The year 2022 marked a significant turning point for Greenbrook Partners, a New York City-based multifamily developer and investment firm. After navigating a period of intense scrutiny and public backlash, the company, led by founder Gregory Fournier, strategically shifted its focus within the competitive New York real estate market. This pivot came after a challenging phase where tenant disputes and legal pressures put Greenbrook Partners in the public eye for reasons they would rather avoid.

Navigating the Storm and Charting a New Course

In late 2022, Greenbrook Partners faced a barrage of challenges. Tenant protests against vacate orders, which even drew the attention of Senator Chuck Schumer, accusations of illegal actions (later proven unfounded), and a lawsuit from New York City over housing violations painted a negative picture. Adding to the pressure, tenants alleged unlawful removal of apartments from rent stabilization, and the state attorney general launched an investigation into tenant harassment claims. A lengthy exposé in Mother Jones further amplified the negative narrative, branding Greenbrook Partners and its private equity partner Carlyle Group as “real estate predators.”

This intense scrutiny placed founder Gregory Fournier directly in the line of fire. However, just as quickly as the media storm gathered, it subsided. In October 2022, Greenbrook Partners reached a settlement with the state for a relatively modest sum, effectively stepping out of the harsh media spotlight.

Simultaneously, Fournier was quietly engineering a strategic realignment for Greenbrook Partners. He began to move away from acquiring large, rent-stabilized properties that had triggered tenant resistance and towards “value-add” opportunities with fewer complexities and less regulatory entanglement. Real estate records and broker insights indicate that Greenbrook Partners‘ new direction focused on buildings ripe for deregulation and smaller rental properties with significant potential for rent growth.

Low Profile, High Stakes: The Fournier Approach

Throughout the controversies of 2021, Gregory Fournier maintained a remarkably low public profile. He consistently avoided or declined requests for comments, cultivating a reputation for being press-shy, a stance he maintains today.

Fournier and fellow Greenbrook Partners principal Frederic LeCao declined interview requests for this profile and opted not to have a spokesperson address questions. Instead, they provided statements emphasizing the firm’s investment of over $100 million since 2018 in “the renovation of apartments in disrepair.”

While the exact start of Fournier’s real estate career remains unclear, his decade-long leadership of Greenbrook Partners has resulted in a substantial portfolio. According to PincusCo data, it comprises 102 buildings with a total of 737 units. Crucially, he cultivated a strong and enduring partnership with private equity giant Carlyle Group.

“He’s an ambitious guy,” noted an anonymous broker familiar with Fournier and Greenbrook Partners, adding, “He’s been around.”

Early in his career, Fournier held a co-management role in real estate investments for the Olayan Group. By 2013, he was interacting with prominent figures like Barry Sternlicht of Starwood Capital. A photo from the opening of Starwood’s Baccarat Hotel New York in 2013 captures Sternlicht, champagne in hand, alongside a seemingly reserved Fournier.

Prior to founding Greenbrook Partners, Fournier transitioned from Olayan to East End Capital, where he directed capital markets activities, as stated in his bio on Greenbrook Partners‘ website. He also participated in industry events, appearing alongside Bill Rudin of Rudin Management on a The Real Deal panel discussing international condo buyers.

In 2014, Fournier ventured out on his own, establishing Greenbrook Partners. Over the subsequent years, he strategically assembled a Brooklyn multifamily portfolio that rivaled those of established players in the borough.

Value-Add Strategy: When Good Intentions Meet Reality

Until the tenant backlash in 2021, Greenbrook Partners‘ strategy was clearly defined: to target “investments in poorly maintained, undermanaged, and undercapitalized assets located in growth-oriented and transitional submarkets of New York City,” according to their website.

Rent-stabilized properties appeared to be a primary focus early on. The 2022 settlement between Greenbrook Partners and the state involved 188 buildings with 1,000 units, “many of which are rent-stabilized,” as highlighted in the attorney general’s press release.

It’s likely that the majority of these acquisitions occurred before the significant rent law changes in June 2019, which drastically limited the ability to remove apartments from rent regulation.

Greenbrook Partners’ website states their investment focus is “in poorly maintained, undermanaged and undercapitalized assets located in growth-oriented and transitional submarkets of New York City.”

Previously, landlords could increase rents by 20 percent on vacant units and convert them to market rate if rents surpassed a specific threshold. The 2019 legislation effectively eliminated this practice, severely impacting owners who had relied on this strategy. Some, like Isaac Kassirer, faced financial distress, with some assets falling into bankruptcy within 18 months.

However, owners of buildings with a mix of regulated and market-rate apartments still had options. Unregulated units could be legally vacated upon lease expiration and then renovated to command higher rents. This “value-add” approach, while potentially lucrative, carried the risk of triggering tenant harassment complaints from those still residing in the building.

The attorney general’s settlement with Greenbrook Partners specifically noted that the firm initiated “significant construction projects” on properties acquired between 2019 and 2021. The A.G. cited complaints related to habitability issues, unpermitted construction, lack of maintenance, harassment, and non-compliance with rent regulation.

The de Blasio administration also took action against Greenbrook Partners. The Department of Housing Preservation and Development (HPD) filed two lawsuits in December 2020, alleging tenant harassment at adjacent buildings on Fourth Street in Park Slope. By mid-2021, online commentary had begun to label Greenbrook Partners a “slumlord,” reflecting the escalating public relations crisis.

Parkside Problems: The 70 Prospect Park West Case

While many landlords in New York City accumulate violations and face lawsuits, few attract the level of public condemnation and political attention that Greenbrook Partners experienced. The acquisition and subsequent actions at 70 Prospect Park West cemented Greenbrook Partners‘ place in this unenviable category.

Greenbrook Partners purchased the 30-unit building, located on a prime block overlooking Prospect Park in Park Slope, for $15 million on March 19, 2021. Tenants had long benefited from below-market rents in this desirable location, despite the building’s dated condition. Just a week after the sale, Greenbrook Partners issued 90-day vacate notices to all tenants.

Within a month, tenants from 70 Prospect Park West and other Greenbrook Partners properties organized as the Greenbrook Tenants Coalition. They staged rallies protesting construction harassment and sought assistance from then-City Council member Brad Lander. Advocates for “good cause eviction” – the right to lease renewals – amplified the case as a key example of landlord overreach.

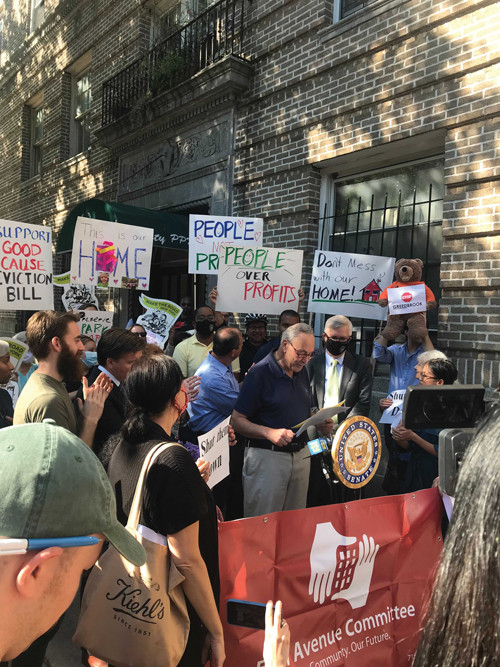

Senator Chuck Schumer, a powerful figure in national politics and a resident of Prospect Park West himself, joined one rally, walking a short distance from his own co-op. As a co-op owner, Schumer expressed disbelief that Greenbrook Partners could evict tenants simply because their leases expired, a standard practice in value-add real estate.

“There is nothing more despicable, despicable, than these predatory real estate equity firms trying to make illegal, in my judgment, billions of dollars on the backs of tenants,” Schumer declared at the protest, highlighting the intense political pressure Greenbrook Partners was facing.

By June, several tenants at 70 Prospect Park West had sued Greenbrook Partners, alleging they were charged market-rate rents for apartments that should have been rent-stabilized. Tenants at another Greenbrook Partners property, 509 12th Street, filed a similar lawsuit in December 2021.

However, the legal challenges were limited. Market-rate renters have limited legal protection against non-renewal of leases, provided landlords give proper notice. Just two months after Greenbrook Partners issued non-renewal notices at another Prospect Park building, nearly half of the residents had moved out, according to a report by City Limits.

In its October settlement with the attorney general, Greenbrook Partners agreed to pay $100,000 to HPD and issue $7,500 in rent credits to tenants in 10 buildings. Following this resolution, the public outcry diminished. The Greenbrook Tenant Coalition’s website has remained inactive since, and the group, once vocal with the press, did not respond to requests for comment. While the rent overcharge lawsuits are technically still ongoing, some tenants have reportedly discontinued their cases. The attorney for the tenants involved in these suits also did not respond to inquiries.

Senator Chuck Schumer at a rally against Greenbrook Partners' real estate practices in Brooklyn, NYC

Senator Chuck Schumer at a rally against Greenbrook Partners' real estate practices in Brooklyn, NYC

Strategic Pivot: Embracing Sub-Rehab and Small Rentals

This period of intense public and legal pressure, while challenging for Greenbrook Partners, ultimately led to a significant strategic shift. Gregory Fournier, unlike landlords such as Steve Croman, who faced jail time and hefty fines, and Raphael Toledano, banned from New York real estate, managed to navigate the crisis without lasting personal or professional damage.

Brokers familiar with Fournier indicate that he developed an interest in “substantial rehabilitation” projects, or “sub-rehabs.” This strategy allows owners who renovate at least 75 percent of a distressed rent-stabilized building to potentially move units to market rate.

“It’s one of the few avenues left to escape rent stabilization,” explained Sherwin Belkin, a partner at Belkin Burden Goldman, a real estate law firm.

However, a key requirement for sub-rehabs is vacancy. Owners seeking to avoid tenant-related complexities often prefer entirely vacant buildings, brokers noted, and Greenbrook Partners‘ recent acquisitions reflect this approach. In December, the firm acquired 168 Sumpter Street in Stuyvesant Heights, Central Brooklyn, for $1.5 million.

“It is worth noting that the six-unit building was delivered vacant,” commented Haley Hasho, co-founder of brokerage Exodus Capital. “The buyer has plans for a substantial rehabilitation play.”

Many of Greenbrook Partners’ deals with Carlyle Group align with this sub-rehab strategy, according to the anonymous broker. Carlyle Group did not respond to a request for comment.

The broker also mentioned a recent shift away from smaller “six- and eight-unit sub-rehab deals” due to increased regulatory scrutiny and paperwork concerns. This refers to state agency efforts to curb sub-rehab projects, which led to litigation and subsequent state legislation tightening the rules.

Previously, the sub-rehab process was “self-operating,” meaning that simply completing the renovations would exempt the building from rent stabilization, according to Belkin. However, starting this year, substantial rehabs require pre-approval from the state housing agency. While the Senate is currently working on amendments requested by Governor Kathy Hochul, significant changes are not anticipated.

Amidst these evolving regulations surrounding sub-rehab, Greenbrook Partners and Carlyle have increasingly focused on buildings entirely exempt from rent regulation.

“They kind of changed it up about a year ago,” the anonymous broker reiterated, highlighting the strategic pivot.

“You buy a turnkey three-, four-family, and nobody’s ever gonna come back and question whether it was done properly and throw it back into rent stabilization,” the broker explained. Buildings with fewer than six units are not subject to rent regulation in New York City, offering a more straightforward investment landscape.

Carlyle Group has made a significant push into Brooklyn’s small rental market. Over the past two years, they have invested nearly $1 billion in 174 properties, according to a PincusCo analysis. Greenbrook Partners has partnered with Carlyle on some of these transactions, which typically involve renovated properties. For example, in late January, the firms acquired a three-family apartment building in Bedford-Stuyvesant for $2 million, property records indicate.

The seller of 1113 Herkimer Street had purchased the building just nine months prior for half the price. An April 2023 listing described the property as having “great potential with some hands-on TLC,” and a current listing for a first-floor apartment advertises it as “newly renovated.”

These smaller properties often fall under the city’s 2A/2B tax designation, which limits annual real estate tax increases to 8 percent – a significant benefit for owners. Greenbrook Partners and Carlyle’s acquisitions have been concentrated in Brooklyn, where new lease signings have doubled year-over-year, and median rents are near record highs.

Interestingly, in some Carlyle deals, it appears Greenbrook Partners may be acting as a developer, renovating properties and then selling them to Carlyle. As of last June, Greenbrook Partners had sold at least 19 properties to Carlyle affiliates in the preceding 18 months, realizing a 75 percent increase over their purchase price from just a year or two earlier, PincusCo reported.

In one notable transaction last year, Greenbrook Partners sold 140 Frost Street, 171 Cooper Street, and 516 Fairview Avenue to a Carlyle entity for $9.5 million. At 140 Frost Street, Carlyle subsequently rented out a two-bedroom apartment in July for $4,350, a 67 percent increase from the previous rent in 2020, before Greenbrook Partners acquired the building.

Greenbrook Partners partly used the proceeds from these sales to repay a watchlisted loan. This securitized debt was short-term and floating-rate, a type of financing commonly used for value-add projects. When questioned about the troubled debt last year, Fournier appeared unfazed. He stated via email that the sale had fully repaid the loan, leaving the three other properties that had served as collateral unencumbered.

“No debt,” he wrote. “Pure profit,” encapsulating Greenbrook Partners‘ ability to navigate challenges and identify new avenues for profitability in the dynamic New York City real estate market.