How Much Should Your Car Payment Be Based On Income? Determining how much to spend on a car payment is a crucial financial decision, and at income-partners.net, we understand the importance of aligning your car expenses with your income to ensure financial stability and growth. By following proven strategies, you can achieve a balanced budget, explore strategic partnerships, and unlock new income streams. This article will guide you through calculating an affordable car payment, considering various factors, and making informed decisions to boost your overall financial health.

1. Understanding the Income-Based Car Payment Rule

What is the golden rule when deciding on your car payment amount based on income? A general guideline suggests that your total monthly car expenses, including the car payment, insurance, and fuel, should not exceed 10-15% of your net monthly income. This rule helps ensure that you don’t overextend yourself financially and leave room for other essential expenses and financial goals.

To determine the ideal car payment, begin by assessing your net monthly income, which is your take-home pay after taxes and other deductions. From there, calculate 10-15% of this amount to find the maximum you should allocate to car expenses. For instance, if your net monthly income is $5,000, your total car expenses should ideally be between $500 and $750.

1.1 Why Follow This Rule?

Why is adhering to the income-based car payment rule so important? Sticking to this guideline ensures financial stability and prevents overspending on a depreciating asset. Overextending yourself on a car payment can lead to financial strain, making it difficult to cover other essential expenses, save for retirement, or invest in opportunities for income growth through income-partners.net.

According to a study by the University of Texas at Austin’s McCombs School of Business, households that allocate more than 20% of their income to car expenses are more likely to face financial difficulties, including higher debt levels and reduced savings rates. By staying within the recommended 10-15% range, you create a buffer in your budget for unexpected expenses and investment opportunities.

1.2 Factors Affecting Your Car Payment Decision

What factors should influence your decision beyond just the income-based rule? Several factors can influence your car payment decision, including your credit score, down payment amount, loan term, and other monthly expenses. Each element plays a critical role in determining what you can realistically afford.

- Credit Score: A higher credit score typically results in lower interest rates on car loans.

- Down Payment: A larger down payment reduces the loan amount and, consequently, the monthly payment.

- Loan Term: Longer loan terms lead to lower monthly payments but higher overall interest paid.

- Monthly Expenses: Existing financial obligations, such as rent, utilities, and debt payments, should be considered to ensure you can comfortably afford the car payment.

Considering these factors alongside the income-based rule provides a comprehensive understanding of your financial capacity to handle a car payment. This approach allows you to make an informed decision that supports your long-term financial goals.

Consider these factors carefully to calculate affordable monthly car payment

Consider these factors carefully to calculate affordable monthly car payment

2. Calculating Your Ideal Car Payment

How can you precisely calculate your ideal car payment? To determine your ideal car payment, start by evaluating your net monthly income and deducting all recurring monthly expenses. The remaining amount is what you can allocate to car-related costs. Aim to keep your total car expenses within 10-15% of your net income, adjusting for factors like credit score and down payment.

2.1 Step-by-Step Calculation Guide

What are the exact steps to calculate an affordable car payment? Follow these steps to calculate an affordable car payment:

- Determine Net Monthly Income: Calculate your take-home pay after taxes and deductions.

- List Monthly Expenses: Include rent, utilities, groceries, debt payments, and other recurring costs.

- Calculate Available Funds: Subtract total expenses from net income.

- Apply the 10-15% Rule: Determine the maximum amount for car expenses based on this percentage.

- Adjust for Additional Factors: Modify the amount based on credit score, down payment, and loan term.

By following these steps, you can arrive at a realistic car payment amount that fits comfortably within your budget.

2.2 Example Scenarios

Can you provide some example scenarios to illustrate this calculation? Consider these scenarios:

- Scenario 1: Net monthly income of $4,000 with $2,000 in monthly expenses. Applying the 10-15% rule, car expenses should be between $200 and $300.

- Scenario 2: Net monthly income of $6,000 with $3,000 in monthly expenses. Car expenses should be between $300 and $450.

- Scenario 3: Net monthly income of $8,000 with $4,000 in monthly expenses. Car expenses should be between $400 and $600.

These examples demonstrate how the 10-15% rule applies to different income levels and expense structures, providing a clear framework for determining an affordable car payment.

3. Factors Influencing Car Affordability

What other factors beyond income should you consider when assessing car affordability? Beyond income, several factors significantly impact car affordability, including credit score, interest rates, down payment, and loan term. Understanding these elements is crucial for making an informed decision.

3.1 Credit Score and Interest Rates

How does your credit score affect the interest rate you’ll receive on a car loan? Your credit score is a primary determinant of the interest rate you’ll receive on a car loan. A higher credit score typically qualifies you for lower interest rates, reducing the overall cost of the loan and the monthly payment.

According to Experian, borrowers with excellent credit scores (750+) receive the lowest interest rates, while those with poor credit scores (below 500) pay significantly higher rates. Improving your credit score before applying for a car loan can save you thousands of dollars over the life of the loan.

3.2 Down Payment Impact

How does making a larger down payment affect your car loan and monthly payments? A larger down payment reduces the loan amount, resulting in lower monthly payments and less interest paid over the loan term. Additionally, a substantial down payment can increase your chances of loan approval and may qualify you for better interest rates.

For example, putting down 20% of the car’s purchase price can significantly reduce the loan amount compared to a 5% down payment. This can make the car more affordable and help you stay within your budget.

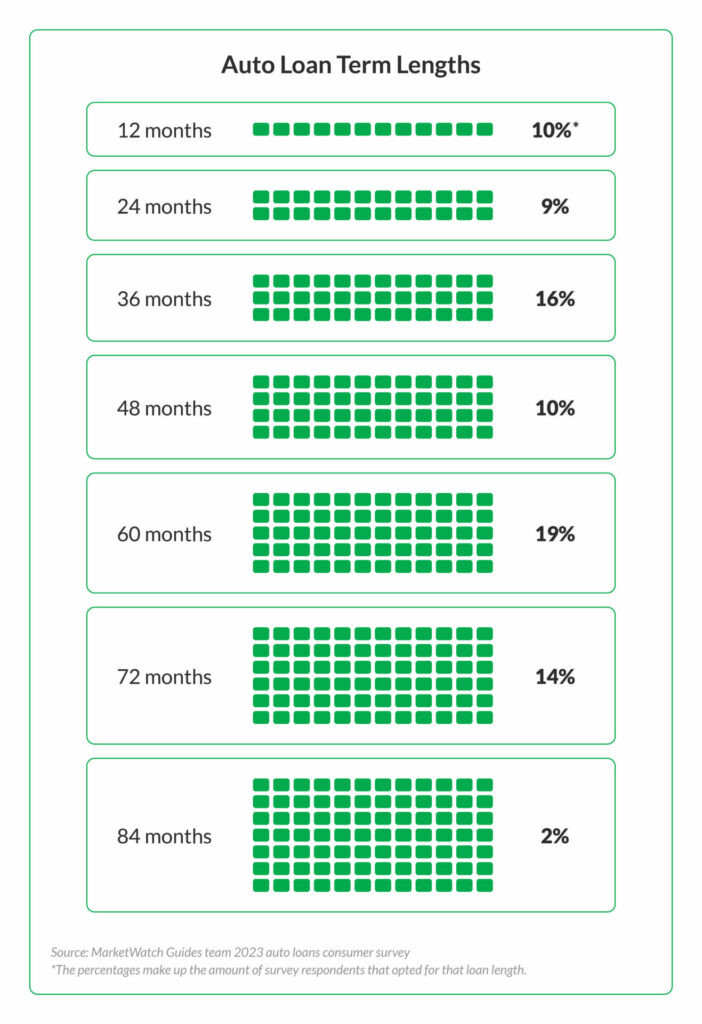

3.3 Loan Term Considerations

What are the pros and cons of choosing a shorter or longer loan term? The loan term, or the length of time you have to repay the loan, affects both the monthly payment and the total interest paid. Shorter loan terms result in higher monthly payments but lower overall interest, while longer loan terms offer lower monthly payments but accumulate more interest over time.

Choosing the right loan term depends on your financial goals and cash flow. If you prioritize paying off the loan quickly and minimizing interest, a shorter term is preferable. If you need lower monthly payments to fit within your budget, a longer term may be necessary.

4. Car Loan Options and Strategies

What are some effective strategies for securing a car loan that aligns with your income and financial goals? Securing a car loan requires careful planning and strategic decision-making. Evaluating loan options, negotiating terms, and considering alternative financing can lead to better affordability and financial outcomes.

4.1 Evaluating Loan Options

Where should you look for the best car loan rates and terms? Shop around and compare offers from various lenders, including banks, credit unions, and online lenders, to find the best interest rates and loan terms. Pre-approval can give you a clear idea of how much you can borrow and at what rate.

Credit unions often offer competitive rates and flexible terms for their members. Online lenders may provide convenience and quick approvals. Banks can offer established relationships and potential discounts for existing customers.

4.2 Negotiating Loan Terms

How can you negotiate the terms of your car loan to lower your monthly payment? Negotiating loan terms, such as the interest rate and loan term, can significantly lower your monthly payment and overall cost. Come prepared with research on current rates and a clear understanding of your budget.

Negotiating tactics include:

- Improving your credit score: Address any errors and ensure timely payments.

- Increasing your down payment: Save more to reduce the loan amount.

- Shopping around: Get multiple quotes to leverage competitive offers.

- Considering a co-signer: A creditworthy co-signer can improve your approval chances and interest rate.

4.3 Alternative Financing Options

Are there alternative financing options to consider besides traditional car loans? Explore alternative financing options, such as leasing or buying a used car, to potentially lower your monthly payments and overall car expenses. Leasing involves making monthly payments to use a car for a set period, while buying a used car can be more affordable than purchasing a new one.

Leasing may be a good option if you prefer driving a new car every few years and don’t mind mileage restrictions. Buying a used car can save you money on depreciation and insurance costs.

5. The Total Cost of Car Ownership

What expenses beyond the car payment should you factor into your car budget? Understanding the total cost of car ownership is essential for accurate budgeting. Beyond the monthly car payment, consider expenses such as insurance, fuel, maintenance, and repairs.

5.1 Insurance Costs

How much can you expect to pay for car insurance, and how can you lower your premium? Car insurance costs vary based on factors like your age, driving record, location, and vehicle type. Obtain quotes from multiple insurers to compare rates and coverage options.

Strategies to lower your insurance premium include:

- Increasing your deductible: A higher deductible lowers the premium but requires you to pay more out-of-pocket in case of an accident.

- Bundling policies: Combining car insurance with home or renters insurance can result in discounts.

- Maintaining a clean driving record: Avoiding accidents and traffic violations keeps your premium low.

- Taking a defensive driving course: Some insurers offer discounts for completing a defensive driving course.

5.2 Fuel and Maintenance

How can you estimate your fuel costs and plan for routine maintenance? Fuel costs depend on your driving habits, the vehicle’s fuel efficiency, and current gas prices. Use online tools to estimate fuel consumption based on your average mileage.

Regular maintenance, such as oil changes, tire rotations, and brake inspections, is essential for keeping your car running smoothly and avoiding costly repairs. Budget for these expenses based on the manufacturer’s recommended maintenance schedule.

5.3 Unexpected Repairs

How should you prepare for unexpected car repairs? Unexpected car repairs can be a significant financial burden. Build an emergency fund specifically for car repairs to avoid debt. Consider purchasing an extended warranty for added protection.

Tips for managing unexpected repairs:

- Get multiple estimates: Compare quotes from different mechanics.

- Prioritize repairs: Address urgent issues first.

- Use a credit card with rewards: Earn points or cash back on repairs.

- Consider DIY repairs: If you have mechanical skills, tackle simple repairs yourself.

6. Balancing Car Expenses With Financial Goals

How can you ensure that your car payment doesn’t derail your long-term financial goals? Balancing car expenses with financial goals requires careful planning and prioritizing. Aligning your car payment with your overall financial strategy helps ensure you achieve your long-term objectives.

6.1 Prioritizing Savings and Investments

How can you ensure you’re still saving and investing while making car payments? Make saving and investing a priority by automating contributions to retirement accounts and investment funds. Treat these contributions as non-negotiable expenses.

Strategies for prioritizing savings and investments:

- Set financial goals: Define clear objectives, such as retirement, homeownership, or education.

- Create a budget: Track income and expenses to identify areas for savings.

- Automate savings: Set up automatic transfers to savings and investment accounts.

- Take advantage of employer-sponsored plans: Maximize contributions to 401(k)s and other retirement plans.

6.2 Debt Management Strategies

What are some effective strategies for managing other debts while paying off a car loan? Managing other debts while paying off a car loan requires a strategic approach. Prioritize high-interest debts and consider debt consolidation or balance transfers to lower interest rates.

Debt management strategies include:

- Prioritizing high-interest debts: Focus on paying off credit card debt and other high-interest loans first.

- Debt consolidation: Combine multiple debts into a single loan with a lower interest rate.

- Balance transfers: Transfer high-interest credit card balances to a card with a lower rate.

- Snowball or avalanche method: Choose a debt repayment strategy based on your preferences.

6.3 Building an Emergency Fund

Why is it crucial to have an emergency fund, and how can you build one? An emergency fund provides a financial safety net for unexpected expenses, reducing the need to rely on debt. Aim to save three to six months’ worth of living expenses in a readily accessible account.

Building an emergency fund involves:

- Setting a savings goal: Determine the amount you need to save.

- Creating a budget: Identify areas where you can cut expenses.

- Automating savings: Set up automatic transfers to your emergency fund.

- Using windfalls wisely: Save unexpected income, such as tax refunds or bonuses.

7. Navigating Car Ownership in Austin, TX

How can you navigate the unique challenges and opportunities of car ownership in Austin, TX? Austin, TX, presents unique challenges and opportunities for car ownership. Understanding local factors like traffic, public transportation, and car insurance rates can help you make informed decisions.

7.1 Local Traffic Considerations

How does Austin’s traffic impact your car payment affordability? Austin’s heavy traffic can increase fuel costs and wear and tear on your vehicle. Consider these factors when calculating your car budget.

Strategies for mitigating the impact of traffic:

- Plan your routes: Use navigation apps to find the most efficient routes.

- Consider public transportation: Explore options like buses, trains, and ride-sharing services.

- Work remotely: If possible, reduce your commute by working from home.

- Carpool: Share rides with colleagues or neighbors.

7.2 Public Transportation Options

What are the public transportation options in Austin, and how can they help reduce car dependency? Austin offers various public transportation options, including buses, trains, and ride-sharing services. Utilizing these alternatives can reduce your reliance on a car and save money on car expenses.

Public transportation options in Austin:

- Capital MetroBus: A network of bus routes throughout the city.

- MetroRail: A commuter rail line connecting downtown Austin with surrounding areas.

- Ride-sharing services: Companies like Uber and Lyft provide on-demand transportation.

- Bicycle sharing: Austin B-cycle offers bike rentals for short trips.

7.3 Insurance Rates in Texas

How do car insurance rates in Texas compare to the national average, and what factors influence these rates? Car insurance rates in Texas tend to be higher than the national average due to factors like population density, traffic congestion, and weather-related risks.

Factors influencing car insurance rates in Texas:

- Location: Urban areas typically have higher rates than rural areas.

- Driving record: Accidents and traffic violations increase premiums.

- Vehicle type: Expensive or high-performance cars cost more to insure.

- Coverage options: Higher coverage levels result in higher premiums.

8. Income-Boosting Opportunities for Car Owners

How can car owners leverage their vehicles to generate additional income and offset car expenses? Car owners can leverage their vehicles to generate additional income and offset car expenses. Exploring opportunities like ride-sharing, delivery services, and advertising can turn your car into an income-generating asset.

8.1 Ride-Sharing Services

How can you make money by driving for ride-sharing services like Uber or Lyft? Driving for ride-sharing services like Uber or Lyft can provide a flexible income stream. Consider the requirements, costs, and potential earnings before signing up.

Factors to consider:

- Vehicle requirements: Ensure your car meets the service’s standards.

- Insurance: Obtain the necessary insurance coverage.

- Time commitment: Determine how many hours you can dedicate to driving.

- Earnings potential: Research average earnings in your area.

8.2 Delivery Services

What are some popular delivery services that allow you to use your car to earn money? Delivery services like DoorDash, Uber Eats, and Instacart offer opportunities to earn money by delivering food, groceries, and other items.

Delivery service options:

- DoorDash: Deliver food from restaurants to customers.

- Uber Eats: Similar to DoorDash, focusing on restaurant deliveries.

- Instacart: Shop for and deliver groceries to customers.

- Amazon Flex: Deliver packages for Amazon.

8.3 Car Advertising

Can you get paid to advertise on your car? Yes, you can get paid to advertise on your car by wrapping it with advertisements for various companies. Research reputable advertising companies and consider the terms and conditions before participating.

Factors to consider:

- Company reputation: Choose a reliable advertising company.

- Contract terms: Understand the duration, payment schedule, and requirements.

- Vehicle appearance: Ensure the wrap is professionally installed and maintained.

- Driving habits: Ad campaigns may require you to drive a certain number of miles.

9. Maximizing Financial Partnerships for Car Ownership

How can you leverage financial partnerships to make car ownership more affordable and financially rewarding? Maximizing financial partnerships can significantly enhance your financial stability and make car ownership more manageable. Strategic collaborations can open doors to increased income, better financial terms, and valuable support. This is where income-partners.net can be an invaluable resource, connecting you with opportunities to improve your financial situation.

9.1 Collaborating With Local Businesses

How can partnering with local businesses help offset car expenses? Collaborating with local businesses can create mutually beneficial relationships that offset car expenses. For example, you might offer delivery services for a local restaurant or provide transportation for clients of a local real estate agency in exchange for compensation or discounts.

Here’s how to make the most of such partnerships:

- Identify potential partners: Look for businesses that could benefit from your services.

- Propose a win-win scenario: Offer services in exchange for compensation or discounts.

- Formalize the agreement: Ensure the terms are clear and documented.

- Maintain open communication: Regularly communicate to ensure mutual satisfaction.

9.2 Leveraging Income-Partners.Net for Opportunities

How can Income-Partners.Net connect you with financial opportunities related to car ownership? Income-partners.net can connect you with financial opportunities related to car ownership by providing a platform to find partners who need transportation or delivery services. This can help you leverage your car as an asset to generate additional income.

Benefits of using income-partners.net:

- Access to a network: Connect with potential partners seeking transportation solutions.

- Diverse opportunities: Find a range of collaborations, from delivery services to client transport.

- Structured agreements: Easily formalize partnerships with clear terms.

- Income diversification: Add a new income stream to your portfolio.

By leveraging income-partners.net, you can transform your car from a mere expense into a revenue-generating asset, contributing to your overall financial health.

9.3 Financial Planning Partnerships

How can working with a financial planner help you optimize your car-related expenses and investments? Collaborating with a financial planner can provide expert guidance on optimizing your car-related expenses and investments. A financial planner can help you create a budget, manage debt, and plan for long-term financial goals, including car ownership.

A financial planner can assist with:

- Budgeting: Creating a realistic budget that includes car expenses.

- Debt management: Developing strategies to pay off car loans and other debts.

- Investment planning: Ensuring your investments align with your financial goals.

- Financial goal setting: Setting clear, achievable financial objectives.

10. Future-Proofing Your Car Payment Strategy

How can you ensure that your car payment strategy remains effective and sustainable in the long run? Future-proofing your car payment strategy involves regularly reviewing your financial situation, adjusting your budget as needed, and exploring new opportunities to optimize your car-related expenses.

10.1 Regular Financial Check-Ups

Why is it important to regularly review your financial situation and adjust your car payment strategy? Regularly reviewing your financial situation ensures that your car payment strategy remains aligned with your goals. Changes in income, expenses, or financial priorities may require adjustments to your budget and car payment plan.

Key steps for a financial check-up:

- Review your income and expenses: Track your cash flow to identify trends.

- Assess your debt: Evaluate your outstanding debts and develop a repayment strategy.

- Evaluate your investments: Ensure your investments are performing as expected.

- Adjust your budget: Modify your budget to reflect changes in your financial situation.

10.2 Adapting to Economic Changes

How can you adjust your car payment strategy in response to economic changes? Economic changes, such as inflation, interest rate hikes, or job loss, can impact your ability to afford your car payment. Be prepared to adjust your strategy as needed to maintain financial stability.

Strategies for adapting to economic changes:

- Refinance your car loan: Take advantage of lower interest rates to reduce your monthly payment.

- Downsize your vehicle: Consider selling your car and purchasing a more affordable model.

- Increase your income: Explore opportunities for additional income through part-time work or side hustles.

- Reduce your expenses: Identify areas where you can cut spending to free up cash flow.

10.3 Staying Informed on Financial Trends

How can staying informed on financial trends help you make better car payment decisions? Staying informed on financial trends helps you make better car payment decisions by providing insights into interest rates, loan terms, and economic conditions. This knowledge empowers you to make informed choices that align with your financial goals.

Resources for staying informed:

- Financial news websites: Stay updated on economic trends and financial news.

- Financial blogs: Follow experts for advice on personal finance and car ownership.

- Financial advisors: Seek professional guidance on managing your finances and car-related expenses.

- Industry reports: Review reports on the automotive and financial sectors.

By proactively managing your car payment strategy, you can ensure that it remains a sustainable part of your overall financial plan, allowing you to achieve your long-term goals and secure your financial future. And with income-partners.net, you can explore innovative ways to boost your income and offset car expenses, turning your vehicle into a financial asset rather than a liability.

FAQ: Car Payments and Income

1. What percentage of my income should go to my car payment?

Ideally, your total monthly car expenses, including the car payment, insurance, and fuel, should not exceed 10-15% of your net monthly income to maintain financial stability.

2. How does my credit score affect my car payment?

A higher credit score typically results in lower interest rates on car loans, reducing the overall cost of the loan and the monthly payment.

3. What is the best loan term for a car loan?

The best loan term depends on your financial goals. Shorter loan terms have higher monthly payments but lower overall interest, while longer loan terms offer lower monthly payments but accumulate more interest over time.

4. Should I lease or buy a car?

Leasing may be a good option if you prefer driving a new car every few years and don’t mind mileage restrictions. Buying a used car can save you money on depreciation and insurance costs.

5. How can I lower my car insurance premium?

Strategies to lower your insurance premium include increasing your deductible, bundling policies, maintaining a clean driving record, and taking a defensive driving course.

6. What other expenses should I consider beyond the car payment?

Beyond the monthly car payment, consider expenses such as insurance, fuel, maintenance, and repairs.

7. How can I use my car to generate additional income?

Explore opportunities like ride-sharing services, delivery services, and car advertising to turn your car into an income-generating asset.

8. How can Income-Partners.Net help with car ownership?

Income-partners.net connects you with financial opportunities related to car ownership by providing a platform to find partners who need transportation or delivery services.

9. How often should I review my car payment strategy?

Regularly review your financial situation and adjust your car payment strategy as needed to maintain alignment with your goals.

10. What should I do if I lose my job and can’t afford my car payment?

Contact your lender immediately to discuss options such as loan modification, deferment, or repossession alternatives. Explore opportunities for additional income and reduce expenses to free up cash flow.

Ready to take control of your car expenses and explore new income opportunities? Visit income-partners.net today to discover how you can partner with others, leverage your assets, and achieve your financial goals. Connect with potential partners, explore diverse opportunities, and transform your car from a liability into an income-generating asset. Your journey to financial success starts now! Address: 1 University Station, Austin, TX 78712, United States. Phone: +1 (512) 471-3434. Website: income-partners.net.