Capio Partners LLC is a name you might encounter if you have past-due medical bills. As a third-party debt collection agency, Capio Partners specializes in recovering unpaid medical debts. It’s crucial to understand your rights and how to respond effectively if Capio Partners contacts you. Before making any payments, ensure they officially validate the debt. If you believe the debt is incorrect or not yours, dispute it immediately. For legitimate debts, explore options like setting up a payment plan or negotiating a settlement to potentially pay less than the original amount owed.

Person looking at debt validation letters

Person looking at debt validation letters

Understanding Capio Partners LLC

Capio Partners LLC operates as a debt collection agency that focuses primarily on medical and healthcare-related debts. Established in 2008, Capio Partners is headquartered in Sherman, Texas, with additional offices in Lawrenceville, Georgia. They operate across the United States, purchasing debts from healthcare providers and then attempting to collect those debts from consumers.

Why is Capio Partners Reaching Out?

If Capio Partners is contacting you, it’s highly likely they are attempting to collect on an outstanding medical debt. This could stem from various healthcare services such as hospital visits, ambulance services, or doctor’s office bills. Often, healthcare providers initially try to recover these debts themselves. However, if the bills remain unpaid after a certain period, these providers may “charge off” the debt and sell it to a third-party agency like Capio Partners. This transfer of debt explains why you might be contacted by Capio Partners instead of the original medical facility.

Is Capio Partners a Legitimate Debt Collector?

Capio Partners is indeed a legitimate third-party debt collection agency. However, it’s worth noting that numerous consumers have lodged complaints against their practices.

While Capio Partners is not accredited by the Better Business Bureau (BBB), they do hold a “B” rating from the BBB. Their consumer review rating on the BBB platform is quite low, at 1.16 out of 5 stars, accompanied by nearly 500 complaints filed by consumers.

Furthermore, the Consumer Financial Protection Bureau (CFPB) has recorded over 1,200 complaints concerning Capio Partners. These complaints often highlight issues such as:

- Being contacted about debts that consumers claim they do not owe or are not responsible for.

- Failure to provide sufficient documentation to validate the debt, including original contracts or account details.

- Lack of legally required information on how to dispute the debt.

These issues raised in consumer complaints may indicate potential violations of the Fair Debt Collection Practices Act (FDCPA). The FDCPA is a federal law designed to protect consumers from abusive, deceptive, and unfair practices by debt collectors. It mandates that debt collectors provide consumers with a debt validation notice and information on how to dispute the debt, among other protections.

It’s important to remember that while these complaints are informative, they may not represent the experiences of every individual who has dealt with Capio Partners.

Avoiding Scams Posing as Capio Partners

While Capio Partners is a real debt collection agency, be vigilant about potential scams. Scammers sometimes impersonate legitimate agencies like Capio Partners to extract money from unsuspecting individuals. Understanding the warning signs of debt collector scams is crucial for protection.

If you are contacted by someone claiming to be a debt collector and you are unsure of their legitimacy, always request debt validation before providing any personal information. A legitimate debt collector should possess details about your debt account. Be particularly cautious if they demand sensitive information like bank account details or your Social Security number upfront, as this is a significant red flag.

Understanding Your Obligation to Pay Capio Partners LLC

Whether you are legally obligated to pay Capio Partners depends on the legitimacy of the debt. The first crucial step is to ensure you receive a debt validation notice from Capio Partners. This notice should detail the original debt, including the name of the healthcare provider, the date of service, and the amount Capio Partners claims you owe.

If you haven’t received a validation notice or need further clarification, you have the right to send a debt verification letter to Capio Partners to request more information.

Step 1: Sending a Debt Verification Letter to Capio Partners

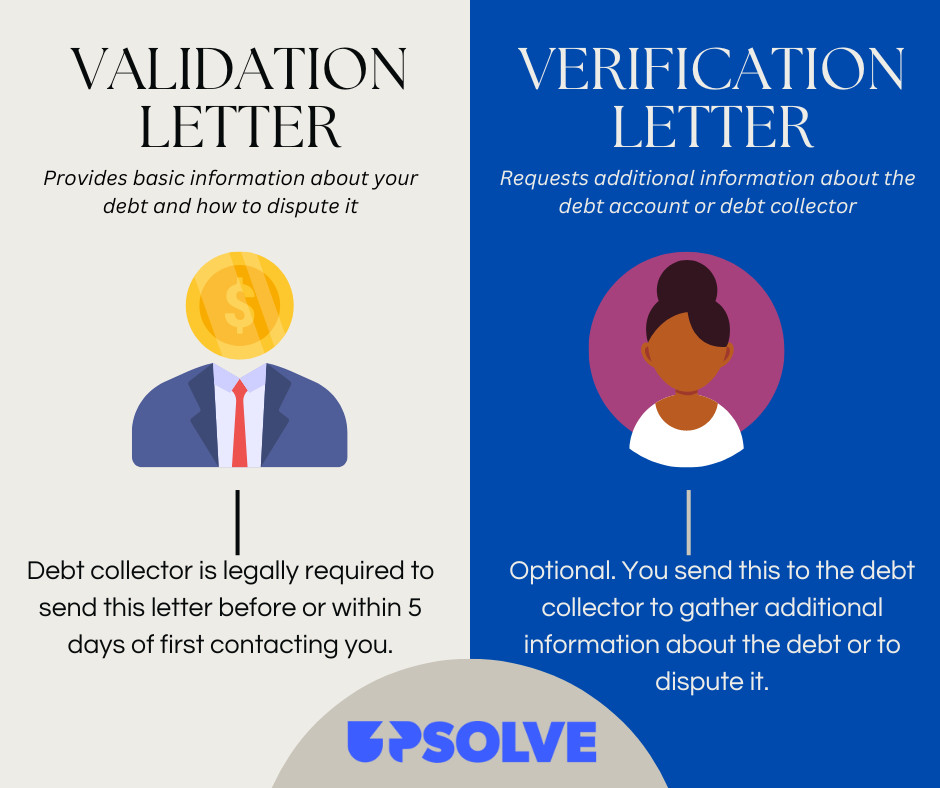

Debt collectors like Capio Partners are legally required under the FDCPA to send a debt validation letter. This should occur either before their initial contact with you or within five days of that first contact. This letter must inform you of your right to dispute the debt if you disagree with its validity.

You have a 30-day period from the receipt of the validation notice to dispute the debt. If you formally dispute the debt, it should be noted on your credit report. During this dispute period, Capio Partners should cease collection attempts, including phone calls, until they have responded to your dispute and provided verification of the debt.

Should you dispute the debt within this 30-day timeframe, and Capio Partners fails to validate it or does not respond to your dispute, they are legally obligated to halt all collection efforts. In such cases, you should not be required to pay the disputed amount.

While often used interchangeably, it’s helpful to distinguish between a debt validation letter (which Capio Partners should send) and a debt verification letter (which you can send to request more details). You might send a verification letter if the initial validation notice is unclear or lacks necessary information.

Here’s a quick summary to clarify the difference:

| Feature | Debt Validation Letter (From Capio Partners) | Debt Verification Letter (From You) |

|---|---|---|

| Purpose | Initial notification of debt & dispute rights | Request for more information about the debt |

| Sender | Capio Partners | You |

| Timing | Before or within 5 days of first contact | Any time, especially if validation is unclear |

| Legal Requirement | Required by FDCPA | Consumer right under FDCPA |

Step 2: Deciding Your Next Steps After Debt Validation

Once Capio Partners has validated the debt, you have several options to consider:

- Dispute the Debt: If you still believe the debt is inaccurate, not yours, or has already been paid.

- Negotiate a Debt Settlement: Attempt to pay a reduced amount or set up a payment plan if you acknowledge the debt but cannot pay the full amount immediately.

- Ignore the Debt: While an option, this is strongly discouraged due to potential negative consequences.

Let’s explore each of these options in more detail to help you make an informed decision.

Option 1: Disputing the Debt with Capio Partners

If you disagree with the debt amount, believe the debt is not yours, or think it has already been settled by you or your insurance, you should formally dispute the debt with Capio Partners.

Instructions for disputing the debt are typically included in the debt validation letter. For more detailed guidance, resources are available to help you navigate disputing a debt you don’t owe.

When disputing a debt, it’s also wise to review your credit report for any inaccuracies. Errors on credit reports are common and can negatively impact your credit score if not corrected. This is particularly relevant for medical debts. However, it’s worth noting that medical debts under $500 should not appear on your credit report, irrespective of their status, according to the CFPB.

The Fair Credit Reporting Act (FCRA) grants you the right to access your credit reports from the three major credit bureaus: Equifax, Experian, and TransUnion. The FCRA also empowers you to dispute any inaccuracies found in your credit reports. Resources are available to guide you through the process of disputing credit report errors effectively.

Option 2: Negotiating a Debt Settlement with Capio Partners

If you acknowledge the debt to Capio Partners but are unable to pay the full amount, negotiating a debt settlement or a payment plan is a viable option. You can contact Capio Partners directly at (888) 502-0303 to discuss these arrangements.

For debt settlement negotiations, it is advisable to present your offer in writing. You can find templates to help you draft a debt settlement offer letter. While phone negotiations are possible, obtaining a written agreement is crucial for clarity and documentation.

How Debt Settlement Works

Debt settlement is often a feasible strategy because debt collection agencies like Capio Partners typically purchase debts for a fraction of their original value. This allows them some flexibility in negotiating settlement amounts.

It’s not uncommon for debt collectors to agree to settlements ranging from 40% to 60% of the total debt. For instance, on a $1,000 medical bill, you might offer to pay $400 to settle the account. Be prepared for a negotiation process that might involve a few counteroffers before reaching an agreement.

Resources are available to provide further strategies on how to effectively negotiate with Capio Partners and potentially reduce your debt.

Types of Debts Eligible for Negotiation

While not all debts are negotiable, many common consumer debts are, including medical bills, credit card debts, and other unsecured debts not tied to assets like homes or vehicles. Even the IRS has specific procedures for settling outstanding tax debts.

However, debts like car loans and home loans are typically less negotiable because they are secured by collateral. Failure to pay these debts can result in the repossession of the car or foreclosure on the home.

Student loans also fall into a unique category. Negotiating student loan debt is generally challenging, although there has been an increase in student loan forgiveness programs in recent years, which may offer relief if you are struggling with student debt.

Option 3: Ignoring the Debt – A Highly Discouraged Approach

Ignoring communication from Capio Partners is generally not a recommended strategy. While medical debts under $500 may not impact your credit score, ignoring Capio Partners is unlikely to make the debt disappear and could lead to increased stress and more aggressive collection actions.

Capio Partners might escalate their collection efforts if ignored. This could include initiating a debt collection lawsuit against you, which could potentially lead to wage garnishment to recover the debt. Furthermore, legal actions often result in additional costs such as court fees and legal expenses being added to your debt.

In conclusion, proactively addressing your debt with Capio Partners is in your best interest. Taking action to dispute or settle the debt will likely be beneficial in the long run, providing clarity and resolution.

Can Capio Partners Take Legal Action Against You?

Yes, Capio Partners, like any debt collector or original creditor, has the legal right to sue you to recover unpaid debt. However, it is not typically their first course of action.

If Capio Partners decides to sue you, you will be officially served with court documents, including a summons and a complaint. These documents notify you of the lawsuit and the reasons behind it.

Responding to a debt collection lawsuit is critical. Ignoring a lawsuit will likely result in a default judgment against you, granting Capio Partners the legal authority to garnish your wages or take other actions to collect the debt.

If you are sued and need assistance responding, resources are available, such as online legal aid services that can help you draft an answer to the lawsuit, potentially for free or at a minimal cost. These services are designed to assist individuals in responding to debt lawsuits effectively, even without legal representation.

Summary: Key Steps for Dealing with Capio Partners

Capio Partners LLC is a legitimate debt collection agency specializing in medical debt. If they contact you, remember these key steps:

- Demand Debt Validation: Before anything else, ensure Capio Partners validates the debt in writing.

- Assess the Debt: Determine if you agree with the debt. If not, dispute it formally.

- Negotiate or Plan Payment: If the debt is valid and you owe it, contact Capio Partners to negotiate a settlement or establish a payment plan.

- Understand Legal Rights: Be aware that Capio Partners could potentially sue you, and it’s crucial to respond to any legal notices.

By taking proactive and informed steps, you can effectively manage interactions with Capio Partners and work towards resolving any outstanding medical debts.