Are Ira Distributions Considered Earned Income? Understanding the nuances of IRA distributions and their impact on Social Security can be complex. At income-partners.net, we’re here to clarify how these distributions affect your eligibility for Social Security benefits and potential tax implications, ensuring you make informed financial decisions. Explore partnership opportunities and strategies for maximizing income with us.

1. Understanding the Basics of IRA Distributions and Earned Income

Are IRA distributions considered earned income? No, IRA distributions are generally not considered earned income for Social Security purposes. To fully grasp this, let’s break down what constitutes earned income and how it differs from other types of income like IRA distributions.

1.1 What is Earned Income?

Earned income is typically defined as income derived from active participation in a business or employment. This includes:

- Wages and salaries

- Tips

- Self-employment income

- Bonuses

According to the IRS, earned income is the compensation you receive for providing goods or services. This income is subject to both income tax and self-employment tax (if you’re self-employed).

1.2 What are IRA Distributions?

IRA distributions refer to the withdrawals you take from your Individual Retirement Account (IRA). There are two main types of IRAs:

- Traditional IRA: Contributions may be tax-deductible, and earnings grow tax-deferred until retirement. Distributions are taxed as ordinary income.

- Roth IRA: Contributions are made with after-tax dollars, and earnings grow tax-free. Qualified distributions in retirement are tax-free.

IRA distributions are typically considered unearned income because they represent the payout of previously accumulated savings and investment gains rather than current work or services rendered.

1.3 Key Differences Between Earned and Unearned Income

The crucial distinction lies in how the income is generated. Earned income comes from active work, while unearned income (like IRA distributions) comes from investments, savings, or other sources not directly tied to your labor.

| Feature | Earned Income | IRA Distributions |

|---|---|---|

| Source | Wages, salaries, self-employment | Retirement savings, investment gains |

| Tax Treatment | Subject to income tax and potentially self-employment tax | Subject to income tax (Traditional IRA) or tax-free (Roth IRA) |

| Social Security | Affects earnings test, may reduce benefits | Does not affect earnings test |

| Medicare Premiums | May impact premiums based on income levels | May impact premiums based on income levels |

Understanding these fundamental differences is essential for navigating the complexities of Social Security benefits and tax planning.

2. The Social Security Earnings Test and IRA Distributions

Are IRA distributions considered earned income when it comes to the Social Security earnings test? The Social Security earnings test is a crucial factor for those planning to claim Social Security benefits before reaching their full retirement age (FRA). Understanding how this test interacts with different income sources, including IRA distributions, is vital.

2.1 What is the Social Security Earnings Test?

The Social Security earnings test applies to individuals who claim Social Security benefits before their FRA. In 2024, if you are under FRA for the entire year, the Social Security Administration (SSA) will deduct $1 from your benefit for every $2 you earn above a certain limit ($22,320 in 2024). In the year you reach FRA, the deduction is $1 for every $3 earned above a different limit ($59,520 in 2024), but only earnings before the month you reach FRA are counted.

2.2 How Does the Earnings Test Affect Social Security Benefits?

The earnings test can significantly reduce your Social Security benefits if your earned income exceeds the threshold. However, it’s important to note that the earnings test only considers earned income. According to the SSA, this includes wages, self-employment income, and net earnings from a business.

2.3 IRA Distributions and the Earnings Test

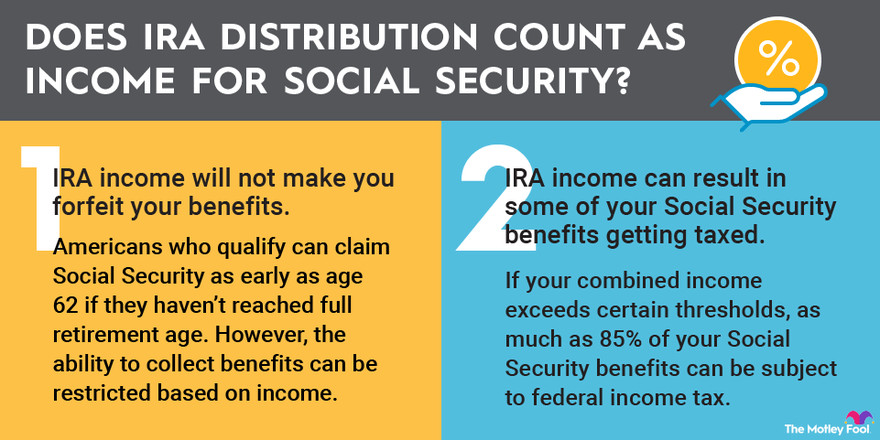

Are IRA distributions considered earned income under the earnings test? No, IRA distributions do not count as earned income under the Social Security earnings test. This means that taking distributions from your IRA will not reduce your Social Security benefits, provided that these distributions are not classified as earned income. This can be a significant advantage for retirees who need to supplement their income without affecting their Social Security benefits.

2.4 Strategies for Managing Income and Social Security Benefits

- Delay Social Security: One of the most effective strategies is to delay claiming Social Security until your FRA or even age 70. This maximizes your benefits and avoids the earnings test altogether.

- Roth IRA Contributions: Utilize Roth IRA accounts, as qualified distributions are tax-free and do not affect your AGI, thus not impacting the taxation of Social Security benefits.

- Careful Withdrawal Planning: Strategically plan your IRA withdrawals to minimize their impact on your overall tax liability.

- Seek Professional Advice: Consult with a financial advisor to develop a comprehensive retirement income plan that considers your specific circumstances and goals.

Understanding the Social Security earnings test and how different income sources are treated can help you optimize your retirement income and maximize your Social Security benefits.

3. Tax Implications of IRA Distributions on Social Security Benefits

Are IRA distributions considered earned income for tax purposes related to Social Security? While IRA distributions do not affect your eligibility for Social Security benefits under the earnings test, they can influence the amount of taxes you pay on those benefits. It’s essential to understand how different types of IRA distributions are treated for tax purposes and how they can impact your overall financial situation.

3.1 How Social Security Benefits are Taxed

The taxation of Social Security benefits depends on your combined income, which includes your adjusted gross income (AGI), nontaxable interest, and one-half of your Social Security benefits. The IRS uses these thresholds to determine how much of your Social Security benefits, if any, are subject to federal income tax.

3.2 Traditional IRA Distributions and Social Security Taxation

Traditional IRA distributions are generally included in your adjusted gross income (AGI). As a result, they can increase your combined income and potentially lead to a larger portion of your Social Security benefits being taxed. If your combined income exceeds the established thresholds, up to 85% of your Social Security benefits could be subject to federal income tax.

3.3 Roth IRA Distributions and Social Security Taxation

Roth IRA distributions offer a significant tax advantage. Qualified distributions from a Roth IRA are tax-free and are not included in your AGI. Therefore, Roth IRA distributions do not increase your combined income and do not cause your Social Security benefits to be taxed. This can be a valuable tool for managing your tax liability in retirement.

3.4 Strategies to Minimize Taxes on Social Security Benefits

- Roth Conversions: Consider converting traditional IRA assets to a Roth IRA. While you’ll pay taxes on the converted amount in the year of the conversion, future qualified distributions will be tax-free and will not affect the taxation of your Social Security benefits.

- Tax-Efficient Investments: Invest in tax-efficient assets that generate minimal taxable income.

- Withdrawal Planning: Strategically plan your withdrawals from various accounts to minimize your overall tax liability.

- Consult a Tax Professional: Work with a tax professional to develop a comprehensive tax plan that optimizes your retirement income and minimizes taxes on your Social Security benefits.

Understanding the tax implications of IRA distributions on Social Security benefits can help you make informed financial decisions and manage your tax liability effectively in retirement.

4. Planning for Retirement: Integrating IRA Distributions and Social Security

Are IRA distributions considered earned income in the context of long-term retirement planning? Integrating IRA distributions and Social Security into a cohesive retirement plan is crucial for ensuring financial security and maximizing your income. Here’s how to effectively plan for retirement by considering these two essential components.

4.1 Assessing Your Retirement Income Needs

The first step in retirement planning is to assess your income needs. This involves estimating your expenses, including housing, healthcare, food, transportation, and other living costs. It’s also important to factor in inflation and potential unexpected expenses.

4.2 Estimating Your Social Security Benefits

You can estimate your Social Security benefits by using the Social Security Administration’s (SSA) online calculator or by reviewing your Social Security statement. Keep in mind that the amount of your benefits will depend on your earnings history and the age at which you claim benefits.

4.3 Determining Your IRA Distribution Strategy

Based on your income needs and estimated Social Security benefits, you can determine how much you need to withdraw from your IRA each year. Consider the tax implications of different types of IRA distributions (traditional vs. Roth) and how they might affect your overall tax liability.

4.4 Creating a Comprehensive Retirement Plan

A comprehensive retirement plan should integrate your Social Security benefits, IRA distributions, and other sources of income, such as pensions, annuities, and investment accounts. The plan should also address your risk tolerance, investment strategy, and long-term financial goals.

4.5 Seeking Professional Financial Advice

Retirement planning can be complex, so it’s often beneficial to seek professional financial advice. A qualified financial advisor can help you assess your income needs, estimate your Social Security benefits, develop an appropriate IRA distribution strategy, and create a comprehensive retirement plan that meets your specific needs and goals.

4.6 Case Studies and Examples

To illustrate how IRA distributions and Social Security can be integrated into a retirement plan, let’s consider a few case studies:

Case Study 1: John, 65, plans to retire and needs $60,000 per year to cover his expenses. He estimates his Social Security benefits will be $30,000 per year. He needs to withdraw $30,000 from his traditional IRA to meet his income needs.

Case Study 2: Mary, 62, wants to retire but is concerned about taxes. She estimates her Social Security benefits will be $25,000 per year. She decides to convert some of her traditional IRA assets to a Roth IRA to minimize her tax liability in retirement.

Case Study 3: David, 70, has delayed claiming Social Security to maximize his benefits. He now receives $40,000 per year from Social Security and withdraws $20,000 from his Roth IRA to cover his expenses. His Roth IRA distributions are tax-free and do not affect the taxation of his Social Security benefits.

These case studies demonstrate how different individuals can integrate IRA distributions and Social Security into their retirement plans based on their specific needs and circumstances.

Planning for retirement requires careful consideration of various factors, including your income needs, Social Security benefits, IRA distributions, and tax implications. By creating a comprehensive retirement plan and seeking professional financial advice, you can ensure a financially secure and fulfilling retirement.

5. Common Misconceptions About IRA Distributions and Social Security

Are IRA distributions considered earned income based on common public understanding? There are several common misconceptions about how IRA distributions interact with Social Security. Clarifying these misunderstandings is essential for making informed financial decisions and avoiding potential pitfalls.

5.1 Misconception 1: IRA Distributions Reduce Social Security Benefits

Reality: As discussed earlier, IRA distributions do not directly reduce your Social Security benefits under the earnings test. The earnings test only applies to earned income, such as wages and self-employment income.

5.2 Misconception 2: All IRA Distributions are Tax-Free

Reality: While Roth IRA distributions are generally tax-free, traditional IRA distributions are subject to income tax. The tax treatment of IRA distributions depends on the type of IRA and whether the distributions are considered qualified.

5.3 Misconception 3: You Can’t Contribute to an IRA if You’re Receiving Social Security

Reality: There is no age limit for contributing to a traditional IRA as long as you have earned income. You can continue to contribute to an IRA even if you are receiving Social Security benefits, provided that you meet the earned income requirements.

5.4 Misconception 4: IRA Distributions Don’t Affect Medicare Premiums

Reality: IRA distributions can affect your Medicare premiums. Medicare Part B and Part D premiums are income-based, meaning that if your income exceeds certain thresholds, you may have to pay higher premiums.

5.5 Misconception 5: Roth IRAs are Always Better Than Traditional IRAs

Reality: The choice between a Roth IRA and a traditional IRA depends on your individual circumstances and tax situation. A Roth IRA may be more beneficial if you expect to be in a higher tax bracket in retirement, while a traditional IRA may be more advantageous if you expect to be in a lower tax bracket.

5.6 Examples of Misconceptions in Practice

- Example 1: A retiree believes that taking distributions from their traditional IRA will reduce their Social Security benefits, so they avoid taking withdrawals and struggle to meet their expenses.

- Example 2: An individual assumes that all of their IRA distributions will be tax-free, so they don’t plan for taxes and are surprised when they receive a tax bill.

- Example 3: Someone thinks that they can no longer contribute to an IRA because they are receiving Social Security benefits and miss out on the opportunity to continue saving for retirement.

Understanding these common misconceptions and the realities behind them can help you make more informed financial decisions and avoid potential pitfalls in retirement planning.

6. Strategies for Maximizing Retirement Income

Are IRA distributions considered earned income, and how can this knowledge inform strategies to maximize retirement income? Maximizing your retirement income involves a combination of strategic planning, informed decision-making, and leveraging various resources. Here are some effective strategies to help you optimize your retirement income:

6.1 Delay Claiming Social Security

Delaying claiming Social Security benefits can significantly increase your monthly payments. For each year you delay claiming benefits beyond your full retirement age (up to age 70), your benefits will increase by approximately 8%. This can result in a substantial boost to your retirement income.

6.2 Optimize IRA Distributions

Carefully plan your IRA distributions to minimize your tax liability. Consider converting traditional IRA assets to a Roth IRA to take advantage of tax-free distributions in retirement. Also, be mindful of the tax implications of traditional IRA distributions and how they may affect the taxation of your Social Security benefits.

6.3 Consider Annuities

Annuities can provide a guaranteed stream of income in retirement. There are various types of annuities, including fixed annuities, variable annuities, and immediate annuities. Consider your risk tolerance and income needs when choosing an annuity.

6.4 Manage Investment Risk

Maintain a diversified investment portfolio that aligns with your risk tolerance and retirement goals. Regularly review and rebalance your portfolio to ensure it continues to meet your needs.

6.5 Work Part-Time

Working part-time in retirement can provide additional income and help you stay active and engaged. Consider pursuing a part-time job in a field you enjoy or starting a small business.

6.6 Reduce Expenses

Reducing your expenses can free up more of your income for other purposes. Look for ways to cut back on unnecessary spending and find more affordable alternatives.

6.7 Leverage Home Equity

If you own a home, you may be able to leverage your home equity to generate additional income. Consider options such as downsizing, renting out a room, or taking out a reverse mortgage.

6.8 Examples of Successful Retirement Income Maximization

- Example 1: A retiree delays claiming Social Security until age 70 and receives a significantly higher monthly payment.

- Example 2: An individual converts traditional IRA assets to a Roth IRA and enjoys tax-free distributions in retirement.

- Example 3: Someone starts a small business in retirement and generates additional income while staying active and engaged.

By implementing these strategies, you can maximize your retirement income and enjoy a financially secure and fulfilling retirement.

7. Resources for Further Information

Are IRA distributions considered earned income, and where can individuals find reliable resources for more detailed information? Navigating the complexities of IRA distributions and their impact on Social Security requires access to reliable and comprehensive resources. Here are several valuable sources of information to help you deepen your understanding and make informed decisions:

7.1 Social Security Administration (SSA)

The SSA website (ssa.gov) is an excellent resource for information about Social Security benefits, the earnings test, and how different types of income affect your benefits. You can also use the SSA’s online calculator to estimate your Social Security benefits.

7.2 Internal Revenue Service (IRS)

The IRS website (irs.gov) provides detailed information about IRA distributions, tax rules, and other retirement-related topics. You can also find publications and forms to help you understand your tax obligations.

7.3 Financial Institutions

Many financial institutions offer educational resources and tools to help you plan for retirement and manage your IRA. Check with your bank, brokerage firm, or insurance company for information and assistance.

7.4 Professional Financial Advisors

A qualified financial advisor can provide personalized advice and guidance to help you develop a comprehensive retirement plan that meets your specific needs and goals. Look for a financial advisor who is experienced in retirement planning and familiar with IRA distributions and Social Security.

7.5 Books and Publications

There are many books and publications available on retirement planning and IRA distributions. Look for reputable sources that provide accurate and up-to-date information.

7.6 Online Forums and Communities

Online forums and communities can be a valuable source of information and support. You can connect with other retirees and financial professionals to share insights and ask questions.

7.7 Examples of Informative Resources

- SSA Publication: “Retirement Benefits”

- IRS Publication 590-B: “Distributions from Individual Retirement Arrangements (IRAs)”

- Websites like Investopedia, The Motley Fool, and Kiplinger

By utilizing these resources, you can gain a deeper understanding of IRA distributions and their impact on Social Security and make more informed decisions about your retirement planning.

8. Partnering for Success: How Income-Partners.net Can Help

Are IRA distributions considered earned income, and how can income-partners.net assist in optimizing financial strategies related to this knowledge? At income-partners.net, we understand the intricacies of retirement planning and the importance of making informed decisions about your financial future. While we don’t provide direct financial advice, we offer a unique platform to connect you with potential partners who can help you navigate these complexities and achieve your financial goals.

8.1 Connecting You with Financial Professionals

Through our platform, you can find and connect with financial advisors, tax professionals, and other experts who can provide personalized guidance on retirement planning, IRA distributions, and Social Security. These professionals can help you assess your income needs, develop an appropriate IRA distribution strategy, and minimize your tax liability.

8.2 Offering Strategic Partnership Opportunities

income-partners.net also provides opportunities to connect with businesses and individuals who offer retirement-related products and services, such as insurance companies, annuity providers, and investment firms. Partnering with these organizations can help you access valuable resources and solutions to enhance your retirement income.

8.3 Providing Educational Resources

While we are not a direct source of financial education, we curate and share valuable articles, guides, and resources from reputable sources to help you stay informed about the latest trends and strategies in retirement planning.

8.4 Case Studies of Successful Partnerships

- Case Study 1: A retiree connects with a financial advisor through income-partners.net and develops a comprehensive retirement plan that integrates their Social Security benefits, IRA distributions, and other sources of income.

- Case Study 2: An individual partners with an insurance company through income-partners.net and purchases an annuity to provide a guaranteed stream of income in retirement.

- Case Study 3: A business that offers retirement planning services connects with potential clients through income-partners.net and expands its reach and impact.

8.5 Taking Action: How to Get Started with Income-Partners.net

Ready to explore how income-partners.net can help you achieve your retirement goals? Here are a few steps to get started:

- Visit our website: Go to income-partners.net to learn more about our platform and the services we offer.

- Explore partnership opportunities: Browse our directory of partners and connect with businesses and individuals who can help you with your retirement planning needs.

- Access educational resources: Check out our blog and resource library for valuable articles, guides, and tips on retirement planning and IRA distributions.

- Contact us: If you have any questions or need assistance, don’t hesitate to contact us. We’re here to help you succeed.

At income-partners.net, we’re committed to empowering you to make informed financial decisions and achieve your retirement goals. While we don’t provide direct financial advice, we offer a valuable platform to connect you with the resources and partners you need to thrive in retirement.

A graphic illustrating the connection between IRA distributions and Social Security benefits.

A graphic illustrating the connection between IRA distributions and Social Security benefits.

9. Real-Life Examples and Scenarios

Are IRA distributions considered earned income, and how does this understanding apply in real-life scenarios? To further illustrate the principles discussed, let’s explore some real-life examples and scenarios that demonstrate how IRA distributions interact with Social Security in various situations:

9.1 Scenario 1: Early Retirement with Traditional IRA Distributions

Situation: John, 62, retires early and starts taking distributions from his traditional IRA to supplement his income before claiming Social Security.

Analysis: John’s IRA distributions are not considered earned income and do not affect his eligibility for Social Security benefits. However, the distributions are taxable and may increase his combined income, potentially leading to a larger portion of his Social Security benefits being taxed when he starts claiming them.

9.2 Scenario 2: Maximizing Social Security with Roth IRA Distributions

Situation: Mary, 65, delays claiming Social Security until age 70 to maximize her benefits. She takes distributions from her Roth IRA to cover her expenses while waiting.

Analysis: Mary’s Roth IRA distributions are tax-free and do not affect her Social Security benefits. By delaying claiming Social Security and using Roth IRA distributions, she maximizes her retirement income and minimizes her tax liability.

9.3 Scenario 3: Part-Time Work and IRA Distributions

Situation: David, 68, works part-time and receives a salary in addition to taking distributions from his traditional IRA.

Analysis: David’s salary is considered earned income and may affect his Social Security benefits if he claims them before his full retirement age. However, his IRA distributions are not considered earned income and do not affect his eligibility for Social Security benefits.

9.4 Scenario 4: Medicare Premiums and IRA Distributions

Situation: Susan, 72, takes large distributions from her traditional IRA, which significantly increases her income.

Analysis: Susan’s higher income may result in increased Medicare Part B and Part D premiums. Medicare premiums are income-based, so higher income can lead to higher premiums.

9.5 Scenario 5: Roth Conversion Strategy

Situation: Tom, 55, decides to convert a portion of his traditional IRA to a Roth IRA to minimize his tax liability in retirement.

Analysis: Tom will pay taxes on the converted amount in the year of the conversion, but future qualified distributions from the Roth IRA will be tax-free and will not affect the taxation of his Social Security benefits.

These real-life examples demonstrate how IRA distributions and Social Security interact in various situations. By understanding these principles, you can make more informed decisions about your retirement planning and maximize your retirement income.

10. Frequently Asked Questions (FAQ)

Are IRA distributions considered earned income, and what are the most common questions surrounding this topic? Here are some frequently asked questions (FAQ) about IRA distributions and their impact on Social Security, along with detailed answers to address your concerns:

10.1 Do IRA distributions reduce my Social Security benefits?

No, IRA distributions do not directly reduce your Social Security benefits under the earnings test. The earnings test only applies to earned income, such as wages and self-employment income.

10.2 Are IRA distributions taxable?

The tax treatment of IRA distributions depends on the type of IRA. Traditional IRA distributions are generally taxable, while qualified Roth IRA distributions are tax-free.

10.3 Can I contribute to an IRA if I’m receiving Social Security benefits?

Yes, there is no age limit for contributing to a traditional IRA as long as you have earned income. You can continue to contribute to an IRA even if you are receiving Social Security benefits, provided that you meet the earned income requirements.

10.4 Do IRA distributions affect my Medicare premiums?

Yes, IRA distributions can affect your Medicare premiums. Medicare Part B and Part D premiums are income-based, meaning that if your income exceeds certain thresholds, you may have to pay higher premiums.

10.5 What is the difference between a traditional IRA and a Roth IRA?

Traditional IRA contributions may be tax-deductible, and earnings grow tax-deferred until retirement. Distributions are taxed as ordinary income. Roth IRA contributions are made with after-tax dollars, and earnings grow tax-free. Qualified distributions in retirement are tax-free.

10.6 Should I convert my traditional IRA to a Roth IRA?

The decision to convert a traditional IRA to a Roth IRA depends on your individual circumstances and tax situation. A Roth IRA may be more beneficial if you expect to be in a higher tax bracket in retirement, while a traditional IRA may be more advantageous if you expect to be in a lower tax bracket.

10.7 How can I minimize taxes on my IRA distributions?

Consider converting traditional IRA assets to a Roth IRA, taking advantage of tax-efficient investments, and strategically planning your withdrawals from various accounts to minimize your overall tax liability.

10.8 Where can I find more information about IRA distributions and Social Security?

You can find more information on the Social Security Administration (SSA) website (ssa.gov), the Internal Revenue Service (IRS) website (irs.gov), and from qualified financial advisors.

10.9 What is the Social Security earnings test?

The Social Security earnings test applies to individuals who claim Social Security benefits before their full retirement age (FRA). The Social Security Administration (SSA) will deduct $1 from your benefit for every $2 you earn above a certain limit ($22,320 in 2024).

10.10 How does the Social Security earnings test affect my benefits?

The earnings test can significantly reduce your Social Security benefits if your earned income exceeds the threshold. However, it’s important to note that the earnings test only considers earned income.

These FAQs provide valuable information to help you understand the complexities of IRA distributions and their impact on Social Security.

Understanding whether are IRA distributions considered earned income is crucial for effective retirement planning. While IRA distributions don’t affect your Social Security eligibility under the earnings test, they can impact the taxation of your benefits. By making informed decisions and strategically planning your income sources, you can maximize your retirement income and ensure financial security.

At income-partners.net, we encourage you to explore partnership opportunities and connect with financial professionals who can provide personalized guidance. Visit our website at income-partners.net to discover how we can help you achieve your retirement goals and build a prosperous future. Let us help you find the partners you need to succeed.