

4.1 Government Bonds

Issued by national governments to fund public spending, government bonds are generally considered low-risk, especially those issued by developed countries.

- Treasury Bonds (U.S.): Issued by the U.S. Department of the Treasury.

- Gilts (U.K.): Issued by the British government.

- Bunds (Germany): Issued by the German government.

4.2 Corporate Bonds

Issued by corporations to finance business operations, corporate bonds offer higher yields than government bonds but also carry greater credit risk.

- Investment-Grade Bonds: Bonds with high credit ratings (e.g., AAA, BBB).

- High-Yield Bonds (Junk Bonds): Bonds with lower credit ratings (e.g., BB, CCC), offering higher yields to compensate for the increased risk.

4.3 Municipal Bonds

Issued by state and local governments to fund public projects, municipal bonds often offer tax advantages to investors.

- General Obligation Bonds: Backed by the full faith and credit of the issuer.

- Revenue Bonds: Backed by the revenue generated from a specific project.

4.4 Other Types of Bonds

- Zero-Coupon Bonds: Sold at a discount and do not pay periodic interest.

- Inflation-Indexed Bonds (TIPS): Protect investors from inflation by adjusting the principal based on changes in the Consumer Price Index (CPI).

- Mortgage-Backed Securities (MBS): Represent ownership in a pool of mortgage loans.

5. What Factors Influence Bond Prices?

Bond prices are influenced by a variety of factors, including interest rates, inflation, credit risk, and market sentiment. Understanding these drivers is essential for predicting bond price movements and managing investment risk.

5.1 Interest Rates

Interest rates have an inverse relationship with bond prices. When interest rates rise, bond prices fall, and vice versa. This is because investors demand a higher yield to compensate for the increased opportunity cost of holding a bond with a lower coupon rate.

5.2 Credit Risk

Credit risk is the risk that the issuer may default on its obligations. Bonds with higher credit ratings are considered less risky and therefore have lower yields. Conversely, bonds with lower credit ratings have higher yields to compensate for the increased risk.

5.3 Inflation

Inflation erodes the purchasing power of fixed income payments. Investors demand higher yields to compensate for the expected rate of inflation. Inflation-indexed bonds (TIPS) offer protection against inflation by adjusting the principal based on changes in the CPI.

5.4 Market Sentiment

Market sentiment, or investor confidence, can also influence bond prices. During times of economic uncertainty, investors often flock to safe-haven assets like government bonds, driving up their prices and lowering their yields.

6. How to Invest in Fixed Income and Bonds?

Investing in fixed income and bonds can be done through various channels, including individual bonds, bond funds, and exchange-traded funds (ETFs). Each approach has its own advantages and disadvantages, depending on your investment goals and risk tolerance.

6.1 Buying Individual Bonds

Buying individual bonds allows you to customize your portfolio and control your maturity dates. However, it requires more research and expertise to select the right bonds and manage credit risk.

6.2 Bond Funds

Bond funds are mutual funds that invest in a portfolio of bonds. They offer diversification and professional management, but also come with fees and expenses.

6.3 Bond ETFs

Bond ETFs are exchange-traded funds that track a specific bond index. They offer diversification, liquidity, and lower expense ratios than bond funds.

7. What are the Risks and Rewards of Investing in Bonds?

Investing in bonds offers both potential rewards and risks. Understanding these trade-offs is crucial for making informed investment decisions and managing your portfolio effectively.

7.1 Rewards of Investing in Bonds

- Stable Income: Bonds provide a predictable stream of income through coupon payments.

- Capital Preservation: Bonds are generally less volatile than equities and can help preserve capital during market downturns.

- Diversification: Bonds can diversify a portfolio and reduce overall risk.

- Inflation Protection: Inflation-indexed bonds (TIPS) offer protection against inflation.

7.2 Risks of Investing in Bonds

- Interest Rate Risk: Rising interest rates can cause bond prices to fall.

- Credit Risk: The issuer may default on its obligations.

- Inflation Risk: Inflation can erode the purchasing power of fixed income payments.

- Liquidity Risk: Some bonds may be difficult to sell quickly at a fair price.

8. How Can Bonds Enhance Your Investment Portfolio?

Bonds play a crucial role in a well-diversified investment portfolio. They provide stability, income, and diversification, helping to balance the risk and return of your overall portfolio.

8.1 Diversification Benefits

Bonds have a low correlation with equities, meaning that they tend to perform differently in response to market conditions. This can help reduce the overall volatility of your portfolio and improve its risk-adjusted returns.

8.2 Income Generation

Bonds provide a steady stream of income through coupon payments, which can be especially valuable for retirees and other income-seeking investors.

8.3 Risk Management

Bonds are generally less volatile than equities and can help preserve capital during market downturns. They can also serve as a safe-haven asset during times of economic uncertainty.

9. What Role Do Bonds Play in Retirement Planning?

Bonds are an essential component of a well-designed retirement portfolio. They provide a stable source of income, help preserve capital, and reduce overall portfolio risk.

9.1 Income Replacement

Bonds can provide a reliable stream of income to replace lost wages during retirement.

9.2 Capital Preservation

Bonds can help protect your retirement savings from market volatility and preserve capital for future expenses.

9.3 Inflation Protection

Inflation-indexed bonds (TIPS) can help protect your retirement income from the eroding effects of inflation.

10. Why Partner with Income-Partners.net for Fixed Income Opportunities?

At income-partners.net, we understand the intricacies of fixed income and bonds. We connect you with strategic partners who can help you navigate the fixed-income landscape, identify lucrative opportunities, and maximize your income potential.

10.1 Access to Expert Insights

We provide access to expert insights and analysis on the fixed-income market, helping you stay informed and make informed investment decisions.

10.2 Strategic Partnership Opportunities

We connect you with strategic partners who can help you access exclusive fixed-income opportunities and optimize your portfolio.

10.3 Customized Solutions

We offer customized solutions tailored to your specific investment goals and risk tolerance.

10.4 Proven Track Record

We have a proven track record of helping our clients achieve their financial goals through strategic partnerships and informed investment decisions.

Here’s a table summarizing the key differences:

| Feature | Fixed Income | Bonds |

|---|---|---|

| Definition | Broad category of investments with fixed returns | Debt instruments issued by corporations/governments |

| Types | Bonds, CDs, Money Market Funds, etc. | Government, Corporate, Municipal, etc. |

| Risk Level | Varies depending on the specific investment | Varies depending on issuer and credit rating |

| Return | Fixed, periodic payments | Coupon payments and principal repayment |

| Market Volatility | Can be lower than bonds in some cases (e.g., CDs) | Subject to market fluctuations |

11. How Does the Yield Curve Affect Bond Investments?

The yield curve illustrates the relationship between bond yields and their time to maturity. Analyzing the yield curve can provide insights into the current economic environment and potential future interest rate movements, influencing investment strategies in bonds.

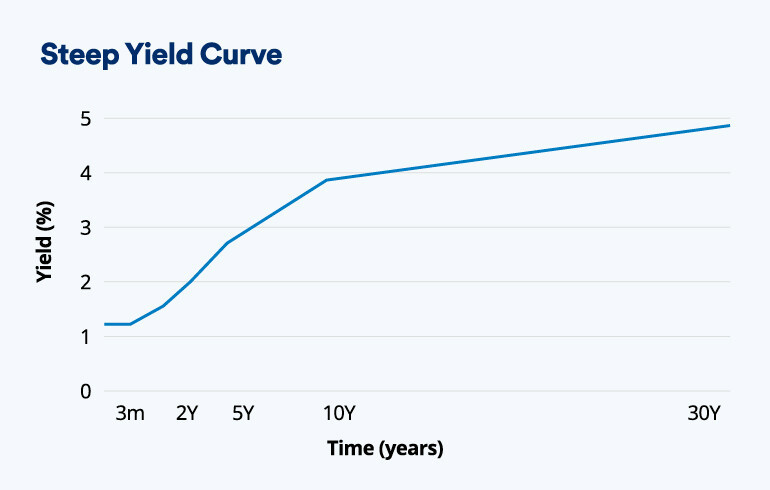

11.1 Understanding the Normal Yield Curve

A normal yield curve slopes upward, indicating that longer-term bonds offer higher yields than shorter-term bonds. This is typically associated with a healthy economy and expectations of future economic growth and inflation.

Normal Yield Curve Showing Upward Slope

Normal Yield Curve Showing Upward Slope

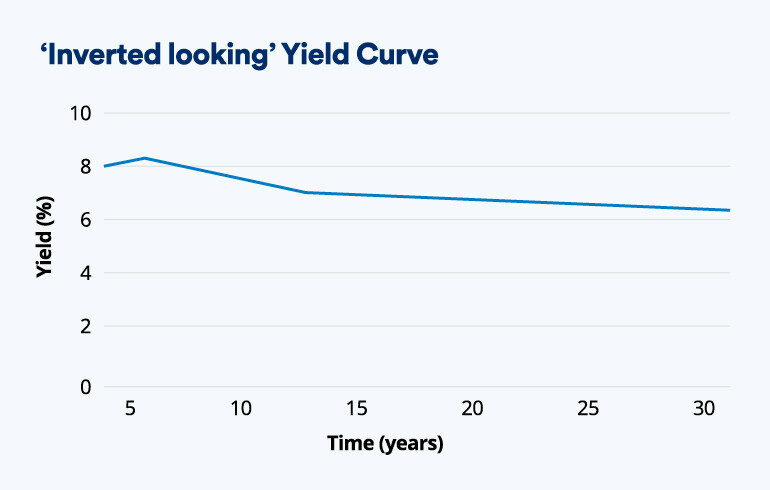

11.2 Interpreting the Inverted Yield Curve

An inverted yield curve occurs when short-term bonds have higher yields than long-term bonds. This is often seen as a warning sign of an impending economic recession, as it suggests that investors expect interest rates to decline in the future.

Inverted Yield Curve Showing Downward Slope

Inverted Yield Curve Showing Downward Slope

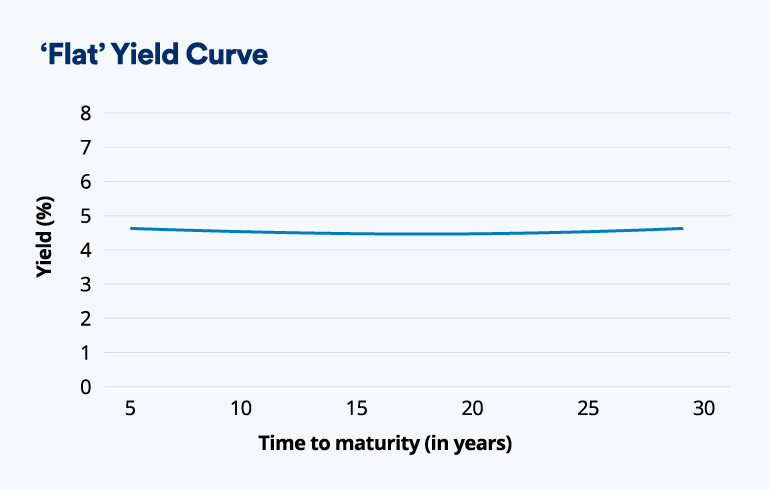

11.3 Analyzing the Flat Yield Curve

A flat yield curve indicates that the yields of bonds with different maturities are relatively constant. This can occur when there is uncertainty about the future direction of interest rates and economic growth.

Flat Yield Curve Showing Constant Yields

Flat Yield Curve Showing Constant Yields

12. How Do Credit Ratings Influence Bond Investment Decisions?

Credit ratings, assigned by agencies like Moody’s, Standard & Poor’s, and Fitch, assess the creditworthiness of bond issuers. These ratings play a critical role in helping investors evaluate the risk associated with different bond investments.

12.1 Understanding Investment-Grade Bonds

Investment-grade bonds are those with high credit ratings (e.g., AAA, AA, A, BBB), indicating a low risk of default. These bonds are typically favored by conservative investors seeking stable income and capital preservation.

12.2 Evaluating High-Yield Bonds

High-yield bonds, also known as junk bonds, have lower credit ratings (e.g., BB, B, CCC) and carry a higher risk of default. However, they offer higher yields to compensate for the increased risk. These bonds may be suitable for investors with a higher risk tolerance seeking potentially greater returns.

12.3 The Role of Credit Rating Agencies

Credit rating agencies provide independent assessments of the creditworthiness of bond issuers, helping investors make informed decisions. However, it’s important to note that credit ratings are not foolproof and should be used in conjunction with other research and analysis.

13. What is Bond Duration and Why Does it Matter?

Bond duration is a measure of a bond’s sensitivity to changes in interest rates. It estimates the percentage change in a bond’s price for a 1% change in interest rates. Understanding bond duration is essential for managing interest rate risk in a bond portfolio.

13.1 Calculating Bond Duration

Bond duration is calculated based on the bond’s maturity, coupon rate, and yield to maturity. Bonds with longer maturities and lower coupon rates tend to have higher durations, making them more sensitive to interest rate changes.

13.2 Interpreting Duration Values

For example, a bond with a duration of 5 years will experience an approximate 5% price change for every 1% change in interest rates. If interest rates rise by 1%, the bond’s price will fall by approximately 5%, and vice versa.

13.3 Using Duration for Risk Management

Investors can use bond duration to manage interest rate risk in their portfolios. By matching the duration of their bond portfolio to their investment time horizon, investors can minimize the impact of interest rate changes on their overall returns.

14. What are Inflation-Indexed Bonds (TIPS) and How Do They Work?

Inflation-indexed bonds, also known as Treasury Inflation-Protected Securities (TIPS) in the U.S., are designed to protect investors from the eroding effects of inflation. The principal of these bonds is adjusted based on changes in the Consumer Price Index (CPI), ensuring that investors maintain their purchasing power.

14.1 How TIPS Protect Against Inflation

TIPS adjust their principal value based on changes in the CPI. If inflation rises, the principal value of the TIPS increases, and vice versa. This helps investors maintain the real value of their investment and protect their purchasing power.

14.2 Benefits of Investing in TIPS

- Inflation Protection: TIPS provide protection against inflation, ensuring that investors maintain their purchasing power.

- Stable Returns: TIPS offer stable returns that are linked to inflation, making them a valuable addition to a diversified portfolio.

- Low Risk: TIPS are backed by the U.S. government, making them a low-risk investment.

14.3 Considerations When Investing in TIPS

- Tax Implications: The increase in principal value due to inflation is taxable, even though it is not received as cash.

- Real Yields: TIPS offer a real yield, which is the yield above inflation.

- Market Conditions: TIPS may underperform in periods of low inflation or deflation.

15. What are Zero-Coupon Bonds and How Do They Generate Returns?

Zero-coupon bonds are debt instruments that do not pay periodic interest payments. Instead, they are sold at a discount to their face value and mature at par. Investors earn a return based on the difference between the purchase price and the face value at maturity.

15.1 How Zero-Coupon Bonds Work

Zero-coupon bonds are purchased at a discount to their face value. The difference between the purchase price and the face value represents the investor’s return. At maturity, the investor receives the face value of the bond.

15.2 Benefits of Investing in Zero-Coupon Bonds

- Predictable Returns: Zero-coupon bonds offer predictable returns, as the investor knows the exact amount they will receive at maturity.

- Tax Advantages: In some cases, zero-coupon bonds may offer tax advantages, as the interest is not paid out until maturity.

- Ideal for Long-Term Goals: Zero-coupon bonds are often used for long-term goals, such as retirement planning or college savings.

15.3 Considerations When Investing in Zero-Coupon Bonds

- Interest Rate Risk: Zero-coupon bonds are highly sensitive to interest rate changes.

- Reinvestment Risk: Investors do not receive periodic interest payments to reinvest.

- Tax Implications: The accrued interest is taxable annually, even though it is not received as cash.

16. Fixed Income Strategies for Different Economic Conditions

Different economic conditions call for different fixed income strategies. Understanding how to adapt your fixed income investments to changing economic environments can help you maximize returns and manage risk.

16.1 Investing in a Rising Interest Rate Environment

When interest rates are rising, it’s generally best to shorten the duration of your bond portfolio. This can be achieved by investing in shorter-term bonds or bond funds with lower durations. You may also consider investing in floating-rate bonds, which adjust their coupon rates based on changes in interest rates.

16.2 Investing in a Falling Interest Rate Environment

When interest rates are falling, it’s generally best to lengthen the duration of your bond portfolio. This can be achieved by investing in longer-term bonds or bond funds with higher durations. You may also consider locking in current yields by investing in callable bonds.

16.3 Investing During Economic Uncertainty

During times of economic uncertainty, it’s generally best to focus on high-quality bonds with low credit risk. This can be achieved by investing in government bonds or investment-grade corporate bonds. You may also consider diversifying your fixed income portfolio across different sectors and maturities.

17. How Do Callable Bonds Impact Investment Returns?

Callable bonds give the issuer the right to redeem the bond before its stated maturity date, typically after a specified call date. This call feature can impact investment returns, as the issuer may choose to redeem the bond when interest rates fall, potentially forcing investors to reinvest at lower yields.

17.1 Understanding the Call Feature

The call feature gives the issuer the option to redeem the bond before maturity, usually at a predetermined price (the call price). Issuers typically call bonds when interest rates have fallen, allowing them to refinance their debt at a lower cost.

17.2 Impact on Investment Returns

- Reinvestment Risk: If a callable bond is called, investors may have to reinvest the proceeds at lower yields, reducing their overall returns.

- Yield Advantage: Callable bonds typically offer higher yields than non-callable bonds to compensate investors for the call risk.

- Price Appreciation: The price appreciation of callable bonds may be limited, as the issuer is likely to call the bond if its price rises significantly above the call price.

17.3 Considerations When Investing in Callable Bonds

- Call Protection: Look for bonds with longer call protection periods to reduce the risk of early redemption.

- Yield to Call: Evaluate the yield to call (YTC), which is the return an investor would receive if the bond is called at the earliest possible date.

- Interest Rate Outlook: Consider the outlook for interest rates, as callable bonds are more likely to be called when interest rates are falling.

18. What are Mortgage-Backed Securities (MBS) and How Do They Work?

Mortgage-backed securities (MBS) are a type of asset-backed security that is secured by a pool of mortgage loans. Investors in MBS receive payments from the underlying mortgage loans, including principal and interest.

18.1 How MBS are Structured

MBS are created when a financial institution, such as a bank or mortgage company, pools together a group of mortgage loans and sells them to investors. The investors receive payments from the underlying mortgage loans, including principal and interest.

18.2 Benefits of Investing in MBS

- Higher Yields: MBS typically offer higher yields than government bonds, as they carry additional risks, such as prepayment risk and credit risk.

- Diversification: MBS can diversify a fixed income portfolio and provide exposure to the housing market.

- Monthly Income: MBS provide a steady stream of monthly income from the underlying mortgage loans.

18.3 Risks of Investing in MBS

- Prepayment Risk: Prepayment risk is the risk that homeowners will repay their mortgages early, reducing the investor’s income and principal.

- Credit Risk: Credit risk is the risk that homeowners will default on their mortgages, resulting in losses for the investor.

- Interest Rate Risk: MBS are sensitive to interest rate changes, as rising interest rates can lead to lower demand for mortgages and lower MBS prices.

19. Understanding Bond Yield and its Different Measures

Bond yield is a measure of the return an investor receives from a bond. There are several different measures of bond yield, including coupon yield, current yield, and yield to maturity. Understanding these different measures is essential for comparing bonds and making informed investment decisions.

19.1 Coupon Yield

Coupon yield is the annual interest payment divided by the face value of the bond. It represents the fixed rate of interest that the bond pays.

19.2 Current Yield

Current yield is the annual interest payment divided by the current market price of the bond. It provides a more accurate measure of the current return on investment than coupon yield.

19.3 Yield to Maturity (YTM)

Yield to maturity (YTM) is the total return an investor can expect to receive if they hold the bond until maturity. It takes into account the coupon payments, the difference between the purchase price and the face value, and the time to maturity. YTM is the most comprehensive measure of bond yield.

20. Key Considerations Before Investing in Bonds

Before investing in bonds, it’s important to consider your investment goals, risk tolerance, and time horizon. It’s also important to conduct thorough research and analysis to select the right bonds and manage your portfolio effectively.

20.1 Assess Your Investment Goals

Determine your investment goals, such as income generation, capital preservation, or growth. Different types of bonds may be more suitable for different investment goals.

20.2 Evaluate Your Risk Tolerance

Assess your risk tolerance, as bonds vary in terms of credit risk, interest rate risk, and other factors. Choose bonds that align with your risk tolerance.

20.3 Consider Your Time Horizon

Consider your time horizon, as bonds with longer maturities are more sensitive to interest rate changes. Choose bonds with maturities that match your investment time horizon.

20.4 Conduct Thorough Research and Analysis

Conduct thorough research and analysis to select the right bonds and manage your portfolio effectively. Consider factors such as credit ratings, yield, duration, and call features.

University of Texas at Austin’s McCombs School of Business emphasizes the importance of understanding these fundamental concepts. According to research from the University of Texas at Austin’s McCombs School of Business, in July 2025, a diversified portfolio, including bonds, provides Y.

Understanding the differences between fixed income and bonds is essential for making informed investment decisions. Bonds are a type of fixed-income investment, but not all fixed-income investments are bonds. By understanding the characteristics, risks, and rewards of different types of bonds, you can build a well-diversified portfolio that meets your investment goals and risk tolerance.

Ready to explore the world of fixed income and bonds and find the right partners to help you succeed? Visit income-partners.net today to discover a wealth of resources, connect with strategic partners, and unlock your income potential. Don’t miss out on the opportunity to take control of your financial future and achieve your investment goals.

Address: 1 University Station, Austin, TX 78712, United States.

Phone: +1 (512) 471-3434.

Website: income-partners.net.

Frequently Asked Questions (FAQ)

1. Are fixed income investments always safe?

Not always. While generally less volatile than stocks, fixed income investments still carry risks like credit risk (the issuer defaulting) and interest rate risk (rising rates decreasing bond value).

2. What’s better, bonds or stocks?

It depends on your risk tolerance and investment goals. Bonds are generally safer and provide income, while stocks offer higher growth potential but with more volatility. A balanced portfolio includes both.

3. How do I choose the right bonds for my portfolio?

Consider your risk tolerance, investment goals, and time horizon. Research the issuer’s credit rating, the bond’s yield, and its maturity date.

4. What is a bond fund and how does it work?

A bond fund is a mutual fund that invests in a portfolio of bonds. It offers diversification and professional management but comes with fees and expenses.

5. What is the difference between a bond’s coupon rate and its yield?

The coupon rate is the fixed interest rate the bond pays on its face value. The yield is the actual return you receive, taking into account the bond’s current market price.

6. How do rising interest rates affect bond prices?

Rising interest rates generally cause bond prices to fall because newly issued bonds offer higher yields, making older bonds less attractive.

7. What are Treasury Inflation-Protected Securities (TIPS)?

TIPS are bonds whose principal is adjusted based on changes in the Consumer Price Index (CPI), protecting investors from inflation.

8. Are municipal bonds tax-exempt?

Yes, the interest income from municipal bonds is often exempt from federal, and sometimes state and local, taxes.

9. What is a callable bond?

A callable bond gives the issuer the right to redeem the bond before its maturity date, typically if interest rates fall.

10. Where can I find more information about fixed income and bonds?

income-partners.net offers a wealth of resources, expert insights, and strategic partnership opportunities to help you navigate the fixed-income landscape and achieve your financial goals.