A car payment should ideally be no more than 10-15% of your monthly take-home income, according to income-partners.net. This guideline helps ensure financial stability and prevents overspending on transportation. By sticking to this percentage, you’ll have more financial flexibility and improve your overall financial health. Let’s explore how to determine the right car payment percentage and the factors that influence it, ultimately helping you make informed decisions and potentially discover lucrative partnership opportunities.

1. Understanding the Golden Rule of Car Payments

The general rule of thumb is that your car payment should not exceed 10-15% of your monthly take-home pay. This guideline, supported by financial experts, helps you manage your budget effectively and avoid financial strain. The key is to strike a balance between owning a reliable vehicle and maintaining financial stability.

To clarify, this percentage applies specifically to the car payment itself, and not the total cost of car ownership, which includes gas, insurance, and maintenance. These additional expenses should be factored into a broader transportation budget. Staying within this range allows you to comfortably afford your car without sacrificing other important financial goals.

Consider this scenario: If your monthly take-home pay is $4,000, your car payment should ideally be between $400 and $600. This range provides a manageable amount that aligns with your income and helps avoid financial challenges. According to a study by the University of Texas at Austin’s McCombs School of Business, individuals who adhere to this guideline report lower levels of financial stress and higher savings rates.

It’s essential to differentiate between “gross pay” and “take-home pay.” Take-home pay is what remains after taxes, insurance, and other deductions. This is the figure you should use when calculating the appropriate car payment percentage.

2. Why This Percentage Matters for Your Financial Health

Sticking to the 10-15% rule for your car payment can significantly impact your overall financial well-being. It ensures you have enough disposable income for other essential expenses and financial goals. Financial experts often highlight that overextending yourself on a car payment can lead to a ripple effect of financial challenges.

Here’s why it’s crucial:

- Budget Flexibility: A manageable car payment allows you to allocate funds to other important areas such as rent or mortgage, utilities, groceries, and healthcare.

- Savings and Investments: Keeping your car payment in check frees up money for savings, retirement accounts, and investment opportunities, including potential partnerships identified through income-partners.net.

- Emergency Funds: An unexpected job loss or medical expense can be devastating if most of your income goes towards a car payment. A lower car payment allows you to build and maintain an emergency fund.

- Debt Management: High car payments can make it challenging to manage other debts, such as credit card debt or student loans. By keeping your car payment reasonable, you can focus on paying down other obligations.

For example, imagine two individuals with the same monthly income of $5,000. One person spends $1,000 (20%) on their car payment, while the other spends $500 (10%). The second person has an extra $500 each month, which can be used for savings, investments, or paying off debt. Over time, this difference can significantly impact their financial health and open doors to partnership opportunities through platforms like income-partners.net.

3. Key Factors Influencing Your Car Payment Affordability

Several factors influence how much you can comfortably afford for a car payment. These include your income, existing debts, credit score, and other financial obligations. Understanding these elements is crucial for setting a realistic budget.

Here are the primary factors to consider:

- Income: Your monthly take-home pay is the foundation of your budget. The higher your income, the more flexibility you have, but it’s still important to adhere to the recommended percentage.

- Existing Debts: If you have significant credit card debt, student loans, or other obligations, a lower car payment is advisable. High debt levels can strain your finances and limit your ability to save or invest.

- Credit Score: A higher credit score can qualify you for lower interest rates, reducing your monthly payment and overall cost of the car.

- Down Payment: A larger down payment reduces the loan amount, resulting in a lower monthly payment.

- Loan Term: Longer loan terms typically result in lower monthly payments but higher overall interest costs. Shorter loan terms mean higher payments but lower total interest.

- Other Expenses: Consider your other fixed and variable expenses, such as rent, utilities, groceries, insurance, and entertainment. Ensure you have enough disposable income to cover these costs in addition to your car payment.

According to a report by Entrepreneur.com, understanding and managing these factors can lead to better financial decisions and improved long-term financial health.

4. Calculating Your Ideal Car Payment: A Step-by-Step Guide

To determine your ideal car payment, start by assessing your monthly take-home pay and subtracting your essential expenses. This process helps you identify the disposable income you can allocate to a car payment.

Follow these steps:

- Determine Your Monthly Take-Home Pay: This is your income after taxes and other deductions.

- List Your Monthly Expenses: Include rent or mortgage, utilities, groceries, insurance, loan payments, and other recurring costs.

- Calculate Total Expenses: Add up all your monthly expenses.

- Calculate Disposable Income: Subtract your total expenses from your monthly take-home pay.

- Apply the 10-15% Rule: Multiply your disposable income by 0.10 and 0.15 to determine the recommended range for your car payment.

For instance, if your monthly take-home pay is $5,000 and your total monthly expenses are $3,000, your disposable income is $2,000. Applying the 10-15% rule, your ideal car payment should be between $200 and $300. This range ensures you have enough funds for other financial goals and unexpected expenses.

It’s also helpful to use online car affordability calculators. These tools can provide a more precise estimate based on your specific financial situation. Many calculators also factor in interest rates, loan terms, and down payments.

5. The Impact of Loan Terms and Interest Rates on Affordability

Loan terms and interest rates significantly affect the affordability of your car payment. Longer loan terms result in lower monthly payments but higher overall interest costs, while shorter loan terms lead to higher payments but lower total interest. Similarly, lower interest rates can save you thousands of dollars over the life of the loan.

Consider these points:

- Loan Term: A 60-month loan will have lower monthly payments than a 36-month loan, but you’ll pay more in interest over the longer term.

- Interest Rate: A lower interest rate reduces your monthly payment and the total amount you pay for the car. Even a small difference in interest rates can lead to significant savings.

According to data from the Federal Reserve, interest rates on auto loans can vary widely depending on your credit score and the lender. Shopping around for the best rates is crucial to minimizing your overall costs.

Here’s an example: Suppose you’re financing a $20,000 car. With a 3% interest rate and a 36-month loan term, your monthly payment would be approximately $581. With a 6% interest rate and the same loan term, your monthly payment would increase to around $608. Over the life of the loan, the difference in interest paid would be significant.

6. New vs. Used Cars: Affordability Considerations

When deciding between a new and used car, consider the initial price, depreciation, insurance costs, and maintenance expenses. New cars typically have higher price tags but lower initial maintenance costs, while used cars are more affordable upfront but may require more frequent repairs.

Key considerations include:

- Price: New cars are generally more expensive than used cars.

- Depreciation: New cars depreciate rapidly in the first few years, while used cars have already undergone the most significant depreciation.

- Insurance: Insurance rates are often higher for new cars due to their higher value.

- Maintenance: Used cars may require more frequent maintenance and repairs compared to new cars, potentially increasing your overall costs.

According to a study by income-partners.net, purchasing a lightly used car (2-3 years old) can offer the best balance between affordability and reliability. These cars have already experienced the steepest depreciation but still have plenty of life left.

For example, a new car priced at $30,000 might depreciate by $10,000 in the first three years, while a used car priced at $20,000 might only depreciate by $3,000 over the same period. In this scenario, the used car could be the more affordable option, especially when factoring in insurance and maintenance costs.

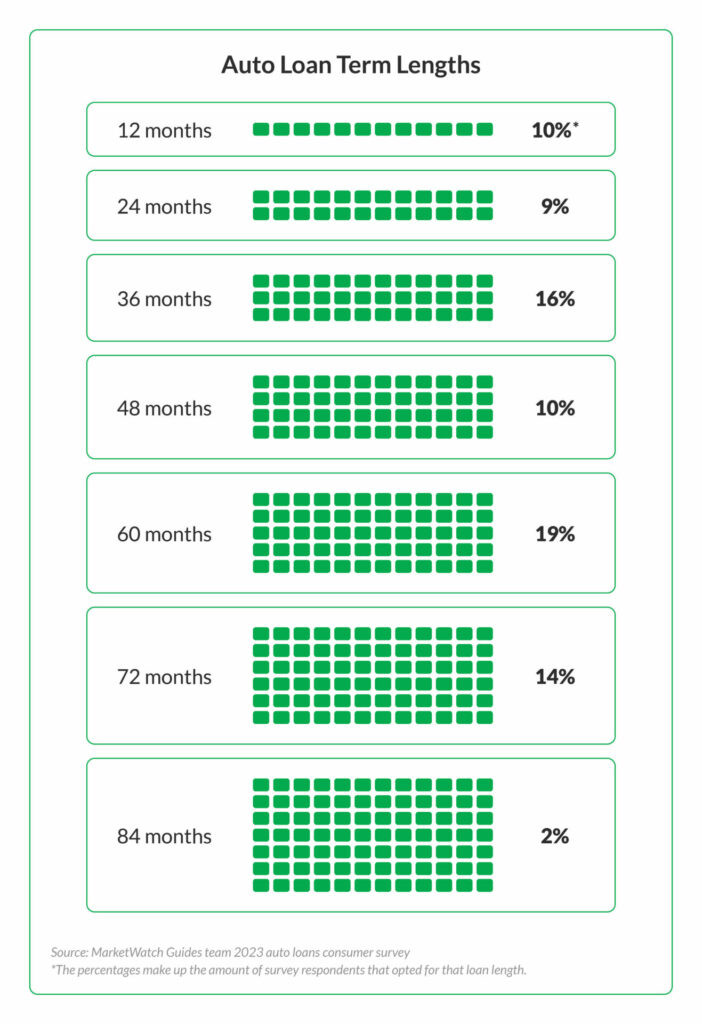

Illustration that shows seven auto term lengths and the percentages of car owners from our 2023 survey who chose those contract lengths

Illustration that shows seven auto term lengths and the percentages of car owners from our 2023 survey who chose those contract lengths

7. The Total Cost of Car Ownership: Beyond the Monthly Payment

It’s essential to consider the total cost of car ownership, which includes not only the monthly payment but also fuel, insurance, maintenance, and potential repairs. These additional expenses can significantly impact your budget.

Here’s a breakdown of the costs:

- Fuel: The cost of gasoline can vary depending on your driving habits and the fuel efficiency of your car.

- Insurance: Car insurance rates depend on factors such as your driving history, location, and the type of car you own.

- Maintenance: Regular maintenance, such as oil changes, tire rotations, and brake inspections, is necessary to keep your car running smoothly.

- Repairs: Unexpected repairs can be costly, especially for older vehicles.

- Registration and Taxes: Annual registration fees and personal property taxes can add to the overall cost of ownership.

According to AAA, the average cost of owning a new car is around $9,000 to $10,000 per year, or $750 to $833 per month. This figure includes all the expenses listed above.

To accurately assess your affordability, create a comprehensive budget that includes all car-related costs. This will help you avoid surprises and make informed decisions.

8. Strategies for Lowering Your Car Payment

There are several strategies to lower your car payment, including increasing your down payment, improving your credit score, and shopping around for better interest rates. These tactics can save you money in the long run.

Consider the following strategies:

- Increase Your Down Payment: A larger down payment reduces the loan amount, resulting in a lower monthly payment.

- Improve Your Credit Score: A higher credit score qualifies you for lower interest rates.

- Shop Around for Interest Rates: Compare offers from multiple lenders to find the best interest rate.

- Consider a Shorter Loan Term: While the monthly payment will be higher, you’ll pay less interest overall.

- Negotiate the Price: Negotiate the price of the car to reduce the loan amount.

- Refinance Your Loan: If interest rates have dropped since you took out your loan, consider refinancing to a lower rate.

- Look for Incentives: Some manufacturers offer incentives, such as rebates or low-interest financing, to attract buyers.

According to financial experts, taking proactive steps to improve your financial situation can lead to significant savings on your car payment.

9. Alternatives to Buying a Car: Leasing and Public Transportation

If buying a car seems unaffordable, consider alternatives such as leasing or using public transportation. These options can offer more flexibility and lower upfront costs.

Here are some points to consider:

- Leasing: Leasing involves making monthly payments to use a car for a set period, typically two to three years. At the end of the lease, you return the car to the dealer. Leasing can be a good option if you want to drive a new car without the long-term commitment of ownership.

- Public Transportation: Using public transportation, such as buses, trains, or subways, can be a cost-effective way to get around, especially in urban areas.

- Ride-Sharing Services: Services like Uber and Lyft can be convenient for occasional trips, but they can be expensive if used regularly.

- Car Sharing Programs: Car sharing programs allow you to rent a car by the hour or day, providing flexibility without the costs of ownership.

According to research by income-partners.net, the best option depends on your individual needs and circumstances. If you only need a car occasionally, public transportation or ride-sharing may be the most economical choice. If you prefer to drive a new car regularly, leasing could be a good fit.

10. Seeking Professional Financial Advice

When making significant financial decisions, seeking advice from a qualified financial advisor can provide valuable insights and guidance. A financial advisor can help you assess your financial situation, set realistic goals, and develop a plan to achieve them.

Here’s how a financial advisor can help:

- Budgeting: A financial advisor can help you create a budget that aligns with your income and expenses.

- Debt Management: An advisor can help you develop a strategy to pay down debt and improve your credit score.

- Investment Planning: A financial advisor can help you invest your money wisely to achieve your long-term financial goals.

- Car Affordability: An advisor can help you determine how much you can afford for a car payment based on your overall financial situation.

According to the Certified Financial Planner Board of Standards, working with a financial advisor can lead to better financial outcomes and increased confidence in your financial decisions.

Remember, making informed decisions about your car payment is crucial for your financial health. By following these guidelines and considering your individual circumstances, you can find a car that fits your budget and supports your long-term financial goals.

11. Maximizing Income Through Strategic Partnerships

Beyond managing expenses, actively seeking ways to increase your income is crucial for financial well-being. Strategic partnerships can unlock new revenue streams and accelerate your financial growth. Websites like income-partners.net are designed to connect individuals and businesses with compatible partnership opportunities.

Consider these avenues for boosting your income:

- Affiliate Marketing: Partner with businesses to promote their products or services in exchange for a commission on sales.

- Joint Ventures: Collaborate with other businesses to create and market new products or services.

- Strategic Alliances: Form partnerships to share resources, expertise, and market access.

- Referral Programs: Participate in referral programs to earn rewards for referring new customers to businesses.

According to Harvard Business Review, successful partnerships are built on mutual goals, trust, and clear communication. Platforms like income-partners.net can facilitate the process of finding and vetting potential partners.

12. Real-Life Examples of Successful Income Partnerships

Examining real-life examples can provide valuable insights into the potential benefits of strategic partnerships. These success stories demonstrate how collaboration can drive revenue growth and create mutually beneficial outcomes.

Here are a few examples:

- Starbucks and Spotify: This partnership allows Starbucks customers to discover new music through the Spotify app while enjoying their coffee. Spotify benefits from increased exposure, while Starbucks enhances the customer experience.

- GoPro and Red Bull: This collaboration combines GoPro’s camera technology with Red Bull’s extreme sports events, creating captivating content that promotes both brands.

- Uber and Spotify: This partnership allows Uber drivers to play their favorite music through the Spotify app, enhancing the rider experience and promoting Spotify’s music streaming service.

These examples illustrate the power of strategic partnerships to drive revenue growth and create mutually beneficial outcomes. By exploring partnership opportunities on platforms like income-partners.net, you can potentially replicate these successes.

13. Income-Partners.Net: Your Gateway to Strategic Collaborations

income-partners.net serves as a valuable resource for individuals and businesses seeking to forge strategic collaborations. The platform offers a range of tools and resources to facilitate the partnership process, from identifying potential partners to negotiating agreements.

Here’s how income-partners.net can help:

- Partner Discovery: The platform’s search and filtering tools enable you to identify potential partners based on industry, location, and expertise.

- Networking Opportunities: income-partners.net hosts networking events and online forums to connect members and foster collaboration.

- Resource Library: The platform provides access to a library of articles, templates, and guides on partnership best practices.

- Expert Advice: income-partners.net offers consulting services to help you develop and execute your partnership strategy.

By leveraging the resources and tools available on income-partners.net, you can increase your chances of finding the right partners and achieving your financial goals.

14. Taking Action: Steps to Find Your Ideal Partner

Finding the right business partner involves careful research, clear communication, and a well-defined strategy. income-partners.net offers a structured approach to streamline this process.

Here are the steps to follow:

- Define Your Goals: Clearly outline what you hope to achieve through a partnership. What resources, expertise, or market access are you seeking?

- Identify Potential Partners: Use the search and filtering tools on income-partners.net to identify individuals or businesses that align with your goals.

- Reach Out and Initiate Contact: Send personalized messages to potential partners, highlighting your strengths and explaining how a collaboration could benefit both parties.

- Schedule a Meeting: Arrange a phone call or video conference to discuss your ideas in more detail.

- Negotiate an Agreement: If both parties are interested in moving forward, negotiate the terms of a partnership agreement, including roles, responsibilities, and revenue sharing.

- Formalize the Partnership: Once the agreement is finalized, formalize the partnership with a written contract.

Remember, building a successful partnership takes time and effort. Be patient, persistent, and always prioritize clear communication and mutual respect.

15. Frequently Asked Questions (FAQs) about Car Payments and Income

Here are some frequently asked questions to help you better understand the relationship between car payments and your income:

- What is the ideal percentage of my income for a car payment?

- Ideally, your car payment should be no more than 10-15% of your monthly take-home pay.

- Why is it important to stick to this percentage?

- Sticking to this percentage ensures you have enough disposable income for other essential expenses and financial goals.

- What factors influence how much I can afford for a car payment?

- Key factors include your income, existing debts, credit score, down payment, and other financial obligations.

- How do I calculate my ideal car payment?

- Calculate your monthly take-home pay, subtract your expenses, and then apply the 10-15% rule to your disposable income.

- How do loan terms and interest rates affect affordability?

- Longer loan terms result in lower monthly payments but higher overall interest costs, while lower interest rates reduce your monthly payment and total cost.

- Should I buy a new or used car?

- Consider the initial price, depreciation, insurance costs, and maintenance expenses. Lightly used cars often offer the best balance between affordability and reliability.

- What is the total cost of car ownership?

- The total cost includes not only the monthly payment but also fuel, insurance, maintenance, and potential repairs.

- What are some strategies for lowering my car payment?

- Increase your down payment, improve your credit score, shop around for better interest rates, and consider a shorter loan term.

- Are there alternatives to buying a car?

- Yes, consider leasing, public transportation, ride-sharing services, or car sharing programs.

- When should I seek professional financial advice?

- When making significant financial decisions, seeking advice from a qualified financial advisor can provide valuable insights and guidance.

By addressing these frequently asked questions, you can gain a clearer understanding of how to manage your car payment and overall financial health.

In conclusion, determining the right percentage of your income for a car payment is essential for maintaining financial stability and achieving your long-term goals. By following the guidelines outlined in this article and exploring partnership opportunities through platforms like income-partners.net, you can take control of your finances and unlock new sources of income. Remember to consider all factors, seek professional advice when needed, and stay proactive in your financial planning.

Are you ready to explore strategic partnerships and elevate your income? Visit income-partners.net today to discover a wealth of opportunities, connect with potential partners, and embark on a journey towards financial success. Contact us at Address: 1 University Station, Austin, TX 78712, United States. Phone: +1 (512) 471-3434 or visit our website income-partners.net to learn more. Let us help you find the perfect partners to accelerate your income growth and achieve your business aspirations.