Calculating your federal income tax manually might seem daunting, but it’s a manageable process that empowers you to understand where your money goes. At income-partners.net, we believe in equipping you with the knowledge and resources to navigate the financial landscape confidently, potentially opening doors to strategic partnerships and increased income. Learning these calculations offers valuable insights into your tax obligations and helps you verify the accuracy of your paycheck withholdings. Let’s explore the steps involved in calculating your federal income tax, focusing on accuracy, compliance, and potential collaborative financial strategies.

1. What is Federal Income Tax and Why Calculate it Manually?

Federal income tax is a tax levied by the U.S. government on the taxable income of individuals, corporations, estates, and trusts. Calculating it manually helps you understand your tax obligations and verify your paycheck withholdings. It ensures transparency and empowers you to manage your finances effectively.

Understanding federal income tax involves knowing that it funds various government programs, including national defense, infrastructure, social security, and Medicare. According to the IRS, federal income tax accounts for a significant portion of the U.S. government’s revenue. Knowing how this tax is calculated helps individuals and businesses plan their finances, optimize deductions, and ensure compliance with tax laws. Manually calculating federal income tax can reveal potential errors in your paycheck withholdings or tax estimates, allowing you to adjust your W-4 form or estimated tax payments to avoid underpayment penalties or overpayment refunds.

2. What Are The Necessary Components For Calculating Federal Income Tax Manually?

To calculate your federal income tax manually, you’ll need your paycheck stub, Form W-4, and IRS Publication 15-T. These tools provide essential information, including gross pay, filing status, withholding allowances, and tax rates.

- Paycheck Stub: Provides details of your gross pay, deductions, and year-to-date earnings. This is crucial for determining your taxable income for each pay period.

- Form W-4: Employee’s Withholding Certificate, which you complete when starting a new job or when you want to change your withholding. It indicates your filing status, number of dependents, and any additional withholding.

- IRS Publication 15-T: Contains the percentage method tables needed to calculate federal income tax based on your wages and withholding information. It also provides guidance on various aspects of payroll tax withholding.

- Calculator: A basic calculator is necessary to perform the arithmetic operations involved in the calculation, ensuring accuracy.

- Tax Records: Keep your previous tax returns and any documentation related to income or deductions to refer to them if needed.

3. What Are The Step-By-Step Instructions to Calculate Federal Income Tax Manually?

Calculating federal income tax manually involves several steps, from determining your gross pay to applying the correct tax rates and credits. Follow these steps carefully to ensure accuracy.

- Determine Gross Pay: Find your gross pay (total earnings before any deductions) on your paycheck stub.

- Calculate Payroll Periods: Determine the number of payroll periods in a year based on your pay frequency (e.g., weekly = 52, bi-weekly = 26, monthly = 12).

- Annual Wage Calculation: Multiply your gross pay by the number of payroll periods to calculate your total annual wage.

- Additional Income: Add any additional income not from jobs (e.g., dividends, retirement income) from Step 4(a) of Form W-4 to your annual wage.

- Additional Deductions: Note any additional deductions beyond the standard deduction from Step 4(b) of Form W-4.

- Step 2 Box Consideration: If the Step 2 box of Form W-4 is checked, this step is $0. If not checked, write down $13,850 for single filers or $27,700 if married filing jointly (2023 standard deduction). Note that these amounts are updated annually by the IRS.

- Adjusted Annual Wage: Add Step 5 and Step 6, then subtract this total from the wages in Step 4. This is the amount you’ll use for the Percentage Method Tables.

- IRS Publication 15-T: Refer to the tables on page 11 of IRS Publication 15-T to find the appropriate tax rates.

- Table Selection: Choose the correct table based on your filing status and whether the box in Step 2 on Form W-4 was checked.

- Taxable Income Range: Locate the range in the table that corresponds to your amount from Step 7. Work across that line from right to left to determine the tentative amount of federal income tax to withhold.

- Payroll Period Tax Amount: Divide the tax amount from Step 10 by the number of payroll periods from Step 2.

- Credit Application: Account for any credits from Step 3 of Form W-4 by dividing the credit amount by the number of payroll periods and subtracting it from the tax amount in Step 11.

- Additional Withholding: Add any additional withholding from Step 4(c) of Form W-4 to the tax amount.

4. What is an Example of Calculating Federal Income Tax Manually?

Let’s walk through an example to illustrate how to calculate federal income tax manually. This will help clarify the steps and provide a practical understanding.

Suppose John Smith is single and earns $2,000 bi-weekly. He claims $200 for dependents on his W-4 and has an additional withholding of $50 per paycheck.

- Gross Pay: $2,000

- Payroll Periods: Bi-weekly = 26

- Annual Wage: $2,000 x 26 = $52,000

- Additional Income: $0 + $52,000 = $52,000

- Additional Deductions: $0

- Standard Deduction (Single): $13,850 (for 2023)

- Adjusted Annual Wage: $52,000 – $13,850 = $38,150

- IRS Publication 15-T Table: Refer to the Single filer table in Publication 15-T.

- Taxable Income Range: Locate the range in the table that includes $38,150.

- Tax Calculation:

- $38,150 – $16,250 = $21,900

- $21,900 x 0.12 = $2,628

- $2,628 + $1,782 = $4,410

- Payroll Period Tax Amount: $4,410 ÷ 26 = $169.62

- Credit Application: $200 ÷ 26 = $7.69; $169.62 – $7.69 = $161.93

- Additional Withholding: $161.93 + $50 = $211.93

John’s federal withholding for this paycheck is $211.93.

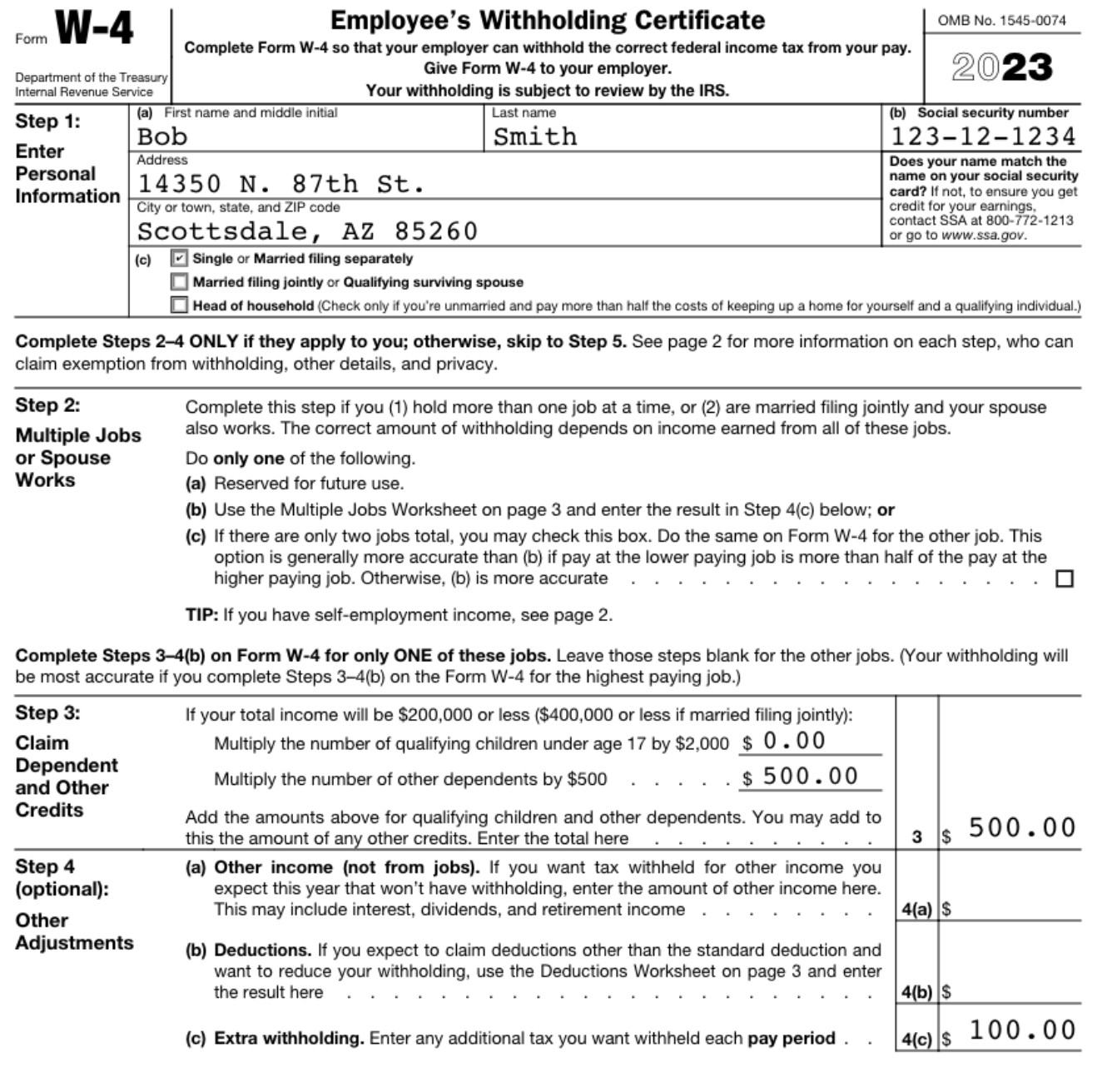

W-4 example where Bob Smith claims filing as single, 0 for dependents, and 0 withholding per paycheck.

W-4 example where Bob Smith claims filing as single, 0 for dependents, and 0 withholding per paycheck.

5. Why Is My Federal Withholding Sometimes $0?

Federal income tax withholding can be $0 if your gross pay and deductions result in an annual pay that is less than the standard deduction. The standard deduction is a fixed amount that the IRS deducts from your federal income tax each year.

The IRS updates the standard deduction annually to account for inflation. For 2023, the standard deductions are:

- Married filing jointly: $27,700

- Head-of-household: $20,800

- All other taxpayers: $13,850

If your annual income after deductions is below these thresholds, no federal income tax will be withheld.

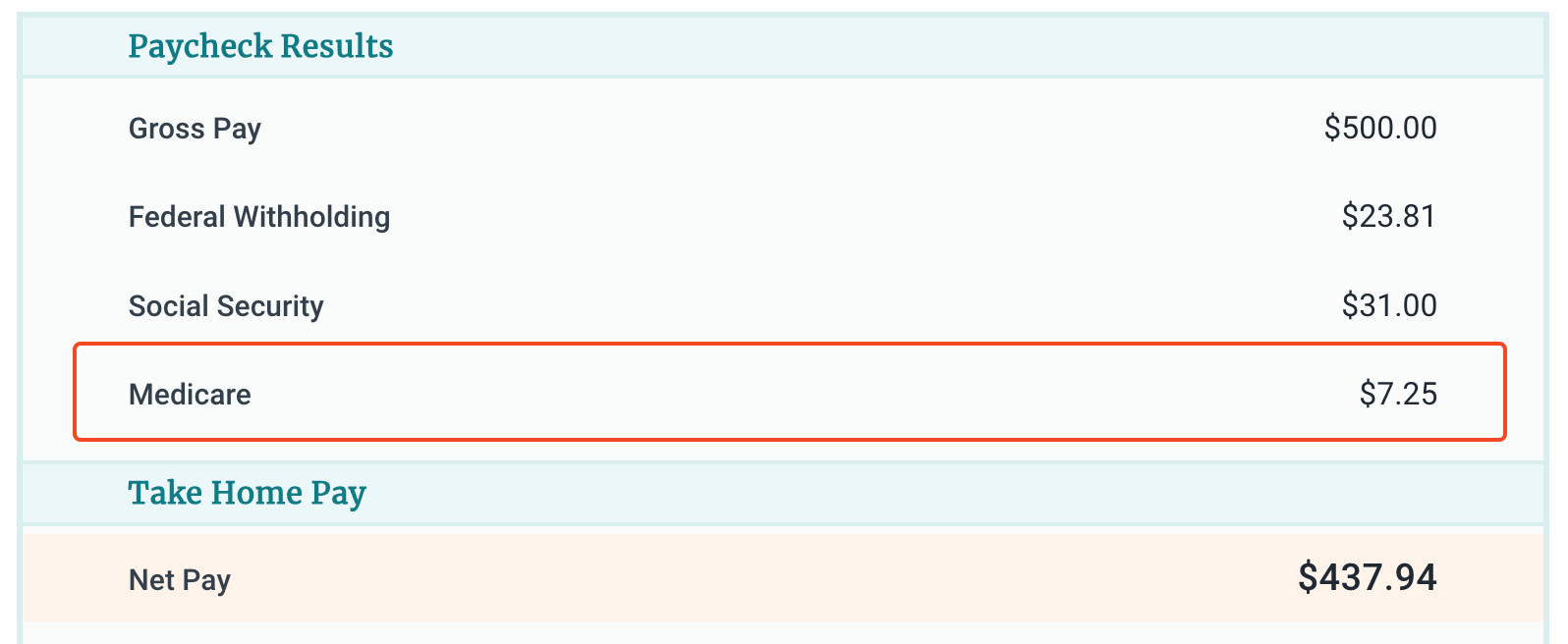

6. How Do I Calculate Medicare Tax Manually?

The Medicare tax rate is 1.45% for all employees. Calculating it manually is straightforward: simply multiply your paycheck’s gross pay by 0.0145.

Formula: Paycheck Gross Pay x 0.0145 = Medicare Tax

For example, if your paycheck’s gross pay is $1,000:

$1,000 x 0.0145 = $14.50

If your year-to-date income surpasses $200,000, you’re subject to the Additional Medicare Tax, which is an extra 0.9%. The calculation is: Paycheck Gross Pay x 0.0235.

PaycheckCity Salary Calculator results for Medicare tax if a paycheck

PaycheckCity Salary Calculator results for Medicare tax if a paycheck

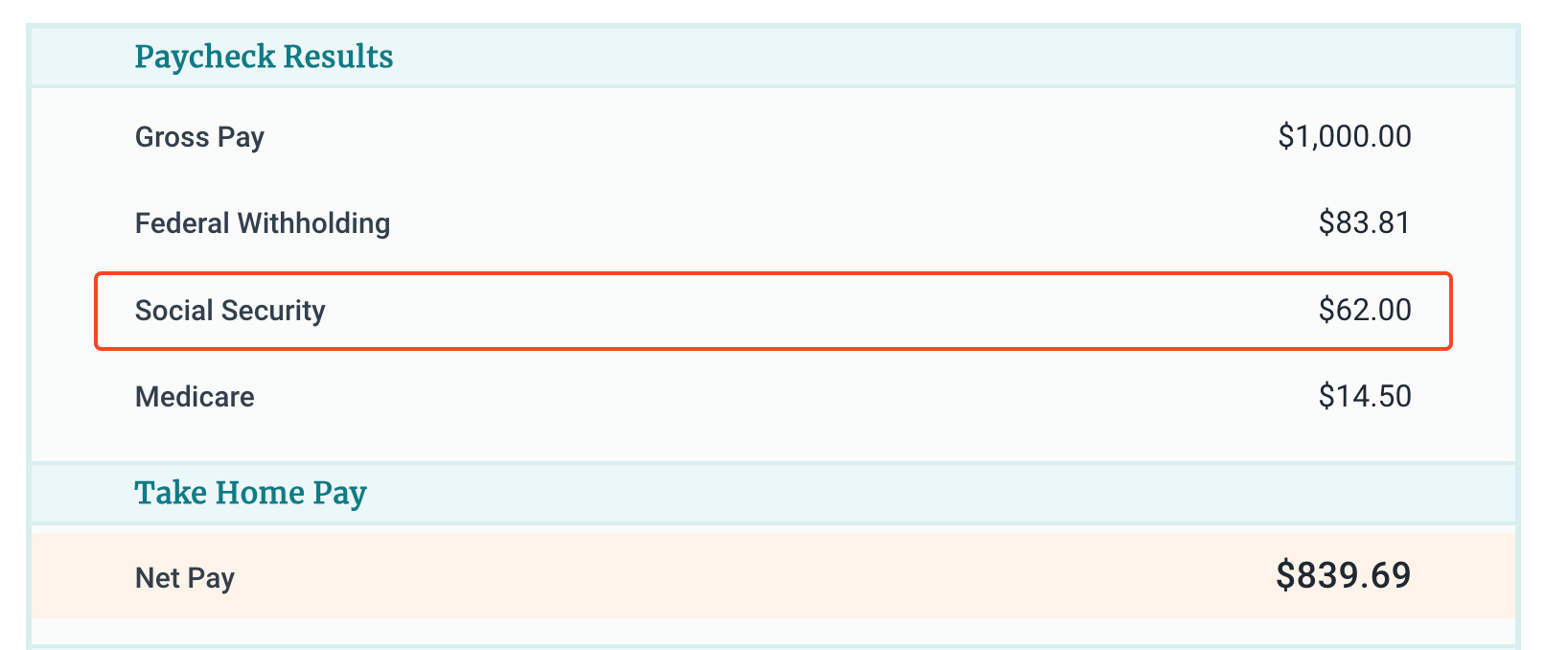

7. How Do I Calculate Social Security Tax Manually?

Social Security tax is 6.2% on up to $160,200 of earned income in 2023. To calculate your Social Security tax manually, multiply your paycheck’s gross pay by 0.062.

Formula: Paycheck Gross Pay x 0.062 = Social Security Tax

For example, if your paycheck’s gross pay is $1,000:

$1,000 x 0.062 = $62.00

The maximum Social Security tax for employees in 2023 is $9,932.40 per year.

PaycheckCity Salary Calculator results for Social Security tax if a paycheck

PaycheckCity Salary Calculator results for Social Security tax if a paycheck

8. What Are the Common Mistakes to Avoid When Calculating Federal Income Tax Manually?

Several common mistakes can occur when calculating federal income tax manually. Avoiding these pitfalls ensures accuracy and compliance.

- Incorrect Gross Pay: Using the wrong gross pay amount from your paycheck can skew the entire calculation. Always double-check this figure.

- Incorrect Payroll Periods: Miscalculating the number of payroll periods in a year can lead to significant errors. Ensure you know your pay frequency (weekly, bi-weekly, etc.).

- Outdated Standard Deductions: Using outdated standard deduction amounts will result in an incorrect taxable income. Always use the current year’s figures from the IRS.

- Incorrect Table Selection: Choosing the wrong table in IRS Publication 15-T based on your filing status and W-4 can lead to incorrect tax withholding.

- Forgetting Credits and Deductions: Failing to account for applicable tax credits and deductions can result in overpaying your taxes.

- Math Errors: Simple arithmetic mistakes can compound throughout the calculation. Use a calculator and double-check each step.

9. How Can Online Tools Simplify Federal Income Tax Calculations?

Online paycheck calculators can greatly simplify federal income tax calculations. These tools automate the process, reducing the risk of manual errors and providing accurate estimates.

Websites like PaycheckCity and the IRS Withholding Estimator offer user-friendly interfaces that guide you through the calculation process. These calculators consider various factors, including your income, filing status, deductions, and credits, to provide a comprehensive estimate of your federal income tax liability. Using these tools not only saves time but also helps ensure compliance with tax regulations. Additionally, these tools often offer insights into how different withholding choices can affect your take-home pay and tax refund.

10. What Are Key Tax Strategies for Individuals in Austin, Texas?

For individuals in Austin, Texas, understanding key tax strategies can help optimize their financial situation. Since Texas has no state income tax, residents focus primarily on federal tax planning.

- Maximize Retirement Contributions: Contributing to 401(k)s and IRAs can reduce taxable income while saving for retirement.

- Utilize Health Savings Accounts (HSAs): If you have a high-deductible health plan, an HSA allows you to save pre-tax dollars for healthcare expenses.

- Claim Eligible Deductions: Take advantage of deductions for mortgage interest, charitable donations, and other eligible expenses.

- Tax-Loss Harvesting: If you have investment losses, use them to offset capital gains and reduce your overall tax liability.

- Consult a Tax Professional: A local tax advisor can provide personalized guidance based on your specific financial situation and help you navigate complex tax laws.

By implementing these strategies, Austin residents can effectively manage their federal income tax and improve their financial well-being.

11. What Is The Significance of Form W-4 in Federal Income Tax Calculation?

Form W-4, the Employee’s Withholding Certificate, plays a crucial role in federal income tax calculation. It informs your employer how much federal income tax to withhold from your paycheck.

Completing Form W-4 accurately is essential because it directly affects your tax liability. The form allows you to indicate your filing status (single, married, head of household), claim dependents, and specify any additional withholding or deductions. The information you provide guides your employer in determining the correct amount of federal income tax to withhold. If you withhold too little, you may owe taxes and penalties at the end of the year. If you withhold too much, you’ll receive a refund, but you’ve essentially given the government an interest-free loan. Regularly reviewing and updating your W-4, especially after major life events like marriage, divorce, or the birth of a child, ensures that your withholding aligns with your tax obligations.

12. How Do Tax Credits Affect Federal Income Tax Liability?

Tax credits directly reduce your federal income tax liability, providing a dollar-for-dollar reduction in the amount of tax you owe. They are a valuable tool for lowering your tax burden.

Unlike tax deductions, which reduce your taxable income, tax credits offer a more significant benefit by directly decreasing the amount of tax you owe. For example, if you qualify for a $1,000 tax credit and you owe $5,000 in taxes, the credit reduces your tax bill to $4,000. Some tax credits are refundable, meaning that if the credit amount exceeds your tax liability, you’ll receive the difference as a refund. Common tax credits include the Child Tax Credit, Earned Income Tax Credit, and education credits like the American Opportunity Tax Credit and Lifetime Learning Credit. Understanding and claiming eligible tax credits can significantly lower your federal income tax liability and improve your overall financial situation.

13. What Are the Best Practices For Keeping Accurate Tax Records?

Maintaining accurate tax records is essential for simplifying the tax filing process and ensuring compliance with IRS regulations. Implementing best practices for record-keeping can save time and reduce the risk of errors.

- Organize Documents: Create a system for organizing your tax-related documents, such as receipts, invoices, and statements.

- Digital Storage: Scan and store digital copies of your documents using secure cloud storage or encrypted hard drives.

- Categorize Expenses: Track your income and expenses throughout the year, categorizing them for easy reference during tax filing.

- Use Accounting Software: Consider using accounting software or apps to automate record-keeping and generate reports.

- Backup Regularly: Regularly back up your digital records to prevent data loss from hardware failures or cyber threats.

- Retain Records: Keep your tax records for at least three years from the date you filed your return or two years from the date you paid the tax, whichever is later.

By following these best practices, you can maintain accurate and organized tax records, making tax preparation easier and more efficient.

14. How Does Filing Status Impact Federal Income Tax Calculation?

Your filing status significantly impacts your federal income tax calculation because it determines your tax bracket, standard deduction, and eligibility for certain tax credits and deductions.

The IRS recognizes five filing statuses: Single, Married Filing Jointly, Married Filing Separately, Head of Household, and Qualifying Widow(er). Each status has its own set of rules and criteria. For example, the standard deduction for married filing jointly is higher than for single filers, which can lower taxable income. Head of Household status is available to unmarried individuals who pay more than half the costs of keeping up a home for a qualifying child, and it offers a higher standard deduction than the single filing status. Your filing status also affects your eligibility for various tax credits and deductions, such as the Earned Income Tax Credit and Child Tax Credit. Choosing the correct filing status is crucial for accurately calculating your federal income tax liability and minimizing your tax burden.

15. What Resources Does Income-Partners.Net Offer to Help Navigate Federal Income Tax?

At income-partners.net, we offer a variety of resources to help you navigate the complexities of federal income tax and explore opportunities for financial partnership and growth.

We provide informative articles, guides, and tools that cover various aspects of federal income tax, including calculation methods, tax strategies, and compliance requirements. Our platform also connects you with experienced financial professionals and tax advisors who can provide personalized guidance and support. Additionally, income-partners.net offers insights into potential partnership opportunities that can help you increase your income and optimize your financial planning. We aim to empower you with the knowledge and resources you need to make informed financial decisions and achieve your financial goals.

Understanding how to calculate federal income tax manually is a valuable skill that empowers you to take control of your finances and verify the accuracy of your withholdings. By following the steps outlined in this guide and utilizing online tools and resources, you can navigate the complexities of federal income tax with confidence. For more insights into financial planning and partnership opportunities, visit income-partners.net. Explore our resources, connect with experts, and discover how strategic collaborations can enhance your financial success. We are located at 1 University Station, Austin, TX 78712, United States, and can be reached at +1 (512) 471-3434.

Remember, accurate tax planning and strategic partnerships are key to long-term financial growth.

FAQ: Calculating Federal Income Tax Manually

1. What if I have multiple jobs? How does that affect my federal income tax calculation?

Having multiple jobs can complicate your federal income tax calculation because each job withholds taxes as if it were your only source of income. This can result in underwithholding, especially if your combined income pushes you into a higher tax bracket. To address this, you can use the IRS’s Tax Withholding Estimator to determine the correct amount of withholding across all your jobs. You may also need to fill out Form W-4 for each job, indicating that you have multiple jobs.

2. Can I claim exemption from federal income tax withholding?

Yes, you can claim exemption from federal income tax withholding if you meet certain criteria. You must have had no tax liability for the previous year and expect to have no tax liability for the current year. This is typically applicable to individuals with very low income. To claim exemption, you need to complete Form W-4 and indicate that you are exempt. However, ensure you meet the eligibility requirements to avoid penalties.

3. How do I adjust my W-4 form if I want to change my withholding?

To adjust your W-4 form and change your withholding, obtain a new W-4 form from your employer or the IRS website. Fill out the form, providing accurate information about your filing status, dependents, and any additional withholding or deductions. Submit the completed form to your employer, who will then adjust your withholding accordingly. It’s a good practice to review and update your W-4 form annually or whenever you experience significant life changes.

4. What happens if I underpay my federal income tax?

If you underpay your federal income tax, you may be subject to penalties and interest charges. The penalty for underpayment is typically a percentage of the underpaid amount. To avoid this, ensure you withhold enough taxes from your paycheck or make estimated tax payments throughout the year. The IRS offers various payment options, including online, by mail, or through electronic funds withdrawal.

5. How do I calculate estimated taxes if I’m self-employed?

If you’re self-employed, you’re responsible for paying estimated taxes on your income throughout the year. To calculate estimated taxes, estimate your expected income for the year, calculate your self-employment tax (Social Security and Medicare), and estimate your income tax liability. Use Form 1040-ES to calculate and pay your estimated taxes quarterly. The IRS provides resources and worksheets to help you with this process.

6. Are there any specific deductions or credits for residents of Austin, Texas?

While Texas has no state income tax, residents of Austin can take advantage of federal tax deductions and credits, such as the home mortgage interest deduction, charitable contribution deduction, and credits for education expenses or energy-efficient home improvements. Consult a tax professional to identify the deductions and credits that are most applicable to your situation.

7. How does the Tax Cuts and Jobs Act of 2017 affect federal income tax calculations?

The Tax Cuts and Jobs Act of 2017 made significant changes to federal income tax, including lower tax rates, a higher standard deduction, and changes to various deductions and credits. These changes affect how federal income tax is calculated and can impact your tax liability. It’s important to stay informed about these changes and how they affect your tax situation.

8. What is the difference between a tax deduction and a tax credit?

A tax deduction reduces your taxable income, while a tax credit directly reduces the amount of tax you owe. Tax credits are generally more valuable because they provide a dollar-for-dollar reduction in your tax liability. Common tax deductions include the standard deduction, itemized deductions (such as mortgage interest and charitable contributions), and deductions for business expenses. Tax credits include the Child Tax Credit, Earned Income Tax Credit, and education credits.

9. How do I find reliable information about federal income tax laws and regulations?

Reliable sources of information about federal income tax laws and regulations include the IRS website, IRS publications, and reputable tax professionals. The IRS website provides comprehensive information about tax laws, forms, and publications. Tax professionals, such as CPAs and Enrolled Agents, can offer personalized guidance and help you navigate complex tax issues.

10. What should I do if I receive a notice from the IRS?

If you receive a notice from the IRS, review it carefully and respond promptly. The notice will typically explain the issue and provide instructions on how to resolve it. If you disagree with the notice or need assistance, contact the IRS or consult a tax professional. Ignoring the notice can lead to penalties and interest charges.