Finding out your taxable income is crucial for accurate tax filing and financial planning; it’s the income amount that is subject to tax after deductions and exemptions, and income-partners.net can help you navigate this process. By understanding how to calculate this figure, you can optimize your tax strategy and potentially increase your income through strategic partnerships. Discover the resources available at income-partners.net to help you succeed with tax management, income growth, and financial awareness.

1. What Exactly Is Taxable Income and Why Does It Matter?

Taxable income is the portion of your total income that is subject to taxation by federal, state, and local governments. It’s a critical figure because it directly impacts the amount of taxes you owe.

-

The Core Concept: Taxable income isn’t simply your gross income. Instead, it’s what remains after you subtract allowable deductions and exemptions from your gross income. This can include deductions for business expenses, contributions to retirement accounts, and other eligible items.

-

Why It Matters: Understanding your taxable income helps you:

- Avoid Penalties: Accurately calculating your taxable income ensures you pay the correct amount of taxes, avoiding potential penalties from underpayment.

- Plan Finances: Knowing your taxable income allows for better financial planning, budgeting, and investment strategies.

- Optimize Tax Strategy: Identifying available deductions and credits can significantly reduce your taxable income, leading to lower tax liabilities.

-

Example: Let’s say you’re a small business owner in Austin. If you don’t accurately calculate your taxable income, you might miss out on deductions related to business expenses, potentially overpaying your taxes.

-

Income-partners.net and Taxable Income: At income-partners.net, we understand the importance of managing your finances effectively. Our resources provide insights into forming strategic partnerships that can not only increase your gross income but also help you navigate tax planning with greater confidence.

2. How Is Taxable Income Calculated for Individuals?

Calculating taxable income for individuals involves several steps, starting with gross income and then subtracting various deductions and exemptions to arrive at the final taxable amount.

- Step 1: Determine Gross Income: Gross income includes all income you receive in the form of money, goods, property, and services that aren’t exempt from tax. This includes wages, salaries, tips, investment income, and income from self-employment.

- Step 2: Calculate Adjusted Gross Income (AGI): AGI is gross income minus certain “above-the-line” deductions. These deductions can include contributions to traditional IRAs, student loan interest payments, and alimony payments.

- Step 3: Choose Standard Deduction or Itemize: After calculating your AGI, you can either take the standard deduction (a fixed amount based on your filing status) or itemize your deductions. Itemized deductions include expenses like medical expenses, state and local taxes (SALT), and charitable contributions.

- Step 4: Calculate Taxable Income: Taxable income is your AGI minus either the standard deduction or your total itemized deductions.

- Example: Consider a marketing specialist in Austin with a salary of $80,000. They contribute $5,000 to a traditional IRA and pay $2,000 in student loan interest. Their AGI is $73,000. If they take the standard deduction of $13,850 (for single filers in 2023), their taxable income would be $59,150.

- Utilizing income-partners.net: Our platform, income-partners.net, helps you connect with financial professionals who can guide you through these calculations. By exploring partnership opportunities, you can also discover new income streams and strategies to optimize your tax planning.

3. What Are Common Above-The-Line Deductions That Reduce AGI?

Above-the-line deductions are subtracted from your gross income to arrive at your Adjusted Gross Income (AGI). These deductions are beneficial because they reduce your income before you decide whether to take the standard deduction or itemize.

- Traditional IRA Contributions: Contributions to a traditional IRA are often deductible, which can significantly lower your taxable income.

- Student Loan Interest: You can deduct the interest you paid on student loans, up to a certain limit.

- Health Savings Account (HSA) Contributions: Contributions to an HSA are deductible and can help you save on healthcare costs while reducing your taxable income.

- Alimony Payments: If you pay alimony under a divorce or separation agreement executed before 2019, these payments may be deductible.

- Self-Employment Tax: You can deduct one-half of your self-employment tax.

- Example: A freelance web developer in Austin earns $70,000 annually. They contribute $4,000 to a traditional IRA and pay $1,500 in student loan interest. Their above-the-line deductions total $5,500, reducing their AGI to $64,500.

- How income-partners.net Helps: Income-partners.net provides resources to help you connect with financial advisors who can identify all applicable deductions. Forming strategic partnerships can also lead to new business opportunities, increasing your income and potential deductions.

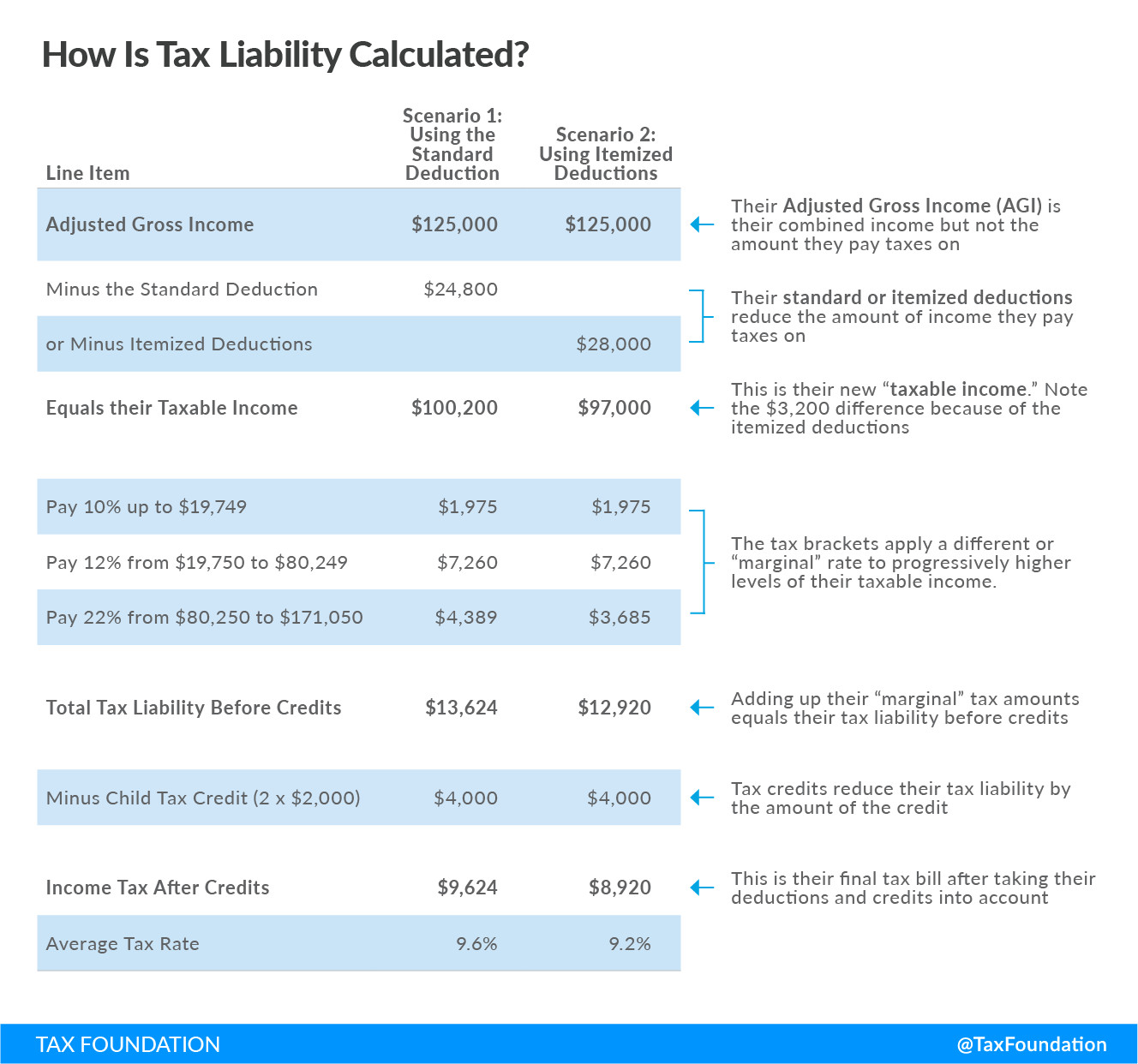

Tax Basics – How Is Tax Liability Calculated, adjusted gross income, average tax rate, child tax credit, earned income tax credit, individual income tax, itemized deduction, marginal tax rate, standard deduction, tax credit, tax deduction, taxable income

Tax Basics – How Is Tax Liability Calculated, adjusted gross income, average tax rate, child tax credit, earned income tax credit, individual income tax, itemized deduction, marginal tax rate, standard deduction, tax credit, tax deduction, taxable income

4. Should I Take the Standard Deduction or Itemize My Deductions?

Deciding whether to take the standard deduction or itemize your deductions can significantly impact your taxable income. The best choice depends on whether your itemized deductions exceed the standard deduction for your filing status.

- Standard Deduction: The standard deduction is a fixed amount that reduces your taxable income. The amount varies based on your filing status (single, married filing jointly, etc.) and is adjusted annually for inflation.

- Itemized Deductions: Itemizing involves listing individual deductions, such as medical expenses, state and local taxes (SALT), mortgage interest, and charitable contributions.

- How to Decide: Compare the total of your itemized deductions to the standard deduction for your filing status. If your itemized deductions are greater than the standard deduction, itemizing will likely result in a lower taxable income.

- Example: A homeowner in Austin has the following itemized deductions: $10,000 in mortgage interest, $5,000 in state and local taxes, and $2,000 in charitable contributions. Their total itemized deductions are $17,000. If the standard deduction for their filing status is $13,850, they should itemize to reduce their taxable income further.

- Income-partners.net’s Role: At income-partners.net, we encourage you to seek advice from tax professionals to make the most informed decision. Our platform also provides opportunities to partner with businesses that can help you manage and optimize your financial strategies.

5. What Are Some Common Itemized Deductions to Be Aware Of?

Itemized deductions can substantially reduce your taxable income if they exceed the standard deduction. Knowing which expenses qualify as itemized deductions is crucial for effective tax planning.

- Medical Expenses: You can deduct medical expenses that exceed 7.5% of your adjusted gross income (AGI). This includes payments for doctors, dentists, hospitals, and long-term care.

- State and Local Taxes (SALT): You can deduct state and local property taxes, income taxes, or sales taxes, up to a combined limit of $10,000 per household.

- Mortgage Interest: Homeowners can deduct the interest paid on their mortgage for the first $750,000 of debt.

- Charitable Contributions: Donations to qualified charitable organizations are deductible, generally up to 60% of your AGI for cash contributions and 30% for property contributions.

- Casualty and Theft Losses: You may be able to deduct losses from casualty or theft of property if the loss is due to a federally declared disaster.

- Example: An entrepreneur in Austin has an AGI of $100,000. They incurred $15,000 in medical expenses. They can deduct $7,500 ($15,000 – 7.5% of $100,000) as a medical expense deduction.

- income-partners.net Resources: Partnering with financial experts through income-partners.net can help you identify and maximize your itemized deductions, leading to significant tax savings.

6. How Does Taxable Income Differ for the Self-Employed Compared to Employees?

Taxable income is calculated differently for self-employed individuals compared to traditional employees, primarily due to the types of deductions and taxes they pay.

- Employees: Employees receive a W-2 form from their employer, detailing their annual earnings and taxes withheld. Their taxable income is their gross income minus any above-the-line deductions, and either the standard or itemized deductions.

- Self-Employed: Self-employed individuals receive a 1099 form (or no form at all if paid under $600). They must calculate their business income and expenses using Schedule C, which directly impacts their taxable income. They also pay self-employment tax (Social Security and Medicare), but can deduct one-half of this tax from their gross income.

- Key Differences:

- Self-Employment Tax: Self-employed individuals pay both the employer and employee portions of Social Security and Medicare taxes.

- Business Expenses: Self-employed individuals can deduct a wide range of business expenses, such as office supplies, travel, and home office expenses.

- Qualified Business Income (QBI) Deduction: Eligible self-employed individuals may also be able to deduct up to 20% of their qualified business income.

- Example: A freelance consultant in Austin earns $90,000 in revenue. They have $20,000 in business expenses and pay $7,000 in self-employment tax. Their taxable income is calculated as: $90,000 (revenue) – $20,000 (expenses) – $3,500 (half of self-employment tax) = $66,500.

- Income-partners.net Benefits: Navigating self-employment taxes and deductions can be complex. Income-partners.net can connect you with tax professionals and business partners who can help you optimize your tax strategy and grow your business.

7. What Is the Qualified Business Income (QBI) Deduction and How Can It Lower My Taxable Income?

The Qualified Business Income (QBI) deduction allows eligible self-employed individuals and small business owners to deduct up to 20% of their qualified business income, significantly reducing their taxable income.

- Eligibility: The QBI deduction is available to self-employed individuals, partnerships, S corporations, and LLCs that are taxed as pass-through entities.

- Calculation: The deduction is generally 20% of your QBI, but it may be limited based on your taxable income. For 2023, the deduction is capped at the lesser of 20% of QBI or 20% of the taxpayer’s taxable income (excluding capital gains).

- QBI Definition: QBI includes income from a trade or business, but excludes items like capital gains, interest income, and wage income.

- Example: A small business owner in Austin has a QBI of $80,000 and a taxable income of $70,000. They can deduct the lesser of 20% of $80,000 ($16,000) or 20% of $70,000 ($14,000). Therefore, their QBI deduction is $14,000, reducing their taxable income to $56,000.

- Income-partners.net Advantage: Income-partners.net helps you connect with tax advisors who can determine your eligibility for the QBI deduction and ensure you maximize this benefit. Forming strategic partnerships can also increase your QBI, potentially leading to a larger deduction.

8. How Do State and Local Taxes Affect My Federal Taxable Income?

State and local taxes (SALT) can affect your federal taxable income through the itemized deduction for SALT. Understanding the limitations and rules surrounding this deduction is essential for accurate tax planning.

- SALT Deduction: Taxpayers who itemize can deduct state and local property taxes, income taxes, or sales taxes. However, the Tax Cuts and Jobs Act of 2017 limited the SALT deduction to $10,000 per household.

- Impact on Taxable Income: If your total itemized deductions, including SALT, exceed the standard deduction, you can reduce your federal taxable income by itemizing. However, the $10,000 limit may restrict the full benefit for taxpayers in high-tax states.

- Example: A homeowner in Austin pays $6,000 in state income taxes and $5,000 in property taxes, totaling $11,000 in SALT. Due to the $10,000 limit, they can only deduct $10,000. If their total itemized deductions exceed the standard deduction, they can reduce their federal taxable income by $10,000.

- Income-partners.net Resources: Consulting with tax professionals through income-partners.net can help you optimize your SALT deduction and explore other tax-saving strategies. Strategic partnerships can also provide opportunities to manage your tax liabilities more effectively.

9. What Types of Income Are Considered Nontaxable?

While most forms of income are taxable, certain types of income are generally considered nontaxable by the IRS. Knowing what income is nontaxable can help you plan your finances more effectively.

- Life Insurance Payouts: Payments received from a life insurance policy are typically nontaxable.

- Gifts and Inheritances: Generally, gifts and inheritances are not considered taxable income to the recipient, although large estates may be subject to estate taxes.

- Certain Scholarship and Grant Money: Scholarship and grant money used for tuition, fees, and required books is often tax-free.

- Workers’ Compensation Benefits: Payments received as workers’ compensation for a job-related injury or illness are usually nontaxable.

- Child Support Payments: Child support payments are not considered taxable income to the recipient.

- Example: A recent college graduate in Austin receives a $20,000 scholarship to cover tuition and books. As long as the money is used for these qualified education expenses, it is generally not considered taxable income.

- How Income-partners.net Can Assist: Income-partners.net provides resources to help you understand various income sources and their tax implications. By partnering with financial experts, you can ensure you are accurately reporting your income and taking advantage of all available tax benefits.

10. How Can Retirement Account Contributions Affect My Taxable Income?

Contributions to retirement accounts, such as 401(k)s and IRAs, can significantly impact your taxable income, offering both immediate and deferred tax benefits.

- Traditional 401(k) and IRA Contributions: Contributions to traditional 401(k)s and IRAs are often tax-deductible, meaning they reduce your taxable income in the year you make the contribution.

- Roth 401(k) and IRA Contributions: Contributions to Roth 401(k)s and IRAs are not tax-deductible, but qualified withdrawals in retirement are tax-free.

- Impact on Taxable Income: Deductible contributions lower your current taxable income, which can result in immediate tax savings. However, withdrawals in retirement are taxed as ordinary income (for traditional accounts).

- Example: An employee in Austin contributes $10,000 to a traditional 401(k). This contribution is tax-deductible, reducing their taxable income by $10,000 for that year.

- Income-partners.net Benefits: Income-partners.net provides access to financial advisors who can help you choose the right retirement account and contribution strategy to optimize your tax situation. Strategic partnerships can also provide opportunities to increase your income and retirement savings.

11. How Do I Account for Capital Gains and Losses When Calculating Taxable Income?

Capital gains and losses, arising from the sale of assets like stocks, bonds, and real estate, are factored into your taxable income, but they are taxed differently than ordinary income.

- Capital Gains: Capital gains are profits from selling capital assets. They can be short-term (held for one year or less) or long-term (held for more than one year).

- Capital Losses: Capital losses occur when you sell a capital asset for less than its purchase price.

- Tax Treatment: Short-term capital gains are taxed at your ordinary income tax rate, while long-term capital gains are taxed at lower rates (0%, 15%, or 20%, depending on your income).

- Netting Gains and Losses: You can use capital losses to offset capital gains. If your capital losses exceed your capital gains, you can deduct up to $3,000 of the excess loss from your ordinary income ($1,500 if married filing separately).

- Example: An investor in Austin sells stocks, realizing a $5,000 long-term capital gain and a $2,000 short-term capital loss. The net capital gain is $3,000. The $5,000 long-term gain is taxed at a preferential rate, while the $2,000 short-term loss offsets some of the gain.

- How income-partners.net Can Help: Income-partners.net connects you with financial professionals who can advise you on managing capital gains and losses to minimize your tax liabilities. Strategic investment partnerships can also help you optimize your portfolio and increase your returns.

12. What Tax Credits Can Reduce My Taxable Income?

Tax credits directly reduce the amount of tax you owe, providing a dollar-for-dollar reduction in your tax liability. They are a valuable tool for lowering your overall tax burden.

- Child Tax Credit: Provides a credit for each qualifying child. The amount varies annually and is subject to income limitations.

- Earned Income Tax Credit (EITC): Benefits low- to moderate-income individuals and families. The credit amount depends on your income and the number of qualifying children you have.

- American Opportunity Tax Credit (AOTC): Helps pay for qualified education expenses for the first four years of college.

- Lifetime Learning Credit: Available for students taking courses to improve their job skills.

- Energy Credits: Available for homeowners who make energy-efficient improvements to their homes, such as installing solar panels.

- Example: A family in Austin with two qualifying children is eligible for the Child Tax Credit, reducing their tax liability by $2,000 per child, for a total reduction of $4,000.

- Income-partners.net’s Assistance: Partnering with tax professionals through income-partners.net can help you identify all the tax credits you are eligible for, maximizing your tax savings. Strategic financial partnerships can also help you manage your income and expenses to qualify for more credits.

13. What Are Some Common Mistakes to Avoid When Calculating Taxable Income?

Calculating taxable income accurately is essential to avoid penalties and ensure you are paying the correct amount of taxes. Here are some common mistakes to watch out for:

- Incorrectly Reporting Income: Failing to report all sources of income, such as freelance work or investment income, can lead to underpayment penalties.

- Missing Deductions: Not taking all eligible deductions, such as those for IRA contributions, student loan interest, or business expenses, can result in overpaying your taxes.

- Incorrectly Claiming Credits: Claiming credits you are not eligible for, such as the Child Tax Credit or Earned Income Tax Credit, can lead to penalties and interest.

- Miscalculating Capital Gains and Losses: Incorrectly calculating capital gains and losses from the sale of assets can result in tax errors.

- Not Keeping Accurate Records: Failing to keep accurate records of income, expenses, and deductions can make it difficult to prepare your tax return and support your claims.

- Example: A small business owner in Austin forgets to deduct eligible business expenses, such as office supplies and travel costs, resulting in a higher taxable income and increased tax liability.

- Income-partners.net’s Role: Income-partners.net offers resources and connections to tax professionals who can help you avoid these common mistakes, ensuring your tax returns are accurate and optimized for savings.

14. How Can Tax Planning Throughout the Year Help Me Manage My Taxable Income?

Engaging in tax planning throughout the year, rather than waiting until tax season, can help you proactively manage your taxable income and optimize your tax strategy.

- Estimate Your Income and Deductions: Regularly estimate your income and deductions to project your tax liability. This allows you to make adjustments throughout the year, such as increasing retirement contributions or making estimated tax payments.

- Adjust Withholding: If you are an employee, review your W-4 form and adjust your withholding to ensure you are not underpaying or overpaying your taxes.

- Maximize Retirement Contributions: Contribute as much as possible to tax-advantaged retirement accounts, such as 401(k)s and IRAs, to reduce your taxable income.

- Track Expenses: Keep detailed records of your income, expenses, and deductions to ensure you have accurate information when preparing your tax return.

- Seek Professional Advice: Consult with a tax advisor to review your tax situation and identify opportunities for tax savings.

- Example: A marketing consultant in Austin reviews their income and expenses quarterly, adjusts their estimated tax payments, and maximizes their contributions to a SEP IRA to reduce their taxable income throughout the year.

- How income-partners.net Supports You: Income-partners.net provides access to financial and tax professionals who can help you develop a comprehensive tax plan, manage your income, and optimize your tax strategy throughout the year.

15. How Do I Find Out My Taxable Income If I Have Multiple Income Streams?

Managing multiple income streams requires careful tracking and reporting to accurately calculate your taxable income. Here’s how to handle it:

- Identify All Income Sources: List all sources of income, including wages, self-employment income, investment income, rental income, and any other taxable income.

- Gather Relevant Documents: Collect all relevant tax documents, such as W-2 forms, 1099 forms, and statements for investment and rental income.

- Calculate Income from Each Source: Calculate the total income from each source. For self-employment income, subtract business expenses from your gross receipts.

- Combine All Income: Add up all your income from various sources to arrive at your gross income.

- Subtract Deductions: Subtract any above-the-line deductions, such as IRA contributions and student loan interest, to calculate your AGI.

- Choose Standard or Itemized Deductions: Decide whether to take the standard deduction or itemize your deductions, based on which method results in a lower taxable income.

- Calculate Taxable Income: Subtract the standard deduction or your total itemized deductions from your AGI to calculate your taxable income.

- Example: An individual in Austin works a full-time job, earns freelance income, and receives rental income. They must report all three sources of income and deduct any eligible expenses to calculate their taxable income accurately.

- Income-partners.net Assistance: Income-partners.net can connect you with tax professionals who specialize in managing complex tax situations involving multiple income streams, ensuring accurate reporting and optimized tax planning.

Calculating your taxable income is a fundamental aspect of financial management and tax compliance. By understanding the components of taxable income, taking advantage of available deductions and credits, and planning proactively, you can minimize your tax liability and achieve your financial goals. Income-partners.net is here to support you with resources, expert connections, and strategic partnership opportunities to help you navigate the complexities of taxable income and optimize your financial future.

Ready to Take Control of Your Taxable Income?

Visit income-partners.net today to explore partnership opportunities, connect with financial advisors, and discover strategies to optimize your tax planning and increase your income. Whether you’re a business owner, investor, or freelancer in Austin, we have the resources and connections you need to succeed.

Contact Us:

Address: 1 University Station, Austin, TX 78712, United States

Phone: +1 (512) 471-3434

Website: income-partners.net

FAQ: Understanding Taxable Income

- What is the definition of taxable income? Taxable income is the amount of income that is subject to taxation after deductions and exemptions are applied.

- How do I calculate my taxable income as a W-2 employee? Start with your gross income from your W-2, subtract any above-the-line deductions, and then subtract either the standard deduction or your itemized deductions.

- What are some examples of nontaxable income? Examples include life insurance payouts, gifts, certain scholarship money, and workers’ compensation benefits.

- Is there a difference between gross income and taxable income? Yes, gross income is the total income before any deductions, while taxable income is the income amount subject to tax after deductions and exemptions.

- How do retirement contributions affect my taxable income? Contributions to traditional retirement accounts like 401(k)s and IRAs are often tax-deductible, reducing your taxable income.

- What is the Qualified Business Income (QBI) deduction? The QBI deduction allows eligible self-employed individuals and small business owners to deduct up to 20% of their qualified business income.

- Can I deduct state and local taxes (SALT) from my federal taxable income? Yes, but the SALT deduction is limited to $10,000 per household.

- How can I find out my taxable income if I have multiple income streams? You need to identify all income sources, gather relevant tax documents, and calculate income from each source before combining them.

- Are capital gains and losses included in taxable income? Yes, capital gains are included, but they are taxed at different rates than ordinary income, and capital losses can offset capital gains.

- What tax credits can reduce my taxable income? Tax credits like the Child Tax Credit, Earned Income Tax Credit, and American Opportunity Tax Credit directly reduce the amount of tax you owe.

Disclaimer: This article provides general information and should not be considered as financial or tax advice. Consult with a qualified professional for personalized guidance.