Understanding your income tax return, specifically Form 1040, is essential for effective financial planning and maximizing potential partnerships; income-partners.net is here to guide you. This comprehensive guide will help you decipher each section of the form, ensure accuracy, and optimize your tax strategy, leading to potential income growth. Let’s unlock the secrets of tax form comprehension, tax return analysis, and tax planning strategies together.

1. Why Understanding Form 1040 Matters

Do you want to take control of your finances and maximize potential business partnerships? Understanding your Form 1040 is essential. It’s not just about filing taxes; it’s about gaining insights into your financial health and making informed decisions that can boost your income.

Understanding Form 1040 matters because it enables you to verify the accuracy of your return, identify potential tax-saving opportunities, and make informed financial decisions. According to the IRS, a significant percentage of tax returns contain errors, highlighting the importance of personal review. By understanding your Form 1040, you can ensure that you are not overpaying or underpaying your taxes. This knowledge empowers you to take proactive steps to optimize your financial situation and potentially uncover new avenues for income generation through strategic partnerships facilitated by platforms like income-partners.net.

1.1 Accuracy Verification

Is ensuring your tax return is accurate your top priority? Form 1040 is the key. By understanding each line, you can verify the reported income, deductions, and credits, preventing errors that could lead to overpayment or penalties.

Verifying the accuracy of your tax return is crucial. Mistakes can lead to penalties, missed deductions, or even audits. According to the Taxpayer Advocate Service, a significant number of tax returns contain errors, often due to misunderstanding of tax laws or incorrect data entry. Reviewing your Form 1040 line by line allows you to cross-reference the information with your records, ensuring that all income, deductions, and credits are correctly reported. This careful verification process not only minimizes the risk of errors but also provides a deeper understanding of your financial situation, which is valuable for identifying potential areas for improvement and strategic partnerships.

1.2 Financial Insights

Can Form 1040 provide insights into your financial well-being? Absolutely! It offers a clear snapshot of your income sources, deductions, and tax liability, helping you identify areas for improvement and make informed financial decisions to improve your financial health.

Form 1040 provides a comprehensive overview of your financial landscape. By analyzing your income sources, deductions, and tax liability, you can gain valuable insights into your financial strengths and weaknesses. For instance, understanding your income sources can help you identify opportunities to diversify your revenue streams, potentially through strategic partnerships offered on platforms like income-partners.net. Similarly, analyzing your deductions can reveal areas where you can optimize your tax strategy and reduce your overall tax burden. This holistic view of your finances empowers you to make informed decisions, such as adjusting your investment strategy, increasing contributions to tax-advantaged accounts, or seeking professional financial advice to maximize your financial well-being.

1.3 Strategic Tax Planning

Want to optimize your tax strategy? Form 1040 is essential. It provides the information needed to identify potential deductions, credits, and other tax-saving opportunities, allowing you to minimize your tax liability and maximize your after-tax income.

Strategic tax planning is essential for minimizing your tax liability and maximizing your after-tax income. Form 1040 serves as a roadmap for identifying potential deductions, credits, and other tax-saving opportunities that you may be eligible for. For instance, understanding the eligibility criteria for various tax credits, such as the Earned Income Tax Credit or the Child Tax Credit, can help you claim these benefits and reduce your overall tax burden. Similarly, identifying potential deductions, such as deductions for student loan interest or contributions to retirement accounts, can further lower your taxable income and minimize your tax liability. By leveraging the information on Form 1040, you can proactively plan your tax strategy, make informed financial decisions, and potentially free up resources for investment or business partnerships that can further enhance your income potential.

2. Key Sections of Form 1040

What are the core components of Form 1040 that you need to understand? Form 1040 is composed of several key sections, including Personal Information, Income, Adjusted Gross Income (AGI), Deductions, Tax Liability, and Payments.

Form 1040 is structured to provide a comprehensive overview of your financial situation, and each section plays a vital role in determining your tax liability. Let’s break down these key sections:

2.1 Personal Information

Why is the personal information section important? This section collects essential details like your name, Social Security number, and filing status, which are vital for accurate processing and claiming the correct deductions and credits.

The Personal Information section is the foundation of your tax return. Accurate information here ensures that your return is properly processed and that you receive all the deductions and credits you are entitled to.

- Full Name and Social Security Number: These details uniquely identify you to the IRS. Incorrect information can lead to processing delays or even rejection of your return.

- Filing Status: Your filing status (Single, Married Filing Jointly, Married Filing Separately, Head of Household, or Qualifying Widow(er)) determines your standard deduction, tax bracket, and eligibility for certain credits. Selecting the correct filing status is crucial for minimizing your tax liability.

2.2 Income

What types of income are reported on Form 1040? This section encompasses various income sources, including wages, salaries, interest, dividends, retirement distributions, and Social Security benefits.

The Income section of Form 1040 consolidates all your taxable income sources. Understanding what to include here is critical for accurate tax reporting.

- Wages, Salaries, and Tips (Line 1): This includes all taxable compensation you receive from employment, as reported on Form W-2.

- Interest Income (Line 2): This includes taxable interest earned from bank accounts, bonds, and other investments, as reported on Form 1099-INT.

- Dividend Income (Line 3): This includes dividends received from stocks, mutual funds, and other investments, as reported on Form 1099-DIV. Qualified dividends are taxed at a lower rate than ordinary income.

- IRA Distributions (Line 4): This includes distributions from traditional IRAs, as reported on Form 1099-R. The taxable amount depends on whether the contributions were pre-tax or after-tax.

- Pensions and Annuities (Line 5): This includes distributions from pensions, annuities, and 401(k) plans, as reported on Form 1099-R.

- Social Security Benefits (Line 6): This includes Social Security retirement, disability, and survivor benefits, as reported on Form SSA-1099. The taxable amount depends on your total income.

- Capital Gains and Losses (Line 7): This includes gains and losses from the sale of stocks, bonds, and other capital assets. These are reported on Schedule D.

- Other Income (Line 8): This includes various other types of income, such as rental income, royalties, and alimony received. These are reported on Schedule 1.

Form 1040

Form 1040

2.3 Adjusted Gross Income (AGI)

What is Adjusted Gross Income (AGI) and why is it important? AGI is your gross income minus certain deductions, and it’s a key factor in determining eligibility for various deductions and credits.

Adjusted Gross Income (AGI) is a critical figure on your tax return because it serves as a benchmark for determining your eligibility for various deductions and credits.

- Calculation: AGI is calculated by subtracting certain deductions from your gross income. These deductions can include contributions to health savings accounts (HSAs), student loan interest payments, and self-employment taxes.

- Impact on Deductions and Credits: Many deductions and credits have income limitations, meaning that your AGI must be below a certain threshold to qualify. For example, the ability to deduct IRA contributions or claim certain education credits may be limited based on your AGI.

- Tax Planning: Keeping your AGI as low as possible can help you maximize your eligibility for deductions and credits, ultimately reducing your tax liability.

2.4 Deductions

What are the two main types of deductions? You can choose between the standard deduction, which is a fixed amount based on your filing status, or itemized deductions, which include expenses like medical expenses, state and local taxes (SALT), and charitable contributions.

The Deductions section of Form 1040 allows you to reduce your taxable income, ultimately lowering your tax liability. You have two main options:

-

Standard Deduction (Line 12a): This is a fixed amount based on your filing status. For the 2023 tax year, the standard deduction amounts are:

- Single: $13,850

- Married Filing Jointly: $27,700

- Head of Household: $20,800

-

Itemized Deductions (Schedule A): If your itemized deductions exceed the standard deduction, you can choose to itemize. Common itemized deductions include:

- Medical Expenses: You can deduct medical expenses that exceed 7.5% of your AGI.

- State and Local Taxes (SALT): You can deduct up to $10,000 in state and local taxes, including property taxes and either state income taxes or sales taxes.

- Charitable Contributions: You can deduct contributions to qualified charitable organizations.

- Home Mortgage Interest: You can deduct interest paid on a home mortgage, subject to certain limitations.

2.5 Tax Liability

How is your tax liability calculated? This section calculates the amount of tax you owe based on your taxable income and the applicable tax rates.

The Tax Liability section is where your tax is calculated based on your taxable income. Understanding how this works is crucial for tax planning.

- Taxable Income (Line 15): This is your AGI minus your deductions.

- Tax Calculation (Line 16): Your tax liability is calculated based on your taxable income and the applicable tax rates for your filing status.

- Tax Credits (Lines 19-20): Tax credits directly reduce your tax liability. Common tax credits include the Child Tax Credit, the Earned Income Tax Credit, and education credits.

2.6 Payments

What types of payments and credits are included in this section? This section includes tax payments made during the year, such as withholding from wages and estimated tax payments, as well as refundable tax credits.

The Payments section of Form 1040 summarizes all the tax payments you made during the year and any refundable credits you are eligible for.

- Withholding (Lines 25a-c): This includes federal income tax withheld from your wages, pensions, and other sources, as reported on Forms W-2 and 1099.

- Estimated Tax Payments (Line 26): If you are self-employed or have other income that is not subject to withholding, you may need to make estimated tax payments throughout the year.

- Refundable Credits (Line 31): Refundable credits can reduce your tax liability to zero, and if the credit exceeds your tax liability, you will receive a refund for the difference. Common refundable credits include the Earned Income Tax Credit and the Additional Child Tax Credit.

3. Understanding Schedules

Are you familiar with the schedules that accompany Form 1040? Schedules provide detailed information about specific income, deductions, and credits. Common schedules include Schedule 1, Schedule A, and Schedule D.

Schedules are supplementary forms that provide detailed information supporting the amounts reported on Form 1040. They are essential for accurately reporting specific types of income, deductions, and credits.

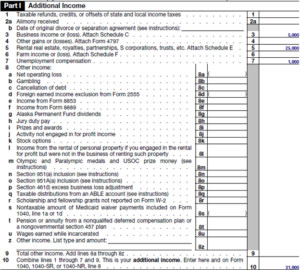

3.1 Schedule 1: Additional Income and Adjustments to Income

What is reported on Schedule 1? This schedule reports additional income not included on Form 1040, such as self-employment income, rental income, and alimony received, as well as adjustments to income, such as student loan interest and self-employment tax.

Schedule 1 is used to report additional income and adjustments to income that are not directly included on Form 1040.

- Part I: Additional Income:

- Business Income or Loss (Line 3): This includes income or loss from a business you operate as a sole proprietor, reported on Schedule C.

- Rental Real Estate, Royalties, and Partnerships (Line 5): This includes income or loss from rental properties, royalties, and partnerships, reported on Schedule E.

- Unemployment Compensation (Line 7): This includes unemployment benefits received during the year.

- Other Income (Line 8): This includes various other types of income, such as gambling winnings and prizes.

- Part II: Adjustments to Income:

- Educator Expenses (Line 11): Eligible educators can deduct up to $300 of unreimbursed educator expenses.

- Self-Employment Tax (Line 15): You can deduct one-half of your self-employment tax.

- Self-Employed Health Insurance Deduction (Line 16): Self-employed individuals can deduct the amount they paid for health insurance coverage.

- IRA Deduction (Line 20): You can deduct contributions to a traditional IRA, subject to certain limitations.

- Student Loan Interest Deduction (Line 21): You can deduct student loan interest payments, up to a maximum of $2,500 per year.

- HSA Deduction (Line 12): You can deduct contributions made to health savings accounts (HSA).

Schedule 1

Schedule 1

3.2 Schedule A: Itemized Deductions

When should you use Schedule A? Use Schedule A to itemize deductions if your itemized deductions exceed the standard deduction for your filing status.

Schedule A is used to itemize deductions, which can reduce your taxable income if they exceed the standard deduction.

- Medical Expenses (Lines 1-4): You can deduct medical expenses that exceed 7.5% of your AGI.

- State and Local Taxes (SALT) (Lines 5a-5e): You can deduct up to $10,000 in state and local taxes, including property taxes and either state income taxes or sales taxes.

- Home Mortgage Interest (Lines 8a-8c): You can deduct interest paid on a home mortgage, subject to certain limitations.

- Charitable Contributions (Lines 11-14): You can deduct contributions to qualified charitable organizations.

3.3 Schedule D: Capital Gains and Losses

What is the purpose of Schedule D? Schedule D reports capital gains and losses from the sale of stocks, bonds, and other capital assets.

Schedule D is used to report capital gains and losses from the sale of stocks, bonds, and other capital assets.

- Short-Term Capital Gains and Losses: These are gains and losses from assets held for one year or less.

- Long-Term Capital Gains and Losses: These are gains and losses from assets held for more than one year. Long-term capital gains are taxed at lower rates than ordinary income.

- Capital Loss Deduction: If your capital losses exceed your capital gains, you can deduct up to $3,000 of the excess loss per year.

4. Common Mistakes to Avoid

What are some common errors to watch out for when preparing your tax return? Common mistakes include incorrect Social Security numbers, misreporting income, and overlooking eligible deductions and credits.

Avoiding common mistakes is crucial for ensuring the accuracy of your tax return and minimizing the risk of penalties.

4.1 Incorrect Social Security Numbers

Why is it important to double-check Social Security numbers? Incorrect Social Security numbers can cause processing delays or even rejection of your tax return.

Incorrect Social Security numbers can lead to significant problems with your tax return, including:

- Processing Delays: The IRS uses Social Security numbers to match your tax return to your account. An incorrect number can cause delays in processing your return.

- Rejection of Return: If the Social Security number does not match IRS records, your return may be rejected altogether.

- Identity Theft: While not directly related to tax preparation, providing an incorrect Social Security number could potentially expose you to identity theft risks.

4.2 Misreporting Income

What happens if you don’t report all of your income? Failing to report all income can result in penalties and interest charges.

Misreporting income, whether intentional or unintentional, can have serious consequences:

- Penalties: The IRS may impose penalties for underreporting income. These penalties can be substantial, often amounting to a percentage of the unpaid tax.

- Interest Charges: In addition to penalties, the IRS will charge interest on any unpaid tax.

- Audit: Underreporting income can increase your chances of being audited by the IRS.

4.3 Overlooking Deductions and Credits

Are you taking advantage of all eligible deductions and credits? Overlooking eligible deductions and credits can result in paying more tax than necessary.

Failing to claim all eligible deductions and credits can result in a higher tax liability. Some commonly overlooked deductions and credits include:

- Earned Income Tax Credit (EITC): This credit is available to low- to moderate-income workers and families.

- Child Tax Credit: This credit is available for qualifying children under age 17.

- Child and Dependent Care Credit: This credit is available for expenses paid for the care of a qualifying child or other dependent so that you can work or look for work.

- Education Credits: The American Opportunity Tax Credit and the Lifetime Learning Credit are available for qualified education expenses.

- IRA Deduction: Contributions to a traditional IRA may be deductible, subject to certain limitations.

- Student Loan Interest Deduction: You can deduct student loan interest payments, up to a maximum of $2,500 per year.

5. Tax Planning Tips for Increased Income

How can you use tax planning to increase your income? Strategic tax planning can help you minimize your tax liability and free up resources for investments or business ventures.

Tax planning is not just about filing your taxes; it’s about making strategic decisions throughout the year to minimize your tax liability and maximize your income potential.

5.1 Maximize Retirement Contributions

Why should you contribute to retirement accounts? Contributing to retirement accounts like 401(k)s and IRAs can reduce your taxable income and provide long-term savings.

Contributing to retirement accounts offers several tax benefits:

- Tax-Deductible Contributions: Contributions to traditional 401(k)s and traditional IRAs are typically tax-deductible, reducing your taxable income in the year of the contribution.

- Tax-Deferred Growth: Your investments grow tax-deferred, meaning you don’t pay taxes on the earnings until you withdraw them in retirement.

- Potential for Higher Income: By reducing your current tax liability, you can free up resources for investments or business ventures that can potentially increase your income.

5.2 Utilize Health Savings Accounts (HSAs)

What are the benefits of using an HSA? HSAs offer tax advantages for healthcare expenses, including tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses.

Health Savings Accounts (HSAs) offer a triple tax advantage:

- Tax-Deductible Contributions: Contributions to an HSA are tax-deductible, reducing your taxable income.

- Tax-Free Growth: Your investments grow tax-free.

- Tax-Free Withdrawals: Withdrawals for qualified medical expenses are tax-free.

5.3 Consider Tax-Loss Harvesting

What is tax-loss harvesting and how does it work? Tax-loss harvesting involves selling investments at a loss to offset capital gains, reducing your overall tax liability.

Tax-loss harvesting is a strategy that involves selling investments at a loss to offset capital gains, thereby reducing your tax liability.

- Offsetting Capital Gains: Capital losses can be used to offset capital gains, reducing the amount of capital gains tax you owe.

- Deducting Excess Losses: If your capital losses exceed your capital gains, you can deduct up to $3,000 of the excess loss per year.

- Rebalancing Portfolio: Tax-loss harvesting can also be used to rebalance your portfolio, allowing you to maintain your desired asset allocation while minimizing your tax liability.

6. Leveraging Partnerships for Income Growth

What role do strategic partnerships play in growing your income? Partnerships can provide access to new markets, resources, and expertise, leading to increased revenue and profitability.

Leveraging partnerships is a powerful strategy for accelerating income growth. By collaborating with other businesses or individuals, you can tap into new opportunities and resources that would otherwise be out of reach.

6.1 Types of Partnerships

What are the different types of partnerships you can explore? Common types include strategic alliances, joint ventures, and affiliate partnerships, each offering unique benefits.

Exploring different types of partnerships can unlock various opportunities for income growth. Here are some common types:

- Strategic Alliances: These partnerships involve collaborating with other businesses to achieve mutual goals, such as expanding market reach or developing new products.

- Joint Ventures: These partnerships involve creating a new entity to pursue a specific project or business opportunity.

- Affiliate Partnerships: These partnerships involve promoting another company’s products or services in exchange for a commission on sales.

6.2 Finding the Right Partners

How can you identify and connect with the right partners? Platforms like income-partners.net can help you find potential partners whose goals align with yours.

Finding the right partners is crucial for the success of any collaborative venture. income-partners.net can help you identify potential partners whose goals align with yours.

- Networking: Attend industry events and conferences to meet potential partners.

- Online Platforms: Utilize online platforms like income-partners.net to search for partners based on industry, expertise, and goals.

- Due Diligence: Before entering into a partnership, conduct thorough due diligence to ensure that the partner is reputable and has a track record of success.

6.3 Structuring Partnership Agreements

What key elements should be included in a partnership agreement? Agreements should clearly define roles, responsibilities, profit-sharing arrangements, and dispute resolution mechanisms.

A well-structured partnership agreement is essential for ensuring that all parties are on the same page and that the partnership operates smoothly.

- Roles and Responsibilities: Clearly define the roles and responsibilities of each partner.

- Profit-Sharing Arrangements: Specify how profits will be shared among the partners.

- Dispute Resolution Mechanisms: Include a process for resolving disputes that may arise during the partnership.

7. Resources and Tools

What resources and tools can help you with tax preparation and planning? The IRS website, tax software, and professional tax advisors can provide valuable assistance.

Navigating the complexities of tax preparation and planning can be challenging, but fortunately, there are numerous resources and tools available to help you.

7.1 IRS Website

What information can you find on the IRS website? The IRS website provides access to tax forms, publications, and educational resources.

The IRS website (irs.gov) is a comprehensive resource for all things tax-related.

- Tax Forms and Publications: You can download all the necessary tax forms and publications from the IRS website.

- Educational Resources: The IRS website offers a variety of educational resources, including FAQs, tutorials, and webinars.

- Online Tools: The IRS website provides access to online tools, such as the Interactive Tax Assistant, which can help you answer tax questions.

7.2 Tax Software

What are the benefits of using tax software? Tax software can simplify tax preparation, provide guidance, and help you identify potential deductions and credits.

Tax software can greatly simplify the tax preparation process.

- Step-by-Step Guidance: Tax software provides step-by-step guidance, making it easier to complete your tax return accurately.

- Deduction and Credit Identification: Tax software can help you identify potential deductions and credits that you may be eligible for.

- Error Checking: Tax software automatically checks for errors, reducing the risk of mistakes.

7.3 Professional Tax Advisors

When should you consider hiring a tax advisor? If you have complex tax situations or need personalized advice, a professional tax advisor can provide valuable assistance.

Hiring a professional tax advisor can be beneficial in certain situations.

- Complex Tax Situations: If you have complex tax situations, such as self-employment income, rental income, or significant investment income, a tax advisor can provide valuable guidance.

- Personalized Advice: A tax advisor can provide personalized advice based on your specific financial situation.

- Peace of Mind: Knowing that a professional is handling your taxes can provide peace of mind.

8. Real-World Examples of Successful Partnerships

Can you provide examples of successful partnerships that have led to income growth? Case studies of companies that have leveraged partnerships to achieve significant results can offer inspiration.

Examining real-world examples of successful partnerships can provide valuable insights and inspiration for your own ventures.

8.1 Starbucks and Spotify

How did Starbucks and Spotify partner to enhance customer experience and drive sales? Their partnership integrated Spotify’s music platform into Starbucks’ loyalty program, creating a unique customer experience.

Starbucks and Spotify partnered to enhance customer experience and drive sales.

- Integration of Music Platform: Starbucks integrated Spotify’s music platform into its loyalty program.

- Enhanced Customer Experience: Customers could discover new music and earn rewards through the partnership.

- Increased Sales: The partnership drove sales by creating a unique and engaging customer experience.

8.2 Apple and Nike

What benefits did Apple and Nike gain from their partnership? Their collaboration resulted in the Apple Watch Nike+, a product that combined Apple’s technology with Nike’s fitness expertise.

Apple and Nike partnered to create the Apple Watch Nike+.

- Combined Expertise: The partnership combined Apple’s technology with Nike’s fitness expertise.

- Innovative Product: The Apple Watch Nike+ offered unique features for runners and fitness enthusiasts.

- Expanded Market Reach: The partnership expanded the market reach for both companies.

8.3 Airbnb and local experience providers

How does Airbnb partner with local experience providers to offer unique travel experiences? Airbnb partners with local experts to offer unique travel experiences, enhancing the overall value proposition for customers.

Airbnb partners with local experience providers to offer unique travel experiences.

- Unique Experiences: Airbnb offers a variety of unique experiences, such as cooking classes, guided tours, and outdoor adventures.

- Enhanced Value Proposition: The experiences enhance the overall value proposition for customers, making Airbnb a more attractive option than traditional hotels.

- Increased Revenue: The experiences generate additional revenue for Airbnb and local experience providers.

9. Current Tax Trends and Updates

What are the latest tax trends and updates you should be aware of? Staying informed about tax law changes is crucial for effective tax planning.

Staying informed about current tax trends and updates is crucial for effective tax planning. Tax laws are constantly evolving, and changes can have a significant impact on your tax liability.

9.1 Tax Law Changes

How do tax law changes affect your tax planning strategies? Tax law changes can impact deductions, credits, and tax rates, requiring adjustments to your tax strategy.

Tax law changes can significantly impact your tax planning strategies.

- Deductions and Credits: Tax law changes can affect the availability and amount of deductions and credits.

- Tax Rates: Tax law changes can affect the tax rates that apply to your income.

- Tax Planning Adjustments: You may need to adjust your tax planning strategies to account for tax law changes.

9.2 Impact of the Inflation Reduction Act

What are the key tax provisions of the Inflation Reduction Act? The Inflation Reduction Act includes provisions related to clean energy incentives and healthcare subsidies, which can impact your tax situation.

The Inflation Reduction Act includes several key tax provisions:

- Clean Energy Incentives: The act provides incentives for investments in clean energy, such as solar panels and electric vehicles.

- Healthcare Subsidies: The act extends enhanced healthcare subsidies for individuals who purchase health insurance through the Affordable Care Act (ACA) marketplace.

- Corporate Tax Changes: The act includes changes to corporate tax rates and provisions aimed at preventing tax avoidance by large corporations.

9.3 Remote Work and Taxes

How does remote work affect your tax obligations? Remote workers may need to consider state income tax rules and home office deductions.

Remote work can have implications for your tax obligations.

- State Income Tax Rules: If you work remotely for a company located in a different state, you may need to consider state income tax rules.

- Home Office Deduction: If you use a portion of your home exclusively and regularly for business, you may be able to deduct home office expenses.

- Business Expenses: If you are self-employed, you may be able to deduct business expenses, such as internet and phone expenses.

10. Frequently Asked Questions (FAQs)

Here are some frequently asked questions about Form 1040:

10.1 What is the standard deduction for 2023?

The standard deduction for 2023 varies based on filing status, with $13,850 for single filers and $27,700 for married filing jointly. These amounts are adjusted annually for inflation.

10.2 How do I know if I should itemize deductions?

You should itemize deductions if your total itemized deductions exceed your standard deduction. Common itemized deductions include medical expenses, state and local taxes, and charitable contributions.

10.3 What is the deadline for filing my tax return?

The deadline for filing your tax return is typically April 15th. If you need more time, you can file for an extension, which gives you until October 15th to file.

10.4 How do I report self-employment income?

You report self-employment income on Schedule C of Form 1040. You will also need to pay self-employment tax, which is calculated on Schedule SE.

10.5 What is the Qualified Business Income (QBI) deduction?

The Qualified Business Income (QBI) deduction allows eligible self-employed individuals and small business owners to deduct up to 20% of their qualified business income.

10.6 How do I correct a mistake on my tax return?

If you find a mistake on your tax return after you have already filed it, you will need to file an amended tax return using Form 1040-X.

10.7 What is the difference between a tax deduction and a tax credit?

A tax deduction reduces your taxable income, while a tax credit directly reduces your tax liability. Tax credits are generally more valuable than tax deductions.

10.8 How do I find a qualified tax advisor?

You can find a qualified tax advisor through referrals from friends and family, online directories, and professional organizations. Be sure to check the advisor’s credentials and experience before hiring them.

10.9 What is the Earned Income Tax Credit (EITC)?

The Earned Income Tax Credit (EITC) is a refundable tax credit for low- to moderate-income workers and families. The amount of the credit depends on your income and the number of qualifying children you have.

10.10 How can income-partners.net help me with tax planning and income growth?

Income-partners.net offers resources and tools to help you with tax planning and income growth, including articles, guides, and a directory of potential business partners.

Understanding your Form 1040 is a powerful tool for financial empowerment and income growth. By mastering the key sections, avoiding common mistakes, and implementing strategic tax planning, you can take control of your financial future.

Ready to unlock more income opportunities and build strategic partnerships? Visit income-partners.net today to explore our comprehensive resources, connect with potential partners, and start maximizing your income potential. Discover collaboration strategies, build valuable relationships, and achieve your financial goals with income-partners.net.

Address: 1 University Station, Austin, TX 78712, United States

Phone: +1 (512) 471-3434

Website: income-partners.net