How Much Tax On 1099 Income is a common question for independent contractors and freelancers. Understanding your 1099 tax obligations is crucial for effective financial planning and maximizing your income; at income-partners.net, we provide the resources and strategies you need to navigate the complexities of self-employment taxes. We offer comprehensive guidance to help you accurately calculate your tax liability and identify valuable partnership opportunities to boost your earnings. Let’s explore how to manage your taxes and unlock your income potential!

1. Understanding 1099 Income and Self-Employment Tax

What exactly is 1099 income and how does self-employment tax factor in? 1099 income is the money you earn as an independent contractor or freelancer, and self-employment tax covers Social Security and Medicare obligations. Let’s break down the essentials.

When you work as an employee, your employer withholds taxes from your paycheck and pays half of your Social Security and Medicare taxes. As a 1099 contractor, you’re responsible for both the employee and employer portions of these taxes, which is what we call self-employment tax. This tax applies to 92.35% of your net earnings, and the combined rate for Social Security and Medicare is 15.3% (12.4% for Social Security and 2.9% for Medicare). Understanding this is the first step in managing your tax responsibilities.

To delve deeper, consider these key aspects:

- Self-Employment Tax Calculation: You calculate this tax on IRS Schedule SE. The tax applies if your net earnings from self-employment are $400 or more.

- Deductibility: The good news is you can deduct one-half of your self-employment tax from your gross income.

- Impact on Estimated Taxes: Because you’re responsible for paying both income tax and self-employment tax, you might need to make estimated tax payments quarterly to avoid penalties.

- Resources: Income-partners.net offers resources and tools to help you estimate your tax liability and plan accordingly.

Understanding these nuances can make a significant difference in your financial planning, helping you avoid surprises when tax season rolls around.

2. Calculating Your 1099 Tax Liability

How do you calculate your 1099 tax liability? To accurately determine your tax liability, you must factor in income tax and self-employment tax, both of which require careful calculation. Let’s walk through the steps.

Calculating your 1099 tax liability involves several key steps. First, determine your net profit by subtracting your business expenses from your gross income. Next, calculate your self-employment tax, which is 15.3% of 92.35% of your net profit. Then, calculate your income tax based on your adjusted gross income and applicable tax bracket. Keep in mind that you can deduct one-half of your self-employment tax from your gross income, which can lower your overall tax liability.

Here’s a more detailed look:

- Net Profit Calculation: Start by calculating your total business income and subtracting all deductible business expenses.

- Self-Employment Tax: Multiply 92.35% of your net profit by 15.3% to determine your self-employment tax.

- Income Tax: Calculate your adjusted gross income (AGI) by subtracting deductions like the self-employment tax deduction.

- Tax Bracket: Use your AGI to determine your income tax based on the current tax brackets.

Understanding these calculations can empower you to manage your finances effectively and avoid any unexpected tax burdens. Income-partners.net provides tools and resources to simplify this process, ensuring you are well-prepared for tax season.

3. Understanding Estimated Taxes for 1099 Income

Why are estimated taxes necessary for 1099 income earners? Estimated taxes are essential for independent contractors and freelancers to avoid penalties for underpayment of taxes throughout the year. Let’s explore this requirement in detail.

As a 1099 income earner, you’re typically required to pay estimated taxes quarterly because taxes aren’t automatically withheld from your payments like they are for employees. Estimated taxes cover both income tax and self-employment tax. The IRS generally requires you to pay at least 90% of your tax liability for the current year or 100% of the tax shown on your return for the prior year to avoid penalties.

Here are key points to remember:

- Quarterly Deadlines: The IRS has specific deadlines for each quarter, typically on April 15, June 15, September 15, and January 15 of the following year.

- Payment Methods: You can pay estimated taxes online, by mail, or through the Electronic Federal Tax Payment System (EFTPS).

- Avoiding Penalties: To avoid penalties, ensure you accurately estimate your income and pay enough tax throughout the year.

- Resources: Income-partners.net provides tools and resources to help you estimate your quarterly tax payments accurately, making tax compliance easier.

By understanding and adhering to these requirements, you can avoid unnecessary penalties and maintain better control over your finances.

4. Key Tax Deductions for 1099 Contractors

What are the most valuable tax deductions for 1099 contractors? Identifying and claiming eligible tax deductions is crucial for reducing your taxable income and lowering your overall tax bill. Let’s explore the most significant deductions available.

As a 1099 contractor, you can take advantage of numerous tax deductions to lower your taxable income. Some of the most valuable deductions include the home office deduction, business expenses (such as supplies, travel, and marketing), health insurance premiums, self-employment tax deduction, and retirement contributions. Keeping detailed records of your expenses is essential for maximizing these deductions.

Here’s a more detailed breakdown:

- Home Office Deduction: If you use a portion of your home exclusively and regularly for business, you can deduct expenses related to that space.

- Business Expenses: Deduct costs for business supplies, software, subscriptions, and other necessary items.

- Travel Expenses: You can deduct costs for travel related to your business, including transportation, lodging, and meals.

- Health Insurance Premiums: Self-employed individuals can often deduct the amount they paid in health insurance premiums.

- Retirement Contributions: Contributions to retirement accounts like SEP IRAs or solo 401(k)s are deductible.

Properly tracking and claiming these deductions can substantially reduce your tax liability. Income-partners.net offers resources and tools to help you identify and document these deductions, ensuring you take full advantage of available tax benefits.

Financial planning for 1099 contractors

Financial planning for 1099 contractors

5. Utilizing the Home Office Deduction for 1099 Income

How can you benefit from the home office deduction when earning 1099 income? The home office deduction is a significant tax benefit for 1099 income earners who use a portion of their home exclusively for business. Let’s explore the requirements and benefits.

If you use part of your home exclusively and regularly for business, you may be eligible for the home office deduction. This deduction allows you to write off a portion of your mortgage interest or rent, utilities, insurance, and other home-related expenses. The space must be used solely for business purposes to qualify.

Here’s what you need to know:

- Exclusive Use: The area must be used exclusively for business; you can’t use the space for personal activities.

- Regular Use: You must use the space regularly as your principal place of business.

- Calculation Methods: You can use the simplified method (up to $5 per square foot, with a maximum of 300 square feet) or the regular method (calculating actual expenses).

- Eligible Expenses: Deductible expenses include mortgage interest, rent, utilities, insurance, and depreciation.

Taking the home office deduction can significantly reduce your taxable income. Income-partners.net provides resources to help you determine if you qualify and how to calculate your deduction accurately.

6. Deducting Business Expenses to Lower 1099 Tax

What business expenses can you deduct to lower your 1099 tax liability? Deducting eligible business expenses is a fundamental way to reduce your taxable income as a 1099 contractor. Let’s explore the types of expenses you can deduct.

Many business expenses are deductible for 1099 contractors, including costs for supplies, software, travel, marketing, and professional development. Keeping detailed records of these expenses is essential for maximizing your deductions and reducing your tax liability.

Here’s a more detailed look:

- Supplies: You can deduct the cost of office supplies, software, and other materials necessary for your business.

- Travel Expenses: Deductible travel expenses include transportation, lodging, and meals related to business trips.

- Marketing Expenses: Costs associated with advertising, website maintenance, and promotional materials are deductible.

- Professional Development: You can deduct expenses for courses, seminars, and other forms of professional development that enhance your skills.

- Other Expenses: Deductible expenses may also include legal and professional fees, insurance, and bank charges.

Properly documenting and claiming these expenses can lead to significant tax savings. Income-partners.net offers resources and tools to help you track and categorize your business expenses effectively, ensuring you don’t miss out on valuable deductions.

7. Health Insurance Deductions for Self-Employed Individuals

How can self-employed individuals deduct health insurance premiums? Self-employed individuals can often deduct the amount they paid in health insurance premiums, which can substantially lower their adjusted gross income (AGI). Let’s explore the specifics of this deduction.

Self-employed individuals can deduct the amount they paid in health insurance premiums for themselves, their spouse, and their dependents. This deduction is taken on Form 1040 and can significantly reduce your adjusted gross income (AGI), potentially lowering your overall tax liability.

Here’s what you need to know:

- Eligibility: You can deduct the premiums if you are self-employed and not eligible to participate in an employer-sponsored health plan.

- Deduction Limit: You can deduct the amount you paid in premiums up to your net profit from self-employment.

- Long-Term Care Insurance: In some cases, you may also be able to deduct premiums for long-term care insurance.

- Form 1040: The deduction is taken on line 16 of Schedule 1 (Form 1040), Additional Income and Adjustments to Income.

Taking this deduction can provide substantial tax relief. Income-partners.net offers resources and tools to help you understand the eligibility requirements and properly claim this deduction, ensuring you maximize your tax savings.

8. Retirement Contributions to Reduce 1099 Taxes

Can retirement contributions help reduce your 1099 taxes? Contributing to retirement accounts like SEP IRAs or solo 401(k)s is an excellent way to reduce your taxable income and save for the future. Let’s explore how these contributions can benefit you.

Contributions to retirement accounts like SEP IRAs or solo 401(k)s are deductible for self-employed individuals. These contributions not only help you save for retirement but also reduce your taxable income, potentially lowering your overall tax liability.

Here’s a more detailed look:

- SEP IRA: A Simplified Employee Pension (SEP) IRA allows you to contribute up to 20% of your net self-employment income, with a maximum contribution limit that changes annually.

- Solo 401(k): A solo 401(k) allows you to contribute both as an employee and as an employer, potentially allowing for higher contributions.

- Deduction Limit: The amount you can deduct is limited by the contribution limits for the respective retirement account.

- Tax Benefits: Contributions are tax-deductible, reducing your taxable income for the year.

Making contributions to these retirement accounts can provide significant tax benefits while helping you secure your financial future. Income-partners.net offers resources and tools to help you understand the different retirement options and maximize your contributions.

9. Strategies for Deferring 1099 Income

What strategies can you use to defer 1099 income and manage your tax liability? Deferring income can be a valuable strategy for managing your tax liability, especially if you anticipate changes in your income or tax situation. Let’s explore some effective techniques.

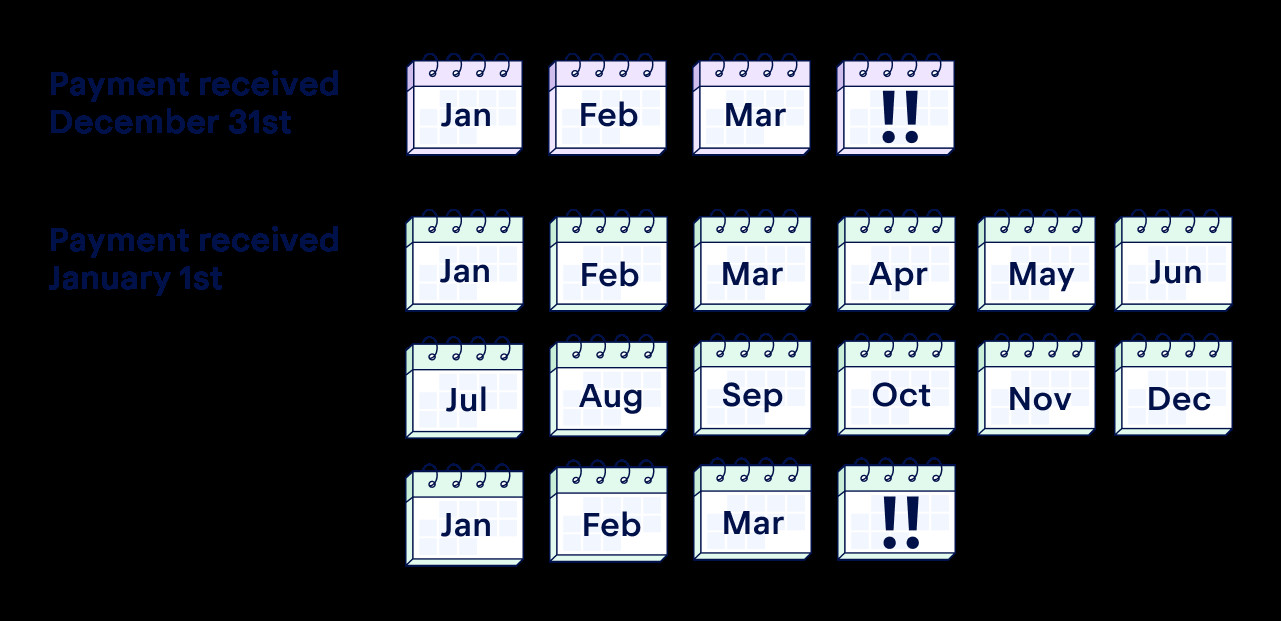

Deferring income involves delaying the receipt of income to a later tax year. This can be a useful strategy if you expect to be in a lower tax bracket in the future or if you want to postpone paying taxes on the income. For example, if your business rent is due January 5, pay it December 30. This will allow you to claim more deductions in the current tax year— essentially borrowing from next year’s write-offs.

Here are some ways to defer income:

- Delay Invoicing: If you invoice clients, consider delaying your December invoicing until the New Year. A payment you receive on December 31st has to be reported on your tax return by the following April. However, a payment you get on January 1st doesn’t have to be reported until April of the following year.

- Prepay Expenses: Rather than waiting until January to pay your regularly scheduled bills, pay them in December instead.

- Planning Ahead: Look ahead to anticipate changes in your income or tax situation and plan accordingly.

Deferring income can provide you with greater flexibility in managing your tax obligations. Income-partners.net offers resources and tools to help you evaluate the potential benefits of deferring income and implement these strategies effectively.

10. Prepaying Work Expenses to Reduce 1099 Tax

How does prepaying work expenses help reduce your 1099 tax? Prepaying work expenses can be a strategic way to lower your taxable income and manage your tax liability effectively. Let’s explore this strategy in detail.

Prepaying work expenses involves paying for business-related expenses before the end of the tax year, which allows you to deduct these expenses in the current year. This can be particularly beneficial if you anticipate a higher tax liability and want to reduce your taxable income.

Here are some scenarios where prepaying could be a beneficial move and help you save money overall:

- You owe a sizable tax bill and haven’t made any estimated payments. In this situation, reducing your tax liability by prepaying expenses is a good idea. The lower your tax liability, the less you’ll pay in underpayment penalties and interest.

- You don’t expect to have much — or any — self-employment income next year. People change jobs and hop careers all the time. If you expect a major change to the type of income you’re earning, it’s probably worthwhile to maximize your write-offs now.

- You expect to have more tax-saving opportunities next year. So for example, if you plan to enroll in college, you’ll have a sizable tax credit to play with. In that case, borrowing from next year’s write-offs probably won’t hurt you.

Here’s how to implement this strategy:

- Identify Eligible Expenses: Determine which business expenses can be prepaid, such as rent, subscriptions, and supplies.

- Make Payments Before Year-End: Ensure you make the payments before December 31 to claim the deduction in the current tax year.

- Keep Detailed Records: Maintain thorough records of all prepaid expenses for tax purposes.

By strategically prepaying expenses, you can effectively manage your tax liability. Income-partners.net offers resources and tools to help you identify and prepay eligible expenses, ensuring you maximize your tax savings.

11. Understanding 1099 Tax Forms: NEC, K, MISC, and B

What are the different types of 1099 tax forms and how do they affect your tax obligations? Understanding the various 1099 tax forms is crucial for accurately reporting your income and fulfilling your tax obligations. Let’s explore these forms in detail.

There are several types of 1099 forms used to report different kinds of income. The most common ones include 1099-NEC, 1099-K, 1099-MISC, and 1099-B. Knowing which form applies to your income is essential for accurate tax reporting.

Here’s a breakdown of each form:

- 1099-NEC (Nonemployee Compensation): This form reports payments made to independent contractors for services rendered. If you earned $600 or more from a client as a contractor, you should receive a 1099-NEC.

- 1099-K (Payment Card and Third-Party Network Transactions): This form reports payments received through third-party networks like PayPal, Venmo, and credit card transactions. For the 2024 tax year, individuals who received $5,000 or more on one of these platforms will receive a 1099-K.

- 1099-MISC (Miscellaneous Income): Although primarily replaced by the 1099-NEC for reporting independent contractor payments, the 1099-MISC is still used for reporting other types of miscellaneous income, such as rents, royalties, and prizes.

- 1099-B (Proceeds from Broker and Barter Exchange Transactions): This form reports proceeds from broker and barter exchange transactions, including the sale of stocks, bonds, and other securities.

Understanding these forms and their specific purposes is essential for accurate tax reporting. Income-partners.net provides resources and tools to help you identify the correct forms and properly report your income, ensuring you comply with IRS regulations.

12. What Triggers a 1099 Tax Audit?

What factors might trigger a 1099 tax audit and how can you prepare for one? Knowing what can trigger a tax audit and being prepared can help you navigate the process with confidence. Let’s explore the common triggers and preparation strategies.

An audit is an IRS review of your financial records to ensure your tax return is accurate. Audits can be random or triggered by certain red flags on your return. While less than 1% of U.S. tax returns are audited, it’s essential to understand what can trigger an audit and how to prepare.

Here are some common triggers:

- High Income: Higher income levels often increase the likelihood of an audit.

- Discrepancies: Inconsistencies between your reported income and information reported by third parties (e.g., 1099 forms) can trigger an audit.

- Large Deductions: Claiming unusually large deductions relative to your income can raise red flags.

- Errors: Simple errors on your tax return can lead to further scrutiny.

Here’s how to prepare for an audit:

- Keep Detailed Records: Maintain thorough records of all income, expenses, and deductions.

- Review Your Return: Carefully review your tax return for errors before filing.

- Seek Professional Advice: Consult with a tax professional if you have complex tax situations.

Knowing what can trigger an audit and being well-prepared can help you navigate the process with confidence. Income-partners.net offers resources and tools to help you maintain accurate records and prepare for potential audits, ensuring you are well-equipped to handle any IRS inquiries.

13. Understanding FICA Tax and Self-Employment

How does FICA tax apply to self-employed individuals, and what do you need to know? Understanding FICA tax is crucial for self-employed individuals, as they are responsible for paying both the employer and employee portions. Let’s explore this aspect in detail.

FICA, which stands for the Federal Insurance Contributions Act, is a tax that funds Social Security and Medicare. While W-2 employees have FICA taxes automatically deducted from their paychecks, self-employed individuals are responsible for paying the entire amount themselves.

Here’s what you need to know:

- Components of FICA: FICA tax consists of two parts: Social Security and Medicare.

- Tax Rate: The combined rate for Social Security and Medicare is 15.3% (12.4% for Social Security and 2.9% for Medicare).

- Self-Employment Tax: Self-employed individuals pay self-employment tax, which covers their FICA obligations.

- Deductibility: You can deduct one-half of your self-employment tax from your gross income.

Understanding how FICA tax applies to self-employed individuals is essential for accurate financial planning. Income-partners.net provides resources and tools to help you calculate and manage your FICA tax obligations effectively.

14. What Is Considered an “Ordinary and Necessary” Business Expense?

How does the IRS define “ordinary and necessary” business expenses, and why is it important for 1099 tax deductions? Understanding the IRS definition of “ordinary and necessary” business expenses is crucial for claiming valid tax deductions and avoiding potential issues. Let’s explore this concept in detail.

The IRS allows you to deduct business expenses that are considered “ordinary and necessary.” An ordinary expense is one that is common and accepted in your industry, while a necessary expense is one that is helpful and appropriate for your business.

Here’s what you need to know:

- Ordinary Expense: An expense that is common and accepted in your trade or business.

- Necessary Expense: An expense that is helpful and appropriate for your trade or business.

- Examples: Common examples include office supplies, business travel, marketing expenses, and professional development.

- Documentation: You must be able to substantiate your expenses with proper documentation, such as receipts and invoices.

Understanding this definition is essential for claiming valid tax deductions. Income-partners.net offers resources and tools to help you determine whether your expenses qualify as “ordinary and necessary” and maintain proper documentation.

15. Quarterly Taxes: A Must for 1099 Income Earners

Why are quarterly tax payments essential for 1099 income earners, and how do you manage them effectively? Quarterly tax payments are a critical requirement for 1099 income earners to avoid penalties and maintain compliance with IRS regulations. Let’s explore the importance of quarterly taxes and how to manage them effectively.

Quarterly taxes are estimated tax payments that many self-employed individuals must make at regular intervals throughout the year. These payments cover both income tax and self-employment tax and are essential for avoiding penalties for underpayment.

Here’s what you need to know:

- Payment Deadlines: Quarterly tax payments are due on April 15, June 15, September 15, and January 15 of the next year.

- Estimating Income: You must estimate your income and calculate your tax liability for each quarter.

- Payment Methods: You can pay quarterly taxes online, by mail, or through the Electronic Federal Tax Payment System (EFTPS).

- Avoiding Penalties: To avoid penalties, ensure you pay at least 90% of your tax liability for the current year or 100% of the tax shown on your return for the prior year.

Managing quarterly taxes effectively requires careful planning and accurate income estimation. Income-partners.net provides resources and tools to help you estimate your quarterly tax payments, track your income and expenses, and stay compliant with IRS regulations.

16. Schedule C: Reporting Profit or Loss from Business

What is Schedule C, and how do you use it to report profit or loss from your business as a 1099 income earner? Schedule C is a crucial form for reporting self-employment income and expenses, and understanding how to use it is essential for accurate tax filing. Let’s explore Schedule C in detail.

Schedule C (Form 1040), Profit or Loss From Business (Sole Proprietorship), is used to report the income and expenses from your business as a sole proprietor. This form is used to calculate your net profit or loss, which is then transferred to your individual income tax return (Form 1040).

Here’s what you need to know:

- Purpose: To report income and expenses from your business.

- Structure: The form includes sections for reporting income, expenses, and calculating net profit or loss.

- Key Sections: Income (Part I), Expenses (Part II), and Net Profit or Loss (Part IV).

- Filing Requirement: You must file Schedule C if you operate a business as a sole proprietor or single-member LLC.

Accurately completing Schedule C is essential for reporting your business income and expenses. Income-partners.net provides resources and tools to help you understand and complete Schedule C correctly, ensuring you accurately report your business activities.

17. Schedule SE: Calculating Self-Employment Tax

What is Schedule SE, and how do you use it to calculate your self-employment tax? Schedule SE is a critical form for calculating the amount of self-employment tax you owe, and understanding how to use it is essential for accurate tax filing. Let’s explore Schedule SE in detail.

Schedule SE (Form 1040), Self-Employment Tax, is used to calculate the amount of self-employment tax you owe. This tax covers your Social Security and Medicare obligations as a self-employed individual.

Here’s what you need to know:

- Purpose: To calculate self-employment tax.

- Structure: The form includes sections for calculating your self-employment income and determining the amount of tax you owe.

- Key Sections: Net Profit or Loss (Part I) and Calculation of Self-Employment Tax (Part II).

- Filing Requirement: You must file Schedule SE if your net earnings from self-employment are $400 or more.

Accurately completing Schedule SE is essential for calculating your self-employment tax. Income-partners.net provides resources and tools to help you understand and complete Schedule SE correctly, ensuring you accurately calculate your tax obligations.

18. Self-Employment Tax: What It Is and How to Pay It

What exactly is self-employment tax, and how do you pay it as a 1099 income earner? Understanding self-employment tax is crucial for 1099 income earners, as it covers their Social Security and Medicare obligations. Let’s explore this tax in detail.

Self-employment tax is the tax you pay as a self-employed individual to cover your Social Security and Medicare obligations. Unlike W-2 employees, who have these taxes withheld from their paychecks, self-employed individuals are responsible for paying the entire amount themselves.

Here’s what you need to know:

- Components of Self-Employment Tax: Self-employment tax consists of Social Security and Medicare taxes.

- Tax Rate: The combined rate for Social Security and Medicare is 15.3% (12.4% for Social Security and 2.9% for Medicare).

- Calculation: You calculate self-employment tax on IRS Schedule SE.

- Payment Methods: You can pay self-employment tax through estimated quarterly payments or when you file your annual tax return.

Understanding self-employment tax and how to pay it is essential for compliance with IRS regulations. Income-partners.net provides resources and tools to help you calculate your self-employment tax and manage your payments effectively.

19. Managing a Side Hustle: Tax Implications

What are the tax implications of managing a side hustle while holding a W-2 job? Managing a side hustle can provide additional income, but it also comes with specific tax considerations. Let’s explore the tax implications of side hustles.

A side hustle is any additional income-generating activity you pursue alongside your primary W-2 job. While it can boost your income, it also means you’ll have additional tax responsibilities.

Here’s what you need to know:

- Reporting Income: You must report all income from your side hustle on your tax return.

- Self-Employment Tax: Income from your side hustle is subject to self-employment tax.

- Deductible Expenses: You can deduct business expenses related to your side hustle to lower your taxable income.

- Estimated Taxes: You may need to pay estimated taxes quarterly to avoid penalties for underpayment.

Managing a side hustle effectively involves careful tax planning and accurate record-keeping. Income-partners.net provides resources and tools to help you navigate the tax implications of your side hustle, ensuring you stay compliant and maximize your income.

20. What Is a Sole Proprietor?

What does it mean to operate as a sole proprietor, and how does it affect your 1099 tax obligations? Understanding the concept of a sole proprietorship is essential for many 1099 income earners, as it’s the most common business structure. Let’s explore sole proprietorships in detail.

A sole proprietor is an individual who owns and runs a business alone, without any formal legal structure. As a sole proprietor, you are personally responsible for all business debts and liabilities.

Here’s what you need to know:

- Definition: A business owned and run by one person, with no legal distinction between the owner and the business.

- Liability: The owner is personally liable for all business debts and obligations.

- Taxation: Income from the business is reported on the owner’s individual income tax return (Form 1040) using Schedule C.

- Simplicity: It’s the simplest form of business to establish and maintain.

Operating as a sole proprietor has specific tax implications that you need to understand. Income-partners.net provides resources and tools to help you manage your tax obligations as a sole proprietor effectively.

21. Tax Deductions vs. Tax Credits: What’s the Difference?

What is the difference between tax deductions and tax credits, and how do they impact your 1099 tax liability? Understanding the difference between tax deductions and tax credits is crucial for maximizing your tax savings. Let’s explore these concepts in detail.

Tax deductions and tax credits are both tax incentives, but they work differently. A tax deduction reduces your taxable income, while a tax credit directly reduces the amount of tax you owe.

Here’s what you need to know:

- Tax Deduction: An expense you can subtract from your taxable income, lowering the amount of income subject to tax.

- Tax Credit: A tax incentive that directly lowers the amount of tax you owe.

- Impact: Tax deductions reduce your taxable income, while tax credits reduce your tax liability.

- Examples: Common tax deductions include business expenses and retirement contributions, while common tax credits include the child tax credit and the earned income tax credit.

Understanding the difference between tax deductions and tax credits can help you make informed decisions to maximize your tax savings. Income-partners.net offers resources and tools to help you identify and claim eligible deductions and credits, ensuring you optimize your tax strategy.

22. Understanding Tax Rates for 1099 Income

How do tax rates affect your 1099 income, and what do you need to know to plan effectively? Understanding tax rates is crucial for 1099 income earners to plan their finances effectively and estimate their tax liability accurately. Let’s explore tax rates in detail.

A tax rate is the percentage at which an individual or business’s income is taxed. Tax rates can be progressive, regressive, or proportional, depending on the tax system.

Here’s what you need to know:

- Progressive Tax Rate: The tax rate increases as income increases.

- Regressive Tax Rate: Everyone pays the same dollar amount, regardless of income.

- Proportional Tax Rate: Everyone is assessed the same tax rate, regardless of income.

- Marginal Tax Rate: The tax rate you pay on the next dollar of income you earn.

Understanding these tax rates and how they apply to your income is essential for effective tax planning. Income-partners.net provides resources and tools to help you understand tax rates and estimate your tax liability, ensuring you are well-prepared for tax season.

23. W-2 vs. 1099: Key Differences

What are the key differences between being a W-2 employee and a 1099 contractor, particularly regarding taxes? Understanding the key differences between W-2 and 1099 status is crucial for managing your tax obligations effectively. Let’s explore these differences in detail.

The main differences between being a W-2 employee and a 1099 contractor lie in how you’re treated for tax purposes and the benefits you receive. W-2 employees have taxes withheld from their paychecks and receive benefits like health insurance and retirement plans. 1099 contractors are responsible for paying their own taxes and typically don’t receive employer-sponsored benefits.

Here’s a comparison:

| Feature | W-2 Employee | 1099 Contractor |

|---|---|---|

| Tax Withholding | Taxes are withheld from paycheck | Responsible for paying own taxes |

| Benefits | Receives employer-sponsored benefits | Typically no employer-sponsored benefits |

| Tax Forms | Receives a W-2 form | Receives a 1099 form |

| FICA Taxes | Employer and employee share FICA taxes | Pays entire self-employment tax |

| Business Expenses | Limited deductions | Can deduct business expenses |

| Control | Employer controls work | More control over work |

| Job Security | More job security | Less job security |

Understanding these differences can help you make informed decisions about your employment status and manage your tax obligations effectively. Income-partners.net provides resources and tools to help you navigate the complexities of both W-2 and 1099 income.

24. Understanding the W-4 Form

What is a W-4 form, and how does it impact your tax withholding as an employee with additional 1099 income? Understanding the W-4 form is crucial for employees with additional 1099 income to ensure they have the correct amount of tax withheld. Let’s explore the W-4 form in detail.

The W-4 form, Employee’s Withholding Certificate, is used by employees to inform their employer how much tax to withhold from their paychecks. If you have both W-2 income and 1099 income, it’s essential to adjust your W-4 to account for the additional income and avoid underpayment penalties.

Here’s what you need to know:

- Purpose: To inform your employer how much tax to withhold from your paycheck.

- Adjustments: You can make adjustments to account for deductions, credits, and additional income.

- Multiple Jobs: If you have multiple jobs or sources of income, you should complete a W-4 for each job.

- Accuracy: It’s essential to complete the W-4 accurately to avoid underpayment penalties.

Completing the W-4 accurately is crucial for managing your tax obligations effectively. Income-partners.net provides resources and tools to help you understand and complete the W-4 form correctly, ensuring you have the appropriate amount of tax withheld.

25. Need Help with 1099 Taxes?

Where can you find reliable assistance and resources to help you navigate the complexities of 1099 taxes? Navigating 1099 taxes can be complex, but numerous resources are available to help you manage your tax obligations effectively. Let’s explore these resources in detail.

Managing 1099 taxes can be challenging, but numerous resources are available to help you navigate the complexities. These resources range from online tools and software to professional tax advisors.

Here are some helpful resources:

- IRS Website: The IRS provides a wealth of information, forms, and publications to help you understand your tax obligations.

- Tax Software: Tax software like TurboTax and H&R Block can help you prepare and file your tax return.

- Tax Professionals: Consulting with a tax professional can provide personalized advice and guidance.

- Online Resources: Websites like income-partners.net offer resources, tools, and articles to help you manage your 1099 taxes.

Leveraging these resources can help you manage your 1099 taxes effectively and ensure you comply with IRS regulations. Income-partners.net offers comprehensive resources and tools to support you in your tax journey.

Navigating the complexities of 1099 income and self-employment tax can be challenging, but with the right knowledge and strategies, you can manage your tax obligations effectively and maximize your income potential.

Ready to take control of your 1099 taxes and explore partnership opportunities to boost your income? Visit income-partners.net today to discover valuable resources, tools, and expert guidance to help you succeed. Don’t miss out on the chance to connect with potential partners and unlock your financial success!

FAQ: How Much Tax on 1099 Income

1. What is 1099 income?

1099 income is the money you earn as