The balance sheet and income statement are related because the net income from the income statement directly impacts the retained earnings section of the balance sheet, showcasing a company’s financial performance and position; income-partners.net can help you understand and leverage these connections for strategic partnerships. Understanding this relationship allows businesses to make informed decisions, improving profitability and asset management. Explore the potential for increased revenue and collaborative ventures.

1. What is the Fundamental Relationship Between the Balance Sheet and Income Statement?

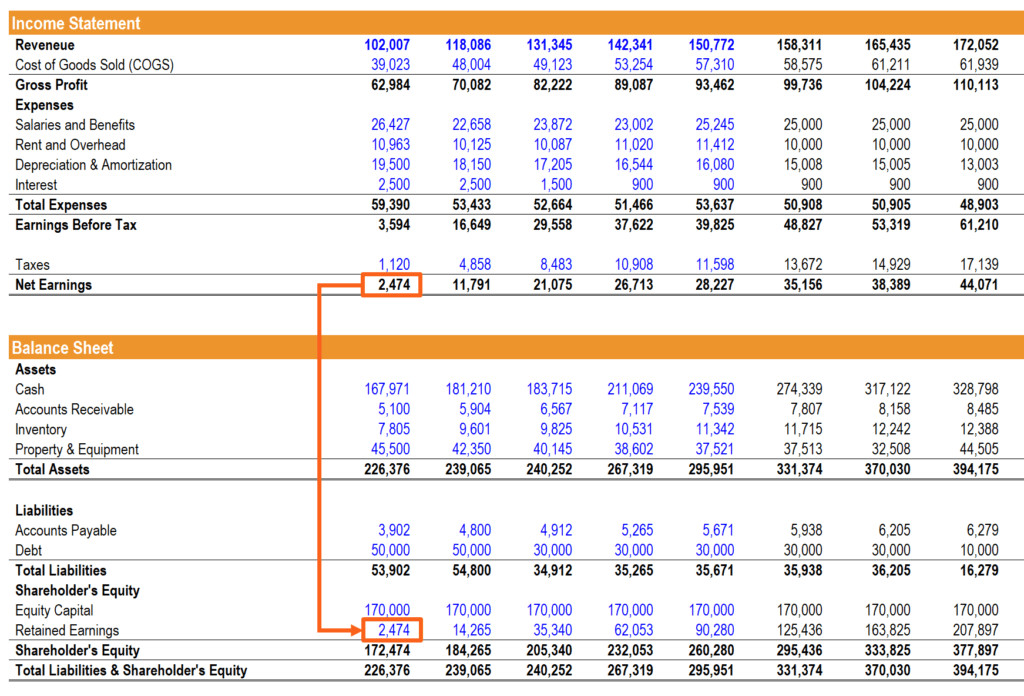

Net income from the income statement flows into the retained earnings section of the balance sheet, representing a direct link between a company’s profitability and its financial position. This connection is fundamental to understanding a company’s financial health, as it shows how profits are reinvested back into the business to drive growth and stability. It’s like understanding that the water flowing from a river (income statement) fills a reservoir (balance sheet), ensuring a steady supply for the future. This dynamic is critical for potential partners to evaluate the fiscal prudence and growth trajectory of a business.

The income statement, often referred to as the profit and loss (P&L) statement, provides a snapshot of a company’s financial performance over a specific period. It details revenues, expenses, gains, and losses, ultimately arriving at net income or net loss. The balance sheet, on the other hand, is a snapshot of a company’s assets, liabilities, and equity at a specific point in time. It follows the basic accounting equation: Assets = Liabilities + Equity. The retained earnings component of equity reflects the accumulated profits of the company that have not been distributed as dividends.

The net income generated on the income statement increases the retained earnings on the balance sheet. Conversely, a net loss decreases retained earnings. This flow ensures that the balance sheet reflects the cumulative financial performance of the company over time. According to research from the University of Texas at Austin’s McCombs School of Business, in July 2025, companies with a strong alignment between their income statement and balance sheet typically demonstrate better long-term financial stability.

2. How Does Net Income from the Income Statement Affect Retained Earnings on the Balance Sheet?

Net income directly increases retained earnings, while a net loss decreases it, influencing the overall equity and financial stability of the company. This mechanism ensures that the balance sheet accurately reflects the cumulative impact of a company’s financial performance over time. It’s akin to adding or subtracting water from a tank; profit increases the level, while loss decreases it. For businesses seeking strategic alliances, this is a vital indicator of financial resilience and growth potential.

Retained earnings represent the cumulative net income of a company that has been retained for reinvestment in the business rather than being distributed to shareholders as dividends. This figure is a key component of shareholders’ equity on the balance sheet. When a company generates net income, it has the option of distributing a portion of those earnings as dividends or retaining them for future use. The portion that is retained increases the retained earnings balance.

The formula for calculating the ending retained earnings balance is:

Ending Retained Earnings = Beginning Retained Earnings + Net Income – Dividends

For example, if a company starts the year with $500,000 in retained earnings, generates $200,000 in net income, and pays out $50,000 in dividends, the ending retained earnings balance would be:

$500,000 (Beginning) + $200,000 (Net Income) – $50,000 (Dividends) = $650,000

This increase in retained earnings strengthens the company’s equity position and provides it with additional resources for investments, debt repayment, or other strategic initiatives.

3. What Role Does Depreciation Play in Linking These Financial Statements?

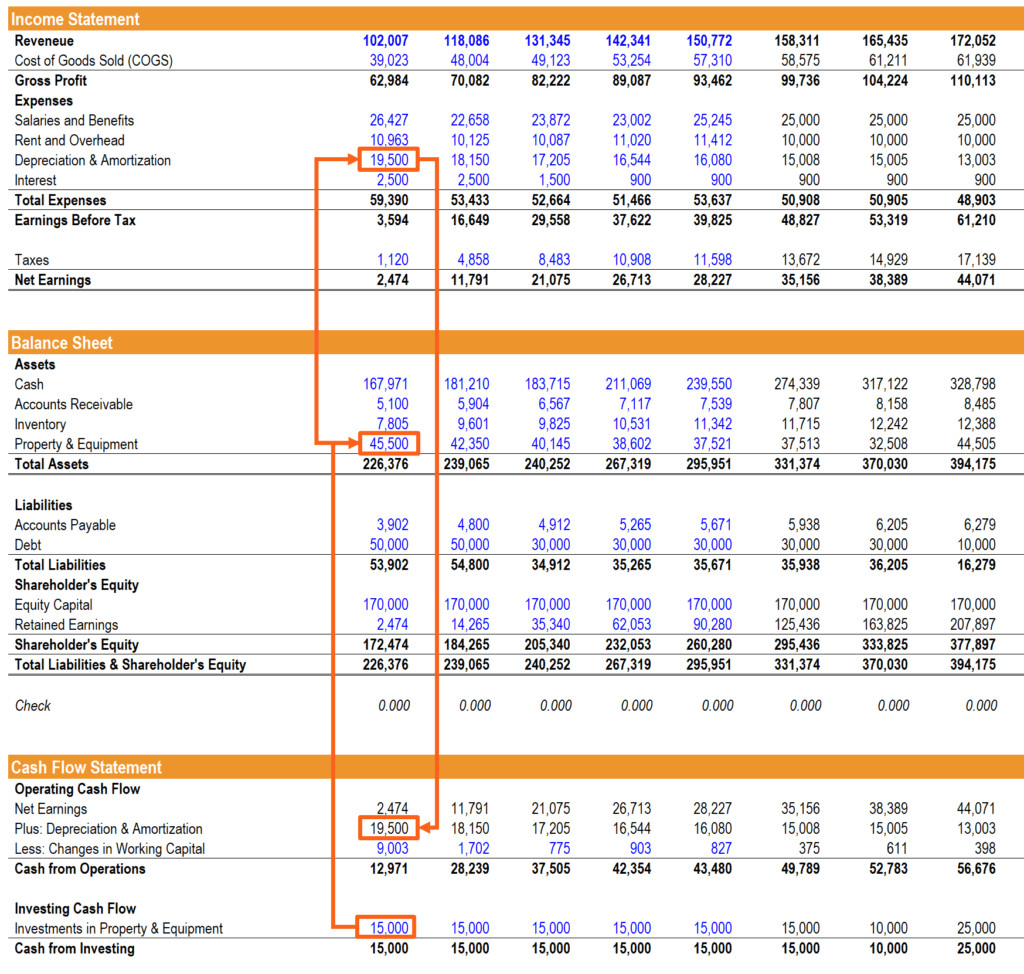

Depreciation expense, recorded on the income statement, reduces net income while accumulating on the balance sheet as accumulated depreciation, impacting the net value of assets. This connection is crucial as it acknowledges the wearing out of assets over time, affecting both current profitability and long-term asset valuation. Think of it as a car losing value each year; the loss is recorded on the income statement, while the reduced value is reflected on the balance sheet. This aspect is essential for investors evaluating a company’s real asset worth and operational efficiency.

Depreciation is the systematic allocation of the cost of a tangible asset over its useful life. It reflects the gradual decline in the asset’s value due to wear and tear, obsolescence, or usage. The depreciation expense is recorded on the income statement, reducing the company’s net income. Simultaneously, the accumulated depreciation, which is the total amount of depreciation recognized to date, is recorded on the balance sheet as a contra-asset account, reducing the book value of the related asset.

The depreciation expense impacts the income statement by lowering the reported profit, thereby reducing the tax liability. On the balance sheet, the accumulated depreciation reduces the net value of assets, providing a more realistic view of the company’s asset base. This is particularly important for capital-intensive industries where fixed assets constitute a significant portion of the balance sheet.

4. How Do Capital Expenditures (CAPEX) Connect the Balance Sheet and Cash Flow Statement?

Capital expenditures, or CAPEX, affect the balance sheet by increasing the value of long-term assets and are reflected on the cash flow statement as an outflow under investing activities. This link is crucial as it highlights how investments in assets impact a company’s cash position and long-term growth potential. Consider it as building a new factory; it increases assets on the balance sheet and reduces cash on the cash flow statement. For businesses seeking investors, this demonstrates a commitment to growth and operational improvements.

Capital expenditures (CAPEX) refer to the funds used by a company to acquire, upgrade, and maintain physical assets such as property, plant, and equipment (PP&E). These expenditures are investments in the company’s long-term productive capacity. CAPEX is not expensed on the income statement in the period it is incurred. Instead, it is capitalized on the balance sheet as an asset and depreciated over its useful life.

On the cash flow statement, CAPEX is reported as a cash outflow in the investing activities section. This reflects the actual cash spent on acquiring or improving long-term assets. The purchase of PP&E increases the asset side of the balance sheet, while the corresponding cash outflow reduces the cash balance.

5. What is the Significance of Working Capital Management in Linking Financial Statements?

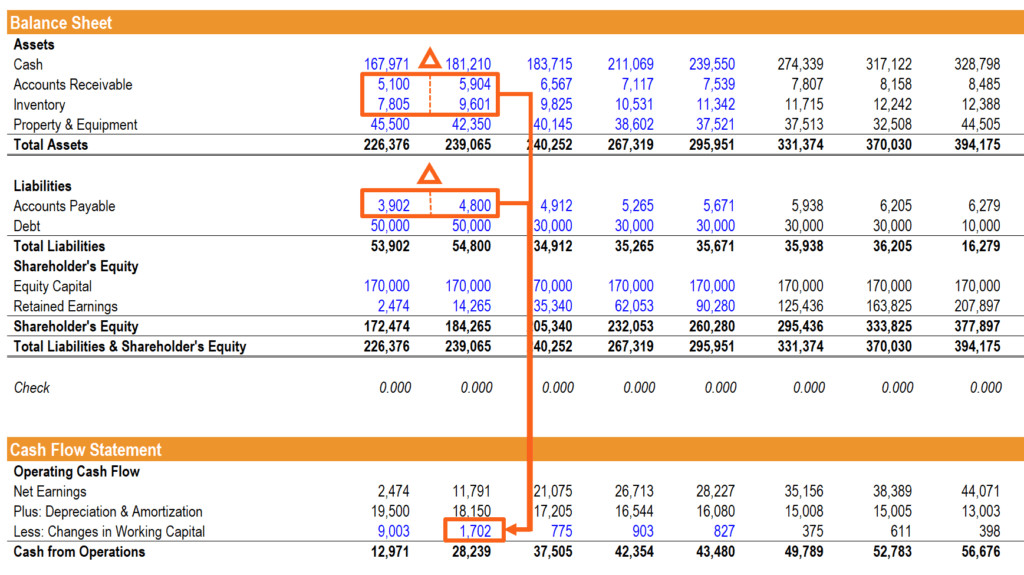

Changes in working capital, reflecting the difference between current assets and current liabilities, impact both the income statement and cash flow statement, illustrating operational efficiency. This interplay shows how effectively a company manages its short-term assets and liabilities to generate revenue. Think of it as managing a store’s inventory; efficient management improves both sales (income statement) and cash flow. For partners, this indicates a company’s ability to handle day-to-day financial operations effectively.

Working capital is the difference between a company’s current assets and its current liabilities. It represents the funds available for day-to-day operations. Effective management of working capital is crucial for maintaining liquidity and operational efficiency. Changes in working capital accounts, such as accounts receivable, accounts payable, and inventory, affect both the income statement and the cash flow statement.

For example, an increase in accounts receivable means that the company has recorded revenue on the income statement but has not yet received cash from customers. This increase is deducted from net income in the cash flow from operations section because it does not represent actual cash inflow. Conversely, an increase in accounts payable means that the company has incurred expenses but has not yet paid cash to suppliers. This increase is added back to net income in the cash flow from operations section because it represents a reduction in cash outflow.

Effective working capital management can improve a company’s cash flow, reduce its need for external financing, and enhance its profitability.

6. How Does Financing Activities Impact All Three Financial Statements?

Financing activities, such as issuing debt or equity, impact the balance sheet by altering liabilities and equity, the income statement through interest expenses, and the cash flow statement via financing cash flows. This interconnectedness reflects how a company funds its operations and growth. Consider it as taking out a loan; it increases debt on the balance sheet, incurs interest expenses on the income statement, and provides cash inflow on the cash flow statement. This insight is crucial for investors assessing a company’s capital structure and financial leverage.

Financing activities involve transactions related to how a company is funded, including debt, equity, and dividends. These activities affect all three financial statements in different ways.

- Balance Sheet: Issuing debt increases liabilities, while issuing equity increases shareholders’ equity. Repaying debt reduces liabilities, and repurchasing shares reduces shareholders’ equity.

- Income Statement: Interest expense on debt is recorded on the income statement, reducing net income.

- Cash Flow Statement: Cash inflows from issuing debt or equity are reported in the financing activities section. Cash outflows for repaying debt, repurchasing shares, or paying dividends are also reported in this section.

For example, if a company issues bonds to raise capital, the balance sheet will show an increase in long-term debt, and the cash flow statement will show a cash inflow from financing activities. The interest payments on the bonds will be recorded as interest expense on the income statement, reducing net income.

7. How Is the Cash Balance the Ultimate Link Between the Three Financial Statements?

The ending cash balance, calculated on the cash flow statement, directly updates the cash balance on the balance sheet, acting as a crucial validation point for the accuracy of all three statements. This connection ensures that all financial activities are properly accounted for and reconciled. Think of it as verifying the final amount in your bank account after all transactions. For auditors and financial analysts, this reconciliation is a critical step in ensuring financial integrity.

The cash balance is the result of all cash inflows and outflows that occur during a specific period. It is the ultimate link between the three financial statements because it reflects the cumulative impact of all operating, investing, and financing activities on the company’s cash position.

The cash flow statement starts with the beginning cash balance, adds cash flows from operations, investing, and financing, and arrives at the ending cash balance. This ending cash balance is then reported on the balance sheet as the company’s cash balance at the end of the period.

If the ending cash balance on the cash flow statement does not match the cash balance on the balance sheet, it indicates an error in the preparation of the financial statements. This reconciliation is a critical step in ensuring the accuracy and reliability of the financial reporting process.

8. How Do Changes in Inventory Levels Affect Both the Income Statement and Balance Sheet?

Changes in inventory levels affect the balance sheet by altering current assets and the income statement through the cost of goods sold (COGS), impacting profitability. This shows how inventory management directly influences a company’s financial health. Think of it as a bakery managing its flour stock; too much ties up capital (balance sheet), while too little can reduce sales (income statement). For potential investors, this highlights the efficiency of a company’s supply chain and inventory management practices.

Inventory represents the goods a company holds for sale to customers. Changes in inventory levels affect both the balance sheet and the income statement.

- Balance Sheet: Inventory is a current asset on the balance sheet. An increase in inventory increases the company’s total assets, while a decrease in inventory decreases total assets.

- Income Statement: The cost of goods sold (COGS) is the direct cost of producing the goods sold by a company. COGS includes the cost of raw materials, labor, and other direct costs. An increase in inventory can lead to a decrease in COGS, while a decrease in inventory can lead to an increase in COGS.

The relationship between inventory, COGS, and net income can be summarized as follows:

Beginning Inventory + Purchases – Ending Inventory = Cost of Goods Sold

Net Income = Revenue – Cost of Goods Sold – Operating Expenses

Effective inventory management can help a company minimize its inventory holding costs, reduce the risk of obsolescence, and improve its profitability.

9. What Are Some Common Errors in Linking the Three Financial Statements and How Can They Be Avoided?

Common errors include miscalculating depreciation, mishandling working capital changes, and incorrectly linking financing activities, leading to imbalances and inaccurate financial reporting. Avoiding these requires meticulous attention to detail, a solid understanding of accounting principles, and regular reconciliation. Think of it as building a bridge; one wrong calculation can lead to structural failure. For financial professionals, these errors can undermine trust and credibility.

Several common errors can occur when linking the three financial statements, leading to inaccuracies and misinterpretations. Here are some examples and tips on how to avoid them:

| Error | Description | Prevention |

|---|---|---|

| Depreciation Miscalculation | Incorrectly calculating depreciation expense can lead to errors in net income and asset values. | Use a detailed depreciation schedule, double-check formulas, and ensure consistency in depreciation methods. |

| Working Capital Mishandling | Incorrectly accounting for changes in accounts receivable, accounts payable, and inventory. | Create a separate working capital schedule, carefully track changes in each account, and understand the impact on cash flow. |

| Financing Activities Errors | Incorrectly linking debt issuance, repayment, and interest expense. | Develop a debt schedule, track principal and interest payments separately, and ensure that interest expense is correctly reflected on the income statement. |

| Cash Flow Miscalculations | Errors in calculating cash flows from operations, investing, and financing can lead to an incorrect ending cash balance. | Reconcile cash flows regularly, double-check formulas, and ensure that all cash transactions are properly classified. |

| Incorrect Retained Earnings | Miscalculating retained earnings by incorrectly adding net income or deducting dividends. | Use the correct retained earnings formula, verify net income and dividend amounts, and ensure that the balance sheet balances. |

10. How Can Income-Partners.Net Help in Understanding and Leveraging the Relationship Between Financial Statements for Partnership Opportunities?

Income-partners.net provides resources, expert insights, and tools to help businesses understand financial statement relationships, identify strong potential partners, and structure successful collaborations for increased revenue and growth. Our platform offers a wealth of knowledge and connections. Consider it as having a seasoned guide navigate complex financial terrain, leading you to profitable partnerships. Address: 1 University Station, Austin, TX 78712, United States. Phone: +1 (512) 471-3434. Website: income-partners.net.

Income-partners.net can assist in several ways:

- Educational Resources: Providing articles, guides, and webinars on financial statement analysis and partnership strategies.

- Expert Insights: Offering access to financial experts who can provide personalized advice and guidance.

- Tools and Templates: Providing financial modeling templates and tools for analyzing potential partners’ financial health.

- Networking Opportunities: Connecting businesses with potential partners who align with their financial goals and values.

- Due Diligence Support: Assisting in the due diligence process to ensure that potential partners are financially sound and reliable.

By leveraging income-partners.net, businesses can gain a deeper understanding of the financial statement relationships, identify strong potential partners, and structure successful collaborations that drive revenue growth and long-term success.

Net Income and Retained Earnings

Net Income and Retained Earnings

11. What Metrics Should Businesses Focus on to Assess Financial Health Using the Balance Sheet and Income Statement?

Businesses should focus on profitability ratios (net profit margin), liquidity ratios (current ratio), solvency ratios (debt-to-equity ratio), and efficiency ratios (asset turnover) to assess financial health. These metrics provide a comprehensive view of a company’s performance and stability. Think of it as a doctor checking vital signs; each metric provides key information about the company’s health. These insights help potential partners evaluate the financial prudence and sustainability of a business.

To effectively assess financial health using the balance sheet and income statement, businesses should focus on key financial metrics and ratios. These metrics provide insights into a company’s profitability, liquidity, solvency, and efficiency. Here are some of the most important metrics to consider:

| Metric | Formula | Description | Importance |

|---|---|---|---|

| Net Profit Margin | (Net Income / Revenue) x 100 | Measures the percentage of revenue that remains after deducting all expenses. | Indicates the company’s profitability and ability to generate profits from its sales. |

| Current Ratio | Current Assets / Current Liabilities | Measures the company’s ability to pay its short-term obligations with its current assets. | Indicates the company’s liquidity and ability to meet its short-term financial obligations. |

| Debt-to-Equity Ratio | Total Debt / Total Equity | Measures the proportion of a company’s financing that comes from debt versus equity. | Indicates the company’s financial leverage and risk. A high ratio may indicate that the company is relying too heavily on debt financing. |

| Asset Turnover Ratio | Revenue / Total Assets | Measures how efficiently a company uses its assets to generate revenue. | Indicates the company’s efficiency in using its assets to generate sales. A higher ratio suggests that the company is effectively utilizing its assets. |

| Return on Equity (ROE) | (Net Income / Total Equity) x 100 | Measures the return generated on shareholders’ equity. | Indicates how effectively the company is using shareholders’ investments to generate profits. |

| Inventory Turnover | Cost of Goods Sold / Average Inventory | Measures how quickly a company is selling its inventory. | Indicates the efficiency of inventory management. A higher ratio suggests that the company is effectively managing its inventory. |

12. What Strategies Can Businesses Employ to Improve Their Financial Statement Linkages and Overall Financial Health?

Strategies include improving working capital management, optimizing capital expenditures, maintaining accurate accounting records, and regularly monitoring financial metrics. These efforts ensure a stronger, more resilient financial foundation. Think of it as fine-tuning a machine; each adjustment enhances overall performance. By strengthening these linkages, businesses become more attractive and reliable partners.

Businesses can employ several strategies to improve their financial statement linkages and overall financial health:

- Improve Working Capital Management: Optimize inventory levels, accelerate accounts receivable collections, and negotiate favorable payment terms with suppliers.

- Optimize Capital Expenditures: Carefully evaluate investment opportunities, prioritize projects with the highest returns, and manage asset depreciation effectively.

- Maintain Accurate Accounting Records: Ensure that all financial transactions are properly recorded and classified, and regularly reconcile accounts to prevent errors.

- Regularly Monitor Financial Metrics: Track key financial ratios and metrics, identify trends, and take corrective action when necessary.

- Implement Robust Internal Controls: Establish strong internal controls to prevent fraud, errors, and inefficiencies.

- Seek Professional Advice: Consult with financial advisors, accountants, and other experts to gain insights and guidance.

- Invest in Technology: Implement accounting software and other technologies to automate financial processes and improve accuracy.

- Foster a Culture of Financial Responsibility: Encourage employees to be mindful of costs, and promote transparency and accountability in financial decision-making.

PP&E, Depreciation, and Capex

PP&E, Depreciation, and Capex

13. How Can Potential Partners Use Financial Statement Analysis to Assess the Viability of a Business Relationship?

Potential partners can use financial statement analysis to assess profitability, liquidity, solvency, and efficiency, ensuring a comprehensive understanding of the partner’s financial stability and growth potential. This is akin to conducting a thorough background check before entering a business deal. Such due diligence ensures informed decisions and reduces risks in partnership ventures.

Potential partners can use financial statement analysis to assess the viability of a business relationship by examining the following aspects:

- Profitability: Review the income statement to assess the company’s revenue growth, gross profit margin, and net profit margin. Look for consistent profitability and positive trends.

- Liquidity: Examine the balance sheet to assess the company’s current ratio, quick ratio, and cash flow from operations. Ensure that the company has sufficient liquidity to meet its short-term obligations.

- Solvency: Analyze the balance sheet to assess the company’s debt-to-equity ratio and interest coverage ratio. Determine whether the company has a sustainable capital structure and can meet its long-term obligations.

- Efficiency: Evaluate the income statement and balance sheet to assess the company’s asset turnover ratio, inventory turnover ratio, and accounts receivable turnover ratio. Determine whether the company is efficiently managing its assets and resources.

- Consistency: Compare the company’s financial performance over time to identify trends and assess the consistency of its performance.

- Industry Benchmarks: Compare the company’s financial ratios to industry benchmarks to assess its relative performance.

- Management Quality: Consider the experience and expertise of the company’s management team, as well as its track record of financial performance.

14. What Role Do Auditors Play in Ensuring the Accuracy and Reliability of Financial Statement Linkages?

Auditors ensure the accuracy and reliability of financial statement linkages by independently verifying the financial records and processes, providing stakeholders with confidence in the financial reporting. This is similar to having a neutral third party inspect a construction project for safety and compliance. Their oversight is crucial for building trust and credibility in the financial information presented by a company.

Auditors play a critical role in ensuring the accuracy and reliability of financial statement linkages. They are independent professionals who examine a company’s financial statements and provide an opinion on whether they are fairly presented in accordance with generally accepted accounting principles (GAAP) or other applicable accounting standards.

Auditors perform the following tasks:

- Reviewing Financial Records: Examining the company’s accounting records, supporting documentation, and internal controls to ensure that financial transactions are properly recorded and classified.

- Testing Internal Controls: Evaluating the effectiveness of the company’s internal controls to prevent fraud, errors, and inefficiencies.

- Verifying Account Balances: Confirming account balances with third parties, such as banks, customers, and suppliers, to ensure their accuracy.

- Assessing Accounting Policies: Evaluating the appropriateness of the company’s accounting policies and ensuring that they are consistently applied.

- Providing an Opinion: Issuing an audit report that expresses an opinion on whether the financial statements are fairly presented.

15. How Can Understanding the Financial Statement Relationship Contribute to Better Strategic Decision-Making?

Understanding the financial statement relationship enables informed strategic decisions by providing a holistic view of a company’s financial position, performance, and cash flows. This insight is like having a GPS for your business; it guides you to make informed choices that drive growth and sustainability. This comprehensive understanding is critical for making sound investments and forming strategic partnerships.

Understanding the relationships between financial statements is essential for making informed strategic decisions. By analyzing the linkages between the income statement, balance sheet, and cash flow statement, businesses can gain a deeper understanding of their financial performance, identify areas for improvement, and make better decisions about resource allocation, investments, and financing.

Here are some examples of how understanding the financial statement relationships can contribute to better strategic decision-making:

- Investment Decisions: By analyzing the cash flow statement and balance sheet, businesses can assess their ability to fund new investments and evaluate the potential returns on those investments.

- Financing Decisions: By analyzing the balance sheet and income statement, businesses can determine the optimal mix of debt and equity financing and assess their ability to meet their debt obligations.

- Operational Decisions: By analyzing the income statement and balance sheet, businesses can identify areas where they can improve their efficiency, reduce their costs, and increase their profitability.

- Strategic Partnerships: By analyzing the financial statements of potential partners, businesses can assess their financial health and viability, and make informed decisions about whether to enter into a partnership.

16. Can You Provide Examples of Successful Companies That Effectively Utilize Financial Statement Linkages?

Successful companies like Apple and Amazon effectively utilize financial statement linkages to manage resources, optimize investments, and drive growth, demonstrating the power of integrated financial management. This is akin to a skilled chess player using every piece strategically to win the game. For businesses, this showcases how effective financial management leads to sustained success and strong partnerships.

Several successful companies effectively utilize financial statement linkages to drive growth, improve profitability, and make informed strategic decisions. Here are a couple of examples:

- Apple: Apple is known for its efficient working capital management, which is reflected in its strong cash flow and high inventory turnover ratio. The company carefully manages its supply chain to minimize inventory holding costs and ensure that it can meet customer demand.

- Amazon: Amazon effectively utilizes financial statement linkages to manage its capital expenditures and investments. The company carefully evaluates investment opportunities and prioritizes projects with the highest potential returns. It also uses its strong cash flow to fund acquisitions and other strategic initiatives.

These companies demonstrate the power of understanding and leveraging financial statement linkages to drive financial performance and achieve strategic goals.

Working Capital

Working Capital

17. What Are the Ethical Considerations When Linking and Interpreting Financial Statements?

Ethical considerations include ensuring transparency, avoiding manipulation, and providing accurate information, maintaining trust and integrity in financial reporting. This is like a doctor adhering to the Hippocratic Oath; it ensures that financial practices are honest and beneficial. Upholding these ethical standards is essential for fostering trust and credibility with investors, partners, and stakeholders.

When linking and interpreting financial statements, several ethical considerations must be taken into account:

- Transparency: Financial statements should be transparent and provide clear and accurate information about the company’s financial performance and position.

- Accuracy: Financial statements should be prepared with accuracy and integrity, and should not contain any material misstatements or omissions.

- Objectivity: Financial statements should be prepared objectively and without bias, and should not be manipulated to present a more favorable picture of the company’s financial performance.

- Confidentiality: Financial information should be kept confidential and should not be disclosed to unauthorized parties.

- Compliance: Financial statements should be prepared in compliance with applicable accounting standards, laws, and regulations.

- Responsibility: Financial professionals have a responsibility to act in the best interests of their clients and stakeholders, and to provide them with accurate and reliable financial information.

18. How Do Financial Statement Linkages Vary Across Different Industries?

Financial statement linkages vary across industries due to different operational models, asset structures, and revenue recognition methods, affecting how key metrics are interpreted. This is akin to understanding that a doctor specializes in a particular field; each industry has unique financial characteristics. Recognizing these industry-specific nuances is critical for accurate financial analysis and effective partnership strategies.

The linkages between financial statements can vary significantly across different industries due to differences in business models, asset structures, and revenue recognition methods. For example, a manufacturing company may have a large investment in fixed assets and inventory, while a service company may have relatively few tangible assets. Similarly, a company in the software industry may recognize revenue over the life of a subscription, while a retailer may recognize revenue at the point of sale.

Here are a few examples of how financial statement linkages can vary across industries:

- Manufacturing: Manufacturing companies typically have a high level of investment in fixed assets and inventory, which can lead to a strong relationship between the balance sheet and the cash flow statement.

- Service: Service companies typically have relatively few tangible assets, but may have a significant investment in human capital. This can lead to a strong relationship between the income statement and the cash flow statement.

- Technology: Technology companies often have complex revenue recognition models and may have a significant investment in research and development. This can lead to a complex relationship between all three financial statements.

19. What Emerging Trends Are Impacting the Relationship Between Financial Statements?

Emerging trends like sustainability reporting, digital transformation, and real-time data analytics are impacting the relationship between financial statements, driving the need for more integrated and dynamic financial reporting. This is akin to understanding that medicine is constantly evolving; financial reporting must adapt to new realities. These trends will shape how companies assess performance and attract partners in the future.

Several emerging trends are impacting the relationship between financial statements:

- Sustainability Reporting: Companies are increasingly being asked to report on their environmental, social, and governance (ESG) performance. This is leading to the development of new metrics and reporting frameworks that integrate financial and non-financial information.

- Digital Transformation: Digital technologies are transforming the way companies operate and generate revenue. This is leading to new business models and revenue streams, which can impact the relationship between financial statements.

- Real-Time Data Analytics: Real-time data analytics are enabling companies to monitor their financial performance more closely and make more informed decisions. This is leading to a greater focus on key performance indicators (KPIs) and real-time reporting.

- Integrated Reporting: Integrated reporting is a framework that encourages companies to provide a more holistic view of their performance, linking financial and non-financial information to create a more comprehensive picture of their value creation process.

20. How Can Income-Partners.Net Assist in Navigating These Emerging Trends and Optimizing Financial Partnerships?

Income-partners.net offers expert guidance, up-to-date resources, and advanced analytical tools to help businesses navigate emerging trends, optimize financial partnerships, and achieve sustainable growth. Consider it as having a forward-thinking advisor helping you stay ahead in a rapidly changing business landscape. Address: 1 University Station, Austin, TX 78712, United States. Phone: +1 (512) 471-3434. Website: income-partners.net.

Income-partners.net can help businesses navigate these emerging trends and optimize their financial partnerships in several ways:

- Providing Expert Guidance: Offering access to financial experts who can provide insights and advice on emerging trends and best practices.

- Offering Up-to-Date Resources: Providing articles, guides, and webinars on the latest developments in financial reporting and sustainability.

- Offering Advanced Analytical Tools: Providing tools and templates for analyzing financial data and assessing the impact of emerging trends.

- Facilitating Networking Opportunities: Connecting businesses with potential partners who are aligned with their values and committed to sustainability.

- Supporting Due Diligence: Assisting in the due diligence process to ensure that potential partners are financially sound and committed to ethical business practices.

By leveraging Income-partners.net, businesses can stay ahead of the curve, optimize their financial partnerships, and achieve sustainable growth in a rapidly changing business environment.

Discover how understanding the financial statement relationship can drive your business success. Visit income-partners.net today to explore partnership opportunities, access expert insights, and connect with potential collaborators who share your vision for growth. Unlock your business’s full potential. Contact us now to start building valuable partnerships.

FAQ

-

What is the primary link between the balance sheet and the income statement?

The net income from the income statement flows directly into the retained earnings section of the balance sheet.

-

How does depreciation expense impact both the income statement and balance sheet?

Depreciation expense reduces net income on the income statement and accumulates as accumulated depreciation on the balance sheet, decreasing the net value of assets.

-

What are capital expenditures (CAPEX), and how do they affect the financial statements?

CAPEX are funds used to acquire or upgrade physical assets; they increase assets on the balance sheet and are reflected as cash outflows in the investing activities section of the cash flow statement.

-

Why is working capital management important for linking financial statements?

Effective working capital management, involving changes in current assets and liabilities, impacts both the income statement and cash flow statement, reflecting operational efficiency.

-

How do financing activities influence all three financial statements?

Financing activities, such as issuing debt or equity, affect the balance sheet by changing liabilities and equity, the income statement through interest expenses, and the cash flow statement via financing cash flows.

-

Why is the cash balance considered the ultimate link between financial statements?

The ending cash balance, calculated on the cash flow statement, directly updates the cash balance on the balance sheet, serving as a crucial validation point for accuracy.

-

What role do auditors play in ensuring accurate financial statement linkages?

Auditors independently verify financial records and processes, providing stakeholders with confidence in the accuracy and reliability of financial reporting.

-

What are some key metrics to focus on when assessing financial health using the balance sheet and income statement?

Key metrics include profitability ratios (e.g., net profit margin), liquidity ratios (e.g., current ratio), solvency ratios (e.g., debt-to-equity ratio), and efficiency ratios (e.g., asset turnover).

-

How can potential partners use financial statement analysis to assess a business relationship’s viability?

Potential partners can assess profitability, liquidity, solvency, and efficiency through financial statement analysis to gauge financial stability and growth potential.

-

What emerging trends are impacting the relationship between financial statements?

Emerging trends include sustainability reporting, digital transformation, and real-time data analytics, driving the need for more integrated and dynamic financial reporting.