Welcome to the latest analysis from income-partners.net, focusing on the evolving landscape of financial technology.

In today’s digital age, the financial world is rapidly transforming, and at the forefront of this revolution is Plaid, an API-first technology company. Plaid is instrumental in forging connections that are shaping the future of finance, particularly within the burgeoning realm of blockchain and Web3 technologies.

alt: Animated graphic illustrating digital connections, symbolizing Plaid’s role in financial technology, keyword rich alt text for Plaid Blockchain Partners.

Plaid: The Cornerstone of Fintech Connections

Often described as the “plumbing” of the financial ecosystem, Plaid facilitates secure connections between consumer bank accounts and a vast array of financial applications. Millions worldwide, potentially including you, rely on Plaid to seamlessly link their accounts to popular apps like Venmo, Robinhood, and Coinbase. This seamless connectivity is powered by Plaid’s robust API, enabling thousands of partners to efficiently serve their customers without the burden of developing complex connection solutions in-house.

Founded in 2013 by Zach Perret and William Hockey, Plaid has ascended to become the 8th most valuable API-first company globally, boasting a valuation of $13.4 billion. Its platform underpins over 12,000 financial institutions and empowers more than 6,000 Fintech enterprises, ranging from buy-now-pay-later services like Affirm to personal finance management tools like Rocket Money.

Plaid’s journey, marked by a near acquisition by Visa and significant strides into the cryptocurrency sphere, underscores its profound impact on the Fintech industry. Driven by its overarching mission to “unlock financial freedom for everyone,” Plaid continues to innovate and expand its reach. This article explores Plaid’s origins, the strategic advantage of its API-centric approach, and its growing influence within Web3 and its partnerships in the blockchain space.

alt: Plaid logo displayed against a tech background, representing Plaid’s brand and its focus on technology solutions for partners in finance and blockchain. Image for plaid blockchain partners article.

The Genesis of Plaid: Solving a Core Fintech Challenge

The inception of Plaid traces back to Zach Perret and William Hockey’s time at Bain & Co. in Atlanta. Their entrepreneurial spirit led them to leave their consulting roles to develop a consumer finance application. Initially aiming to simplify personal finance management through budgeting and bookkeeping apps, they encountered a recurring obstacle.

Instead of concentrating on user-facing features, their development efforts were heavily consumed by the backend complexities of establishing connections with diverse banking systems—a crucial step for their apps to function. This realization sparked a fundamental question: “Why is connecting a bank account and accessing my own money so arduous?” This question gained further urgency with the rise of FinTech in 2012 and the increasing consumer demand for digital financial solutions.

This challenge became the catalyst for Plaid’s unified banking API. Perret and Hockey recognized the inherent value of their backend technology, foreseeing its potential to expedite the development of Fintech products for numerous startups. This pivotal insight led them to New York, where they dedicated themselves to prototyping Plaid. By 2013, they had secured $2.8 million in funding to advance their groundbreaking platform.

At this juncture, a significant demand emerged within the financial sector for infrastructure solutions that could accelerate product development. Startups consistently faced the substantial hurdle of building proprietary platforms for financial data exchange.

alt: Founders of Plaid, Zach Perret and William Hockey, image representing Plaid’s leadership and vision in financial technology and blockchain partnerships.

By offering their banking API, Plaid became a pivotal enabler of the consumer fintech boom of recent years. Young companies could now effortlessly offer secure bank account connectivity to their customers.

[Zachary Perret @zachperret

Past three hours: meet company, explain @plaidhq, they integrate on the spot, and the app is now live in the US.](https://twitter.com/zachperret/status/395900679996186624?s=46&t=ydfOMqvCsTR0WSWF0xdk1Q)[1:10 PM ∙ Oct 31, 2013](https://twitter.com/zachperret/status/395900679996186624?s=46&t=ydfOMqvCsTR0WSWF0xdk1Q)

alt: Tweet from Zachary Perret announcing rapid Plaid integration, showcasing Plaid’s ease of use and quick partner onboarding for fintech and blockchain integrations.

Adrian Klee highlights the appeal of APIs in fintech:

“APIs have enabled both (fin)tech companies and traditional brands to enter the market by disaggregating banking products and enhancing convenience, focusing on financial services tailored to customer needs. Consumers and businesses prioritize convenience and instant access in financial management, preferring digital solutions and non-banking apps for transactions. Non-financial companies are increasingly leveraging API technology to expand into financial services.”

As consumer demand for digital finance solutions surged, Plaid’s growth mirrored this trend. Subsequent funding rounds of $12.5 million in 2014, $44 million in 2016, and $250 million in 2018, backed by financial giants like American Express and Goldman Sachs, fueled its expansion and solidified its position as a key player for plaid blockchain partners and the wider fintech ecosystem.

Understanding Plaid’s API and Functionality

Plaid’s core innovation lies in its API, which revolutionized how applications access private bank account information securely. In an era of heightened data privacy awareness, this is a significant achievement.

alt: Infographic depicting Plaid’s API connection process, illustrating secure data transfer between banks and applications, vital for understanding plaid blockchain partners integrations.

Plaid reports that approximately 90% of U.S. consumers utilize digital apps for financial management, underscoring the immense value of Plaid’s API for innovators aiming to address traditional consumer finance challenges. Plaid’s business model is ingenious: it charges the app for its service, not the end-user, making it seamless for consumers.

Here’s a simplified overview of the user experience with Plaid:

- An app prompts you to connect your bank account (e.g., during signup for a budgeting app or Robinhood).

- A Plaid-branded interface appears, prompting you to select your bank from over 10,000 institutions.

- You are redirected to your bank’s online login page within the app interface.

- You complete bank authentication (e.g., via SMS verification).

- You choose the accounts to link to the app.

- You finalize the connection process as per the app’s instructions.

Behind the scenes, Plaid’s API ensures:

- Instant verification of account ownership.

- Encryption of shared data.

- Secure data transmission to the app.

Plaid maintains a secure, persistent connection without ever accessing user login credentials. This streamlined process represents a monumental advancement over previous methods of financial data sharing.

Plaid’s Ascent and Near Acquisition by Visa

Plaid’s unwavering focus on its mission to “make money easier for everyone” fueled its rapid rise, attracting the attention of Visa. In early 2020, Visa announced a $5.3 billion acquisition plan for Plaid.

Visa’s interest stemmed from Plaid’s potential to enhance Visa’s infrastructure capabilities. Plaid’s intermediary role between consumers and banks provided access to vast user data, a valuable asset for Visa.

Ben Thompson of Stratechy summarized Visa’s acquisition rationale: “Plaid operates a unique three-sided network, distinct from Visa’s.

alt: Diagram illustrating Plaid’s three-sided network, connecting developers, consumers, and banks, key to Plaid’s value proposition for fintech and blockchain partners. Image source Stratechery.

The network benefits include:

- Developers: Instant bank account connectivity, eliminating complex integrations and slow verification processes.

- Consumers: Immediate access to Fintech apps like Venmo.

- Banks: [Complexities exist in bank benefits.]”

Despite the strategic alignment, the Department of Justice filed an antitrust lawsuit to block the merger, arguing it would stifle competition and further entrench Visa’s market dominance in online payments. Visa, controlling approximately 70% of the digital debit card market, was seen as preventing future competition by acquiring Plaid.

While Visa contended it could win the lawsuit, both companies mutually called off the deal, citing prolonged regulatory uncertainty. Plaid’s robust growth in 2020, fueled by the pandemic-driven surge in customers for Fintech platforms like Coinbase and Robinhood, also contributed to the decision. Plaid’s customer base grew by 60% in 2020 alone.

Mario Gabriele noted in ‘Plaid’s Quiet End Run’:

“Plaid’s success transcends the Visa deal. Even without payments, Plaid can achieve outcomes far exceeding Visa’s offer. By expanding geographically and adding products, Plaid strengthens its position in the financial system. In a dynamic market, Plaid remains a constant.”

The failed merger proved advantageous for Plaid, enhancing its visibility and market position. By 2021, Plaid’s valuation reached $13.4 billion, preceding a $425 million funding round, signaling continued growth.

alt: News headline graphic about Plaid’s valuation increase after Visa deal cancellation, highlighting Plaid’s resilience and growth potential for fintech and blockchain partnerships. Image source Axios.

Competition with Stripe and Market Dynamics

While Plaid is known for bank account connectivity, it has also entered into competition with Stripe, a payment technology giant valued at $95 billion in 2021.

Previously, Stripe partnered with Plaid to facilitate ACH payments, leveraging Plaid for simplified ACH verification. However, this partnership evolved as both companies sought to expand their product offerings.

Plaid’s acquisition of payment company Flannel in 2021 signaled its intent to move into payment processing, directly competing with Stripe. Subsequently, Stripe launched “Financial Connections,” a product mirroring Plaid’s functionality by enabling secure financial data sharing and bank account verification, positioning Stripe as a direct competitor.

This move sparked debate about Stripe leveraging its prior partnership with Plaid, even leading to public discussions. Despite the competition, Plaid CEO Zach Perret has differentiated Plaid by emphasizing its API-first approach and direct bank integrations, contrasting with Stripe’s more aggregated solution.

alt: Logo comparison graphic of Plaid and Stripe, illustrating the competitive landscape between these two major fintech companies and their evolving strategies in payments and blockchain.

Plaid’s resilience and adaptability remain key as it navigates increasing competition and market share dynamics with companies like Stripe.

Expanding Product Suite and Industry Solutions

](https://substackcdn.com/image/fetch/f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fbucketeer-e05bbc84-baa3-437e-9518-adb32be77984.s3.amazonaws.com%2Fpublic%2Fimages%2Fbac2282a-1197-4524-8337-9cfcfce85e91_800x550.png)

alt: Plaid company culture image, showcasing Plaid’s team and innovative environment driving fintech solutions and blockchain partnerships. Image source Plaid company website.

Plaid is extending its product offerings beyond core bank connectivity. A significant addition is the acquisition of Cognito, a leading identity verification platform. Plaid’s “Identity Verification” solution streamlines customer identity verification in as little as 30 seconds, utilizing email, phone, IP address, and device ID analysis to prevent fraud and enhance conversion rates.

“Monitor” is another Plaid product, aiding financial institutions in maintaining compliance with sanctions and watchlists. Plaid is also innovating in ACH payments with “Signal,” which assesses transaction risk to expedite fund access by evaluating over 1,000 risk factors, bringing Plaid closer to the payments sector.

These expanded solutions demonstrate Plaid’s ambition to evolve beyond its origins, aiming to connect all facets of finance, both traditional and decentralized, including strong moves towards plaid blockchain partners.

Plaid’s Vision: An API Ecosystem for Financial Freedom

[ alt: Graphic depicting Plaid’s API exchange and open banking vision, emphasizing data flow and connectivity in the financial ecosystem, including blockchain and crypto integration. Image source Forbes.

alt: Graphic depicting Plaid’s API exchange and open banking vision, emphasizing data flow and connectivity in the financial ecosystem, including blockchain and crypto integration. Image source Forbes.

Plaid’s mission is to democratize financial services through technology, building user-friendly experiences and developer-centric infrastructure. Their vision extends beyond simple bank connectivity to creating a comprehensive API-based ecosystem for Fintech.

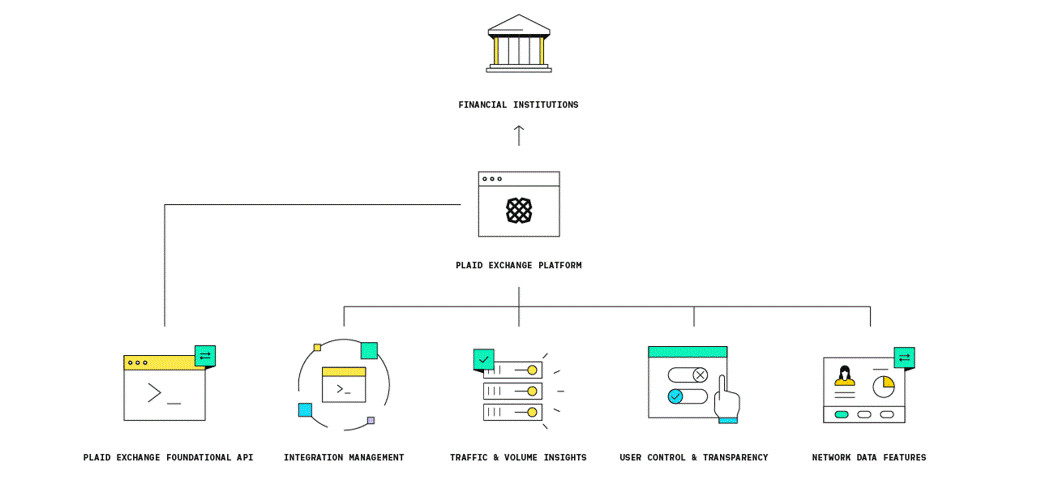

To realize this, Plaid is expanding its API capabilities to facilitate seamless financial data sharing. Cryptocurrency and Web3 represent a significant evolution in financial data, requiring new approaches. Plaid has adapted by innovating data connectivity solutions like “Plaid Exchange,” supporting API integrations for emerging fintech data types, including cryptocurrency and blockchain assets.

Currently, over 50% of Plaid’s connections utilize direct APIs, with over 1,000 partners committed to these integrations. Plaid’s innovations are fostering secure and reliable API connectivity, crucial for the future of finance and its intersection with blockchain technologies and plaid blockchain partners.

Plaid’s Foray into Web3 and Cryptocurrency

Web3, the decentralized internet, presents a paradigm shift, aiming to redistribute data ownership from corporations to individuals, leveraging blockchain and cryptocurrency for decentralized finance (DeFi).

Despite Web3’s nascent stage, its influence is growing, with 16% of US adults already using cryptocurrencies. Plaid is uniquely positioned to bridge traditional finance (TradFi) and DeFi.

[Zachary Perret @zachperret

What else should Plaid build to support the crypto community? All ideas welcome!](https://twitter.com/zachperret/status/1547619155200708608?s=46&t=ydfOMqvCsTR0WSWF0xdk1Q)[4:28 PM ∙ Jul 14, 202280Likes9Retweets](https://twitter.com/zachperret/status/1547619155200708608?s=46&t=ydfOMqvCsTR0WSWF0xdk1Q)

alt: Tweet from Zachary Perret soliciting ideas for Plaid’s crypto support, indicating Plaid’s active engagement with the crypto community and blockchain partners.

Plaid is facilitating a holistic financial view for consumers by integrating cryptocurrency exchanges and investment platforms, enabling users to manage both traditional and crypto assets in one place securely. Plaid is also lowering barriers to entry in cryptocurrency, simplifying crypto purchasing. For instance, Plaid enables secure bank account linking for exchanges like Gemini, streamlining ACH verification for faster crypto transactions, and fostering relationships with plaid blockchain partners.

](https://substackcdn.com/image/fetch/f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fbucketeer-e05bbc84-baa3-437e-9518-adb32be77984.s3.amazonaws.com%2Fpublic%2Fimages%2Ffd74d9e0-4503-4955-9182-0d21f11941eb_321x575.png)

alt: Plaid mobile app interface, showing account aggregation and financial management tools, reflecting Plaid’s role in unified finance including crypto and blockchain assets. Image source Plaid website.

Plaid has partnered with crypto exchanges and platforms including Gemini, Binance.us, Robinhood, SoFi, and Circle, with plans for further expansion in the crypto space, strengthening its position as a bridge for plaid blockchain partners.

Alain Meier, Plaid’s head of identity, noted: “We want to help consumers create a holistic view of their finances, bridging the gap between Web2 and Web3 with developer-first tooling.”

The Future Trajectory: Crypto and Beyond

](https://substackcdn.com/image/fetch/f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fbucketeer-e05bbc84-baa3-437e-9518-adb32be77984.s3.amazonaws.com%2Fpublic%2Fimages%2Fac0ba1af-7dfc-46f9-b236-680bb53c39b6_1200x1200.png)

alt: Abstract image representing cryptocurrency and blockchain technology, symbolizing Plaid’s future direction and deeper integration with Web3 and plaid blockchain partners.

Plaid’s entry into crypto suggests a future with deeper integration into wallets, Dapps, and bridging TradFi to crypto via stablecoins like USDC.

Plaid’s Collaboration with USDC and EUROC

Plaid integrated with Circle in 2021 to facilitate ACH payments for USDC, leveraging Plaid’s rapid account verification.

](https://substackcdn.com/image/fetch/f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fbucketeer-e05bbc84-baa3-437e-9518-adb32be77984.s3.amazonaws.com%2Fpublic%2Fimages%2Fa3dd765e-5a23-4d7f-bc7b-9a55c9fba366_1460x844.png)

alt: Flowchart illustrating Circle’s integration with Plaid for USDC payments, detailing the process of rapid account verification and ACH transfers, showcasing benefits for plaid blockchain partners using USDC. Image source Circle blog.

Plaid’s existing infrastructure for traditional finance positions it to connect TradFi with crypto seamlessly. Envision a future where money flows effortlessly between bank accounts and digital currencies like USDC and EUROC via simple API connections, enabling faster, safer, and more efficient global transactions.

Packy McCormick in ‘Circle & USDC: Building a Stable Platform’ notes:

“Stablecoins will coexist with banks and fintechs. Fintechs will build superior products on USDC rails, providing necessary compliance and interfaces. USDC will become a core component of more companies’ tech stacks.”

Plaid is poised to be the bridge, and Circle, the bedrock of crypto, especially with Circle’s ‘Cross-Chain Transfer Protocol’ enhancing USDC interoperability, creating new opportunities for cross-chain applications and strengthening the ecosystem for plaid blockchain partners.

](https://substackcdn.com/image/fetch/f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fbucketeer-e05bbc84-baa3-437e-9518-adb32be77984.s3.amazonaws.com%2Fpublic%2Fimages%2F9e1ddb8f-03e5-421c-b0c6-bf74a1c112df_1200x675.png)

alt: Graphic depicting cross-chain transfer protocol for USDC, highlighting interoperability across blockchains and benefits for developers building cross-chain applications and for plaid blockchain partners.

This initiative improves USDC liquidity and efficiency, fostering user-friendly cross-chain applications and expanding the utility for plaid blockchain partners.

Plaid: The Bridge to Web3 and Beyond

](https://substackcdn.com/image/fetch/f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fbucketeer-e05bbc84-baa3-437e-9518-adb32be77984.s3.amazonaws.com%2Fpublic%2Fimages%2F48637f3a-6e0c-4e30-9788-950c87c6b3bd_1600x900.png)

alt: Futuristic cityscape with bridges, symbolizing Plaid’s role as a bridge between traditional finance and the future of finance, including Web3, crypto, and blockchain.

Plaid’s early innovations marked the start of fintech’s infrastructure phase. It is poised to be critical infrastructure for future financial systems, bridging the gap to Web3, DeFi, and the Metaverse. As Plaid connected traditional financial rails, it is now beginning to connect Web3 and crypto, building the bridge to a more inclusive financial future with strong support for plaid blockchain partners.

Thank you for reading this edition of income-partners.net. Join us next time for more insights into the API Economy.