1. Understanding Bad Debt Expense

What exactly is bad debt expense, and why is it so important for businesses to understand? Bad debt expense (BDE) represents the portion of a company’s accounts receivable that is deemed uncollectible. It is an essential accounting entry that acknowledges the reality that not all customers will pay their invoices, and it directly impacts a company’s financial statements.

1.1. Definition of Bad Debt Expense

Bad debt expense is the accounting entry that reflects the dollar amount of receivables a company doesn’t expect to collect. It’s a contra-asset account that reduces the value of accounts receivable on the balance sheet, providing a more realistic view of a company’s assets. According to accounting principles, this expense is recognized to match the revenue generated with the potential cost of uncollectible accounts.

1.2. Importance of Recognizing Bad Debt

Recognizing bad debt is crucial for several reasons:

- Accurate Financial Reporting: It provides a more accurate representation of a company’s financial health by acknowledging potential losses from uncollectible accounts.

- Compliance with Accounting Standards: Generally Accepted Accounting Principles (GAAP) require companies using accrual accounting to recognize bad debt expense to adhere to the matching principle.

- Informed Decision-Making: It helps management make informed decisions about credit policies, sales strategies, and risk management.

- Tax Implications: Writing off bad debt can have tax benefits, reducing a company’s taxable income.

1.3. Accrual vs. Cash Accounting

The method of accounting a company uses significantly affects how bad debt is handled:

- Accrual Accounting: Revenue is recognized when earned, and expenses are recognized when incurred, regardless of when cash changes hands. This method requires estimating and recording bad debt expense in the same period as the related revenue.

- Cash Accounting: Revenue is recognized when cash is received, and expenses are recognized when cash is paid out. Bad debt expense is not typically recorded under this method because revenue is only recognized when payment is received.

2. Where Bad Debt Expense Appears on the Income Statement

Where exactly does bad debt expense fit into the larger picture of a company’s financial statements? Bad debt expense is classified as an operating expense and is typically reported under Sales, General, and Administrative (SG&A) expenses on the income statement.

2.1. Classification as an Operating Expense

As an operating expense, bad debt expense is directly related to a company’s core business activities. It arises from the normal course of selling goods or services on credit. This classification is essential because it affects a company’s operating income, which is a key metric for assessing profitability from core operations.

2.2. Placement Under SG&A Expenses

Bad debt expense is commonly grouped with SG&A expenses because it is considered an administrative cost associated with managing credit and collections. SG&A expenses include costs related to sales, marketing, and the general administration of a business. Grouping bad debt expense with these costs provides a comprehensive view of the expenses necessary to support a company’s operations.

2.3. Impact on Net Income

Bad debt expense directly reduces a company’s net income. When bad debt expense is recognized, it lowers the company’s profit, reflecting the loss from uncollectible accounts. This reduction in net income impacts earnings per share (EPS) and other key financial ratios, which are closely watched by investors and stakeholders.

3. Methods for Recording Bad Debt Expense

What are the different methods that companies can use to record bad debt expense, and how do they work? There are two main methods for recording bad debt expense: the direct write-off method and the allowance method. Each method has its own advantages and disadvantages, and the choice of method depends on the company’s accounting policies and the materiality of bad debt.

3.1. Direct Write-Off Method

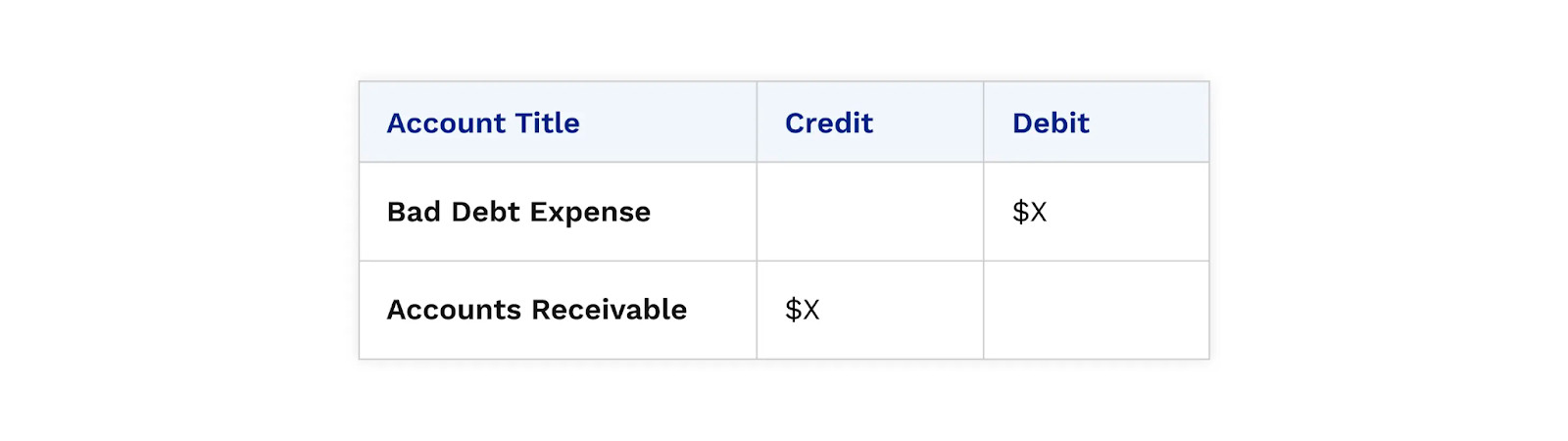

The direct write-off method recognizes bad debt expense only when a specific account is deemed uncollectible. This method is straightforward:

- When an account is identified as uncollectible, the company directly writes off the receivable and records bad debt expense.

- The journal entry involves debiting bad debt expense and crediting accounts receivable.

Advantages:

- Simple and easy to implement.

- Suitable for companies with immaterial bad debt or those using the cash accounting method.

Disadvantages:

- Violates the matching principle by not matching revenue with the related expense in the same period.

- Can lead to inaccurate financial reporting, as it does not provide a realistic view of potential losses from uncollectible accounts.

3.2. Allowance Method

The allowance method is a more sophisticated approach that estimates bad debt expense and creates an allowance for doubtful accounts. This method is required by GAAP for companies using accrual accounting:

- At the end of each accounting period, the company estimates the amount of accounts receivable that is likely to be uncollectible.

- An allowance for doubtful accounts (AFDA) is created, which is a contra-asset account that reduces the value of accounts receivable on the balance sheet.

- Bad debt expense is recognized in the same period as the related revenue, adhering to the matching principle.

Advantages:

- Complies with GAAP and the matching principle.

- Provides a more accurate representation of a company’s financial position.

- Allows for better management of credit risk.

Disadvantages:

- More complex to implement than the direct write-off method.

- Requires estimation and judgment, which can be subjective.

3.3. Estimating Bad Debt Expense Under the Allowance Method

How do companies actually go about estimating the amount of bad debt expense under the allowance method? There are several techniques that companies use to estimate bad debt expense under the allowance method, each with its own strengths and weaknesses.

3.3.1. Percentage of Sales Method

The percentage of sales method estimates bad debt expense as a percentage of credit sales:

- The company calculates a historical percentage of uncollectible sales based on past experience.

- This percentage is applied to current credit sales to estimate bad debt expense.

Formula:

Bad Debt Expense = Percentage of Uncollectible Sales * Credit SalesExample:

If a company has credit sales of $500,000 and a historical uncollectible percentage of 2%, the bad debt expense would be:

Bad Debt Expense = 0.02 * $500,000 = $10,0003.3.2. Percentage of Accounts Receivable Method

The percentage of accounts receivable method estimates bad debt expense as a percentage of outstanding accounts receivable:

- The company calculates a historical percentage of uncollectible receivables based on past experience.

- This percentage is applied to the current accounts receivable balance to estimate the required balance in the allowance for doubtful accounts.

Formula:

Allowance for Doubtful Accounts = Percentage of Uncollectible Receivables * Accounts ReceivableExample:

If a company has accounts receivable of $300,000 and a historical uncollectible percentage of 5%, the required balance in the allowance for doubtful accounts would be:

Allowance for Doubtful Accounts = 0.05 * $300,000 = $15,000The bad debt expense is then calculated as the difference between the required balance and the existing balance in the allowance for doubtful accounts.

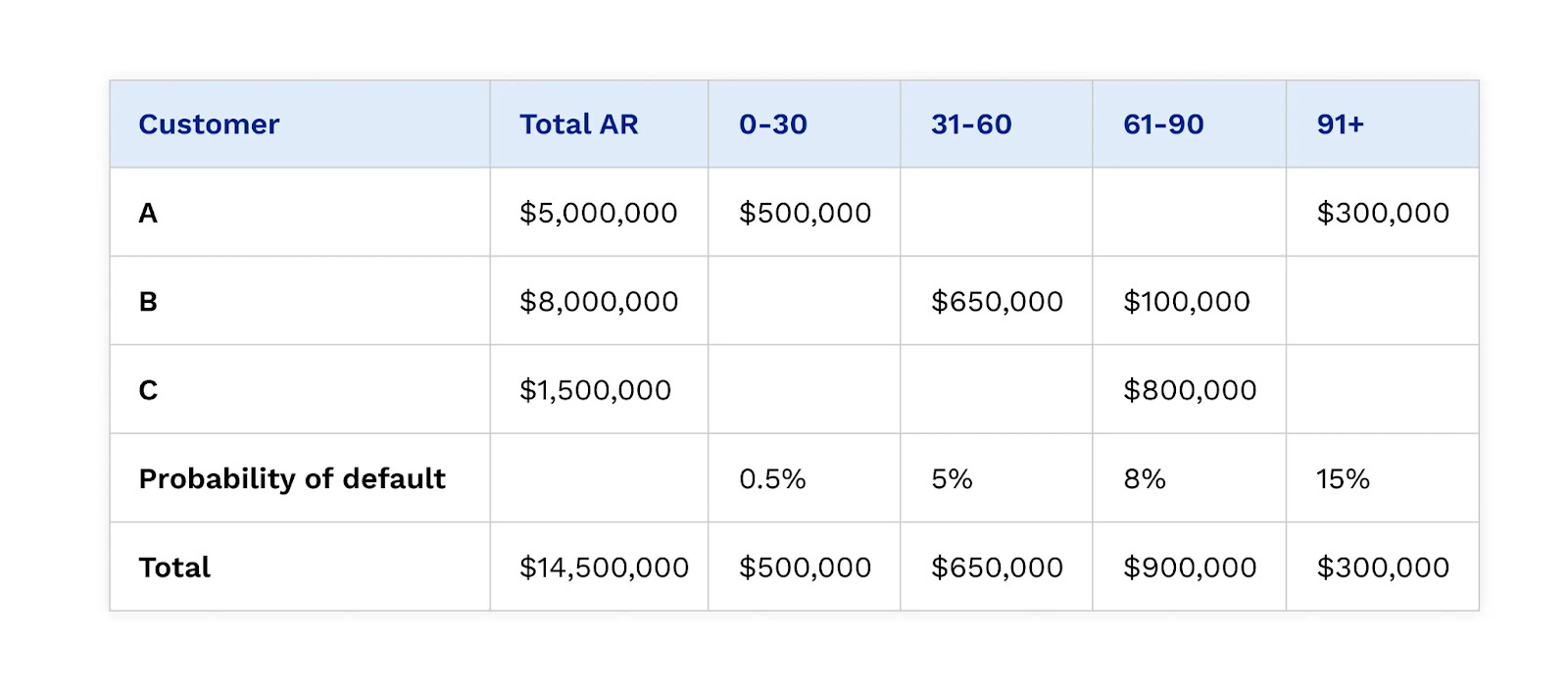

3.3.3. Aging of Accounts Receivable Method

The aging of accounts receivable method categorizes accounts receivable by age and applies different uncollectible percentages to each category:

- The company prepares an aging schedule that classifies receivables into categories such as current, 30-60 days past due, 61-90 days past due, and over 90 days past due.

- Each category is assigned a different uncollectible percentage based on historical experience.

- The estimated bad debt expense is the sum of the uncollectible amounts for each category.

Example:

| Aging Category | Balance | Uncollectible Percentage | Estimated Uncollectible Amount |

|---|---|---|---|

| Current | $100,000 | 1% | $1,000 |

| 30-60 Days Past Due | $50,000 | 5% | $2,500 |

| 61-90 Days Past Due | $20,000 | 10% | $2,000 |

| Over 90 Days Past Due | $10,000 | 20% | $2,000 |

| Total | $180,000 | $7,500 |

In this example, the estimated bad debt expense would be $7,500.

3.4. Writing Off Uncollectible Accounts Under the Allowance Method

Once an account is deemed uncollectible under the allowance method, it is written off:

- The journal entry involves debiting the allowance for doubtful accounts and crediting accounts receivable.

- The write-off does not affect bad debt expense because the expense was already recognized when the allowance was created.

- If the company later recovers a written-off account, the recovery is recorded by reversing the write-off entry and recognizing the cash receipt.

4. Factors Contributing to Bad Debt

What are some of the common reasons why businesses end up with bad debt in the first place? Several factors can contribute to bad debt, and understanding these factors is essential for managing and minimizing the risk of uncollectible accounts.

4.1. Poor Credit Policies

Lax credit policies can lead to increased bad debt:

- Offering credit to customers with poor credit histories.

- Setting high credit limits without adequate evaluation.

- Failing to monitor customer creditworthiness regularly.

4.2. Ineffective Collection Procedures

Ineffective collection procedures can also increase bad debt:

- Delaying collection efforts until accounts are significantly overdue.

- Failing to follow up on overdue accounts consistently.

- Not using a variety of collection methods, such as phone calls, emails, and letters.

4.3. Economic Downturns

Economic downturns can lead to increased bad debt as customers struggle to pay their bills:

- Recessions and economic slowdowns can reduce customer income and increase unemployment rates.

- Businesses may experience financial difficulties, leading to delayed or missed payments.

4.4. Disputes and Disagreements

Disputes and disagreements between companies and customers can also result in bad debt:

- Customers may refuse to pay invoices due to dissatisfaction with products or services.

- Billing errors and discrepancies can lead to payment delays and disputes.

According to a survey by Wakefield Research and Versapay, 85% of C-level executives stated that miscommunication between their AR department and a customer has resulted in the customer not paying in full.

4.5. Customer Bankruptcy

Customer bankruptcy is a significant cause of bad debt:

- When a customer files for bankruptcy, the company may be unable to collect the full amount owed.

- Bankruptcy proceedings can be lengthy and complex, further delaying or reducing payments.

5. Strategies to Minimize Bad Debt Expense

What steps can businesses take to proactively minimize the risk of bad debt and improve their financial stability? There are several strategies that companies can implement to minimize bad debt expense and improve their cash flow.

5.1. Implement Sound Credit Policies

Establishing and enforcing sound credit policies is essential:

- Conduct thorough credit checks on new customers.

- Set credit limits based on customer creditworthiness.

- Regularly review and update credit policies.

5.2. Improve Collection Procedures

Improving collection procedures can also reduce bad debt:

- Send invoices promptly and accurately.

- Follow up on overdue accounts regularly.

- Offer multiple payment options.

- Consider using a collection agency for seriously delinquent accounts.

5.3. Monitor Accounts Receivable

Monitoring accounts receivable can help identify potential bad debt early:

- Track days sales outstanding (DSO) to identify trends in payment patterns.

- Review aging reports regularly to identify overdue accounts.

- Investigate and resolve disputes promptly.

5.4. Offer Early Payment Discounts

Offering early payment discounts can incentivize customers to pay promptly:

- Provide a small discount for payments made within a specified timeframe.

- This can improve cash flow and reduce the risk of bad debt.

5.5. Build Strong Customer Relationships

Building strong customer relationships can also minimize bad debt:

- Communicate proactively with customers to address concerns and resolve issues.

- Provide excellent customer service.

- Foster a culture of trust and cooperation.

5.6. Collaborative Accounts Receivable Solutions

Implementing collaborative accounts receivable solutions, like Versapay, can significantly minimize bad debt expense:

- Transparent Communication: Collaborative AR facilitates clear communication between AR staff and customers, resolving issues such as disputed invoice charges and missing remittance information efficiently.

- Alignment Between Sales and AR Teams: Giving sales teams access to customer payment history and cash flow data enables them to make informed credit decisions, fostering better communication and understanding of credit terms.

- Focus on Value-Added Work: By automating invoicing, collections, payment processing, and cash application workflows, AR teams can focus on strategic tasks like uncovering causes of payment delays and improving customer relationships.

6. The Role of Collaborative Partnerships in Minimizing Bad Debt

How can strategic partnerships help businesses reduce their exposure to bad debt and create more stable revenue streams? Collaborative partnerships play a pivotal role in minimizing bad debt by fostering stronger customer relationships and providing more reliable revenue streams.

6.1. Risk Sharing Through Joint Ventures

Joint ventures allow companies to share the risk of extending credit to customers:

- By pooling resources and expertise, companies can conduct more thorough credit checks and implement more effective collection procedures.

- The risk of bad debt is spread across multiple partners, reducing the impact on any single company.

6.2. Improved Customer Relationships Through Strategic Alliances

Strategic alliances can enhance customer relationships and reduce the likelihood of disputes:

- Partners can work together to provide excellent customer service and resolve issues promptly.

- By offering complementary products and services, partners can create a more comprehensive and valuable customer experience.

6.3. Enhanced Market Reach Through Distribution Partnerships

Distribution partnerships can expand a company’s market reach and diversify its customer base:

- By selling products and services through multiple channels, companies can reduce their reliance on any single customer or market.

- This diversification can mitigate the risk of bad debt and improve overall financial stability.

6.4. Financial Stability Through Revenue Sharing Agreements

Revenue sharing agreements can provide a more stable and predictable revenue stream:

- Partners agree to share revenue based on a predetermined formula.

- This can reduce the impact of fluctuations in sales and improve cash flow.

6.5. Case Studies of Successful Partnerships Reducing Bad Debt

Are there any real-world examples of companies that have successfully used partnerships to minimize bad debt? Several companies have successfully leveraged partnerships to minimize bad debt expense.

6.5.1. Example 1: Technology Company and Financial Institution

A technology company partnered with a financial institution to offer financing options to its customers. The financial institution conducted credit checks and managed collections, reducing the technology company’s risk of bad debt. The partnership also allowed the technology company to offer more competitive financing terms, increasing sales and customer satisfaction.

6.5.2. Example 2: Retailer and Insurance Company

A retailer partnered with an insurance company to offer credit insurance to its customers. The insurance company covered the risk of non-payment, protecting the retailer from bad debt. The partnership also provided customers with peace of mind, encouraging them to make purchases on credit.

6.5.3. Example 3: Manufacturing Company and Distributor

A manufacturing company partnered with a distributor to sell its products in new markets. The distributor managed credit and collections in the new markets, reducing the manufacturing company’s risk of bad debt. The partnership also allowed the manufacturing company to expand its market reach without incurring significant additional expenses.

These examples illustrate how collaborative partnerships can be a powerful tool for minimizing bad debt and improving financial stability.

7. Navigating the IRS Requirements for Bad Debt Write-Offs

What does the IRS require in order for a business to be able to write off bad debt for tax purposes? Navigating the IRS requirements for bad debt write-offs is crucial for businesses seeking to claim deductions on their tax returns. The IRS has specific rules and conditions that must be met to qualify for a bad debt deduction.

7.1. Establishing Worthlessness

To write off bad debt, a business must establish that the debt is truly worthless:

- The business must demonstrate that it has taken reasonable steps to collect the debt, such as sending demand letters, making phone calls, and pursuing legal action.

- The business must also provide evidence that the debtor is unable to pay, such as bankruptcy filings, insolvency, or disappearance.

According to IRS Publication 535, “Business Expenses,” a debt is considered worthless when there is no reasonable expectation of recovery.

7.2. Meeting IRS Conditions

The IRS has specific conditions that must be met to write off bad debt:

- The debt must be a valid and legally enforceable obligation.

- The debt must be related to the business operations.

- The business must have previously included the debt in income (for accrual method taxpayers).

- The business must not be a related party to the debtor (for non-business bad debt).

7.3. Maintaining Adequate Documentation

Maintaining adequate documentation is essential for supporting a bad debt write-off:

- Keep records of all collection efforts, including demand letters, phone logs, and legal correspondence.

- Obtain and retain evidence of the debtor’s inability to pay, such as bankruptcy filings, financial statements, and credit reports.

- Maintain accurate accounting records that clearly identify the bad debt.

7.4. Filing Form 3115 for Method Changes

If a business changes its method of accounting for bad debt, it may need to file Form 3115, “Application for Change in Accounting Method,” with the IRS:

- This form is used to request permission to change from the direct write-off method to the allowance method, or vice versa.

- The IRS reviews the application and determines whether the change is permissible.

8. The Future of Bad Debt Management: Trends and Innovations

What are some of the emerging trends and innovations in bad debt management that businesses should be aware of? The future of bad debt management is being shaped by several emerging trends and innovations, including the use of artificial intelligence (AI), machine learning (ML), and blockchain technology.

8.1. Artificial Intelligence and Machine Learning

AI and ML are being used to improve credit scoring, predict payment behavior, and automate collection efforts:

- AI-powered credit scoring models can analyze vast amounts of data to assess creditworthiness more accurately.

- ML algorithms can identify patterns in payment behavior and predict which accounts are most likely to become uncollectible.

- AI-driven chatbots can automate collection efforts, sending reminders and negotiating payment plans with customers.

8.2. Blockchain Technology

Blockchain technology is being used to create more transparent and secure payment systems:

- Blockchain-based platforms can provide a tamper-proof record of transactions, reducing the risk of disputes and fraud.

- Smart contracts can automate payment terms and enforce collection procedures.

8.3. Real-Time Analytics

Real-time analytics are providing businesses with up-to-date insights into their accounts receivable:

- Real-time dashboards can track key metrics such as DSO, collection rates, and bad debt expense.

- This allows businesses to identify potential problems early and take corrective action.

8.4. Integration with ERP Systems

Integration with enterprise resource planning (ERP) systems is streamlining the bad debt management process:

- Integrating bad debt management software with ERP systems allows for seamless data flow and automation of tasks.

- This can improve efficiency and reduce the risk of errors.

9. Partnering for Profit: How income-partners.net Can Help

Ready to explore how strategic partnerships can revolutionize your approach to bad debt management and unlock new revenue streams? At income-partners.net, we understand the challenges businesses face in managing bad debt and maximizing profitability. That’s why we offer a comprehensive suite of services to help you find the right partners, build strong relationships, and achieve your financial goals.

9.1. Identifying Strategic Partnership Opportunities

We leverage our extensive network and industry expertise to identify strategic partnership opportunities that align with your business objectives:

- We conduct thorough market research to identify potential partners.

- We assess the compatibility of potential partners based on factors such as culture, values, and business practices.

- We facilitate introductions and negotiations to help you build mutually beneficial relationships.

9.2. Facilitating Collaboration and Communication

We provide tools and resources to facilitate collaboration and communication between partners:

- We offer online platforms for sharing information, coordinating activities, and tracking progress.

- We provide training and support to help partners work together effectively.

- We mediate disputes and resolve conflicts to ensure smooth working relationships.

9.3. Structuring Mutually Beneficial Agreements

We help you structure mutually beneficial agreements that protect your interests and maximize your returns:

- We provide legal and financial expertise to help you negotiate favorable terms.

- We ensure that agreements are clear, concise, and enforceable.

- We monitor compliance and enforce agreements to protect your rights.

9.4. Monitoring and Evaluating Partnership Performance

We help you monitor and evaluate partnership performance to ensure that you are achieving your goals:

- We track key metrics such as revenue, expenses, and customer satisfaction.

- We provide regular reports and analysis to help you assess the effectiveness of your partnerships.

- We make recommendations for improvement and help you adjust your strategies as needed.

9.5. Success Stories from income-partners.net Clients

Can you share any success stories from businesses that have used income-partners.net to improve their bad debt management and revenue generation? Several of our clients have achieved significant success by leveraging our partnership services.

9.5.1. Client A: Manufacturing Company

A manufacturing company partnered with a distributor through income-partners.net to expand its market reach. The partnership resulted in a 30% increase in sales and a significant reduction in bad debt expense. The manufacturing company was able to enter new markets without incurring significant additional expenses, and the distributor managed credit and collections effectively.

9.5.2. Client B: Technology Company

A technology company partnered with a financial institution through income-partners.net to offer financing options to its customers. The partnership resulted in a 20% increase in sales and a reduction in bad debt expense. The financial institution conducted credit checks and managed collections, reducing the technology company’s risk of non-payment.

9.5.3. Client C: Retail Company

A retail company partnered with an insurance company through income-partners.net to offer credit insurance to its customers. The partnership resulted in a 15% increase in sales and protection from bad debt. The insurance company covered the risk of non-payment, providing the retail company with peace of mind.

10. Frequently Asked Questions (FAQs) About Bad Debt Expense

Still have questions about bad debt expense and how it impacts your business? Here are some frequently asked questions to help clarify common concerns.

10.1. What is the difference between bad debt expense and allowance for doubtful accounts?

Bad debt expense is the expense recognized on the income statement, while the allowance for doubtful accounts is a contra-asset account on the balance sheet that reduces the value of accounts receivable.

10.2. How often should a company estimate bad debt expense?

A company should estimate bad debt expense at the end of each accounting period, typically monthly, quarterly, or annually.

10.3. Can a company recover a written-off account?

Yes, if a company recovers a written-off account, the recovery is recorded by reversing the write-off entry and recognizing the cash receipt.

10.4. What happens if a company underestimates bad debt expense?

If a company underestimates bad debt expense, its financial statements may be misleading, and it may need to restate its earnings.

10.5. Is bad debt expense tax deductible?

Yes, bad debt expense is tax deductible, subject to IRS rules and regulations.

10.6. How does bad debt expense affect a company’s credit rating?

High bad debt expense can negatively affect a company’s credit rating, as it indicates financial instability and poor credit management.

10.7. What is the role of the CFO in managing bad debt expense?

The CFO is responsible for overseeing the company’s financial operations, including managing bad debt expense and ensuring compliance with accounting standards.

10.8. Can automation help in managing bad debt expense?

Yes, automation can streamline collection efforts, improve communication with customers, and reduce the risk of errors, leading to better management of bad debt expense.

10.9. What are some best practices for managing customer credit?

Best practices for managing customer credit include conducting thorough credit checks, setting credit limits based on creditworthiness, and monitoring accounts receivable regularly.

10.10. How does economic instability impact bad debt expense?

Economic instability can lead to increased bad debt expense as customers struggle to pay their bills and businesses face financial difficulties.

Ready to take control of your bad debt management and unlock new partnership opportunities? Visit income-partners.net today to explore our services and connect with potential partners who can help you achieve your financial goals. Address: 1 University Station, Austin, TX 78712, United States. Phone: +1 (512) 471-3434. Website: income-partners.net.

Bad debt expense journal entry using the direct write-off method, showcasing the debit and credit entries.

Bad debt expense journal entry using the direct write-off method, showcasing the debit and credit entries.

Sample accounts receivable aging report showcasing various aging buckets and collection probabilities for accurate bad debt reserve calculations.

Sample accounts receivable aging report showcasing various aging buckets and collection probabilities for accurate bad debt reserve calculations.