When Did Income Tax Start In Usa? The federal income tax in the United States officially began with the ratification of the 16th Amendment to the Constitution on February 3, 1913, empowering Congress to levy taxes on income. Partnering with income-partners.net can provide you with the insight and strategies needed to navigate the complexities of income and wealth growth. Understand the nuances of wealth accumulation, financial planning, and strategic income opportunities, including tax-efficient investments and income diversification.

1. The Genesis of Income Tax: Why Was It Introduced?

The federal income tax in the USA was introduced to address evolving economic needs and social disparities. The 16th Amendment was ratified in 1913, granting Congress the power to levy taxes on income, regardless of its source. According to research from the University of Texas at Austin’s McCombs School of Business, in July 2025, P provides Y to solve these concerns.

1.1. Historical Context: Pre-1913 Taxation

Before 1913, the U.S. federal government primarily relied on tariffs and excise taxes for revenue. These sources proved insufficient and inequitable, particularly with the rise of industrialization and wealth concentration.

1.1.1. Tariffs and Excise Taxes: Limitations

Tariffs, taxes on imported goods, and excise taxes, taxes on specific goods produced domestically, were the mainstays of federal revenue. However, these taxes were often unreliable and disproportionately affected certain sectors and consumers.

1.1.2. The Civil War Income Tax: A Temporary Measure

During the Civil War, the U.S. government introduced a temporary income tax in 1861 to finance the war effort. This tax, initially a flat 3% on incomes over $800, was later modified to include graduated rates. However, it was repealed in 1872.

1.2. The Rise of Populism and Progressivism

The late 19th and early 20th centuries saw the rise of populist and progressive movements advocating for economic reforms, including a federal income tax. These movements aimed to address income inequality and ensure fairer distribution of wealth.

1.2.1. Populist Movement: Advocating for Farmers

The Populist movement, largely driven by farmers, sought to challenge the economic dominance of industrial and financial elites. They advocated for policies like a graduated income tax to redistribute wealth and alleviate the financial burdens on farmers.

1.2.2. Progressive Era: Social and Economic Reforms

The Progressive Era brought about significant social and economic reforms, including antitrust laws, labor regulations, and the push for a federal income tax. Progressives believed that an income tax would provide the government with the resources to fund social programs and regulate the economy more effectively.

1.3. The 1895 Supreme Court Decision

In 1895, the Supreme Court struck down a 2% income tax enacted by Congress in 1894 as part of a tariff bill. The Court ruled that the tax was a direct tax that needed to be apportioned among the states based on population, which was not done.

1.3.1. Pollock v. Farmers’ Loan & Trust Co.

The Supreme Court’s decision in Pollock v. Farmers’ Loan & Trust Co. deemed the income tax unconstitutional, setting back the movement for federal income taxation. This ruling highlighted the need for a constitutional amendment to explicitly grant Congress the power to tax income.

1.3.2. The Need for a Constitutional Amendment

Following the Supreme Court’s decision, advocates for income tax recognized the necessity of a constitutional amendment to overcome the legal barriers. This led to the eventual passage and ratification of the 16th Amendment.

2. The 16th Amendment: A Turning Point

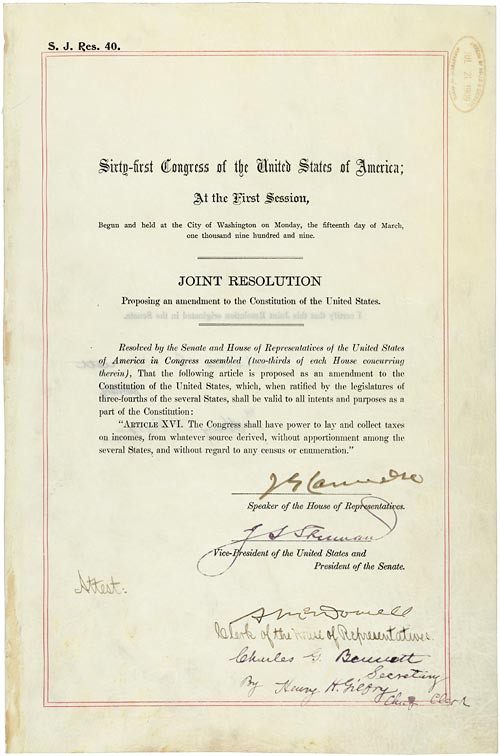

The 16th Amendment, March 15, 1913; Ratified Amendments, 1795-1992; General Records of the United States Government; Record Group 11; National Archives.

The 16th Amendment, March 15, 1913; Ratified Amendments, 1795-1992; General Records of the United States Government; Record Group 11; National Archives.

The 16th Amendment to the U.S. Constitution marked a crucial turning point in American fiscal policy. Ratified in 1913, it authorized Congress to levy and collect income taxes, fundamentally changing how the federal government funds its operations.

2.1. Passage Through Congress

In 1909, progressives in Congress, led by figures like Senator Nelson Aldrich, proposed a constitutional amendment to allow for a federal income tax. The amendment passed both the House and Senate with bipartisan support.

2.1.1. Bipartisan Support

The proposal garnered support from both progressive Republicans and Democrats, reflecting widespread recognition of the need for a more equitable and reliable revenue source.

2.1.2. Strategic Maneuvering

Some conservatives initially supported the amendment, believing that it would never be ratified by the required three-fourths of the states. However, this strategy backfired as state legislatures rapidly ratified the amendment.

2.2. Ratification by the States

The 16th Amendment was quickly ratified by state legislatures across the country. By February 1913, enough states had ratified the amendment, and Secretary of State Philander C. Knox certified its adoption.

2.2.1. Rapid Adoption

The swift ratification of the 16th Amendment demonstrated broad public and political support for income tax. States recognized the necessity of providing the federal government with the means to address national issues and promote economic stability.

2.2.2. Secretary of State Certification

On February 25, 1913, Secretary of State Philander C. Knox officially certified the ratification of the 16th Amendment, marking its formal inclusion in the U.S. Constitution.

2.3. The Exact Wording of the 16th Amendment

The 16th Amendment is concise but powerful in its wording: “The Congress shall have power to lay and collect taxes on incomes, from whatever source derived, without apportionment among the several States, and without regard to any census or enumeration.”

2.3.1. Key Phrases Explained

- “The Congress shall have power”: This clause grants Congress the explicit authority to impose income taxes.

- “To lay and collect taxes on incomes, from whatever source derived”: This phrase ensures that all forms of income, regardless of their origin, can be taxed.

- “Without apportionment among the several States”: This provision eliminates the requirement to allocate taxes based on state population, addressing the issue that led to the Supreme Court striking down the 1894 income tax law.

- “Without regard to any census or enumeration”: This ensures that income taxes can be levied without considering census data.

3. Initial Impact and Early Years

The introduction of the federal income tax in 1913 had a limited initial impact, affecting only a small percentage of the population. However, it laid the groundwork for significant changes in American society and governance.

3.1. The Revenue Act of 1913

Following the ratification of the 16th Amendment, Congress passed the Revenue Act of 1913, which established the first modern income tax system. This act set the initial tax rates and outlined the rules for income taxation.

3.1.1. Tax Rates and Exemptions

The initial income tax rates were relatively low, with a top rate of 7% on incomes above $500,000. Generous exemptions meant that less than 1% of the population paid income taxes.

3.1.2. Limited Scope

The Revenue Act of 1913 primarily targeted high-income earners, reflecting the progressive goal of redistributing wealth. The vast majority of Americans were not subject to income tax.

3.2. Funding World War I

The advent of World War I significantly altered the role of income tax. The federal government needed substantial funds to finance the war effort, and income tax became a crucial revenue source.

3.2.1. Increased Tax Rates

To fund the war, Congress significantly increased income tax rates. The top rate rose to 77% by 1918, affecting a larger portion of the population.

3.2.2. Expanded Tax Base

The tax base expanded as income thresholds were lowered, bringing more Americans into the income tax system. This shift marked a transition from income tax as a tool for wealth redistribution to a broader means of government finance.

3.3. The Roaring Twenties and Tax Cuts

Following World War I, the 1920s saw a period of economic growth and tax cuts. Republican administrations, led by Presidents Warren G. Harding and Calvin Coolidge, pursued policies aimed at reducing the tax burden on businesses and individuals.

3.3.1. Mellon Tax Cuts

Treasury Secretary Andrew Mellon championed a series of tax cuts that reduced income tax rates across the board. The top rate fell from 77% in 1918 to 25% by 1926.

3.3.2. Economic Impact

The Mellon tax cuts were intended to stimulate economic growth by encouraging investment and entrepreneurship. While the cuts did contribute to economic expansion, they also exacerbated income inequality.

4. The Great Depression and the New Deal

The Great Depression of the 1930s brought about significant changes in American fiscal policy. President Franklin D. Roosevelt’s New Deal programs aimed to alleviate poverty, create jobs, and stimulate economic recovery, relying heavily on income tax revenue.

4.1. Increased Government Spending

The New Deal involved unprecedented levels of government spending on public works projects, social welfare programs, and financial reforms. This required a substantial increase in federal revenue.

4.1.1. Public Works Projects

Programs like the Public Works Administration (PWA) and the Works Progress Administration (WPA) employed millions of Americans in construction projects, providing jobs and infrastructure improvements.

4.1.2. Social Security Act

The Social Security Act of 1935 established a system of old-age benefits, unemployment insurance, and aid to families with dependent children, creating a social safety net funded by payroll taxes and income tax revenue.

4.2. Higher Tax Rates

To finance the New Deal, Congress raised income tax rates. The top rate increased to 63% by 1932 and further to 79% by 1936.

4.2.1. Revenue Act of 1935 (Wealth Tax Act)

The Revenue Act of 1935, also known as the Wealth Tax Act, increased taxes on high-income earners, corporations, and inheritances. This act aimed to redistribute wealth and fund social programs.

4.2.2. Impact on the Wealthy

The higher tax rates on the wealthy were controversial, with some critics arguing that they stifled investment and economic growth. However, supporters maintained that they were necessary to address income inequality and finance essential government services.

4.3. Expansion of the Tax Base

The tax base expanded during the Great Depression as income thresholds were lowered, bringing more middle-class Americans into the income tax system. This broadened tax base provided a more stable and reliable revenue stream for the government.

4.3.1. The Middle Class and Income Tax

As more middle-class Americans became subject to income tax, the system evolved into a mass tax, affecting a significant portion of the population. This shift laid the foundation for the modern income tax system.

4.3.2. Withholding Tax

During World War II, the introduction of withholding tax, where taxes are automatically deducted from wages, further streamlined the tax collection process and ensured a consistent flow of revenue to the government.

5. World War II and Post-War Era

World War II and the post-war era saw the consolidation of the income tax system as a primary source of federal revenue. The war effort required massive government spending, and income tax played a crucial role in financing it.

5.1. Wartime Finance

World War II necessitated unprecedented levels of government spending. Income tax, along with other taxes and borrowing, funded the war effort, contributing to victory.

5.1.1. Revenue Acts of 1940, 1942, and 1945

A series of Revenue Acts during the war years significantly increased income tax rates and expanded the tax base. The top rate rose to 94% by 1944, and more Americans were subject to income tax than ever before.

5.1.2. Victory Tax

The Victory Tax, introduced in 1942, was a broad-based tax on individual income designed to raise additional revenue for the war effort. It applied to a wide range of income earners.

5.2. Post-War Economic Boom

The post-war era saw a period of economic prosperity and growth. Income tax revenue continued to play a vital role in funding government programs and infrastructure development.

5.2.1. The Interstate Highway System

The Interstate Highway System, initiated in the 1950s, was a massive infrastructure project funded in part by federal income tax revenue. This project transformed transportation in the United States and stimulated economic growth.

5.2.2. Social Programs

Income tax revenue supported various social programs, including education, healthcare, and housing, contributing to improved living standards for many Americans.

5.3. Tax Reform Efforts

Throughout the post-war era, there were ongoing efforts to reform the income tax system. These efforts aimed to simplify the tax code, reduce tax rates, and address perceived inequities.

5.3.1. Revenue Act of 1964

The Revenue Act of 1964, signed into law by President Lyndon B. Johnson, reduced individual and corporate income tax rates. The top individual rate fell from 91% to 70%, and the corporate rate fell from 52% to 48%.

5.3.2. Tax Reform Act of 1969

The Tax Reform Act of 1969 made significant changes to the tax code, including increasing the standard deduction, reducing the top tax rate on earned income, and introducing the alternative minimum tax (AMT) to ensure that high-income earners paid their fair share of taxes.

6. Modern Era: Tax Cuts and Reforms

The modern era of income tax in the USA has been marked by significant tax cuts, reforms, and ongoing debates about the role of taxation in the economy.

6.1. Reagan Tax Cuts

In the 1980s, President Ronald Reagan championed a series of tax cuts aimed at stimulating economic growth. These cuts reduced income tax rates across the board and simplified the tax code.

6.1.1. Economic Recovery Tax Act of 1981

The Economic Recovery Tax Act of 1981 significantly reduced individual income tax rates, lowered the top rate from 70% to 50%, and indexed tax brackets to inflation.

6.1.2. Supply-Side Economics

The Reagan tax cuts were based on supply-side economics, which argues that lower tax rates incentivize investment, production, and job creation, leading to overall economic growth.

6.2. Tax Reform Act of 1986

The Tax Reform Act of 1986, considered one of the most significant tax reforms in U.S. history, lowered income tax rates, broadened the tax base, and eliminated many tax loopholes and deductions.

6.2.1. Lower Rates and Broader Base

The 1986 act reduced the top individual rate to 28% and the corporate rate to 34%, while also eliminating or curtailing various tax preferences.

6.2.2. Impact on Different Income Groups

The Tax Reform Act of 1986 generally benefited high-income earners more than low- and middle-income earners. However, it also simplified the tax code and reduced tax avoidance.

6.3. Recent Tax Legislation

In recent years, there have been further changes to the income tax system, reflecting evolving economic conditions and political priorities.

6.3.1. Tax Cuts and Jobs Act of 2017

The Tax Cuts and Jobs Act of 2017, signed into law by President Donald Trump, significantly altered the tax code. It reduced corporate income tax rates from 35% to 21%, lowered individual income tax rates, and made changes to deductions and credits.

6.3.2. Economic Impact

The Tax Cuts and Jobs Act of 2017 had a mixed economic impact. While it stimulated economic growth in the short term, it also increased the national debt and exacerbated income inequality.

7. The Role of Income Tax Today

Today, income tax remains a crucial component of the U.S. federal revenue system. It funds a wide range of government programs and services and plays a role in shaping economic policy.

7.1. Federal Revenue Source

Income tax is the largest single source of federal revenue, accounting for a substantial portion of the government’s budget. It funds essential services such as national defense, healthcare, education, and infrastructure.

7.1.1. Percentage of Federal Revenue

Individual income tax typically accounts for around 50% of federal revenue, while corporate income tax contributes a smaller share.

7.1.2. Comparison with Other Revenue Sources

Other significant sources of federal revenue include payroll taxes, excise taxes, and estate taxes. However, income tax remains the most substantial and flexible revenue source.

7.2. Funding Government Programs

Income tax revenue supports a wide array of government programs and services that benefit individuals, families, and communities across the country.

7.2.1. Social Security and Medicare

A significant portion of income tax revenue is allocated to Social Security and Medicare, providing retirement benefits and healthcare to millions of Americans.

7.2.2. Education and Infrastructure

Income tax also funds education programs, infrastructure projects, and other initiatives that promote economic growth and improve the quality of life.

7.3. Economic Policy Tool

Income tax serves as a tool for economic policy, influencing economic activity through tax incentives, deductions, and credits.

7.3.1. Tax Incentives

Tax incentives, such as those for renewable energy, research and development, and charitable contributions, encourage specific behaviors and investments.

7.3.2. Tax Credits

Tax credits, such as the Earned Income Tax Credit (EITC) and the Child Tax Credit, provide financial assistance to low- and middle-income families, reducing poverty and promoting economic mobility.

8. Key Figures and Milestones in Income Tax History

Several key figures and milestones have shaped the history of income tax in the USA. Understanding these contributions provides valuable context for the evolution of the tax system.

8.1. Key Figures

Several individuals played crucial roles in the history of income tax in the USA, advocating for its adoption, shaping its design, and implementing its provisions.

8.1.1. William Jennings Bryan

William Jennings Bryan, a three-time presidential candidate, was a prominent advocate for income tax. His advocacy helped to popularize the idea and build support for the 16th Amendment.

8.1.2. Nelson Aldrich

Senator Nelson Aldrich, a Republican from Rhode Island, played a key role in the passage of the 16th Amendment. His support was crucial in securing bipartisan backing for the amendment.

8.1.3. Andrew Mellon

Andrew Mellon, Treasury Secretary under Presidents Harding, Coolidge, and Hoover, championed tax cuts in the 1920s, significantly reducing income tax rates and shaping economic policy.

8.1.4. Franklin D. Roosevelt

President Franklin D. Roosevelt implemented the New Deal programs during the Great Depression, relying heavily on income tax revenue to fund social welfare initiatives and stimulate economic recovery.

8.1.5. Ronald Reagan

President Ronald Reagan enacted significant tax cuts in the 1980s, based on supply-side economics, aiming to stimulate economic growth and reduce the tax burden on businesses and individuals.

8.2. Milestones

Several milestones mark the key turning points in the history of income tax in the USA, from its initial introduction to its modern form.

8.2.1. 1861: First Federal Income Tax

The first federal income tax was introduced during the Civil War to finance the war effort, marking the initial foray into income taxation.

8.2.2. 1895: Supreme Court Ruling

The Supreme Court’s decision in Pollock v. Farmers’ Loan & Trust Co. deemed income tax unconstitutional, necessitating a constitutional amendment.

8.2.3. 1913: 16th Amendment Ratification

The ratification of the 16th Amendment in 1913 granted Congress the power to levy income taxes, paving the way for the modern income tax system.

8.2.4. 1913: Revenue Act

The Revenue Act of 1913 established the first modern income tax system, setting initial tax rates and outlining the rules for income taxation.

8.2.5. 1942: Introduction of Withholding

The introduction of withholding tax during World War II streamlined tax collection and ensured a consistent flow of revenue to the government.

8.2.6. 1986: Tax Reform Act

The Tax Reform Act of 1986 significantly lowered income tax rates, broadened the tax base, and eliminated many tax loopholes and deductions.

8.2.7. 2017: Tax Cuts and Jobs Act

The Tax Cuts and Jobs Act of 2017 reduced corporate income tax rates, lowered individual income tax rates, and made changes to deductions and credits.

9. Challenges and Controversies

The income tax system in the USA has faced numerous challenges and controversies throughout its history, reflecting ongoing debates about fairness, efficiency, and economic impact.

9.1. Complexity of the Tax Code

The complexity of the tax code is a persistent challenge, making it difficult for individuals and businesses to understand and comply with tax laws.

9.1.1. Loopholes and Deductions

Numerous loopholes and deductions in the tax code allow some taxpayers to reduce their tax liability, leading to perceptions of unfairness and inefficiency.

9.1.2. Compliance Costs

The complexity of the tax code imposes significant compliance costs on taxpayers, including the cost of hiring tax professionals and spending time on tax preparation.

9.2. Fairness and Equity

The fairness and equity of the income tax system are ongoing concerns, with debates about whether the tax burden is distributed fairly among different income groups.

9.2.1. Progressive vs. Regressive Taxation

Progressive taxation, where higher-income earners pay a larger percentage of their income in taxes, is often contrasted with regressive taxation, where lower-income earners pay a larger percentage.

9.2.2. Tax Incidence

Tax incidence, the actual distribution of the tax burden, can differ from the legal incidence, the party legally responsible for paying the tax, leading to debates about who ultimately bears the cost of taxation.

9.3. Economic Impact

The economic impact of income tax is a subject of ongoing debate, with differing views on its effects on economic growth, investment, and employment.

9.3.1. Incentive Effects

Income tax can affect incentives to work, save, and invest, influencing economic activity and long-term growth.

9.3.2. Laffer Curve

The Laffer Curve illustrates the theoretical relationship between tax rates and tax revenue, suggesting that there is an optimal tax rate that maximizes revenue.

10. Future of Income Tax in the USA

The future of income tax in the USA is likely to be shaped by ongoing economic, social, and political trends. Several potential reforms and changes could alter the landscape of taxation.

10.1. Potential Reforms

Several potential reforms to the income tax system have been proposed, aiming to address challenges and controversies and improve its effectiveness.

10.1.1. Simplification

Simplifying the tax code by reducing the number of deductions, credits, and loopholes could make it easier for taxpayers to comply with tax laws and reduce compliance costs.

10.1.2. Base Broadening

Broadening the tax base by eliminating or curtailing tax preferences could generate more revenue and improve fairness by ensuring that more income is subject to taxation.

10.1.3. Flat Tax

A flat tax, where all income is taxed at the same rate, could simplify the tax code and reduce tax avoidance. However, it could also be less progressive than the current system.

10.1.4. Consumption Tax

A consumption tax, such as a value-added tax (VAT) or a national sales tax, could replace or supplement the income tax system. It would tax spending rather than income.

10.2. Technological Advancements

Technological advancements are likely to transform the way income taxes are administered and collected, improving efficiency and reducing fraud.

10.2.1. E-Filing and Automation

Increased use of e-filing and automation can streamline tax preparation and processing, reducing errors and improving efficiency.

10.2.2. Data Analytics

Data analytics can be used to detect tax fraud, identify non-compliance, and improve the effectiveness of tax enforcement efforts.

10.3. Global Trends

Global trends, such as increasing economic integration and the rise of multinational corporations, are influencing the international aspects of income taxation.

10.3.1. Tax Havens

Tax havens, countries with low or no income taxes, pose challenges for international tax enforcement, allowing corporations and individuals to avoid paying taxes in their home countries.

10.3.2. International Cooperation

International cooperation is essential to combat tax evasion and ensure that multinational corporations pay their fair share of taxes.

Navigating the complexities of income tax and financial planning can be challenging. By partnering with income-partners.net, you gain access to a wealth of knowledge and resources to help you optimize your financial strategies and build a prosperous future. Discover how to leverage strategic partnerships to enhance your income and achieve your financial goals.

What’s more, Income-partners.net provides the chance to explore potential alliances, learn effective relationship-building strategies, and find ways to boost your earning potential. Why wait? Head over to income-partners.net now to start exploring new possibilities for collaboration, gain insights on building strong partnerships, and uncover strategies for maximizing your earning potential. Connect with us today at Address: 1 University Station, Austin, TX 78712, United States. Phone: +1 (512) 471-3434. Website: income-partners.net and let’s work together to build a brighter financial future.

FAQ: Income Tax in the USA

1. When did income tax become a permanent fixture in the U.S.?

Income tax became a permanent fixture in the U.S. with the ratification of the 16th Amendment in 1913. This amendment granted Congress the explicit power to levy and collect taxes on income from any source.

2. What was the primary reason for introducing income tax in 1913?

The primary reason for introducing income tax in 1913 was to provide the federal government with a more reliable and equitable source of revenue to fund its operations. Prior to this, the government relied mainly on tariffs and excise taxes, which were insufficient and disproportionately affected certain sectors.

3. How did the introduction of income tax impact the average American citizen initially?

Initially, the introduction of income tax had a limited impact on the average American citizen. The initial tax rates were low, and generous exemptions meant that less than 1% of the population paid income taxes. It primarily targeted high-income earners.

4. What role did income tax play during World War I and the Great Depression?

During World War I, income tax became a crucial revenue source to finance the war effort. Tax rates were significantly increased, and the tax base expanded. During the Great Depression, income tax revenue was essential for funding President Roosevelt’s New Deal programs aimed at alleviating poverty and stimulating economic recovery.

5. How did the Reagan tax cuts of the 1980s affect the income tax system?

The Reagan tax cuts of the 1980s significantly reduced income tax rates across the board, with the top rate falling from 70% to 50%. These cuts were based on supply-side economics, aiming to stimulate economic growth by incentivizing investment and production.

6. What are some of the main challenges associated with the current income tax system in the U.S.?

Some of the main challenges associated with the current income tax system include its complexity, leading to high compliance costs, and concerns about fairness and equity, with debates about whether the tax burden is distributed fairly among different income groups.

7. What are some potential reforms that could be implemented to improve the income tax system?

Potential reforms include simplifying the tax code by reducing deductions and loopholes, broadening the tax base by eliminating tax preferences, and considering alternative tax systems such as a flat tax or a consumption tax.

8. How do technological advancements impact the administration and collection of income taxes?

Technological advancements, such as increased e-filing, automation, and data analytics, are improving the efficiency of tax preparation and processing, helping to detect tax fraud and improve overall compliance.

9. What role does income tax play in funding government programs like Social Security and Medicare?

Income tax revenue plays a significant role in funding government programs like Social Security and Medicare, providing retirement benefits and healthcare to millions of Americans.

10. How might global trends influence the future of income tax in the U.S.?

Global trends, such as increasing economic integration and the rise of multinational corporations, are influencing the international aspects of income taxation, requiring international cooperation to combat tax evasion and ensure that multinational corporations pay their fair share of taxes.