Reporting W9 income can seem daunting, but it’s a crucial part of being a self-employed individual or business owner. This guide, brought to you by income-partners.net, will break down the process and help you understand your tax obligations, ensuring you accurately report your earnings and avoid penalties. We’ll explore strategies for partnership and income enhancement, making tax season less stressful. Discover reliable methods for ensuring accuracy in your income declarations and exploring opportunities for financial collaboration.

1. Understanding the Basics of Form W-9 and Income Reporting

1.1. What is Form W-9 and Why is it Important?

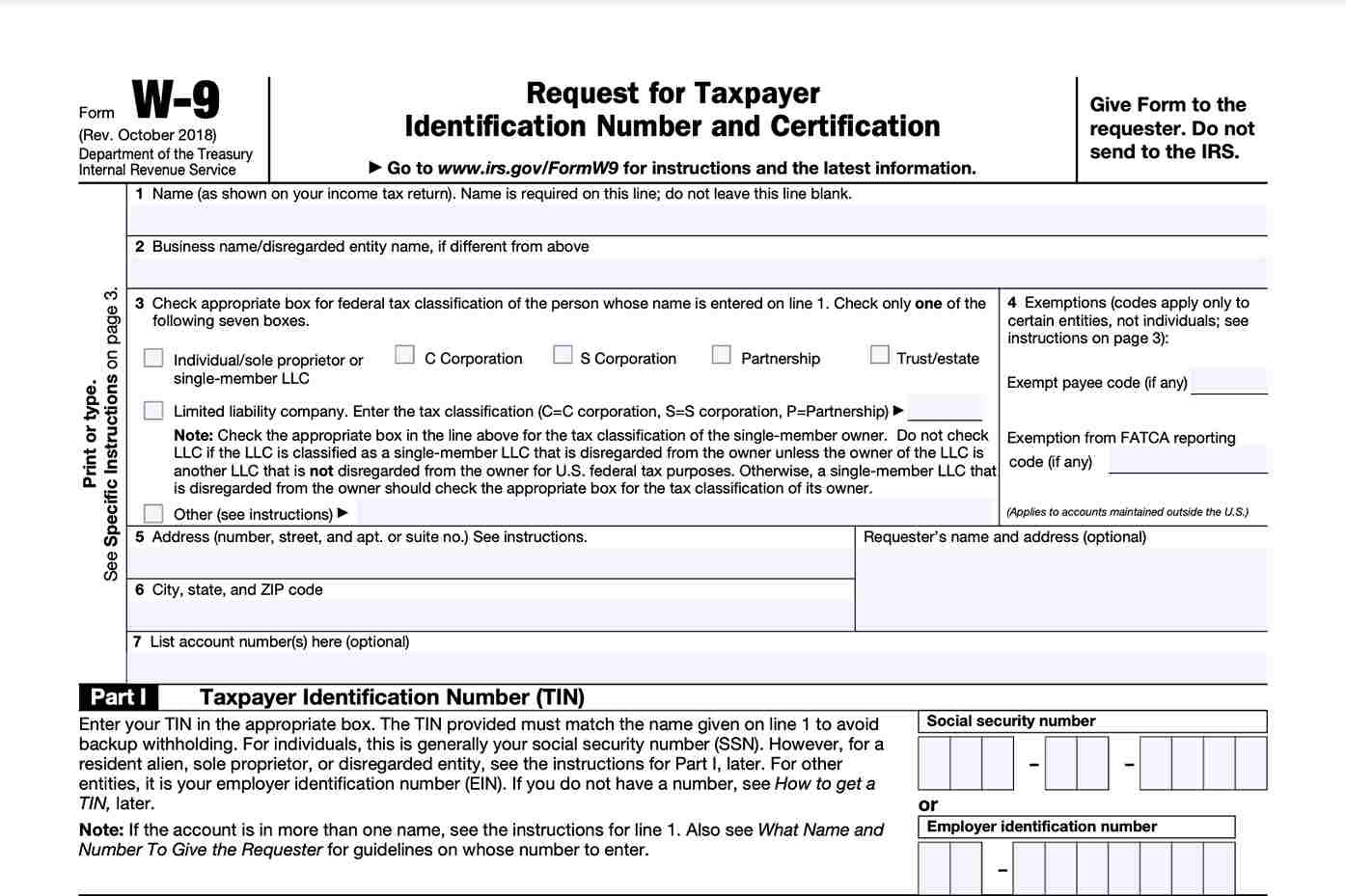

Form W-9, officially titled “Request for Taxpayer Identification Number (TIN) and Certification,” is a critical document for independent contractors, freelancers, and other non-employee service providers in the United States. It serves as a mechanism for businesses to gather essential information from individuals or entities they’ve paid, ensuring accurate reporting of income to the Internal Revenue Service (IRS). This information includes the recipient’s name, address, and Taxpayer Identification Number (TIN), which could be a Social Security Number (SSN) for individuals or an Employer Identification Number (EIN) for businesses.

The importance of Form W-9 lies in its role as the foundation for accurate income reporting. When a business pays an independent contractor or freelancer $600 or more in a tax year, they are required to report this income to the IRS using Form 1099-NEC (Nonemployee Compensation). The information provided on the W-9 is used to complete the 1099-NEC, ensuring that the income is correctly attributed to the recipient for tax purposes. According to the IRS, providing an accurate W-9 helps prevent potential issues such as backup withholding, where the payer is required to withhold 24% of the payment for taxes.

1.2. What Types of Income Are Typically Reported on Form 1099?

Form 1099 is used to report various types of income, and the specific type of 1099 form depends on the nature of the payment. Here are some of the most common types of income reported on 1099 forms:

- Nonemployee Compensation (Form 1099-NEC): This is used to report payments made to independent contractors, freelancers, and other self-employed individuals for services rendered. This is the most common form associated with Form W-9.

- Interest Income (Form 1099-INT): Banks and other financial institutions use this form to report interest earned on savings accounts, CDs, and other investments.

- Dividend Income (Form 1099-DIV): This form reports dividends and distributions from stocks, mutual funds, and other investments.

- Proceeds from Broker and Barter Exchange Transactions (Form 1099-B): This form reports sales of stocks, bonds, and other securities through a broker. It also covers transactions through barter exchanges.

- Rental Income (Form 1099-MISC): If you receive rental income from real estate, this will be reported on Form 1099-MISC.

- Royalties (Form 1099-MISC): Payments for royalties from copyrights, patents, and natural resources are reported on this form.

- Miscellaneous Income (Form 1099-MISC): Although the 1099-NEC is now used for independent contractor payments, the 1099-MISC can still report other types of miscellaneous income, such as prizes and awards, or payments made to attorneys.

Understanding which type of 1099 form applies to your income is crucial for accurate tax reporting. Each form has specific instructions and requirements, so it’s important to consult the IRS guidelines or a tax professional if you’re unsure which form to use.

1.3. Who Needs to Fill Out Form W-9?

Generally, anyone who performs services as an independent contractor or receives certain types of income, such as interest or dividends, may be required to complete Form W-9. Here’s a more detailed breakdown of who typically needs to fill out this form:

- Independent Contractors: If you work as a freelancer, consultant, or independent contractor and receive payments for your services, you’ll likely need to provide a completed W-9 to the businesses that pay you.

- Self-Employed Individuals: Sole proprietors and other self-employed individuals who receive income that is not subject to employment taxes (Social Security and Medicare) will also need to fill out Form W-9.

- Partnerships, LLCs, and Corporations: Businesses operating as partnerships, limited liability companies (LLCs), or corporations may need to complete Form W-9 when they provide services to other businesses.

- Recipients of Interest, Dividends, and Royalties: Individuals who receive interest income from bank accounts or investments, dividend income from stocks, or royalty payments may also be asked to complete a W-9.

- U.S. Citizens, Resident Aliens, and Other U.S. Persons: Form W-9 is primarily for U.S. citizens, resident aliens, and other “U.S. persons” as defined by the IRS. Non-resident aliens typically use Form W-8BEN instead.

Completing Form W-9 accurately is essential for ensuring that your income is properly reported to the IRS. Failure to provide a W-9 or providing inaccurate information can lead to backup withholding, where the payer is required to withhold a portion of your payments for taxes.

Form W-9

Form W-9

2. Step-by-Step Guide to Completing Form W-9

2.1. Downloading the Form and Gathering Necessary Information

The first step in completing Form W-9 is to download the latest version from the IRS website (IRS.gov). Using the most current version ensures that you are providing the correct information according to the latest IRS guidelines.

Before you start filling out the form, gather all the necessary information. This will help you complete the form accurately and efficiently. Here’s a list of what you’ll need:

- Full Legal Name: This should be the name as it appears on your Social Security card or other official identification documents.

- Business Name (if applicable): If you operate a business under a name different from your personal name, include your business name or “doing business as” (DBA) name.

- Federal Tax Classification: Determine your tax classification (Individual/sole proprietor, C Corporation, S Corporation, Partnership, LLC, Trust/estate) and be ready to check the appropriate box on the form.

- Exemptions (if applicable): If you are exempt from backup withholding or FATCA reporting, you’ll need to know the appropriate exemption codes.

- Address: Have your current mailing address ready, including street address, city, state, and ZIP code.

- Taxpayer Identification Number (TIN): This is either your Social Security Number (SSN) or Employer Identification Number (EIN), depending on your tax classification.

- Account Numbers (optional): If the payer requires you to provide account numbers, have those handy.

Having all this information readily available will make the process of completing Form W-9 much smoother and reduce the risk of errors.

2.2. Filling Out Each Section of the Form

Once you have downloaded the form and gathered all the necessary information, you can begin filling out each section. Here’s a detailed breakdown of how to complete each line:

- Line 1: Name: Enter your full legal name as it appears on your tax return. If you are a sole proprietor or single-member LLC, enter your individual name. If you operate under a business name, you can enter that on Line 2.

- Line 2: Business Name/Disregarded Entity Name, if different from above: If you have a business name or DBA name, enter it here. This is also where a single-member LLC that is disregarded as separate from its owner would enter the owner’s name.

- Line 3: Federal Tax Classification: Check the box that corresponds to your federal tax classification. The options are:

- Individual/sole proprietor or single-member LLC

- C Corporation

- S Corporation

- Partnership

- Trust/estate

- Limited liability company. (Enter the tax classification: P=Partnership, C=C corporation, or S=S corporation)

- Line 4: Exemptions (if applicable): Certain entities are exempt from backup withholding or FATCA reporting. If you qualify for an exemption, enter the appropriate code here. Refer to the IRS instructions for Form W-9 for a list of exemption codes. Individuals typically do not need to fill out this section.

- Line 5: Address (number, street, and apt. or suite no.): Enter your current mailing address.

- Line 6: City, state, and ZIP code: Enter the city, state, and ZIP code for your mailing address.

- Line 7: Account number(s) (optional): If the payer requires you to provide account numbers, enter them here. This is not always necessary.

- Part I: Taxpayer Identification Number (TIN): Enter your TIN in the appropriate box. For individuals and sole proprietors, this is typically your Social Security Number (SSN). For businesses, it’s usually the Employer Identification Number (EIN).

- Part II: Certification: Read the certification statement carefully. By signing the form, you are certifying that the information you have provided is accurate and that you are a U.S. citizen, resident alien, or other U.S. person. Sign and date the form. If you have been notified by the IRS that you are subject to backup withholding due to underreporting interest or dividends, you must cross out item 2 in the certification before signing.

Filling out each section accurately is crucial for avoiding issues with income reporting and potential penalties. Double-check all the information before submitting the form to the payer.

2.3. Common Mistakes to Avoid on Form W-9

Completing Form W-9 accurately is essential for ensuring that your income is properly reported and to avoid potential issues with the IRS. Here are some common mistakes to avoid:

- Incorrect Name: Make sure you enter your full legal name as it appears on your Social Security card or other official documents. Using a nickname or an abbreviated name can cause problems.

- Incorrect Taxpayer Identification Number (TIN): This is one of the most common errors. Ensure that you enter your Social Security Number (SSN) or Employer Identification Number (EIN) correctly. A mismatch between the TIN and the name can lead to backup withholding.

- Incorrect Federal Tax Classification: Choosing the wrong tax classification can have significant consequences. Make sure you understand your business structure and select the appropriate classification (Individual/sole proprietor, C Corporation, S Corporation, Partnership, LLC, etc.).

- Leaving Lines Blank: Fill out all applicable lines on the form. Leaving lines blank can cause confusion and may result in the payer requesting a new form.

- Incorrect Address: Providing an outdated or incorrect address can prevent you from receiving important tax documents, such as Form 1099-NEC.

- Forgetting to Sign and Date the Form: The certification section must be signed and dated for the form to be valid. Make sure you read the certification statement carefully before signing.

- Using an Old Version of the Form: Always download the latest version of Form W-9 from the IRS website to ensure that you are providing the correct information according to the current IRS guidelines.

Avoiding these common mistakes will help ensure that your Form W-9 is accurate and complete, which can save you time and trouble come tax season.

3. Understanding Your Tax Obligations as a W-9 Recipient

3.1. Reporting Income from Form 1099 on Your Tax Return

If you receive income reported on Form 1099-NEC, it is crucial to understand how to properly report this income on your tax return. Here’s a step-by-step guide:

- Gather Your 1099 Forms: Collect all the 1099-NEC forms you received from clients or businesses that paid you during the tax year. Each form will show the amount of income you earned from that payer.

- Determine Your Business Structure: Identify your business structure (sole proprietorship, LLC, S-corp, etc.) as this will determine which tax forms you need to use.

- Use Schedule C (Form 1040) for Sole Proprietorships: If you operate as a sole proprietorship, you’ll report your 1099-NEC income and related expenses on Schedule C (Form 1040), Profit or Loss from Business (Sole Proprietorship).

- Gross Income: Enter the total income reported on your 1099-NEC forms on Line 1 of Schedule C.

- Business Expenses: Deduct any eligible business expenses to arrive at your net profit or loss. Common business expenses include office supplies, travel, advertising, and professional fees.

- Net Profit or Loss: Calculate your net profit or loss by subtracting your total expenses from your gross income. This amount is then transferred to Form 1040.

- Use Form 1065 for Partnerships: If your business is a partnership, you’ll need to file Form 1065, U.S. Return of Partnership Income, to report the partnership’s income, deductions, and credits. Each partner will then receive a Schedule K-1, which reports their share of the partnership’s income or loss.

- Use Form 1120 or 1120-S for Corporations: If your business is a corporation, you’ll need to file either Form 1120, U.S. Corporation Income Tax Return (for C corporations), or Form 1120-S, U.S. Income Tax Return for an S Corporation (for S corporations).

- Calculate Self-Employment Tax: If you operate as a sole proprietorship or partnership and have a net profit of $400 or more, you’ll need to pay self-employment tax. This tax covers Social Security and Medicare taxes, which are typically withheld from employees’ paychecks. Use Schedule SE (Form 1040), Self-Employment Tax, to calculate the amount of self-employment tax you owe.

- File Your Tax Return: Include all necessary forms and schedules with your Form 1040 and file your tax return by the due date (typically April 15th, unless an extension is filed).

Properly reporting your 1099-NEC income is essential for complying with tax laws and avoiding penalties. Be sure to keep accurate records of your income and expenses throughout the year to make tax preparation easier.

3.2. Deducting Business Expenses to Reduce Taxable Income

One of the key benefits of being an independent contractor or self-employed individual is the ability to deduct business expenses, which can significantly reduce your taxable income. Here are some common business expenses that you may be able to deduct:

- Home Office Deduction: If you use a portion of your home exclusively and regularly for business, you may be able to deduct expenses related to that space, such as rent, mortgage interest, utilities, and insurance. According to the IRS, the home office must be your principal place of business or a place where you meet with clients or customers.

- Office Supplies: You can deduct the cost of office supplies, such as paper, pens, ink, and software.

- Travel Expenses: You can deduct expenses related to business travel, including transportation, lodging, and meals. However, the IRS typically only allows you to deduct 50% of meal expenses.

- Vehicle Expenses: If you use your vehicle for business purposes, you can deduct either the actual expenses (gas, oil, repairs, etc.) or take the standard mileage rate, which is set by the IRS each year.

- Advertising and Marketing Expenses: You can deduct the costs of advertising your business, including online ads, printed materials, and website development.

- Professional Fees: You can deduct fees paid to professionals such as accountants, lawyers, and consultants.

- Insurance: You may be able to deduct the cost of business insurance, such as liability insurance or professional indemnity insurance.

- Education: You can deduct expenses for education that maintains or improves your skills in your current business.

To deduct business expenses, you must keep accurate records, such as receipts, invoices, and bank statements. The IRS requires you to be able to substantiate your expenses with proper documentation. Consult with a tax professional to ensure that you are taking all eligible deductions and complying with IRS regulations.

3.3. Understanding Self-Employment Tax and Estimated Taxes

As an independent contractor or self-employed individual, you are responsible for paying self-employment tax, which covers Social Security and Medicare taxes. Employees typically have these taxes withheld from their paychecks, but as a self-employed individual, you must pay both the employer and employee portions of these taxes.

Self-employment tax is calculated on Schedule SE (Form 1040) and consists of two parts:

- Social Security Tax: 12.4% of your self-employment income up to the annual Social Security wage base (which is $168,600 for 2024).

- Medicare Tax: 2.9% of your total self-employment income.

In addition to self-employment tax, you may also need to pay estimated taxes throughout the year. Estimated taxes are payments you make to the IRS to cover your income tax liability. If you expect to owe $1,000 or more in taxes for the year, you are generally required to make estimated tax payments.

Estimated taxes are typically paid quarterly, and the due dates are:

- April 15

- June 15

- September 15

- January 15 of the following year

You can pay estimated taxes online, by mail, or by phone. The IRS provides several methods for calculating estimated taxes, including using the prior year’s tax return or estimating your income and deductions for the current year.

Failing to pay estimated taxes or underpaying your estimated taxes can result in penalties from the IRS. It’s important to accurately estimate your income and tax liability and make timely payments to avoid these penalties. Consult with a tax professional to determine the best approach for managing your self-employment tax and estimated tax obligations.

4. Optimizing Your Financial Strategy as a W-9 Recipient

4.1. Setting Up a Retirement Plan for Self-Employed Individuals

As a self-employed individual, setting up a retirement plan is a crucial step in securing your financial future. Unlike traditional employees who often have access to employer-sponsored retirement plans, you are responsible for creating your own retirement savings strategy. Here are some popular retirement plan options for self-employed individuals:

- Solo 401(k): A Solo 401(k) allows you to contribute both as an employee and as an employer, offering the potential for significant tax-deferred savings. You can contribute up to $23,000 as an employee in 2024, plus an additional employer contribution of up to 25% of your net adjusted self-employment income. The maximum total contribution for 2024 is $69,000.

- Simplified Employee Pension (SEP) IRA: A SEP IRA is a simple and flexible retirement plan that allows you to contribute up to 20% of your net adjusted self-employment income, with a maximum contribution of $69,000 for 2024. SEP IRAs are easy to set up and maintain, making them a popular choice for self-employed individuals.

- Savings Incentive Match Plan for Employees (SIMPLE) IRA: A SIMPLE IRA allows you to contribute up to $16,000 in 2024, with an additional employer matching contribution. SIMPLE IRAs are generally less complex than Solo 401(k)s, but they may have lower contribution limits.

- Traditional IRA: While not exclusively for the self-employed, a Traditional IRA allows you to make tax-deductible contributions and defer taxes on your investment earnings until retirement. However, contributions may not be fully deductible if you are also covered by a retirement plan at work.

- Roth IRA: A Roth IRA allows you to make contributions with after-tax dollars, but your investment earnings and withdrawals in retirement are tax-free. Roth IRAs can be a good option if you expect to be in a higher tax bracket in retirement.

Choosing the right retirement plan depends on your individual circumstances, including your income, age, and risk tolerance. Consider consulting with a financial advisor to determine the best retirement savings strategy for your needs.

4.2. Strategies for Managing Cash Flow and Budgeting

Managing cash flow and budgeting effectively is essential for the financial stability of any self-employed individual or business. Here are some strategies to help you manage your cash flow and budget effectively:

- Track Your Income and Expenses: Use accounting software, spreadsheets, or mobile apps to track your income and expenses. This will give you a clear picture of where your money is coming from and where it’s going.

- Create a Budget: Develop a budget that allocates your income to various expense categories, such as business expenses, personal expenses, taxes, and savings.

- Separate Business and Personal Finances: Keep your business and personal finances separate to make it easier to track your business income and expenses. Open a separate bank account and credit card for your business.

- Set Financial Goals: Establish clear financial goals, such as saving for retirement, paying off debt, or purchasing equipment. This will help you stay motivated and focused on managing your finances effectively.

- Monitor Your Cash Flow Regularly: Review your cash flow statements regularly to identify trends, potential problems, and opportunities for improvement.

- Build an Emergency Fund: Set aside funds in a savings account to cover unexpected expenses or periods of low income. Aim to have at least three to six months’ worth of living expenses in your emergency fund.

- Invoice Promptly: Send invoices to your clients or customers promptly to ensure timely payment. Consider offering incentives for early payment or charging late fees for overdue invoices.

- Negotiate Payment Terms: Negotiate favorable payment terms with your suppliers and vendors. This can help you manage your cash flow and reduce your expenses.

- Plan for Taxes: Set aside funds each month to cover your estimated tax payments. This will help you avoid surprises at tax time.

- Regularly Review and Adjust Your Budget: Review your budget regularly and make adjustments as needed to reflect changes in your income, expenses, or financial goals.

By implementing these strategies, you can gain greater control over your finances and ensure the long-term financial health of your business.

4.3. Exploring Opportunities for Financial Partnerships and Collaborations

Financial partnerships and collaborations can provide valuable resources, expertise, and opportunities for growth. Here are some ways to explore and leverage financial partnerships:

- Strategic Alliances: Form strategic alliances with other businesses or professionals in your industry. This can help you expand your reach, access new markets, and share resources. According to a study by Harvard Business Review, strategic alliances can increase revenue by as much as 20%.

- Joint Ventures: Collaborate with other businesses on specific projects or ventures. This can allow you to pool resources, share risks, and access specialized expertise.

- Referral Partnerships: Partner with other businesses to refer clients or customers to each other. This can be a cost-effective way to generate new leads and grow your business.

- Investor Partnerships: Seek out investors who can provide capital and expertise to help you grow your business. This can be a good option if you need funding to expand your operations or develop new products or services.

- Mentorship: Seek guidance from experienced entrepreneurs or business professionals who can provide valuable insights and advice.

- Networking: Attend industry events, join professional organizations, and participate in online communities to network with other professionals and potential partners.

- Financial Consulting: Work with a financial consultant who can help you develop a financial plan, manage your cash flow, and make informed investment decisions.

- Collaborative Marketing: Partner with other businesses to conduct joint marketing campaigns or promotions. This can help you reach a wider audience and increase your brand awareness.

By actively seeking out and leveraging financial partnerships, you can unlock new opportunities for growth and success. Remember to carefully evaluate potential partners and ensure that the partnership aligns with your goals and values.

5. Avoiding Common Pitfalls and Staying Compliant

5.1. Record-Keeping Best Practices for W-9 Recipients

Maintaining accurate and organized records is crucial for W-9 recipients to ensure compliance with tax laws and to effectively manage their finances. Here are some record-keeping best practices:

- Keep All 1099 Forms: Store all 1099 forms you receive in a safe and organized manner. These forms are essential for accurately reporting your income on your tax return.

- Maintain Detailed Expense Records: Keep detailed records of all your business expenses, including receipts, invoices, and bank statements. These records are necessary to support your deductions and reduce your taxable income.

- Use Accounting Software: Consider using accounting software, such as QuickBooks or Xero, to track your income and expenses. These programs can help you automate your record-keeping and generate reports.

- Separate Business and Personal Records: Keep your business and personal records separate to avoid confusion and to make it easier to track your business income and expenses.

- Digitize Your Records: Scan or photograph your paper records and store them electronically. This will help you save space and ensure that your records are accessible and secure.

- Back Up Your Records: Regularly back up your electronic records to protect against data loss. Store your backups in a secure location, such as a cloud storage service or an external hard drive.

- Organize Your Records: Organize your records in a logical and consistent manner. Use folders, labels, and naming conventions to make it easy to find the information you need.

- Retain Your Records: The IRS generally recommends keeping your tax records for at least three years from the date you filed your return or two years from the date you paid the tax, whichever is later. However, it’s a good idea to keep your records for longer periods, especially if you have complex financial transactions.

- Document All Transactions: Document all your business transactions, including sales, purchases, and payments. This will help you track your cash flow and prepare your tax return.

- Review Your Records Regularly: Review your records regularly to identify errors, inconsistencies, or missing information. This will help you catch problems early and avoid costly mistakes.

By following these record-keeping best practices, you can ensure that you have accurate and complete records to support your tax filings and manage your finances effectively.

5.2. Understanding Backup Withholding and How to Avoid It

Backup withholding is a system where payers are required to withhold a portion of your payments for taxes. This typically occurs when you have not provided a Taxpayer Identification Number (TIN) or if the IRS believes that you have underreported your income in the past. Here’s what you need to know about backup withholding and how to avoid it:

- What is Backup Withholding? Backup withholding is a flat 24% rate that is withheld from your payments and sent to the IRS. This is in place to ensure that taxes are paid on income that might otherwise go unreported.

- Why Does Backup Withholding Occur? Backup withholding can occur for several reasons:

- You failed to provide a TIN to the payer.

- The TIN you provided is incorrect.

- The IRS has notified the payer that you are subject to backup withholding because you have underreported your income in the past.

- You failed to certify that you are not subject to backup withholding.

- How to Avoid Backup Withholding: You can avoid backup withholding by taking the following steps:

- Provide your correct TIN to the payer when requested.

- Ensure that the name on your W-9 matches the name on your Social Security card or other official documents.

- Certify on Form W-9 that you are not subject to backup withholding.

- If you have been notified by the IRS that you are subject to backup withholding, contact the IRS to resolve the issue.

- What to Do if You Are Subject to Backup Withholding: If you are subject to backup withholding, you will receive a 1099 form showing the amount of taxes that were withheld. You can claim this amount as a credit on your tax return.

- How to Stop Backup Withholding: Once you have resolved the issue that caused the backup withholding, you can request that the payer stop withholding taxes from your payments. You may need to provide documentation from the IRS to support your request.

By understanding backup withholding and taking steps to avoid it, you can ensure that you receive the full amount of your payments and avoid unnecessary complications with the IRS.

5.3. Staying Up-to-Date with Tax Law Changes and IRS Guidance

Tax laws and IRS guidance are constantly evolving, so it’s important to stay informed to ensure that you are complying with the latest regulations. Here are some tips for staying up-to-date with tax law changes:

- Subscribe to IRS Publications: Sign up to receive email updates from the IRS on tax law changes, new guidance, and important announcements.

- Follow Tax Professionals and Organizations: Follow tax professionals, organizations, and blogs on social media to stay informed about tax law changes and updates.

- Attend Tax Seminars and Webinars: Attend tax seminars and webinars to learn about the latest tax laws and regulations. These events are often hosted by tax professionals, accounting firms, and business organizations.

- Consult with a Tax Professional: Work with a tax professional who can provide personalized advice and guidance on tax planning and compliance.

- Read IRS Publications and Notices: Review IRS publications, notices, and other guidance documents to understand the latest tax laws and regulations.

- Use Tax Software: Use tax software that is updated with the latest tax laws and regulations. This can help you prepare your tax return accurately and avoid errors.

- Join Professional Organizations: Join professional organizations, such as the National Association for the Self-Employed (NASE) or the American Institute of CPAs (AICPA), to stay informed about tax law changes and other important issues.

- Monitor Legislation: Monitor pending legislation that could affect tax laws. This can help you anticipate changes and plan accordingly.

By staying up-to-date with tax law changes and IRS guidance, you can ensure that you are complying with the latest regulations and avoiding costly mistakes.

Form W-9

6. Leveraging Income-Partners.Net for Business Growth

6.1. How Income-Partners.Net Helps You Find Strategic Partnerships

income-partners.net provides a platform for finding strategic partnerships to help you grow your business and increase your income. Here’s how it works:

- Extensive Network: income-partners.net connects you with a diverse network of businesses and professionals across various industries.

- Targeted Search: Use the platform’s search filters to find partners who align with your business goals, target market, and industry.

- Detailed Profiles: View detailed profiles of potential partners, including their experience, expertise, and business objectives.

- Direct Communication: Communicate directly with potential partners through the platform’s messaging system.

- Partnership Opportunities: Discover partnership opportunities, such as joint ventures, strategic alliances, and referral programs.

- Industry Insights: Access industry insights and trends to identify potential partnership opportunities.

- Collaboration Tools: Use the platform’s collaboration tools to manage your partnerships and track your progress.

- Expert Advice: Receive expert advice on building successful partnerships and maximizing your income.

- Community Support: Connect with other members of the income-partners.net community to share ideas, insights, and best practices.

- Success Stories: Learn from success stories of other businesses who have used income-partners.net to find strategic partnerships and grow their businesses.

By leveraging income-partners.net, you can find the right partners to help you achieve your business goals and increase your income.

6.2. Building Effective Partnership Agreements

A well-crafted partnership agreement is essential for ensuring the success of any business partnership. Here are some key elements to include in your partnership agreement:

- Scope of Work: Clearly define the scope of work for each partner, including their responsibilities, duties, and obligations.

- Compensation: Specify how each partner will be compensated, including salary, profit sharing, or other forms of remuneration.

- Decision-Making Process: Outline the decision-making process for the partnership, including how decisions will be made and who has the authority to make them.

- Dispute Resolution: Include a dispute resolution process to address any conflicts that may arise between partners.

- Term and Termination: Specify the term of the partnership and the conditions under which it can be terminated.

- Ownership and Equity: Define the ownership and equity stake of each partner in the business.

- Confidentiality: Include a confidentiality clause to protect the business’s trade secrets and other sensitive information.

- Non-Compete: Include a non-compete clause to prevent partners from competing with the business after they leave the partnership.

- Intellectual Property: Specify how intellectual property will be owned and managed by the partnership.

- Liability: Address the liability of each partner in the event of legal claims or other liabilities.

- Amendments: Include a process for amending the partnership agreement as needed.

A well-crafted partnership agreement can help prevent misunderstandings, resolve disputes, and ensure that the partnership operates smoothly and successfully.

6.3. Maximizing Your Income Through Strategic Collaborations

Strategic collaborations can be a powerful way to maximize your income and grow your business. Here are some strategies for maximizing your income through strategic collaborations:

- Identify Complementary Businesses: Partner with businesses that offer complementary products or services to expand your reach and increase your customer base.

- Develop Joint Products or Services: Collaborate with other businesses to develop new products or services that can be offered to a wider audience.

- Cross-Promote Each Other’s Businesses: Cross-promote each other’s businesses to increase brand awareness and generate new leads.

- Share Resources and Expertise: Share resources and expertise with other businesses to reduce costs and improve efficiency.

- Create Referral Programs: Create referral programs to incentivize customers to refer new business to your partners.

- Joint Marketing Campaigns: Conduct joint marketing campaigns to reach a wider audience and generate more leads.

- Bundle Products or Services: Bundle your products or services with those of your partners to create more attractive offers for customers.

- Co-Create Content: Co-create content, such as blog posts, videos, or webinars, to attract new audiences and generate leads.

- Host Joint Events: Host joint events, such as workshops, conferences, or webinars, to engage with customers and partners.

- Collaborate on Research and Development: Collaborate on research and development projects to create innovative products or services.

By leveraging strategic collaborations, you can maximize your income, grow your business, and achieve your financial goals.

7. Frequently Asked Questions (FAQs) About Reporting W9 Income

7.1. What Happens if I Don’t Report My W9 Income?

If you don’t report your W9 income, the IRS may assess penalties, including interest and late filing fees. According to IRS guidelines, failure to report income can lead to an audit, where the IRS examines your financial records to verify your income and expenses. In severe cases, it can result in legal consequences.

7.2. Can I File an Extension for My Taxes if I’m Waiting on a 1099 Form?

Yes, you can file an extension for your taxes if you’re waiting on a 1099 form. Filing Form 4868, Application for Automatic Extension of Time to File U.S. Individual Income Tax Return, gives you an additional six months to file your return. However, it’s essential to estimate your tax liability and pay any taxes due by the original filing deadline to avoid penalties.

7.3. What is the Difference Between a W-9 and a W-4 Form?

A W-9 form is used by businesses to collect information from independent contractors, while a W-4 form is used by employees to inform their employer how much tax to withhold from their paycheck.