Income tax can significantly impact your potential revenue. This guide breaks down the costs, offering strategies to optimize your tax situation and maximize your earnings through strategic partnerships, all with the support of income-partners.net. Let’s explore income tax implications, effective tax planning, and collaborative opportunities.

1. What are the Key Factors Influencing How Much Income Tax Costs?

The cost of income tax hinges on various elements, including your filing status, total taxable income, applicable deductions, and tax credits. Understanding these components helps in effective tax planning and potentially lowers your tax burden.

- Filing Status: Your filing status—single, married filing jointly, head of household, etc.—determines your tax bracket and standard deduction amount. For example, married couples filing jointly usually have higher income thresholds for each tax bracket than single filers.

- Taxable Income: This is your adjusted gross income (AGI) minus any itemized or standard deductions. AGI includes wages, salaries, tips, investment income, and other earnings.

- Deductions: Deductions reduce your taxable income. Common deductions include the standard deduction, itemized deductions (like mortgage interest, state and local taxes up to $10,000, and charitable contributions), and deductions for business expenses.

- Tax Credits: Tax credits directly reduce your tax liability. They are more valuable than deductions because they lower the amount of tax you owe dollar-for-dollar. Examples include the Child Tax Credit, Earned Income Tax Credit, and credits for education expenses.

- Tax Planning Strategies: Implementing tax-efficient strategies, such as contributing to retirement accounts (401(k), IRA), investing in tax-advantaged accounts (like Health Savings Accounts), and timing income and expenses, can significantly affect your tax outcome.

For those seeking to boost their income through strategic alliances, understanding these tax implications is crucial. Explore resources and partnership opportunities at income-partners.net to further enhance your financial strategies.

2. What are the Current U.S. Federal Income Tax Brackets?

Understanding U.S. federal income tax brackets is key to estimating your income tax liability; these brackets determine the tax rate applied to each portion of your income. Tax brackets are adjusted annually to account for inflation.

| Tax Rate | Single Filers | Married Filing Jointly | Head of Household |

|---|---|---|---|

| 10% | $0 to $11,600 | $0 to $23,200 | $0 to $17,400 |

| 12% | $11,601 to $47,150 | $23,201 to $82,350 | $17,401 to $59,475 |

| 22% | $47,151 to $100,525 | $82,351 to $172,750 | $59,476 to $132,200 |

| 24% | $100,526 to $191,950 | $172,751 to $343,900 | $132,201 to $255,350 |

| 32% | $191,951 to $243,725 | $343,901 to $487,450 | $255,351 to $510,900 |

| 35% | $243,726 to $609,350 | $487,451 to $731,200 | $510,901 to $609,350 |

| 37% | Over $609,350 | Over $731,200 | Over $609,350 |

Note: These brackets are for the 2024 tax year, filed in 2025.

Understanding Progressive Taxation

The U.S. tax system is progressive, meaning that higher incomes are taxed at higher rates. Each bracket is taxed at its specific rate.

For example, if you’re single and have a taxable income of $60,000, your tax is calculated as follows:

- 10% on income from $0 to $11,600 = $1,160

- 12% on income from $11,601 to $47,150 = $4,265.88

- 22% on income from $47,151 to $60,000 = $2,826.78

Total tax = $1,160 + $4,265.88 + $2,826.78 = $8,252.66

Strategic Income Planning

Understanding your tax bracket can help in strategic income planning. If you’re close to a higher tax bracket, consider strategies to reduce your taxable income, such as increasing contributions to tax-deferred retirement accounts.

For those looking to optimize their financial situation through strategic partnerships, income-partners.net offers resources and connections to explore collaborative opportunities.

3. What are Common Income Tax Deductions and Credits to Reduce Tax Costs?

Tax deductions and credits are powerful tools to reduce your income tax liability. Deductions lower your taxable income, while credits directly reduce the amount of tax you owe.

Standard Deduction

The standard deduction is a fixed amount based on your filing status. For 2024, these are:

- Single: $14,600

- Married Filing Jointly: $29,200

- Head of Household: $21,900

Many taxpayers choose the standard deduction for its simplicity.

Itemized Deductions

Itemized deductions involve listing individual deductible expenses. You should itemize if your total itemized deductions exceed your standard deduction. Common itemized deductions include:

- Medical Expenses: You can deduct medical expenses exceeding 7.5% of your adjusted gross income (AGI).

- State and Local Taxes (SALT): You can deduct state and local taxes, including property taxes and either state income taxes or sales taxes, up to a combined limit of $10,000.

- Mortgage Interest: You can deduct interest paid on a mortgage for a primary or secondary residence, subject to certain limitations.

- Charitable Contributions: You can deduct contributions to qualified charitable organizations, typically up to 60% of your AGI for cash contributions and 50% for other property.

Tax Credits

Tax credits offer a dollar-for-dollar reduction in your tax liability, making them highly valuable. Key tax credits include:

- Child Tax Credit: For 2024, the child tax credit is worth up to $2,000 per qualifying child.

- Earned Income Tax Credit (EITC): This credit benefits low-to-moderate income individuals and families. The amount of the credit depends on your income and the number of qualifying children.

- Child and Dependent Care Credit: If you pay for childcare to work or look for work, you may be eligible for this credit.

- Education Credits: The American Opportunity Tax Credit (AOTC) and the Lifetime Learning Credit help offset the costs of higher education.

Strategic Use of Deductions and Credits

Maximize your tax savings by tracking and utilizing all eligible deductions and credits. Determine whether itemizing or taking the standard deduction results in a lower tax liability.

For those aiming to increase their income through partnerships, leveraging these deductions and credits can optimize your financial benefits. Explore strategic collaborations at income-partners.net to enhance your earnings.

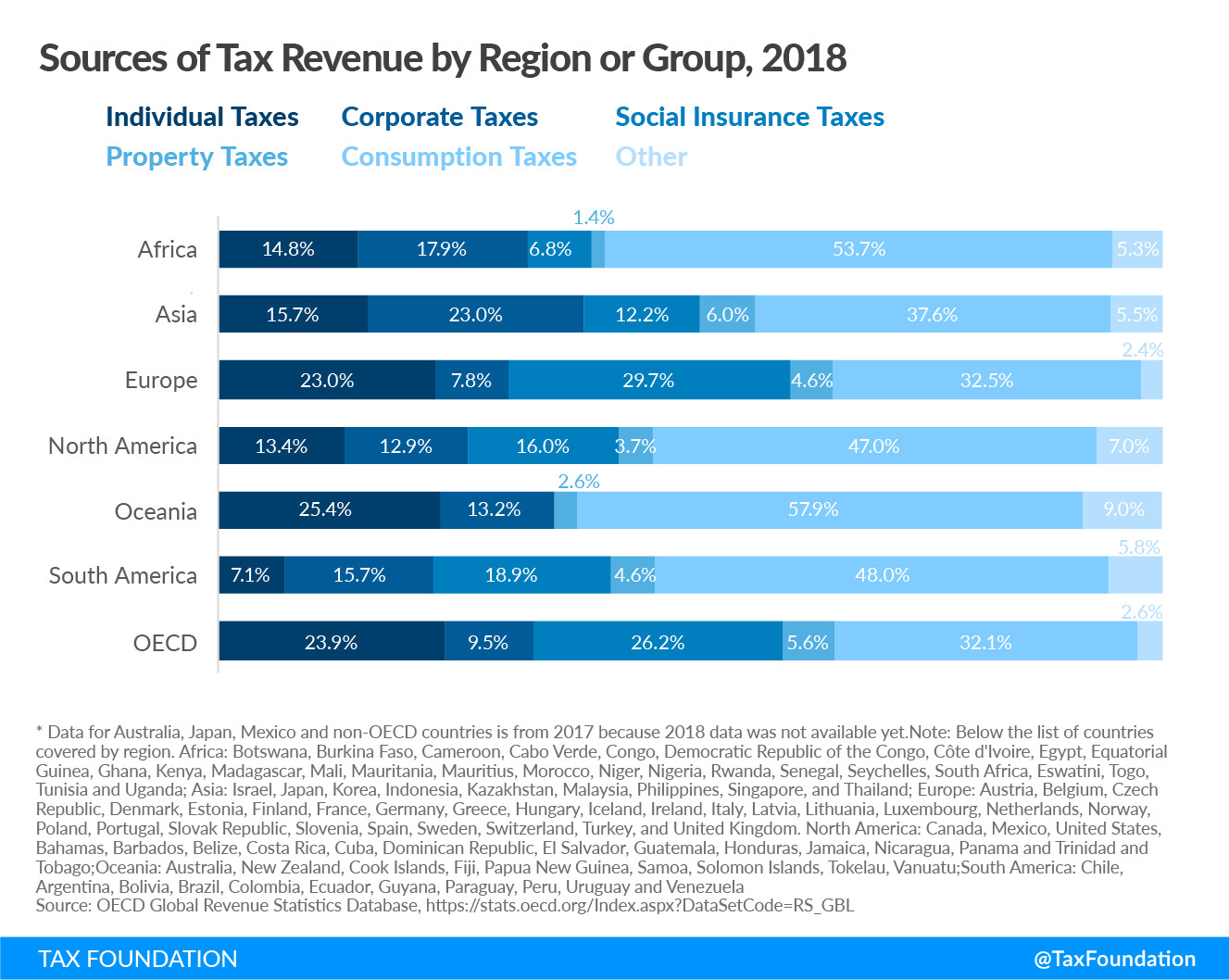

Tax strategy Sources of Tax Revenue by Region or Group 2018

Tax strategy Sources of Tax Revenue by Region or Group 2018

4. How Does Income Tax Affect Different Business Structures?

The impact of income tax varies significantly based on the business structure you choose. Each structure has its own tax implications, affecting your overall tax liability.

Sole Proprietorship

A sole proprietorship is the simplest business structure, where the business is owned and run by one person. Income is reported on Schedule C of your personal income tax return (Form 1040).

- Taxation: Profits are taxed at your individual income tax rate.

- Self-Employment Tax: You’ll also pay self-employment tax (Social Security and Medicare taxes) on your profits.

- Deductions: You can deduct business expenses on Schedule C, reducing your taxable income.

Partnership

A partnership involves two or more individuals who agree to share in the profits or losses of a business.

- Taxation: Partnerships file an information return (Form 1065) but do not pay income tax. Instead, profits and losses are passed through to the partners, who report their share on their individual income tax returns (Form 1040).

- Self-Employment Tax: Partners pay self-employment tax on their share of the partnership’s profits.

- Deductions: Partners can deduct business expenses related to their partnership income.

Limited Liability Company (LLC)

An LLC offers liability protection similar to a corporation but with simpler operational procedures. LLCs can choose how they are taxed:

- Single-Member LLC: Treated as a sole proprietorship for tax purposes (reported on Schedule C).

- Partnership LLC: Treated as a partnership for tax purposes (files Form 1065, and income passes through to members).

- Corporation (C-Corp): Can elect to be taxed as a C-Corp, which means the LLC pays corporate income tax on its profits, and shareholders pay individual income tax on dividends received.

- S Corporation (S-Corp): Can elect to be taxed as an S-Corp, which allows profits and losses to be passed through to the owners’ individual tax returns, avoiding double taxation (files Form 1120-S).

Corporation (C-Corp)

A C-Corp is a separate legal entity from its owners and is subject to corporate income tax.

- Taxation: C-Corps pay corporate income tax on their profits. Shareholders also pay individual income tax on dividends received, resulting in double taxation.

- Deductions: C-Corps can deduct business expenses, which reduces their taxable income.

- Tax Rate: The corporate income tax rate is a flat 21%.

S Corporation (S-Corp)

An S-Corp is a corporation that has elected to pass its income, losses, deductions, and credits through to its shareholders.

- Taxation: Profits and losses are passed through to the shareholders’ individual income tax returns (Form 1040), avoiding double taxation.

- Deductions: S-Corps can deduct business expenses, and shareholders report their share of the corporation’s income and deductions on their individual returns.

- Reasonable Salary: Shareholders who work for the S-Corp must be paid a reasonable salary, which is subject to payroll taxes.

Strategic Tax Planning

Choosing the right business structure is critical for tax efficiency. Consider factors such as liability protection, tax rates, and administrative complexity when making your decision.

For those seeking to expand their income through partnerships, understanding these tax implications is crucial for strategic financial planning. Explore resources and collaboration opportunities at income-partners.net.

5. What is the Difference Between Tax Planning and Tax Evasion?

Understanding the distinction between tax planning and tax evasion is crucial. Tax planning is a legal strategy to minimize your tax liability, while tax evasion is an illegal act.

Tax Planning

Tax planning involves using legal means to reduce your tax liability. It includes:

- Taking advantage of deductions and credits: Claiming all eligible deductions and credits to lower your taxable income or tax liability.

- Choosing the right business structure: Selecting a business structure that minimizes taxes based on your specific circumstances.

- Investing in tax-advantaged accounts: Contributing to retirement accounts (401(k), IRA) or health savings accounts (HSA) to defer or avoid taxes.

- Timing income and expenses: Strategically timing when you recognize income or incur expenses to minimize your tax liability in a given year.

- Using tax-efficient investments: Investing in assets that generate tax-favored income, such as municipal bonds.

Tax planning is a proactive approach to managing your taxes effectively.

Tax Evasion

Tax evasion involves illegal activities to avoid paying taxes. Examples include:

- Underreporting income: Failing to report all income earned.

- Claiming false deductions or credits: Claiming deductions or credits that you are not entitled to.

- Hiding assets: Concealing assets to avoid paying taxes on them.

- Failing to file tax returns: Not filing required tax returns.

- Using offshore accounts to hide income: Hiding income in foreign accounts to evade U.S. taxes.

Tax evasion is a serious crime that can result in severe penalties, including fines and imprisonment.

Ethical Considerations

While tax planning is legal and encouraged, it is essential to stay within the bounds of the law. Avoid aggressive tax strategies that could be considered abusive or illegal. Work with qualified tax professionals to ensure your tax planning strategies are compliant with tax laws and regulations.

For those seeking to enhance their income through partnerships, maintaining ethical and legal tax practices is paramount. Explore responsible financial strategies and partnership opportunities at income-partners.net.

Difference between tax planning and tax evasion Businesses Are Central to US Tax Collections

Difference between tax planning and tax evasion Businesses Are Central to US Tax Collections

6. What Are State and Local Income Taxes and How Do They Work?

In addition to federal income taxes, many states and some localities also impose income taxes. These taxes can significantly impact your overall tax burden.

State Income Taxes

Most states have a state income tax, which is typically calculated as a percentage of your federal adjusted gross income (AGI) or taxable income. However, some states, like Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington, and Wyoming, do not have a state income tax.

- Tax Rates: State income tax rates vary widely. Some states have a flat tax rate, where all income is taxed at the same rate, while others have progressive tax rates similar to the federal system.

- Deductions and Credits: States may offer their own set of deductions and credits, which can differ from federal deductions and credits. Common state deductions include deductions for state and local taxes (SALT), retirement contributions, and education expenses. State credits may include credits for child care, energy efficiency, and charitable contributions.

- Tax Forms: You’ll need to file a separate state income tax return in addition to your federal return. State tax forms and filing deadlines may differ from federal requirements.

Local Income Taxes

Some cities and counties also impose local income taxes, which are typically a small percentage of your income.

- Tax Rates: Local income tax rates are generally low but can add up, especially in areas with high local tax rates.

- Tax Base: Local income taxes may be based on your wages, net profits from self-employment, or other types of income.

- Administration: Local income taxes are often administered by the state or a local tax authority.

Impact on Overall Tax Burden

State and local income taxes can significantly increase your overall tax burden, especially if you live in a high-tax state or locality. When evaluating the cost of living in different areas, consider the impact of state and local income taxes.

Tax Planning Strategies

- Maximize State Deductions and Credits: Take advantage of all eligible state deductions and credits to reduce your state income tax liability.

- Consider Location: If you have the flexibility to move, consider living in a state or locality with lower income taxes.

- Consult a Tax Professional: Work with a tax professional who is familiar with state and local tax laws to optimize your tax planning strategies.

For those looking to expand their income through partnerships, understanding state and local income taxes is crucial for effective financial planning. Explore resources and collaboration opportunities at income-partners.net.

7. How Do Capital Gains and Dividends Impact Your Income Tax?

Capital gains and dividends are types of investment income that are taxed differently from ordinary income. Understanding how these are taxed can help you optimize your investment strategies and minimize your tax liability.

Capital Gains

Capital gains result from the sale of assets, such as stocks, bonds, real estate, and other investments. There are two types of capital gains:

- Short-Term Capital Gains: These are profits from assets held for one year or less. Short-term capital gains are taxed at your ordinary income tax rate.

- Long-Term Capital Gains: These are profits from assets held for more than one year. Long-term capital gains are taxed at preferential rates, which are generally lower than ordinary income tax rates.

Long-Term Capital Gains Tax Rates (2024)

| Taxable Income | Single Filers | Married Filing Jointly | Head of Household | Rate |

|---|---|---|---|---|

| $0 to $47,025 | $0 to $47,025 | $0 to $94,050 | $0 to $63,000 | 0% |

| $47,026 to $518,900 | $47,026 to $518,900 | $94,051 to $583,750 | $63,001 to $518,900 | 15% |

| Over $518,900 | Over $518,900 | Over $583,750 | Over $518,900 | 20% |

Dividends

Dividends are distributions of a company’s earnings to its shareholders. There are two types of dividends:

- Qualified Dividends: These are dividends that meet certain requirements and are taxed at the same preferential rates as long-term capital gains.

- Ordinary Dividends: These are dividends that do not meet the requirements for qualified dividends and are taxed at your ordinary income tax rate.

Tax Planning Strategies for Capital Gains and Dividends

- Hold Assets Longer Than One Year: To qualify for long-term capital gains rates, hold your assets for more than one year.

- Tax-Loss Harvesting: Use capital losses to offset capital gains. If your capital losses exceed your capital gains, you can deduct up to $3,000 of the excess loss against your ordinary income.

- Invest in Tax-Advantaged Accounts: Hold investments that generate capital gains and dividends in tax-advantaged accounts, such as retirement accounts, to defer or avoid taxes.

- Consider Tax Efficiency When Investing: When choosing investments, consider their tax efficiency. For example, municipal bonds are exempt from federal income tax and may be exempt from state and local income taxes as well.

For those seeking to increase their income through partnerships, understanding the tax implications of capital gains and dividends is crucial for effective investment planning. Explore resources and collaboration opportunities at income-partners.net.

8. What is the Impact of Self-Employment Tax on Independent Contractors?

Self-employment tax is a significant consideration for independent contractors and freelancers. Unlike employees, who have Social Security and Medicare taxes withheld from their paychecks, self-employed individuals are responsible for paying both the employer and employee portions of these taxes.

Understanding Self-Employment Tax

Self-employment tax consists of Social Security and Medicare taxes. For 2024, the self-employment tax rates are:

- Social Security: 12.4% on the first $168,600 of net self-employment income

- Medicare: 2.9% on all net self-employment income

This means that self-employed individuals pay a combined 15.3% in self-employment taxes.

Calculating Self-Employment Tax

To calculate your self-employment tax, you’ll need to complete Schedule SE (Form 1040), Self-Employment Tax.

- Calculate Net Earnings: Start by calculating your net earnings from self-employment. This is your gross income minus business expenses.

- Multiply by 0.9235: Multiply your net earnings by 0.9235. This adjustment accounts for the fact that employees do not pay Social Security and Medicare taxes on the employer’s share of these taxes.

- Calculate Social Security Tax: Multiply the result from step 2 by 12.4% (up to the Social Security wage base of $168,600).

- Calculate Medicare Tax: Multiply the result from step 2 by 2.9%.

- Total Self-Employment Tax: Add the Social Security tax and Medicare tax to get your total self-employment tax.

Deduction for One-Half of Self-Employment Tax

You can deduct one-half of your self-employment tax from your gross income. This deduction is taken on Form 1040, Schedule 1, line 15. This deduction reduces your adjusted gross income (AGI), which can lower your overall tax liability.

Tax Planning Strategies for Self-Employed Individuals

- Track Business Expenses: Keep detailed records of all business expenses, as these can be deducted from your gross income, reducing your net self-employment income.

- Consider Retirement Contributions: Contributing to a retirement plan, such as a SEP IRA or Solo 401(k), can reduce your taxable income and provide tax-deferred savings for retirement.

- Form an S Corporation: If you have significant self-employment income, consider forming an S Corporation. As an S-Corp, you can pay yourself a reasonable salary and take the remaining profits as a distribution, which is not subject to self-employment tax.

For those seeking to enhance their income through partnerships, understanding self-employment tax is crucial for managing your finances effectively. Explore resources and collaboration opportunities at income-partners.net.

9. How Can Estimated Taxes Help You Avoid Penalties?

Estimated taxes are a way for self-employed individuals, investors, and others who don’t have taxes withheld from their income to pay their income tax and self-employment tax throughout the year. Paying estimated taxes can help you avoid penalties for underpayment of taxes.

Who Needs to Pay Estimated Taxes?

You generally need to pay estimated taxes if:

- You expect to owe at least $1,000 in taxes for the year after subtracting your withholding and refundable credits.

- Your withholding and refundable credits are less than the smaller of:

- 90% of the tax shown on the return for the year in question, or

- 100% of the tax shown on the return for the prior year.

When to Pay Estimated Taxes

Estimated taxes are typically paid in four quarterly installments. The due dates for these installments are:

- April 15

- June 15

- September 15

- January 15 of the following year

If any of these dates fall on a weekend or holiday, the due date is shifted to the next business day.

How to Calculate Estimated Taxes

To calculate your estimated taxes, you’ll need to estimate your income, deductions, and credits for the year. You can use Form 1040-ES, Estimated Tax for Individuals, to help you calculate your estimated tax liability.

- Estimate Your Income: Estimate your total income for the year, including wages, self-employment income, investment income, and other sources of income.

- Estimate Your Deductions: Estimate your deductions, including the standard deduction or itemized deductions, as well as any other deductions you are eligible for.

- Estimate Your Credits: Estimate your tax credits, such as the Child Tax Credit, Earned Income Tax Credit, and other credits.

- Calculate Your Tax Liability: Use the tax rates for the year to calculate your estimated tax liability.

- Calculate Your Self-Employment Tax: If you are self-employed, calculate your estimated self-employment tax using Schedule SE (Form 1040).

- Determine Your Estimated Tax Payments: Divide your estimated tax liability by four to determine the amount of each quarterly payment.

Avoiding Penalties

To avoid penalties for underpayment of taxes, you must pay enough estimated tax throughout the year. There are several ways to avoid penalties:

- Pay 90% of the Current Year’s Tax: Pay at least 90% of the tax shown on your current year’s tax return.

- Pay 100% of the Prior Year’s Tax: Pay 100% of the tax shown on your prior year’s tax return. This option is available if your prior year’s tax return covered a 12-month period.

- Use the Annualized Income Installment Method: If your income varies throughout the year, you can use the annualized income installment method to adjust your estimated tax payments based on your income for each quarter.

For those seeking to increase their income through partnerships, understanding estimated taxes is crucial for managing your finances effectively and avoiding penalties. Explore resources and collaboration opportunities at income-partners.net.

10. What are the Best Tax Planning Tips for Maximizing Your Income?

Effective tax planning is essential for maximizing your income and minimizing your tax liability. By implementing strategic tax planning techniques, you can optimize your financial situation and keep more of what you earn.

Maximize Retirement Contributions

Contributing to retirement accounts is one of the most effective ways to reduce your taxable income.

- 401(k): If you have access to a 401(k) plan through your employer, contribute as much as possible, especially if your employer offers matching contributions.

- IRA: Contribute to a traditional IRA or Roth IRA, depending on your eligibility and financial goals. Traditional IRA contributions are tax-deductible, while Roth IRA contributions are not, but qualified withdrawals in retirement are tax-free.

- SEP IRA or Solo 401(k): If you are self-employed, consider contributing to a SEP IRA or Solo 401(k). These plans allow you to contribute a significant portion of your self-employment income and deduct the contributions from your taxable income.

Take Advantage of All Eligible Deductions and Credits

Ensure you are taking advantage of all eligible deductions and credits to reduce your tax liability.

- Itemize Deductions: If your itemized deductions exceed the standard deduction, itemize on Schedule A (Form 1040).

- Claim Tax Credits: Claim all eligible tax credits, such as the Child Tax Credit, Earned Income Tax Credit, and education credits.

Invest in Tax-Advantaged Accounts

Consider investing in tax-advantaged accounts to defer or avoid taxes on your investment income.

- Health Savings Account (HSA): If you have a high-deductible health plan, contribute to an HSA. Contributions are tax-deductible, earnings grow tax-free, and withdrawals for qualified medical expenses are tax-free.

- 529 Plan: If you have children, consider investing in a 529 plan to save for their education expenses. Earnings grow tax-free, and withdrawals for qualified education expenses are tax-free.

Consider Tax Efficiency When Investing

When choosing investments, consider their tax efficiency.

- Municipal Bonds: Invest in municipal bonds, which are exempt from federal income tax and may be exempt from state and local income taxes as well.

- Tax-Advantaged Funds: Invest in tax-advantaged mutual funds or ETFs that are designed to minimize capital gains and dividend distributions.

Time Income and Expenses

Strategically time when you recognize income or incur expenses to minimize your tax liability in a given year.

- Defer Income: If possible, defer income to a future year when you expect to be in a lower tax bracket.

- Accelerate Expenses: If possible, accelerate expenses into a current year when you expect to be in a higher tax bracket.

Work with a Tax Professional

Consult with a qualified tax professional who can provide personalized tax planning advice based on your specific financial situation. A tax professional can help you identify tax-saving opportunities and ensure you are compliant with tax laws and regulations.

For those seeking to enhance their income through partnerships, implementing these tax planning tips can help you maximize your earnings and minimize your tax liability. Explore resources and collaboration opportunities at income-partners.net.

Income tax considerations are critical for entrepreneurs. To maximize your income and minimize your tax burden, explore partnership opportunities and resources at income-partners.net, located at 1 University Station, Austin, TX 78712, United States, or call +1 (512) 471-3434.

FAQ: Navigating Income Tax Costs

Here are some frequently asked questions to help you better understand income tax costs and how to manage them effectively.

-

What is the difference between a tax deduction and a tax credit?

A tax deduction reduces your taxable income, while a tax credit directly reduces the amount of tax you owe. Tax credits are generally more valuable than deductions because they provide a dollar-for-dollar reduction in your tax liability.

-

How do I know if I should itemize deductions or take the standard deduction?

You should itemize deductions if your total itemized deductions exceed the standard deduction for your filing status. Common itemized deductions include medical expenses, state and local taxes (limited to $10,000), mortgage interest, and charitable contributions.

-

What is self-employment tax, and who has to pay it?

Self-employment tax is the Social Security and Medicare tax that self-employed individuals must pay. It applies to anyone who earns $400 or more in net self-employment income during the year.

-

How can I reduce my self-employment tax liability?

You can reduce your self-employment tax liability by deducting business expenses, contributing to a retirement plan (such as a SEP IRA or Solo 401(k)), and considering forming an S Corporation if you have significant self-employment income.

-

What are estimated taxes, and why do I need to pay them?

Estimated taxes are payments made throughout the year to cover income tax and self-employment tax obligations. You need to pay estimated taxes if you expect to owe at least $1,000 in taxes and your withholding and refundable credits are less than 90% of the current year’s tax or 100% of the prior year’s tax.

-

What are the penalties for underpaying estimated taxes?

The penalty for underpaying estimated taxes varies depending on the amount of the underpayment and the length of time it goes unpaid. To avoid penalties, you should pay at least 90% of the current year’s tax or 100% of the prior year’s tax.

-

How can I minimize my income tax liability?

You can minimize your income tax liability by maximizing retirement contributions, taking advantage of all eligible deductions and credits, investing in tax-advantaged accounts, considering tax efficiency when investing, and timing income and expenses strategically.

-

What is the difference between short-term and long-term capital gains?

Short-term capital gains are profits from assets held for one year or less and are taxed at your ordinary income tax rate. Long-term capital gains are profits from assets held for more than one year and are taxed at preferential rates, which are generally lower than ordinary income tax rates.

-

How do dividends affect my income tax?

Dividends are distributions of a company’s earnings to its shareholders. Qualified dividends are taxed at the same preferential rates as long-term capital gains, while ordinary dividends are taxed at your ordinary income tax rate.

-

Where can I get help with tax planning and preparation?

You can get help with tax planning and preparation from a qualified tax professional, such as a Certified Public Accountant (CPA) or an Enrolled Agent (EA). These professionals can provide personalized tax advice based on your specific financial situation and ensure you are compliant with tax laws and regulations.

This FAQ aims to provide clarity on common income tax questions. For personalized advice and partnership opportunities, visit income-partners.net and connect with our experts.