Are Distributions From An Ira Considered Earned Income? Not necessarily, but understanding the nuances is crucial for your financial planning, particularly when it comes to Social Security benefits. At income-partners.net, we help you navigate these complexities to maximize your income and build strategic partnerships. By understanding these distinctions, you can optimize your income streams, explore strategic financial collaborations and unlock new avenues for wealth creation.

1. What Exactly Is Earned Income?

Earned income isn’t what you get from investments like an IRA; it’s the money you make from working. Earned income specifically refers to compensation received for providing labor or services. This can include:

- Salaries

- Wages

- Tips

- Bonuses

- Self-employment income (from a business where you actively participate)

According to the Social Security Administration (SSA), earned income is the primary factor in determining your eligibility for and the amount of Social Security benefits you can receive before reaching full retirement age.

1.1. Why Earned Income Matters

Earned income affects your Social Security benefits in two main ways:

- Eligibility Before Full Retirement Age: If you claim Social Security benefits before reaching your full retirement age, your benefits may be reduced if your earned income exceeds certain limits. This is known as the Social Security earnings test.

- Taxation of Benefits: Your combined income, which includes a portion of your Social Security benefits, adjusted gross income (AGI), and nontaxable interest, determines whether your Social Security benefits are subject to federal income tax.

Understanding these distinctions is essential for effective financial planning. Let’s delve into how IRA distributions fit into this picture.

2. How IRA Distributions Are Treated

IRA distributions are generally not considered earned income, but they do impact your overall financial picture differently depending on the type of IRA. To clarify, let’s look at the two main types of IRAs: Traditional IRAs and Roth IRAs.

2.1. Traditional IRA Distributions

- Not Earned Income: Distributions from a traditional IRA are not considered earned income under the Social Security earnings test. This means taking money out of your traditional IRA won’t directly reduce your Social Security benefits if you’re under full retirement age.

- Taxable Income: However, traditional IRA distributions are generally included in your adjusted gross income (AGI) and are subject to income tax. This can indirectly affect your Social Security benefits by increasing your combined income. If your combined income exceeds certain thresholds, a larger portion of your Social Security benefits could become taxable.

- Impact on Social Security Taxes: Because traditional IRA distributions increase your AGI, they can push you into a higher tax bracket, potentially leading to more of your Social Security benefits being taxed.

2.2. Roth IRA Distributions

- Not Earned Income: Like traditional IRA distributions, Roth IRA distributions are not considered earned income for the Social Security earnings test.

- Tax-Free Income: The key difference with Roth IRAs is that qualified distributions are tax-free and are not included in your AGI. This means Roth IRA distributions do not increase your combined income and will not cause your Social Security benefits to be taxed.

The table below summarizes the key differences:

| Feature | Traditional IRA Distributions | Roth IRA Distributions |

|---|---|---|

| Considered Earned Income | No | No |

| Included in AGI | Yes | No |

| Affects Social Security Tax | Yes, potentially | No |

3. Understanding the Social Security Earnings Test

The Social Security earnings test is a crucial factor for those considering claiming benefits before their full retirement age. Let’s break down how it works and how IRA distributions fit in.

3.1. How the Earnings Test Works

If you claim Social Security benefits before reaching your full retirement age, the Social Security Administration (SSA) may reduce your benefits if your earned income exceeds certain limits. In 2024, the earnings limit is $22,320. If you earn more than this amount, $1 in benefits will be withheld for every $2 you earn above the limit. In the year you reach your full retirement age, a different, higher limit applies.

According to the SSA, the earnings test only considers earned income. As mentioned earlier, this includes wages, salaries, self-employment income, and other forms of compensation for work. It does not include investment income, pensions, annuities, or IRA distributions.

3.2. The Impact of IRA Distributions on the Earnings Test

Since IRA distributions are not considered earned income, they do not directly affect the Social Security earnings test. This means you can withdraw money from your IRA without worrying about it reducing your Social Security benefits, as long as you are under the earnings limit for earned income.

For example, if you are 63 years old and claiming Social Security benefits, you can withdraw funds from your IRA to supplement your income without impacting your Social Security benefits, provided that your earned income remains below the annual limit.

3.3. Key Considerations

- Full Retirement Age: Once you reach your full retirement age (67 for those born in 1960 or later), the earnings test no longer applies. You can earn as much as you want without any reduction in your Social Security benefits.

- Year of Retirement: There’s a special rule for the year you reach full retirement age. The earnings limit is higher, and the reduction in benefits is less severe. This provides some flexibility as you transition into retirement.

4. Tax Implications of IRA Distributions on Social Security

While IRA distributions don’t directly affect the Social Security earnings test, they can impact the taxation of your Social Security benefits. Here’s how.

4.1. Calculating Combined Income

The IRS uses a formula to determine whether your Social Security benefits are taxable. This formula involves calculating your combined income, which includes:

- Adjusted Gross Income (AGI): This includes income from various sources, such as wages, salaries, interest, dividends, and traditional IRA distributions.

- Nontaxable Interest: This includes interest from municipal bonds and other tax-exempt investments.

- Half of Your Social Security Benefits: This is added to your AGI and nontaxable interest to arrive at your combined income.

4.2. Taxation Thresholds

The amount of your Social Security benefits that may be taxable depends on your combined income. Here are the general guidelines:

- Single, Head of Household, or Qualifying Widow(er):

- Combined income between $25,000 and $34,000: Up to 50% of your benefits may be taxable.

- Combined income above $34,000: Up to 85% of your benefits may be taxable.

- Married Filing Jointly:

- Combined income between $32,000 and $44,000: Up to 50% of your benefits may be taxable.

- Combined income above $44,000: Up to 85% of your benefits may be taxable.

- Married Filing Separately:

- If you lived with your spouse at any time during the year, 85% of your benefits may be taxable.

4.3. Examples of How IRA Distributions Affect Taxation

Let’s look at a couple of examples to illustrate how IRA distributions can impact the taxation of Social Security benefits:

Example 1: Traditional IRA Distribution

- Sarah is single and receives $20,000 in Social Security benefits.

- Her AGI (including a $10,000 traditional IRA distribution) is $30,000.

- Her combined income is $30,000 (AGI) + $0 (nontaxable interest) + $10,000 (half of Social Security benefits) = $40,000.

- Since her combined income is above $34,000, up to 85% of her Social Security benefits may be taxable.

Example 2: Roth IRA Distribution

- John is single and receives $20,000 in Social Security benefits.

- His AGI (excluding a $10,000 Roth IRA distribution) is $30,000.

- His combined income is $30,000 (AGI) + $0 (nontaxable interest) + $10,000 (half of Social Security benefits) = $40,000.

- Since his combined income is above $34,000, up to 85% of his Social Security benefits may be taxable.

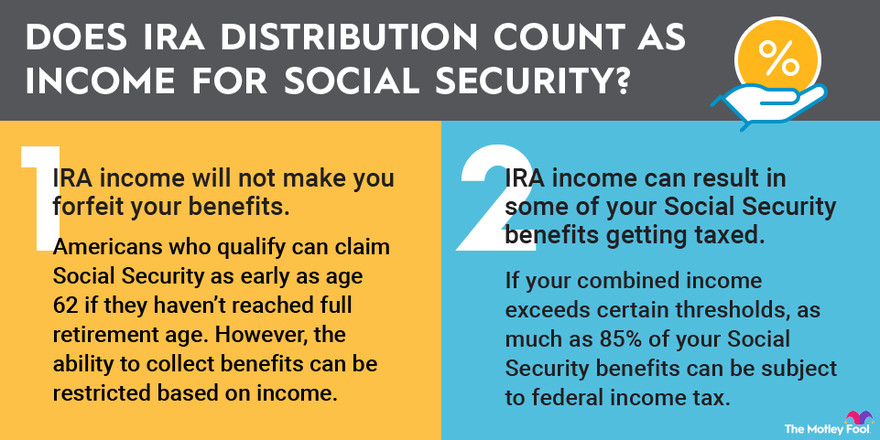

An infographic explaining whether IRA distributions count as income for Social Security and their impact on Social Security taxes, showing the distinction between traditional and Roth IRAs

An infographic explaining whether IRA distributions count as income for Social Security and their impact on Social Security taxes, showing the distinction between traditional and Roth IRAs

5. Strategic Planning: Optimizing IRA Distributions and Social Security

Given the complexities of how IRA distributions and Social Security benefits interact, strategic planning is essential to maximize your financial well-being. Here are some tips to help you optimize your approach:

5.1. Consider a Roth Conversion

Converting a traditional IRA to a Roth IRA can be a powerful strategy to reduce your future tax liabilities. While you’ll pay taxes on the converted amount in the year of the conversion, future distributions from the Roth IRA will be tax-free. This can be particularly beneficial if you anticipate being in a higher tax bracket in retirement.

5.2. Manage Your AGI

Be mindful of how your IRA distributions impact your AGI. If possible, try to keep your AGI below the thresholds that trigger higher taxation of Social Security benefits. This might involve spreading out your IRA distributions over multiple years or using other strategies to reduce your taxable income.

5.3. Coordinate with Other Income Sources

Consider how your IRA distributions fit into your overall income picture. If you have other sources of income, such as pensions, annuities, or investment income, coordinate your withdrawals to minimize your tax liability.

5.4. Seek Professional Advice

Given the complexities of tax law and financial planning, it’s often wise to seek professional advice from a qualified financial advisor or tax professional. They can help you develop a personalized strategy that takes into account your individual circumstances and goals.

5.5. Understand State Taxes

While we’ve focused on federal taxes, keep in mind that some states also tax Social Security benefits. Be sure to understand the tax laws in your state and how they might impact your retirement income.

6. Navigating Retirement Income Taxation

Retirement income taxation can seem like a complex maze, but understanding the basics can empower you to make informed decisions and optimize your financial strategy.

6.1. Types of Retirement Income

Retirement income can come from a variety of sources, each with its own tax implications:

- Social Security Benefits: As we’ve discussed, a portion of your Social Security benefits may be taxable, depending on your combined income.

- IRA Distributions: Traditional IRA distributions are generally taxable, while Roth IRA distributions are tax-free if certain conditions are met.

- Pension Income: Pension income is typically taxable as ordinary income.

- Annuities: The taxation of annuities can be complex, depending on whether they are qualified or non-qualified.

- Investment Income: Investment income, such as interest, dividends, and capital gains, is generally taxable.

6.2. Tax-Advantaged Accounts

Tax-advantaged accounts, such as IRAs and 401(k)s, can play a crucial role in managing your retirement income and minimizing your tax liability.

- Traditional IRAs and 401(k)s: Contributions to these accounts are typically tax-deductible, and earnings grow tax-deferred. However, distributions are generally taxable as ordinary income.

- Roth IRAs and 401(k)s: Contributions to these accounts are not tax-deductible, but earnings grow tax-free, and qualified distributions are also tax-free.

6.3. Tax Planning Strategies

Effective tax planning is essential to maximize your retirement income and minimize your tax burden. Here are some strategies to consider:

- Tax Diversification: Diversify your retirement savings across different types of accounts, including taxable, tax-deferred, and tax-free accounts. This can provide flexibility in managing your tax liability in retirement.

- Tax-Loss Harvesting: Use tax-loss harvesting to offset capital gains with capital losses. This can help reduce your overall tax bill.

- Charitable Giving: Consider making charitable donations from your IRA to reduce your taxable income.

- Qualified Charitable Distributions (QCDs): If you are age 70 1/2 or older, you can donate up to $100,000 per year from your IRA directly to a qualified charity. This can satisfy your required minimum distribution (RMD) and reduce your taxable income.

6.4. Required Minimum Distributions (RMDs)

Once you reach age 73, you are generally required to start taking required minimum distributions (RMDs) from your traditional IRAs and 401(k)s. The amount of your RMD is based on your account balance and your life expectancy. Failure to take your RMD can result in a significant tax penalty.

Understanding RMDs and how they impact your tax liability is crucial for effective retirement planning.

7. Partnering for Success with Income-Partners.Net

At income-partners.net, we understand the challenges and opportunities that come with navigating the complex world of retirement income, Social Security, and strategic financial planning. Our mission is to empower you with the knowledge, resources, and partnerships you need to achieve your financial goals.

7.1. Identifying Potential Partners

Finding the right partners can be a game-changer for your business. At income-partners.net, we help you identify potential partners who align with your goals and values.

- Strategic Alliances: Collaborate with businesses that complement your offerings.

- Joint Ventures: Partner with companies to create new products or services.

- Referral Partnerships: Build relationships with businesses that can refer clients to you.

7.2. Building Strong Relationships

Once you’ve identified potential partners, building strong relationships is key.

- Clear Communication: Establish open and honest communication channels.

- Mutual Benefits: Ensure that the partnership is mutually beneficial.

- Shared Goals: Align on common goals and objectives.

7.3. Leveraging Partnership Opportunities

Successful partnerships can lead to increased revenue and market share.

- Cross-Promotions: Promote each other’s products or services.

- Co-Branding: Create co-branded products or services.

- Joint Marketing Campaigns: Launch joint marketing campaigns to reach new audiences.

7.4. Success Stories

We’ve seen firsthand how strategic partnerships can drive success. For example, one of our clients, a financial planning firm, partnered with a local accounting firm to offer comprehensive financial services to their clients. This partnership resulted in a 30% increase in revenue for both firms.

Another client, a real estate investment company, partnered with a property management firm to streamline their operations. This partnership allowed them to focus on acquiring new properties while the property management firm handled the day-to-day management tasks.

These are just a few examples of how strategic partnerships can lead to increased revenue, efficiency, and growth.

Address: 1 University Station, Austin, TX 78712, United States

Phone: +1 (512) 471-3434

Website: income-partners.net.

8. Future Trends in Partnership and Income Generation

The landscape of partnership and income generation is constantly evolving. Staying ahead of the curve requires an understanding of emerging trends and a willingness to adapt.

8.1. The Rise of Digital Partnerships

With the increasing importance of online channels, digital partnerships are becoming more prevalent.

- Affiliate Marketing: Partner with bloggers and influencers to promote your products or services.

- Content Partnerships: Collaborate with other businesses to create valuable content for your audience.

- Social Media Partnerships: Partner with other businesses to run joint social media campaigns.

8.2. The Importance of Data-Driven Partnerships

Data is playing an increasingly important role in partnership strategy.

- Data Sharing: Share data with your partners to gain insights into customer behavior.

- Analytics: Use analytics to track the performance of your partnerships and identify areas for improvement.

- Personalization: Personalize your partnership offerings based on customer data.

8.3. The Growth of Purpose-Driven Partnerships

Consumers are increasingly drawn to businesses that have a strong sense of purpose.

- Social Impact Partnerships: Partner with non-profit organizations to support social causes.

- Environmental Partnerships: Partner with businesses that are committed to sustainability.

- Ethical Partnerships: Partner with businesses that have a strong ethical code of conduct.

8.4. The Role of Technology

Technology is transforming the way businesses form and manage partnerships.

- Partnership Platforms: Use partnership platforms to find and connect with potential partners.

- Automation: Automate partnership processes such as onboarding, tracking, and reporting.

- AI: Use AI to identify potential partnership opportunities and personalize partnership offerings.

9. Conclusion: Seize Your Financial Future Today

Understanding the intricacies of IRA distributions and their impact on Social Security is paramount for strategic retirement planning. Remember, distributions from traditional IRAs are not considered earned income but can affect the taxation of your Social Security benefits. Roth IRA distributions, on the other hand, offer tax-free income that doesn’t impact your Social Security taxation.

By partnering with income-partners.net, you gain access to a wealth of knowledge, resources, and opportunities to optimize your income and achieve your financial goals. Whether you’re looking to identify potential partners, build strong relationships, or leverage partnership opportunities, we’re here to help you every step of the way.

Don’t wait to take control of your financial future. Visit income-partners.net today to explore our services, connect with potential partners, and start building a brighter financial future. Take the first step towards financial success by exploring opportunities that strategically align with your goals. Discover, connect, and thrive with income-partners.net.

10. Frequently Asked Questions (FAQ)

10.1. Do withdrawals from my IRA affect Social Security benefits?

If you withdraw money from a traditional IRA, it won’t affect your ability to claim and collect Social Security benefits. However, a traditional IRA distribution is considered taxable income, so it can result in some of your Social Security benefits being subject to income tax.

10.2. Is withdrawal from an IRA considered earned income?

IRA withdrawals can be considered taxable income, but they are not considered earned income. Earned income is money you receive from a job, as an independent contractor for work you perform, or from a business you actively participate in.

10.3. What income counts toward Social Security earnings limit?

The Social Security earnings test considers only earned income, which includes salary, wages, tips, bonuses or other compensation from a job, money paid to you as an independent contractor for work you perform, or money you earn from a business you actively participate in.

10.4. Do IRA withdrawals count as income for Medicare?

Yes, traditional IRA withdrawals typically count as income for the purpose of calculating Medicare premiums. If your income is greater than a certain level, your Medicare Part B or Part D premiums can be higher.

10.5. What income does not count against Social Security?

Roth IRA distributions have no effect on Social Security benefits, including the earnings test or taxation of benefits. Any unearned income, such as interest or dividends, doesn’t affect your ability to collect Social Security, but it can make more of your benefits taxable.

10.6. How can I minimize the impact of IRA distributions on my Social Security benefits?

Consider converting to a Roth IRA, managing your adjusted gross income (AGI), coordinating with other income sources, and seeking professional advice.

10.7. What is the Social Security earnings test?

The Social Security earnings test is a rule that reduces your Social Security benefits if you claim them before your full retirement age and your earned income exceeds certain limits.

10.8. What is combined income and how does it affect my Social Security benefits?

Combined income is your adjusted gross income (AGI) plus nontaxable interest plus one-half of your Social Security benefits. It is used to determine whether your Social Security benefits are taxable.

10.9. What are Required Minimum Distributions (RMDs)?

Required Minimum Distributions (RMDs) are the minimum amounts you must withdraw from your retirement accounts each year, starting at age 73.

10.10. Where can I find more information about strategic partnerships and income generation?

Visit income-partners.net for a wealth of knowledge, resources, and opportunities to optimize your income and achieve your financial goals through strategic partnerships.