Can Passive Losses Offset Active Income? Yes, in certain situations passive losses can offset active income, especially within the context of real estate activities. This article, brought to you by income-partners.net, explores the nuances of passive activity loss (PAL) rules and provides strategies for maximizing tax benefits through strategic partnerships. Understanding these rules can significantly impact your tax planning and financial outcomes. Let’s delve into how you can leverage passive losses to your advantage and connect with potential partners to optimize your income. We’ll explore active participation, rental real estate, and loss deductions.

1. Understanding Passive Activity Loss (PAL) Rules

Passive Activity Loss (PAL) rules are designed to prevent taxpayers from using losses from passive activities to offset income from active businesses or investments. It’s crucial to grasp these rules to navigate tax planning effectively. These regulations dictate how losses from passive ventures, like rental properties, can be used to reduce your overall tax liability. Knowing the ins and outs of PALs is vital for anyone involved in real estate or other passive income streams.

1.1 What Constitutes Passive Activity?

A passive activity generally includes any trade or business in which the taxpayer does not materially participate. According to research from the University of Texas at Austin’s McCombs School of Business, real estate rentals are typically considered passive, regardless of material participation. This classification has significant implications for how losses from these activities can be used to offset other income. It’s essential to determine whether your involvement meets the criteria for material participation.

1.2 General Rule: Passive Losses vs. Active Income

The general rule is that passive losses can only offset passive income. This means that if you have a loss from a rental property, you can only use it to offset income from other passive activities, such as another rental property or a business in which you don’t materially participate. The IRS provides detailed guidelines on what constitutes material participation. Understanding this offset mechanism is crucial for managing your tax obligations.

1.3 Exceptions to the Rule

There are a few notable exceptions to this rule, particularly for rental real estate activities. These exceptions allow certain taxpayers to deduct passive losses against active income, providing significant tax relief. These exceptions are designed to support individuals who actively manage their rental properties. Let’s explore these exceptions in detail.

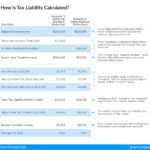

2. The $25,000 Rental Real Estate Loss Allowance

One significant exception is the $25,000 rental real estate loss allowance. This provision allows qualifying individuals and estates to offset up to $25,000 of nonpassive income with rental real estate losses and credits. It’s a valuable tool for those who actively participate in managing their rental properties. This allowance can significantly reduce your tax burden.

2.1 Qualification Requirements for the Allowance

To qualify for the $25,000 deduction, the taxpayer must own at least 10% of the value of all interests in the activity at all times during the tax year. They must also actively participate in the operations of the rental property. Meeting these criteria allows you to take advantage of this valuable tax break. Ownership and active participation are the key elements.

2.2 Ownership Test: 10% Ownership Rule

The ownership test requires that you own at least 10% of the value of all interests in the rental real estate activity. This ensures that the benefit is targeted toward individuals with a significant stake in the property. Spousal interests are also included when measuring an individual’s ownership. Maintaining this level of ownership is crucial for eligibility.

2.3 Active Participation: What Does It Mean?

Active participation is a less stringent standard than material participation. It doesn’t require regular, continuous, and substantial involvement in the operations. Rather, the taxpayer must participate in a significant way, such as making management decisions or arranging for others to provide services. This includes approving new tenants, setting rental policies, and approving capital expenditures. Understanding this standard is vital for claiming the allowance.

2.4 Examples of Active Participation

Consider the following examples to better understand active participation:

Example 1: Managing the Property

F lives in Texas but owns 100% of a rental property in Arkansas. He receives all rent through the mail and hasn’t been to Arkansas to see the rental property for more than a year. If problems with the property occur or repairs are needed, he hires someone in Arkansas to perform the work. F continues to set the policy on rentals and approves tenants when vacancies occur. F actively participates in this rental property because he owns at least 10% of the real estate rental activity, makes all management decisions, and provides for others to perform services.

Example 2: Silent Partner Fails the Test

F and his cousin, D, are equal shareholders in an S corporation that owns an apartment building in Las Vegas. D lives in Las Vegas, while F lives in Dallas. D makes all management decisions regarding the rental property. He inspects it regularly and collects all rents. F has had no contact with the property since he invested in it several years ago. Both F and D meet the ownership test, but only D actively participates because he makes all management decisions.

2.5 Limited Partnership Exclusion

A taxpayer who owns rental real estate through an interest in a limited partnership will not be considered to actively participate in the rental real estate activity for the $25,000 offset. This exclusion is important to note for those involved in limited partnerships. Understanding this limitation is crucial for planning.

2.6 Phaseout of the $25,000 Deduction

The $25,000 maximum amount that can be deducted from nonpassive income is reduced by 50% of the amount by which the taxpayer’s modified adjusted gross income (AGI) exceeds $100,000. Therefore, the $25,000 amount is totally phased out when the taxpayer’s modified AGI reaches $150,000. This phaseout can impact the amount of the deduction you can claim.

2.7 What is Modified Adjusted Gross Income (AGI)?

Modified AGI is AGI calculated without considering several items, including:

- Individual retirement account deductions

- Interest deductions on higher education loans

- Taxable Social Security benefits

- Any passive losses allowed under the exception for real estate professionals

- The Sec. 250 deductions for foreign-derived intangible income and global intangible low-taxed income

- Any overall loss from a publicly traded partnership

Also added back to income is:

- The Sec. 164(f) deduction for one-half of self-employment tax

- Income excluded for U.S. savings bond interest used for higher education expenses

- Any tax-free Olympic and Paralympic medals and prize money

- Amounts received from employer-provided adoption-assistance programs

Understanding what constitutes modified AGI is vital for calculating the phaseout.

2.8 Strategies to Maximize the $25,000 Allowance

Because the $25,000 loss allowance begins being phased out when modified AGI exceeds $100,000 and is completely phased out when modified AGI exceeds $150,000, taxpayers with income within or around this range can maximize the allowance with careful tax planning. Strategies that reduce AGI may help increase the allowable deduction when taxpayers are subject to the phaseout.

Deductible contributions to Keogh and simplified employee pension (SEP) retirement plans may help self-employed taxpayers reduce their AGI. Investing in tax-exempt securities or investments that defer income to later years will reduce AGI. Similarly, self-employed taxpayers (using the cash method) can shift income from one year to another by timing when they bill and collect revenue.

3. Real Estate Professionals and the Passive Loss Rules

Another exception to the passive loss rules applies to real estate professionals. If you qualify as a real estate professional, you may be able to deduct rental real estate losses against your active income without the limitations imposed by the passive loss rules. This can provide significant tax advantages. Let’s explore the criteria for qualifying as a real estate professional.

3.1 Who Qualifies as a Real Estate Professional?

To qualify as a real estate professional, you must meet specific requirements related to your involvement in real property trades or businesses. This typically involves spending a significant amount of time and effort in real estate activities. The IRS has specific guidelines for determining whether you meet these criteria. It’s important to document your activities thoroughly.

3.2 Material Participation in Rental Real Estate

If you qualify as a real estate professional, you must also materially participate in the rental real estate activity. This means you must be involved in the operations of the activity on a regular, continuous, and substantial basis. Meeting this standard allows you to deduct losses against active income. Material participation is a key element for real estate professionals.

3.3 How to Prove Material Participation

Proving material participation requires maintaining detailed records of your involvement in the rental real estate activity. This includes documenting the time you spend on various tasks, such as managing the property, making repairs, and handling tenant issues. Accurate documentation is crucial for substantiating your claims. Keep thorough records of your activities.

4. Contributing Rental Loss Activities to Profitable Closely Held C Corporations

Individuals must apply the PAL rules to activities they hold personally and in passthrough entities. The passive loss rules also apply to activities held by closely held corporations and personal service corporations (PSCs). However, closely held corporations are afforded more favorable treatment.

4.1 Advantages of Closely Held C Corporations

Closely held corporations (other than PSCs) can use passive losses to offset net active income, but not portfolio income. Thus, these corporations don’t have to generate passive activity income before passive losses can be deducted. This provides a significant advantage for businesses with passive losses.

4.2 Definition of a Closely Held Corporation

When applying the PAL rules, a closely held corporation is a C corporation that at any time during the last half of the tax year is owned more than 50% in value by five or fewer individuals. Also, the corporation must not qualify as a PSC. Understanding this definition is crucial for determining eligibility.

4.3 Example: Shifting Passive Activity Losses

Consider the following example:

J owns a 50% interest in a general partnership that owns a 50-unit apartment complex. J’s share of the partnership’s rental loss is about $50,000 a year. He actively participates in the management of the property. He has no other passive income or losses. J also owns 100% of T Co., a manufacturer of specialty sporting goods. He is a full-time employee of T Co., which operates as a C corporation. In the current year, J anticipates having AGI of $200,000 ($175,000 salary and $25,000 interest and dividend income). T Co. will have current-year net income of approximately $250,000.

J is unable to benefit from the special $25,000 rental real estate loss allowance since his modified AGI exceeds the phaseout threshold of $150,000. This situation is likely to continue in the future, so the losses from the apartment complex will be suspended under the PAL rules.

In this situation, J might find it advantageous to contribute his partnership interest in the apartment complex to T Co., using a Sec. 351 tax-free exchange. Although the corporation is closely held and subject to the PAL rules, it can offset net active income with passive losses. This enables the passive losses to be deducted currently.

4.4 Considerations Before Transferring Passive Activities

Before transferring passive activities to closely held corporations, taxpayers must consider the tax consequences of conducting business in C corporations, such as double taxation. Understanding these consequences is vital for making informed decisions.

5. Strategic Partnerships for Maximizing Income and Offsetting Losses

Forming strategic partnerships can be a powerful way to maximize income and offset losses. By collaborating with others, you can leverage their expertise, resources, and networks to achieve your financial goals. Strategic partnerships can open up new opportunities and reduce your overall tax burden.

5.1 Types of Strategic Partnerships

There are various types of strategic partnerships you can consider, including:

- Joint Ventures: Collaborating on a specific project or venture.

- Equity Partnerships: Sharing ownership and profits in a business.

- Referral Partnerships: Exchanging leads and referrals.

- Marketing Partnerships: Co-branding and cross-promotional activities.

Each type of partnership offers unique benefits and opportunities.

5.2 Benefits of Forming Partnerships

Forming partnerships can provide numerous benefits, such as:

- Increased Income: Access to new markets and customers.

- Reduced Risk: Sharing the financial burden of investments.

- Access to Expertise: Leveraging the skills and knowledge of others.

- Tax Advantages: Utilizing passive losses to offset active income.

These benefits can significantly enhance your financial position.

5.3 How to Find the Right Partners

Finding the right partners is crucial for the success of any strategic alliance. Consider the following tips:

- Define Your Goals: Clearly identify what you hope to achieve through the partnership.

- Research Potential Partners: Look for individuals or businesses with complementary skills and values.

- Network: Attend industry events and connect with potential partners.

- Due Diligence: Thoroughly vet potential partners before entering into any agreements.

Finding the right fit is essential for a successful partnership.

5.4 Structuring Partnership Agreements

A well-structured partnership agreement is essential for outlining the rights and responsibilities of each partner. The agreement should address key issues such as:

- Profit and Loss Sharing: How profits and losses will be divided.

- Decision-Making Authority: Who has the authority to make decisions.

- Capital Contributions: How much capital each partner will contribute.

- Dispute Resolution: How disagreements will be resolved.

A clear and comprehensive agreement can prevent misunderstandings and conflicts.

6. Utilizing Income-Partners.net for Strategic Collaborations

Income-partners.net offers a unique platform for individuals and businesses to connect and form strategic partnerships. The site provides a wealth of information and resources to help you find the right partners and maximize your income potential. Leveraging this platform can significantly enhance your partnership opportunities.

6.1 Resources Available on Income-Partners.net

Income-partners.net offers a variety of resources, including:

- Partner Directory: A comprehensive directory of potential partners in various industries.

- Articles and Guides: Informative articles and guides on strategic partnerships and tax planning.

- Networking Events: Opportunities to connect with potential partners at industry events.

- Expert Advice: Access to expert advice on structuring partnership agreements and maximizing tax benefits.

These resources are designed to help you succeed in your partnership endeavors.

6.2 How to Connect with Potential Partners

Connecting with potential partners on income-partners.net is easy. Simply create a profile, search the partner directory, and reach out to individuals or businesses that align with your goals. The platform provides tools for effective communication and collaboration. Building your network is key to finding the right partners.

6.3 Success Stories from Income-Partners.net

Numerous individuals and businesses have found success through strategic partnerships formed on income-partners.net. These success stories demonstrate the power of collaboration and the potential for increased income and tax benefits. Learning from these stories can inspire your own partnership endeavors.

7. Understanding the Tax Implications of Partnerships

Partnerships have unique tax implications that you need to be aware of. Understanding these implications is crucial for maximizing your tax benefits and avoiding potential pitfalls. Tax planning is an essential aspect of successful partnerships.

7.1 Partnership Taxation Basics

Partnerships are generally treated as pass-through entities for tax purposes. This means that the partnership itself does not pay income tax. Instead, the profits and losses of the partnership are passed through to the partners, who report them on their individual tax returns. This structure can provide significant tax advantages.

7.2 Allocating Income and Losses

The partnership agreement should clearly outline how income and losses will be allocated among the partners. This allocation must have substantial economic effect, meaning it must reflect the true economic realities of the partnership. Proper allocation is crucial for compliance with tax laws.

7.3 Partnership Tax Forms

Partnerships are required to file Form 1065, U.S. Return of Partnership Income, to report their income, deductions, and credits to the IRS. Each partner receives a Schedule K-1, which reports their share of the partnership’s income, deductions, and credits. Accurate reporting is essential for avoiding penalties.

8. Common Mistakes to Avoid When Offsetting Passive Losses

Several common mistakes can prevent you from successfully offsetting passive losses against active income. Avoiding these mistakes is crucial for maximizing your tax benefits. Careful planning and attention to detail can help you navigate the complexities of passive loss rules.

8.1 Not Meeting the Active Participation Requirements

Failing to meet the active participation requirements for the $25,000 rental real estate loss allowance is a common mistake. Ensure that you actively participate in the management of your rental properties. Document your activities thoroughly to substantiate your claims.

8.2 Exceeding the AGI Phaseout Threshold

Exceeding the AGI phaseout threshold for the $25,000 allowance can reduce or eliminate your deduction. Plan your income and deductions carefully to stay within the threshold. Strategies to reduce AGI can help you maximize your allowance.

8.3 Not Documenting Material Participation

Failing to document material participation in rental real estate activities is a common mistake for real estate professionals. Maintain detailed records of your involvement to support your claims. Accurate documentation is essential for substantiating your tax benefits.

8.4 Overlooking the Tax Consequences of C Corporations

Overlooking the tax consequences of conducting business in C corporations can lead to unexpected tax liabilities. Consider the potential for double taxation and other issues. Seek professional advice to make informed decisions.

9. Staying Updated on Tax Law Changes

Tax laws are constantly evolving, so it’s important to stay updated on the latest changes. Regularly review tax publications, consult with tax professionals, and attend industry seminars to stay informed. Keeping up with tax law changes can help you maximize your tax benefits and avoid potential penalties.

9.1 Resources for Staying Informed

Several resources can help you stay informed on tax law changes, including:

- IRS Publications: Official publications from the IRS.

- Tax Newsletters: Newsletters from reputable tax organizations.

- Professional Seminars: Seminars and webinars from tax professionals.

- Online Forums: Online forums and discussion groups.

Utilize these resources to stay up-to-date.

9.2 Consulting with Tax Professionals

Consulting with tax professionals is a valuable way to stay informed on tax law changes and ensure that you are taking advantage of all available tax benefits. A qualified tax advisor can provide personalized guidance and help you navigate the complexities of passive loss rules. Professional advice is essential for effective tax planning.

10. Frequently Asked Questions (FAQs) About Passive Losses and Active Income

1. What are passive losses?

Passive losses are losses from any trade or business in which you do not materially participate, often including rental activities.

2. Can passive losses offset active income?

Generally, no, passive losses can only offset passive income. However, there are exceptions, such as the $25,000 rental real estate loss allowance.

3. What is the $25,000 rental real estate loss allowance?

This allowance allows qualifying individuals to offset up to $25,000 of nonpassive income with rental real estate losses and credits.

4. How do I qualify for the $25,000 allowance?

You must own at least 10% of the value of all interests in the activity and actively participate in the operations of the rental property.

5. What is active participation?

Active participation involves making management decisions or arranging for others to provide services for the rental property.

6. What is modified adjusted gross income (AGI)?

Modified AGI is AGI calculated without considering certain deductions and exclusions, such as IRA deductions and student loan interest.

7. How does the AGI phaseout affect the $25,000 allowance?

The allowance is reduced by 50% of the amount by which your modified AGI exceeds $100,000, and it is completely phased out when your AGI reaches $150,000.

8. Who qualifies as a real estate professional?

To qualify, you must spend more than half of your working hours and more than 750 hours during the year in real property trades or businesses.

9. Can a closely held C corporation use passive losses to offset active income?

Yes, closely held C corporations (other than PSCs) can use passive losses to offset net active income.

10. Where can I find more information and connect with potential partners?

Visit income-partners.net for resources, articles, and a partner directory to connect with individuals and businesses for strategic collaborations.

Navigating the complexities of passive loss rules requires careful planning and attention to detail. By understanding the rules, exceptions, and strategies discussed in this article, you can maximize your tax benefits and achieve your financial goals. Don’t forget to explore the resources and opportunities available on income-partners.net to connect with potential partners and take your business to the next level. Visit income-partners.net today to discover how you can leverage strategic partnerships to maximize your income and offset passive losses, turning financial challenges into opportunities for growth and success in the dynamic world of business.

Ready to explore new income streams and maximize your tax benefits? Visit income-partners.net now to discover strategic partnership opportunities and expert resources tailored for ambitious entrepreneurs and investors in the USA. Connect with potential partners in Austin, TX, and beyond, and start building profitable collaborations today. Our comprehensive platform offers the tools and knowledge you need to turn passive losses into active gains. Don’t wait—your next successful partnership awaits at income-partners.net! For inquiries, contact us at Address: 1 University Station, Austin, TX 78712, United States. Phone: +1 (512) 471-3434. Website: income-partners.net.