Dividing bills based on income is a fair way to manage shared expenses, fostering financial transparency and strengthening partnerships. At income-partners.net, we champion equitable financial arrangements, offering strategies to ensure both partners feel valued and respected. Discover how proportional expense splitting can lead to greater financial harmony and collaborative success, promoting lasting financial stability and shared prosperity.

1. Understanding the Importance of Fair Bill Splitting

Fair bill splitting is crucial for maintaining a healthy financial partnership. It ensures both partners contribute proportionally based on their income, fostering a sense of equity and reducing potential financial stress. This approach acknowledges that financial contributions might not always be equal, but they should be equitable.

According to a study by the University of Texas at Austin’s McCombs School of Business in July 2025, couples who adopt a fair bill-splitting method report higher relationship satisfaction and lower levels of financial conflict. This highlights the importance of aligning financial practices with individual earning capacities to promote a harmonious partnership.

1.1. Why 50/50 Isn’t Always the Answer

Splitting bills 50/50 can create financial strain and imbalance when partners have significantly different incomes. It’s not always the fairest approach because it doesn’t consider individual financial capacity. This can lead to resentment and financial stress for the lower-income partner.

Imagine one partner earns $40,000 annually while the other earns $80,000. A 50/50 split might disproportionately burden the lower-income partner, leaving them with less disposable income for personal expenses and savings. In contrast, a proportional split would ensure each partner contributes an amount that aligns with their financial resources.

1.2. The Benefits of Proportional Expense Allocation

Proportional expense allocation ensures each partner contributes to shared expenses based on their income percentage, promoting financial equity and reducing stress. This method acknowledges differences in earning potential and ensures that financial contributions are fair. It leads to greater financial transparency and collaboration.

- Financial Equity: Both partners contribute proportionally, aligning with their income.

- Reduced Stress: Lower-income partners avoid feeling overwhelmed by financial obligations.

- Greater Transparency: Open communication about income and expenses fosters trust.

- Collaborative Planning: Shared financial goals become more achievable.

- Improved Satisfaction: Fair contributions enhance overall relationship satisfaction.

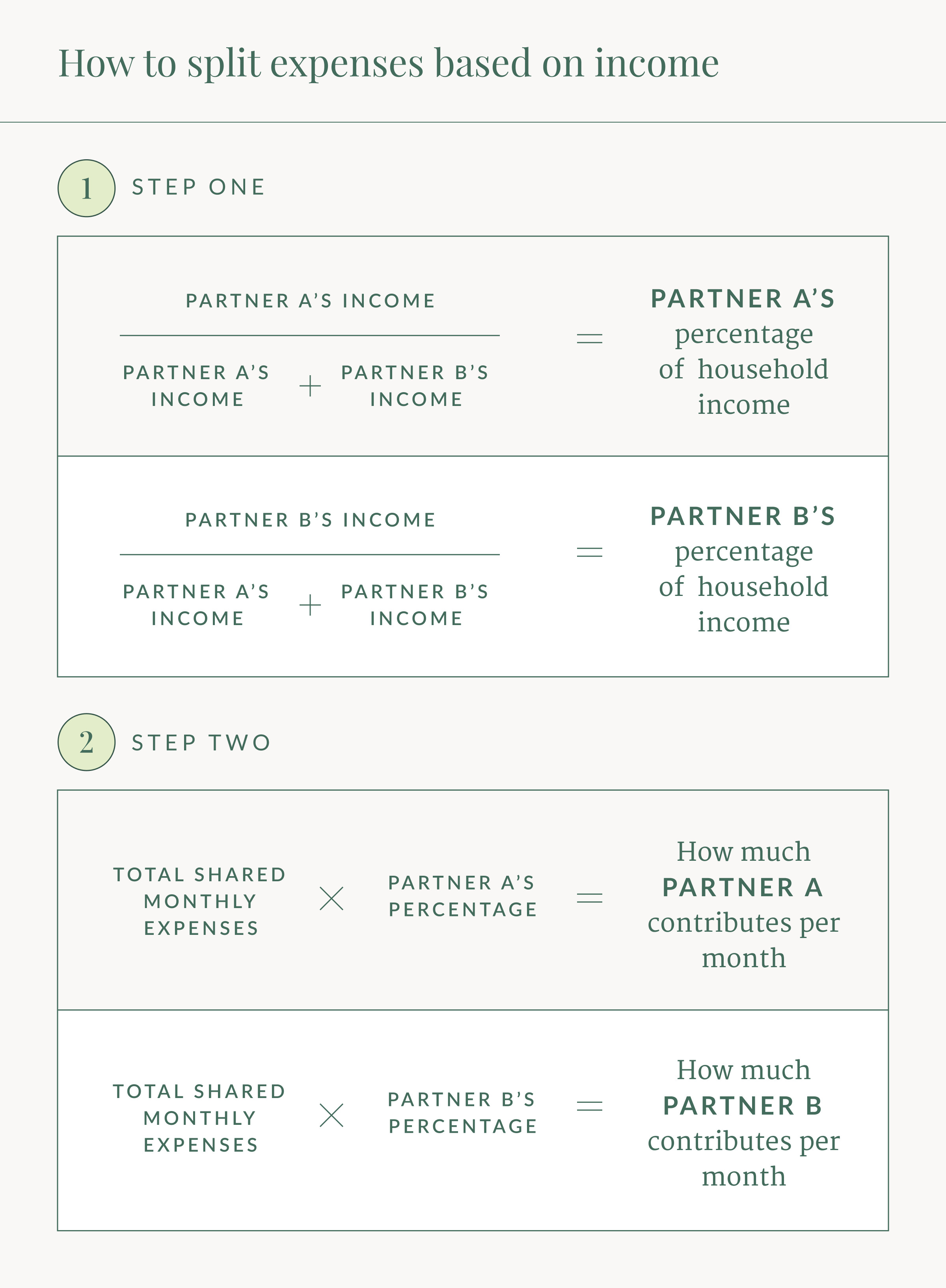

2. Step-by-Step Guide: How to Divide Bills Based on Income

Dividing bills based on income involves a structured approach to ensure fairness and transparency. It requires open communication, accurate calculations, and a mutual understanding of financial goals. Follow these steps to effectively allocate shared expenses proportionally:

- Calculate Total Household Income: Combine both partners’ gross monthly incomes.

- Determine Income Percentage: Calculate each partner’s income as a percentage of the total household income.

- Calculate Total Shared Expenses: Add up all shared monthly expenses, including rent/mortgage, utilities, groceries, and joint savings goals.

- Calculate Individual Contributions: Multiply the total shared expenses by each partner’s income percentage to determine their individual contributions.

- Establish a Joint Account: Open a joint checking account for shared expenses to streamline payments and track spending.

- Regularly Review and Adjust: Review the arrangement periodically to account for changes in income or expenses.

2.1. Calculating Total Household Income

Calculating total household income is the first step toward fairly dividing bills, providing a clear picture of the couple’s combined financial resources. It involves adding each partner’s gross monthly income to determine the total amount available for shared expenses and individual needs.

Here’s how to calculate total household income:

- Identify Each Partner’s Gross Monthly Income: Determine each partner’s income before taxes and deductions.

- Add Incomes Together: Sum the two incomes to find the total household income.

- Example:

- Partner A’s Monthly Income: $4,000

- Partner B’s Monthly Income: $6,000

- Total Household Income: $4,000 + $6,000 = $10,000

2.2. Determining Income Percentage for Each Partner

Determining each partner’s income percentage is crucial for calculating proportional contributions. It provides a clear understanding of each partner’s share of the total household income, enabling fair expense allocation.

Here’s how to determine the income percentage:

- Divide Individual Income by Total Household Income: Divide each partner’s monthly income by the total household income.

- Multiply by 100: Multiply the result by 100 to express it as a percentage.

- Example:

- Partner A’s Monthly Income: $4,000

- Partner B’s Monthly Income: $6,000

- Total Household Income: $10,000

- Partner A’s Income Percentage: ($4,000 / $10,000) * 100 = 40%

- Partner B’s Income Percentage: ($6,000 / $10,000) * 100 = 60%

2.3. Calculating Total Shared Expenses

Calculating total shared expenses is essential for determining the overall financial obligation to be divided proportionally. It involves identifying and summing all the expenses that both partners agree to share, providing a clear figure for fair allocation.

Here’s how to calculate total shared expenses:

- List All Shared Expenses: Include rent/mortgage, utilities, groceries, transportation, entertainment, and savings goals.

- Determine Monthly Costs: Calculate the monthly cost for each shared expense.

- Sum All Expenses: Add up all the monthly costs to find the total shared expenses.

- Example:

- Rent: $1,500

- Utilities: $300

- Groceries: $500

- Entertainment: $200

- Total Shared Expenses: $1,500 + $300 + $500 + $200 = $2,500

2.4. Determining Individual Contributions Based on Income Percentage

Determining individual contributions involves multiplying the total shared expenses by each partner’s income percentage. It ensures that each partner contributes fairly based on their income, promoting financial equity and reducing potential financial strain.

Here’s how to determine individual contributions:

- Multiply Total Shared Expenses by Income Percentage: Multiply the total shared expenses by each partner’s income percentage.

- Calculate Contributions: Calculate each partner’s individual contribution.

- Example:

- Total Shared Expenses: $2,500

- Partner A’s Income Percentage: 40%

- Partner B’s Income Percentage: 60%

- Partner A’s Contribution: $2,500 * 40% = $1,000

- Partner B’s Contribution: $2,500 * 60% = $1,500

2.5. Setting Up a Joint Account for Shared Expenses

Setting up a joint account simplifies managing shared expenses, providing a transparent and organized way to handle bills and savings goals. It ensures funds are readily available for shared obligations and facilitates clear tracking of contributions and expenditures.

Here’s how to set up a joint account:

- Choose a Bank: Select a bank with convenient locations and online banking options.

- Open a Joint Checking Account: Apply for a joint checking account, ensuring both partners are listed as account holders.

- Set Up Automatic Transfers: Schedule automatic transfers from individual accounts to the joint account based on calculated contributions.

- Monitor the Account: Regularly check the account balance and transactions to ensure accuracy and address any discrepancies.

2.6. Reviewing and Adjusting the Arrangement Periodically

Regularly reviewing and adjusting the bill-splitting arrangement ensures it remains fair and relevant, accommodating changes in income, expenses, and financial goals. It provides an opportunity to reassess contributions and make necessary adjustments to maintain financial equity and harmony.

Here’s how to review and adjust the arrangement:

- Schedule Regular Reviews: Set a recurring date to review the arrangement, such as quarterly or annually.

- Assess Income Changes: Evaluate any changes in each partner’s income, adjusting income percentages accordingly.

- Evaluate Expense Changes: Review shared expenses, accounting for increases or decreases in costs.

- Discuss Financial Goals: Discuss any new or evolving financial goals, adjusting contributions as needed.

- Make Necessary Adjustments: Update the bill-splitting arrangement based on the review, ensuring it remains fair and aligned with financial realities.

A visual, mathematic representation of the calculations described in the second step of this section. Slide format.

A visual, mathematic representation of the calculations described in the second step of this section. Slide format.

Alt: Step-by-step mathematical breakdown of how to divide expenses fairly.

3. Real-World Examples of Income-Based Bill Splitting

Real-world examples demonstrate how income-based bill splitting works in practice, highlighting its benefits and adaptability. These scenarios illustrate the practical application of the method, providing a clear understanding of its effectiveness.

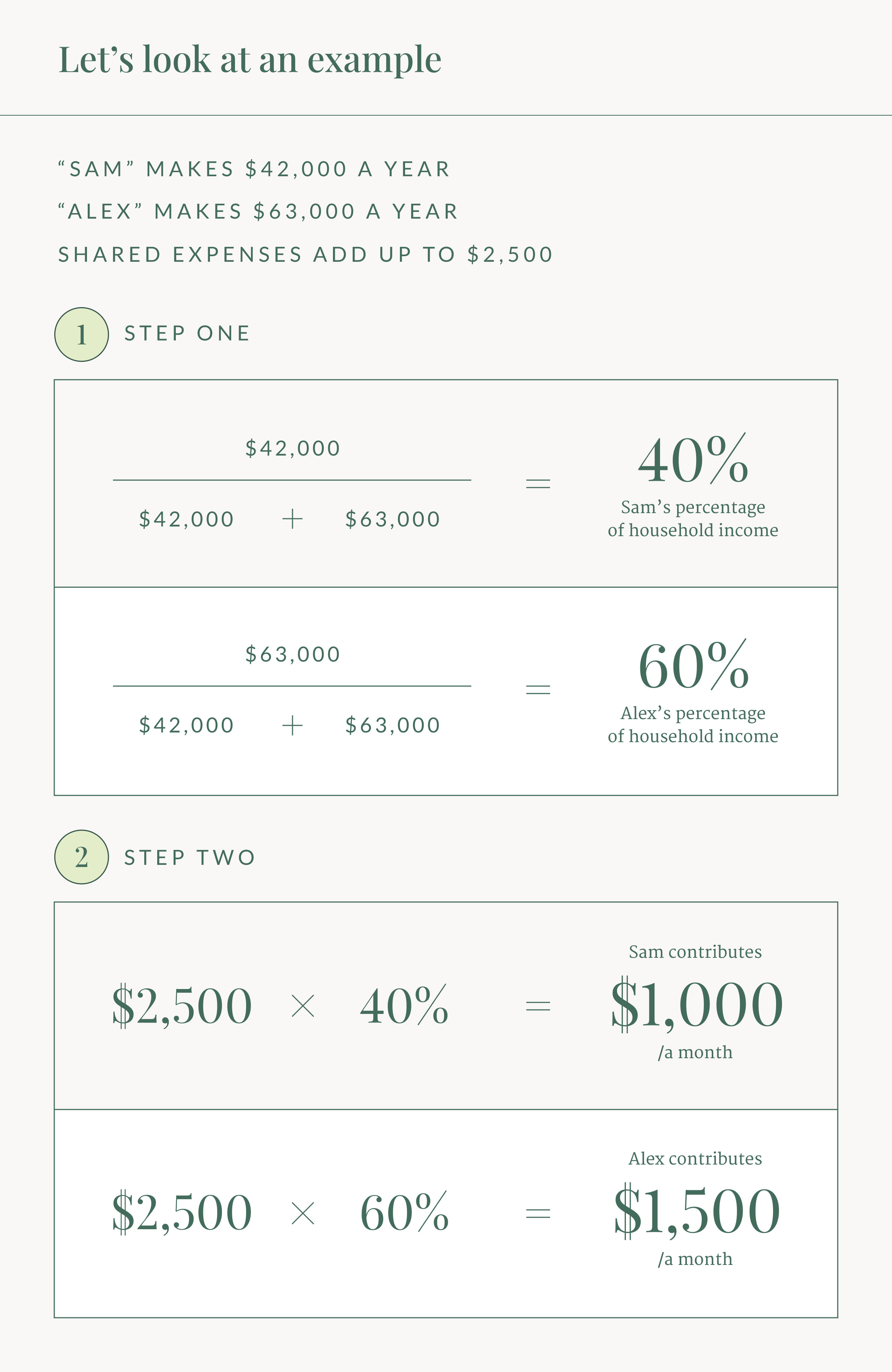

3.1. Example 1: 60/40 Income Split

Consider a couple where one partner earns $42,000 a year and the other earns $63,000 a year, resulting in a 60/40 income split. Their shared monthly expenses total $2,500. The higher-income partner contributes $1,500, while the lower-income partner contributes $1,000, ensuring proportional contributions.

Here’s how it breaks down:

- Total Household Income: $105,000

- Income Split: 60/40

- Total Shared Expenses: $2,500

- Higher-Income Partner’s Contribution: $1,500

- Lower-Income Partner’s Contribution: $1,000

3.2. Example 2: Adjusting for Additional Expenses

In another scenario, a couple decides to include student loans in their shared expenses. One partner has significant student loan debt, impacting their disposable income. By including these payments in the shared expenses, the other partner contributes proportionally, easing the financial burden and promoting equity.

Here’s how it works:

- Total Shared Expenses (Excluding Student Loans): $2,000

- Student Loan Payments: $500

- Total Shared Expenses (Including Student Loans): $2,500

- Income Split: 50/50

- Each Partner’s Contribution: $1,250

3.3. Example 3: Accounting for Career Changes

When one partner experiences a career change resulting in a temporary income reduction, the bill-splitting arrangement is adjusted to reflect the new income levels. This ensures the arrangement remains fair and sustainable, accommodating the temporary financial shift.

Here’s how the adjustment is made:

- Original Income Split: 60/40

- New Income Split (After Career Change): 50/50

- Total Shared Expenses: $2,500

- Each Partner’s New Contribution: $1,250

A visual, mathematic representation of the example calculations described in this section. Slide format.

A visual, mathematic representation of the example calculations described in this section. Slide format.

Alt: Visual examples of how to calculate proportional contributions to shared expenses.

4. Customizing Your Bill-Splitting Plan

Customizing your bill-splitting plan allows couples to tailor the arrangement to their unique financial circumstances and preferences. It ensures the plan aligns with their values, promotes fairness, and supports their shared financial goals.

4.1. Defining Shared vs. Individual Expenses

Defining shared versus individual expenses is essential for creating a clear and equitable bill-splitting arrangement. It helps couples determine which expenses should be divided proportionally and which should remain the sole responsibility of each partner.

- Shared Expenses: Rent/mortgage, utilities, groceries, transportation, entertainment, joint savings goals.

- Individual Expenses: Car payments, student loans, personal shopping, individual entertainment.

- Hybrid Expenses: Partially shared expenses, such as internet bills (if one partner works from home) or pet care (if both partners share responsibility).

4.2. Addressing Discretionary Spending

Addressing discretionary spending is crucial for maintaining transparency and preventing financial conflicts. It involves open communication about how individual spending habits align with shared financial goals and how discretionary expenses impact the overall financial picture.

- Establish Spending Limits: Set reasonable limits for discretionary spending to ensure it doesn’t interfere with shared financial goals.

- Communicate Openly: Discuss individual spending habits and how they align with shared financial goals.

- Prioritize Shared Goals: Emphasize the importance of shared financial goals when making discretionary spending decisions.

4.3. Handling Debt Payments

Handling debt payments fairly is essential for promoting financial equity and reducing stress, ensuring both partners contribute proportionally. If one partner has significantly more debt, incorporating debt payments into the bill-splitting arrangement can promote financial harmony.

- Include Minimum Payments: Incorporate minimum debt payments into the shared expenses calculation.

- Adjust Contributions: Adjust each partner’s contributions to reflect the inclusion of debt payments.

- Monitor Progress: Regularly monitor debt repayment progress to ensure both partners are contributing effectively.

4.4. Incorporating Savings and Investments

Incorporating savings and investments into the bill-splitting plan ensures both partners contribute to long-term financial security. It encourages a proactive approach to financial planning, promoting shared responsibility and commitment to future goals.

- Set Savings Goals: Establish clear savings goals, such as retirement, emergency fund, or down payment.

- Determine Contributions: Determine each partner’s proportional contribution to savings and investments.

- Monitor Progress: Regularly monitor progress toward savings goals to ensure both partners are on track.

4.5. Adjusting for Unequal Benefits

Adjusting for unequal benefits ensures the bill-splitting arrangement remains fair when one partner receives significantly more benefits from a shared expense. It requires open communication and a willingness to compromise to maintain financial equity.

- Identify Unequal Benefits: Identify situations where one partner benefits more from a shared expense, such as a car primarily used by one partner.

- Calculate Benefit Disparity: Calculate the monetary value of the unequal benefit.

- Adjust Contributions: Adjust each partner’s contributions to compensate for the unequal benefit.

5. Common Pitfalls and How to Avoid Them

Avoiding common pitfalls in bill splitting requires awareness, communication, and a proactive approach to problem-solving. Understanding these challenges and implementing strategies to overcome them is essential for maintaining a harmonious financial partnership.

5.1. Lack of Communication

Lack of communication can lead to misunderstandings and resentment, undermining the effectiveness of the bill-splitting arrangement. Open and honest communication is essential for addressing concerns and ensuring both partners feel heard and valued.

- Schedule Regular Check-Ins: Set aside time to discuss financial matters and address any concerns.

- Be Open and Honest: Share financial information openly and honestly.

- Listen Actively: Listen to your partner’s concerns and perspectives.

5.2. Resentment Over Income Disparity

Resentment over income disparity can strain the relationship, creating tension and undermining financial harmony. Addressing this requires empathy, understanding, and a willingness to find a fair and equitable solution.

- Acknowledge Feelings: Acknowledge and validate each partner’s feelings about income disparity.

- Focus on Fairness: Focus on creating a bill-splitting arrangement that feels fair to both partners.

- Express Gratitude: Express gratitude for each other’s contributions to the household.

5.3. Unclear Expectations

Unclear expectations can lead to misunderstandings and conflict, undermining the effectiveness of the bill-splitting arrangement. Clearly defining shared expenses, contributions, and financial goals is essential for setting expectations and promoting transparency.

- Define Shared Expenses: Clearly define which expenses are shared and which are individual.

- Determine Contributions: Clearly determine each partner’s proportional contribution.

- Set Financial Goals: Set clear financial goals and discuss how they will be achieved.

5.4. Neglecting Periodic Reviews

Neglecting periodic reviews can cause the bill-splitting arrangement to become outdated and unfair, as income and expenses change over time. Regularly reviewing and adjusting the arrangement ensures it remains relevant and equitable.

- Schedule Regular Reviews: Set a recurring date to review the arrangement.

- Assess Income Changes: Evaluate any changes in each partner’s income.

- Evaluate Expense Changes: Review shared expenses and adjust contributions as needed.

5.5. Ignoring Individual Financial Needs

Ignoring individual financial needs can create financial stress and resentment, undermining the effectiveness of the bill-splitting arrangement. Balancing shared expenses with individual financial needs is essential for maintaining financial well-being.

- Allocate Personal Funds: Ensure each partner has sufficient funds for personal expenses.

- Respect Individual Goals: Respect each partner’s individual financial goals.

- Communicate Needs: Communicate individual financial needs openly and honestly.

6. Seeking Professional Advice

Seeking professional advice can provide valuable insights and guidance, ensuring couples establish a fair and effective bill-splitting arrangement. Financial advisors and relationship therapists can offer unbiased perspectives and tailored solutions to address unique financial circumstances.

6.1. When to Consult a Financial Advisor

Consulting a financial advisor is beneficial when couples face complex financial situations, such as significant income disparities, debt management challenges, or long-term financial planning needs. A financial advisor can provide expert guidance and personalized recommendations.

- Complex Financial Situations: Significant income disparities, debt management challenges.

- Long-Term Financial Planning: Retirement planning, investment strategies.

- Unbiased Advice: Objective guidance and personalized recommendations.

6.2. The Role of Relationship Counseling

Relationship counseling can help couples navigate financial conflicts and improve communication, fostering a healthier financial partnership. A therapist can provide tools and strategies for addressing underlying issues and promoting mutual understanding.

- Financial Conflicts: Recurring disagreements about money.

- Communication Issues: Difficulty discussing financial matters openly and honestly.

- Improved Understanding: Strategies for addressing underlying issues and promoting mutual understanding.

6.3. Resources Available at Income-Partners.net

At income-partners.net, we provide resources and tools to assist couples in establishing and maintaining equitable bill-splitting arrangements. Our platform offers expert advice, customizable templates, and a supportive community to help you navigate your financial partnership.

- Expert Advice: Access to articles, guides, and insights from financial professionals.

- Customizable Templates: Tools for calculating income percentages, shared expenses, and individual contributions.

- Supportive Community: Connect with other couples and share experiences and advice.

Address: 1 University Station, Austin, TX 78712, United States.

Phone: +1 (512) 471-3434.

Website: income-partners.net.

7. Optimizing Your Financial Partnership

Optimizing your financial partnership involves ongoing effort, communication, and a commitment to fairness. It ensures that both partners feel valued, respected, and aligned in their financial goals.

7.1. Regular Financial Check-Ins

Regular financial check-ins are essential for maintaining transparency and addressing any emerging issues. Scheduling these meetings ensures both partners stay informed and engaged in their financial partnership.

- Set a Recurring Schedule: Establish a regular schedule for financial check-ins, such as monthly or quarterly.

- Review Financial Goals: Discuss progress toward shared financial goals and make any necessary adjustments.

- Address Concerns: Provide a forum for addressing any financial concerns or issues.

7.2. Celebrating Financial Milestones

Celebrating financial milestones reinforces positive financial habits and strengthens the partnership, encouraging continued commitment to shared goals. Recognizing achievements, big or small, promotes a sense of accomplishment and mutual support.

- Acknowledge Achievements: Recognize and celebrate financial milestones, such as paying off debt or reaching a savings goal.

- Plan a Reward: Plan a small reward or celebration to commemorate the achievement.

- Express Appreciation: Express appreciation for each other’s contributions to the financial partnership.

7.3. Continuous Learning and Adaptation

Continuous learning and adaptation are essential for navigating evolving financial landscapes and maintaining a resilient financial partnership. Staying informed about financial trends and adapting your approach as needed ensures long-term success.

- Stay Informed: Stay informed about financial trends and best practices.

- Adapt as Needed: Adapt your bill-splitting arrangement to accommodate changes in income, expenses, or financial goals.

- Seek Professional Advice: Consult financial advisors or relationship therapists as needed to address complex issues.

8. Success Stories: Income-Based Bill Splitting in Action

Hearing success stories can inspire and motivate couples to implement income-based bill splitting, demonstrating its real-world benefits. These examples highlight the positive impact of fair financial arrangements on relationships.

8.1. The Johnson’s Story

The Johnsons, a couple with a significant income disparity, implemented income-based bill splitting to reduce financial stress and improve communication. They found that the arrangement fostered a sense of fairness and strengthened their partnership.

- Challenge: Significant income disparity leading to financial stress.

- Solution: Implemented income-based bill splitting.

- Outcome: Reduced financial stress, improved communication, strengthened partnership.

8.2. The Garcia’s Experience

The Garcias, facing debt management challenges, incorporated debt payments into their bill-splitting arrangement. This helped them manage their debt more effectively and achieve their financial goals.

- Challenge: Debt management challenges impacting financial stability.

- Solution: Incorporated debt payments into the bill-splitting arrangement.

- Outcome: Improved debt management, achieved financial goals, reduced financial strain.

8.3. The Lee’s Journey

The Lees, navigating a career change, adjusted their bill-splitting arrangement to accommodate the temporary income reduction. This helped them maintain financial stability and navigate the transition smoothly.

- Challenge: Career change resulting in temporary income reduction.

- Solution: Adjusted bill-splitting arrangement to accommodate income changes.

- Outcome: Maintained financial stability, navigated career transition smoothly, strengthened partnership.

9. Resources and Tools for Effective Bill Splitting

Utilizing available resources and tools can streamline the bill-splitting process, making it more efficient and transparent. These resources provide valuable support and guidance for couples seeking to establish equitable financial arrangements.

9.1. Online Calculators

Online calculators simplify the process of calculating income percentages and individual contributions, providing quick and accurate results. These tools eliminate the need for manual calculations, saving time and reducing the risk of errors.

- Income Percentage Calculators: Calculate each partner’s income percentage.

- Contribution Calculators: Determine each partner’s proportional contribution.

- Shared Expense Calculators: Calculate total shared expenses.

9.2. Budgeting Apps

Budgeting apps provide a comprehensive platform for tracking expenses, managing budgets, and monitoring financial progress. These tools offer real-time insights into spending habits and financial performance, empowering couples to make informed decisions.

- Expense Tracking: Monitor spending habits and identify areas for improvement.

- Budget Management: Create and manage budgets for shared expenses.

- Financial Progress Tracking: Monitor progress toward financial goals.

9.3. Spreadsheet Templates

Spreadsheet templates offer a customizable solution for organizing financial data and tracking bill-splitting arrangements. These templates can be tailored to meet the specific needs of each couple, providing a flexible and adaptable tool.

- Customizable Format: Tailor the template to meet your specific needs.

- Data Organization: Organize financial data in a clear and structured manner.

- Tracking Capabilities: Track bill-splitting arrangements and monitor progress.

10. Frequently Asked Questions (FAQs)

10.1. What if our incomes fluctuate monthly?

Calculate the average income over the last three to six months to smooth out fluctuations and determine a stable percentage. Review and adjust quarterly.

10.2. How do we handle unexpected expenses?

Establish an emergency fund to cover unexpected expenses. Both partners contribute proportionally based on their income.

10.3. Should we include retirement contributions in shared expenses?

Consider including retirement contributions to ensure both partners are equally investing in their future.

10.4. What if one partner is a stay-at-home parent?

Acknowledge the value of the stay-at-home parent’s contributions and assign a monetary value to their work when calculating income percentages.

10.5. How often should we review our bill-splitting arrangement?

Review your bill-splitting arrangement at least quarterly to account for changes in income, expenses, and financial goals.

10.6. What if one partner has significantly more debt?

Incorporate debt payments into shared expenses to ensure fairness, adjusting contributions accordingly.

10.7. How do we handle disagreements about spending?

Establish clear communication guidelines and spending limits to prevent conflicts. Seek relationship counseling if needed.

10.8. Should we have separate bank accounts?

Maintaining separate accounts while using a joint account for shared expenses can provide both autonomy and transparency.

10.9. What if one partner receives a bonus or raise?

Re-evaluate income percentages to ensure contributions remain proportional after significant income changes.

10.10. How do we handle gifts and personal spending?

Establish clear guidelines for personal spending to ensure it doesn’t impact shared financial goals.

Dividing bills based on income is more than just a financial strategy; it’s a commitment to fairness, transparency, and mutual respect in your partnership. By following the steps outlined in this guide, customizing your plan to fit your unique circumstances, and maintaining open communication, you can create a financial arrangement that supports your relationship and helps you achieve your shared goals.

Ready to take the next step? Visit income-partners.net to discover more resources, connect with financial experts, and find the perfect partner to help you achieve your financial aspirations. Explore our comprehensive guides, customizable templates, and supportive community to optimize your financial partnership today. Start building a stronger, more equitable financial foundation at income-partners.net.