How Much Income To Buy A 2m House? Affording a $2 million home is attainable with the right financial strategy, and at income-partners.net, we specialize in connecting you with opportunities to potentially boost your income through strategic partnerships. Our platform provides resources and connections to help you explore various partnership models, increase your earnings, and ultimately achieve your dream of homeownership. Consider exploring collaborations, joint ventures, and strategic alliances to reach your financial goals and make that $2 million house a reality with passive income, financial planning, and real estate investment.

Table of Contents

1. What Income Is Needed to Afford a $2 Million House?

2. Understanding the Full Cost of Owning a $2 Million House

3. How Much Income is Needed to Buy a $2 Million House?

4. Family Budget Considerations for a $2 Million House

5. Minimum Income Required to Afford a $2 Million Home

6. Where Should You Buy Real Estate?

7. Exploring Alternative Real Estate Investment Options

8. Leveraging Partnerships to Achieve Homeownership Goals

9. Navigating the Home Buying Process With Confidence

10. FAQs About Affording a $2 Million House

1. What Income Is Needed to Afford a $2 Million House?

To comfortably afford a $2 million house, a general guideline suggests earning at least $667,000 annually, which aligns with spending no more than 3x your gross income on a home. This income level allows for a 20% down payment of $400,000 and a cash buffer of $100,000. However, with low-interest rates, it’s possible to stretch up to 5x your annual gross income, requiring a minimum of $400,000 per year, although this might cause financial strain without a significant cash reserve.

1.1 How to Calculate Affordability

Calculating affordability involves more than just the purchase price. Property taxes, insurance, maintenance, and potential mortgage payments must be considered. A higher-priced home means higher expenses across the board.

1.1.1 Key Factors in Determining Affordability:

- Gross Annual Income: Your total income before taxes and deductions.

- Debt-to-Income Ratio (DTI): The percentage of your monthly income that goes towards debt payments. Lenders typically prefer a DTI of 43% or lower.

- Down Payment: Aim for at least 20% to avoid Private Mortgage Insurance (PMI) and secure better interest rates.

- Interest Rates: Lower interest rates can significantly reduce your monthly mortgage payments.

- Property Taxes: These can vary widely depending on location and can significantly impact your monthly expenses.

- Homeowners Insurance: Protects your property from damage and liability.

- Maintenance Costs: Budget for ongoing repairs and upkeep, which can be substantial for a high-value home.

1.2 The 30/30/3 Rule for Home Buying

The 30/30/3 rule, as highlighted on income-partners.net, provides a responsible framework for home buying.

1.2.1 Breaking Down the 30/30/3 Rule:

- 30% Income: Spend no more than 30% of your gross monthly income on housing costs (including mortgage payments, property taxes, and insurance).

- 30% Down Payment: Aim for at least a 30% down payment to reduce your loan amount and monthly payments.

- 3X Income: Buy a home that costs no more than 3 times your annual gross income.

1.3 Income vs. Lifestyle

While the numbers might align on paper, consider your lifestyle. Owning a $2 million house can impact your spending on other priorities like travel, education, and investments.

1.3.1 Balancing Income and Lifestyle:

- Assess Your Spending Habits: Track your current expenses to identify areas where you can save.

- Set Financial Goals: Determine your priorities and allocate your income accordingly.

- Create a Realistic Budget: Ensure that your housing costs don’t compromise your other financial goals.

2. Understanding the Full Cost of Owning a $2 Million House

Owning a $2 million house involves more than just the initial purchase price. Property taxes, insurance, maintenance, and potential mortgage payments can add up significantly, impacting your overall financial health.

2.1 Ongoing Expenses

Expect to pay upwards of $24,000 annually in property taxes alone, coupled with increased costs for heating, insurance, maintenance, cleaning, and landscaping.

2.1.1 Detailed Breakdown of Ongoing Expenses:

| Expense | Average Annual Cost |

|---|---|

| Property Taxes | $24,000+ |

| Home Insurance | $5,000 – $10,000 |

| Maintenance | $10,000 – $20,000 |

| Utilities | $5,000 – $10,000 |

| Landscaping | $3,000 – $7,000 |

| Cleaning Services | $2,000 – $5,000 |

| Total Estimated | $49,000 – $76,000+ |

2.2 Opportunity Cost

Consider the opportunity cost of owning a $2 million home, like the potential rental income if you were to rent it out. Unused rooms represent wasted money.

2.2.1 Evaluating Opportunity Costs:

- Potential Rental Income: Calculate how much you could earn by renting out your property or unused rooms.

- Investment Opportunities: Consider alternative investments that could generate higher returns.

- Personal Enjoyment: Weigh the benefits of homeownership against other lifestyle choices and experiences.

2.3 Real Estate Market

Keep an eye on the real estate market, especially in cities like Austin, Dallas, and Nashville, which may be overvalued.

2.3.1 Analyzing Market Trends:

- Price Appreciation: Monitor how quickly property values are increasing in your target area.

- Inventory Levels: Pay attention to the supply of available homes, as higher inventory can lead to price corrections.

- Economic Factors: Consider the overall economic health of the region, including job growth and demographic trends.

3. How Much Income is Needed to Buy a $2 Million House?

The income needed to buy a $2 million house varies based on factors like down payment, interest rates, and location. A general rule of thumb is to earn at least $400,000 annually with a 20% down payment.

3.1 Income Multiples

Stretching your income multiple to 5x may be possible in a low-interest rate environment, but it requires careful career and income projections.

3.1.1 Understanding Income Multiples:

- 3x Income: A conservative approach, ensuring financial stability and lower monthly payments.

- 4x Income: A moderate approach, balancing affordability and lifestyle.

- 5x Income: An aggressive approach, requiring careful financial planning and risk assessment.

3.2 Down Payment Impact

A larger down payment reduces the mortgage amount and monthly payments, making homeownership more affordable.

3.2.1 Benefits of a Larger Down Payment:

- Lower Monthly Payments: Reducing the loan amount translates to lower monthly mortgage payments.

- Better Interest Rates: Lenders typically offer more favorable interest rates to borrowers with larger down payments.

- Avoid PMI: Putting down at least 20% can help you avoid Private Mortgage Insurance (PMI).

3.3 Cash Buffer

Having a cash buffer is crucial for unexpected expenses or job loss. Aim for at least 5% of the home’s value as a cash reserve.

3.3.1 Building a Cash Buffer:

- Emergency Fund: Maintain an emergency fund with 3-6 months’ worth of living expenses.

- Savings Account: Keep a separate savings account specifically for housing-related expenses.

- Investment Portfolio: Consider liquidating some investments to build your cash buffer.

4. Family Budget Considerations for a $2 Million House

Owning a $2 million house significantly impacts a family’s budget. It’s crucial to assess all expenses and ensure financial stability.

4.1 Mortgage Payments

A $1.6 million mortgage at 3.15% can result in monthly payments of around $6,854, which is a significant expense.

4.1.1 Managing Mortgage Payments:

- Shop Around for Rates: Compare interest rates from different lenders to secure the best deal.

- Consider a Fixed-Rate Mortgage: Provides stability and predictability in your monthly payments.

- Make Extra Payments: Paying down your mortgage faster can save you thousands of dollars in interest over the life of the loan.

4.2 Additional Expenses

Property taxes, insurance, and maintenance costs can add thousands of dollars to your monthly expenses.

4.2.1 Planning for Additional Expenses:

- Create a Detailed Budget: Track all income and expenses to identify areas where you can save.

- Set Aside Funds: Allocate a portion of your income each month to cover property taxes, insurance, and maintenance costs.

- Consider Tax Deductions: Explore potential tax deductions for mortgage interest and property taxes.

4.3 Financial Security

Job security and income stability are essential when owning a high-value home. Avoid overextending yourself to minimize financial risk.

4.3.1 Ensuring Financial Security:

- Diversify Income Streams: Explore additional income opportunities, such as side hustles or investments.

- Maintain Job Skills: Stay up-to-date with industry trends and continuously develop your skills to remain competitive in the job market.

- Build a Strong Network: Cultivate relationships with colleagues and industry professionals to expand your job opportunities.

5. Minimum Income Required to Afford a $2 Million Home

Experts suggest aiming for a household income of at least $500,000 before buying a $2 million house, balancing the recommended 3x and maximum 5x income multiple.

5.1 Income Scenarios

Different income scenarios require varying down payments and cash reserves. Use a home affordability calculator to determine the income needed for your specific situation.

5.1.1 Factors Affecting Income Requirements:

| Factor | Impact |

|---|---|

| Down Payment | Larger down payments reduce the required income. |

| Interest Rates | Lower interest rates reduce the monthly mortgage payment. |

| Property Taxes | Higher property taxes increase the required income. |

| Debt Levels | Higher debt levels reduce the amount you can afford for housing. |

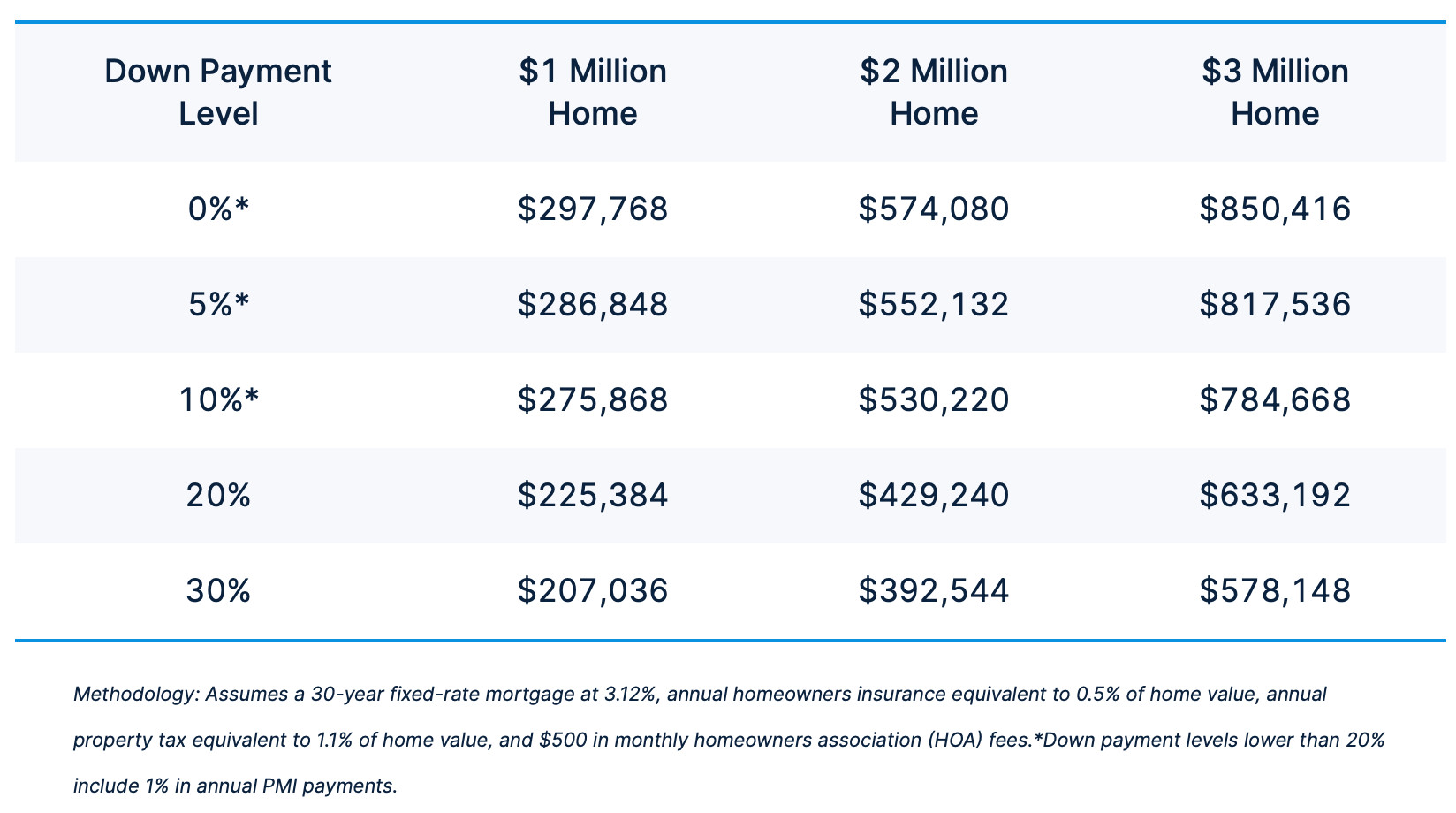

5.2 Affordability Chart

This chart provides a general guideline for the minimum income needed to afford homes of different values:

5.2.1 Income Needed for Different Home Values:

| Home Value | Minimum Income Needed |

|---|---|

| $1 Million | $196,272 – $287,040 |

| $2 Million | $392,544 – $574,080 |

| $3 Million | $588,816 – $861,120 |

Affordability chart

Affordability chart

5.3 Risks of Overextending

Overextending yourself in the real estate market can lead to financial stress and potential foreclosure. Avoid buying a $2 million house if you don’t meet the minimum income requirements.

5.3.1 Signs of Overextending:

- High Debt-to-Income Ratio: Spending more than 43% of your monthly income on debt payments.

- Limited Savings: Lacking an emergency fund or cash buffer for unexpected expenses.

- Dependence on Credit: Relying on credit cards to cover essential expenses.

6. Where Should You Buy Real Estate?

Location plays a crucial role in real estate investment. Cities with less price appreciation and lower supply may be more attractive.

6.1 Market Analysis

Analyze the real estate market in different cities to identify areas with growth potential and reasonable valuations.

6.1.1 Key Market Indicators:

- Job Growth: Cities with strong job markets tend to have higher demand for housing.

- Population Growth: Increasing population can drive up property values.

- Inventory Levels: Lower inventory can lead to price appreciation.

6.2 Overvalued Markets

Be cautious about stretching in overvalued markets like Austin, Dallas, and Nashville. Consider cities with less price appreciation and more affordable valuations.

6.2.1 Identifying Overvalued Markets:

- High Price-to-Rent Ratio: Indicates that property values are high relative to rental income.

- Rapid Price Appreciation: Unsustainable price increases can signal a market bubble.

- Increased Inventory: A surge in new construction can lead to price corrections.

6.3 Attractive Markets

Explore cities in the lower left quadrant of the valuation chart, with less supply and less price appreciation.

6.3.1 Characteristics of Attractive Markets:

- Stable Economy: A diversified economy with multiple industries.

- Affordable Housing: Lower median home prices and rental rates.

- Quality of Life: Access to amenities, good schools, and a safe environment.

7. Exploring Alternative Real Estate Investment Options

Consider alternative real estate investment options like real estate crowdfunding to diversify your portfolio and generate passive income.

7.1 Real Estate Crowdfunding

Real estate crowdfunding platforms allow you to invest in commercial and residential properties with smaller amounts of capital.

7.1.1 Benefits of Real Estate Crowdfunding:

- Diversification: Invest in multiple properties and markets.

- Passive Income: Earn rental income without the hassle of property management.

- Lower Investment Minimums: Start investing with as little as $500.

7.2 Platforms to Consider

Explore platforms like Fundrise and CrowdStreet to invest in real estate crowdfunding opportunities.

7.2.1 Popular Real Estate Crowdfunding Platforms:

- Fundrise: Offers private eFunds for accredited and non-accredited investors.

- CrowdStreet: Provides opportunities to invest in individual real estate projects.

7.3 Passive Income Generation

Real estate crowdfunding can generate passive income with annual returns of around 8%, providing financial flexibility and growth potential.

7.3.1 Maximizing Passive Income:

- Invest in High-Yield Properties: Look for properties with strong rental income potential.

- Reinvest Your Earnings: Compound your returns by reinvesting your rental income.

- Diversify Your Portfolio: Spread your investments across multiple properties and markets to reduce risk.

8. Leveraging Partnerships to Achieve Homeownership Goals

Strategic partnerships can significantly enhance your income and accelerate your path to owning a $2 million house.

8.1 Types of Partnerships

Explore various partnership models, including business partnerships, joint ventures, and strategic alliances.

8.1.1 Partnership Models:

- Business Partnerships: Collaborating with other businesses to expand your reach and increase revenue.

- Joint Ventures: Partnering with other companies on specific projects or ventures.

- Strategic Alliances: Forming alliances with complementary businesses to achieve shared goals.

8.2 Income-Partners.net

Income-partners.net specializes in connecting individuals with strategic partnership opportunities to increase their income and achieve their financial goals.

8.2.1 Benefits of Using Income-Partners.net:

- Access to Partnership Opportunities: Discover a wide range of partnership opportunities in various industries.

- Expert Guidance: Receive expert advice and resources on forming successful partnerships.

- Networking Opportunities: Connect with potential partners and collaborators.

8.3 Success Stories

Learn from real-life success stories of individuals who have leveraged partnerships to achieve their homeownership goals.

8.3.1 Keys to Successful Partnerships:

- Clear Communication: Establish clear communication channels and expectations.

- Shared Goals: Align your goals and interests with your partners.

- Mutual Trust: Build a foundation of trust and respect with your partners.

9. Navigating the Home Buying Process With Confidence

The home buying process can be complex and overwhelming. Having the right knowledge and support can help you navigate it with confidence.

9.1 Pre-Approval

Get pre-approved for a mortgage to understand how much you can afford and strengthen your negotiating position.

9.1.1 Steps to Getting Pre-Approved:

- Gather Financial Documents: Collect your income statements, tax returns, and bank statements.

- Check Your Credit Score: Review your credit report for any errors or discrepancies.

- Contact a Lender: Speak with a mortgage lender to discuss your options and get pre-approved.

9.2 Finding a Real Estate Agent

Work with an experienced real estate agent who can guide you through the home buying process and negotiate on your behalf.

9.2.1 Qualities of a Good Real Estate Agent:

- Local Market Knowledge: Familiarity with the local real estate market.

- Negotiation Skills: Ability to negotiate favorable terms on your behalf.

- Communication Skills: Clear and effective communication.

9.3 Making an Offer

Craft a competitive offer that reflects the market value of the property and your financial capabilities.

9.3.1 Tips for Making a Strong Offer:

- Offer a Fair Price: Base your offer on recent comparable sales in the area.

- Include Contingencies: Protect yourself with contingencies for inspections and financing.

- Provide a Strong Earnest Money Deposit: Demonstrates your commitment to the purchase.

10. FAQs About Affording a $2 Million House

Here are some frequently asked questions about affording a $2 million house:

10.1 What is the ideal debt-to-income ratio for buying a $2 million house?

Ideally, your debt-to-income ratio (DTI) should be below 43%. Lenders prefer borrowers who allocate less than 43% of their monthly income to debt payments, as it indicates a greater ability to manage financial obligations.

10.2 How can I increase my income to afford a $2 million house?

Consider exploring various partnership models, such as business partnerships, joint ventures, or strategic alliances, to increase your income. Platforms like income-partners.net can connect you with potential partnership opportunities.

10.3 What are the ongoing costs of owning a $2 million house?

Ongoing costs include property taxes (potentially $24,000+ annually), homeowners insurance, maintenance, utilities, landscaping, and cleaning services. These expenses can significantly impact your monthly budget.

10.4 Is it better to rent or buy a $2 million house?

The decision to rent or buy depends on your financial situation, lifestyle, and long-term goals. Buying a home offers potential appreciation and equity, but it also comes with significant upfront and ongoing costs. Renting provides flexibility but doesn’t offer the same financial benefits.

10.5 What is the 30/30/3 rule for home buying?

The 30/30/3 rule suggests spending no more than 30% of your gross monthly income on housing costs, having at least a 30% down payment, and buying a home that costs no more than 3 times your annual gross income.

10.6 How important is a cash buffer when buying a $2 million house?

A cash buffer is crucial for covering unexpected expenses or periods of unemployment. Aim for at least 5% of the home’s value as a cash reserve to provide financial security.

10.7 What are some alternative real estate investment options?

Consider real estate crowdfunding platforms like Fundrise and CrowdStreet, which allow you to invest in commercial and residential properties with smaller amounts of capital.

10.8 How can a real estate agent help me buy a $2 million house?

A real estate agent can guide you through the home buying process, negotiate on your behalf, and provide valuable insights into the local market. They can also help you find properties that meet your needs and budget.

10.9 What should I look for in a real estate crowdfunding platform?

Look for platforms with a strong track record, transparent fees, and a diversified portfolio of properties. Consider the investment minimums, potential returns, and the level of due diligence conducted on the properties.

10.10 How can I ensure financial security when owning a $2 million house?

Diversify your income streams, maintain job skills, build a strong network, and create a detailed budget to manage your expenses effectively. Avoid overextending yourself in the real estate market to minimize financial risk.

By understanding the income needed, the full costs involved, and alternative investment strategies, you can confidently pursue your dream of owning a $2 million house. Visit income-partners.net to explore partnership opportunities and connect with experts who can help you achieve your financial goals. Contact us at Address: 1 University Station, Austin, TX 78712, United States. Phone: +1 (512) 471-3434. Website: income-partners.net.

[