Age and income have a significant correlation, and understanding this relationship is crucial for making informed financial decisions and strategic partnerships, with income-partners.net being a resourceful tool. As individuals gain experience and expertise throughout their careers, their earning potential typically increases, although this isn’t always the case. By exploring the impact of age on income, individuals can better prepare for their financial futures and businesses can forge strategic partnerships to boost earning potential, leveraging resources like partner programs, affiliate marketing, and joint ventures.

1. What Is the Relationship Between Age and Income?

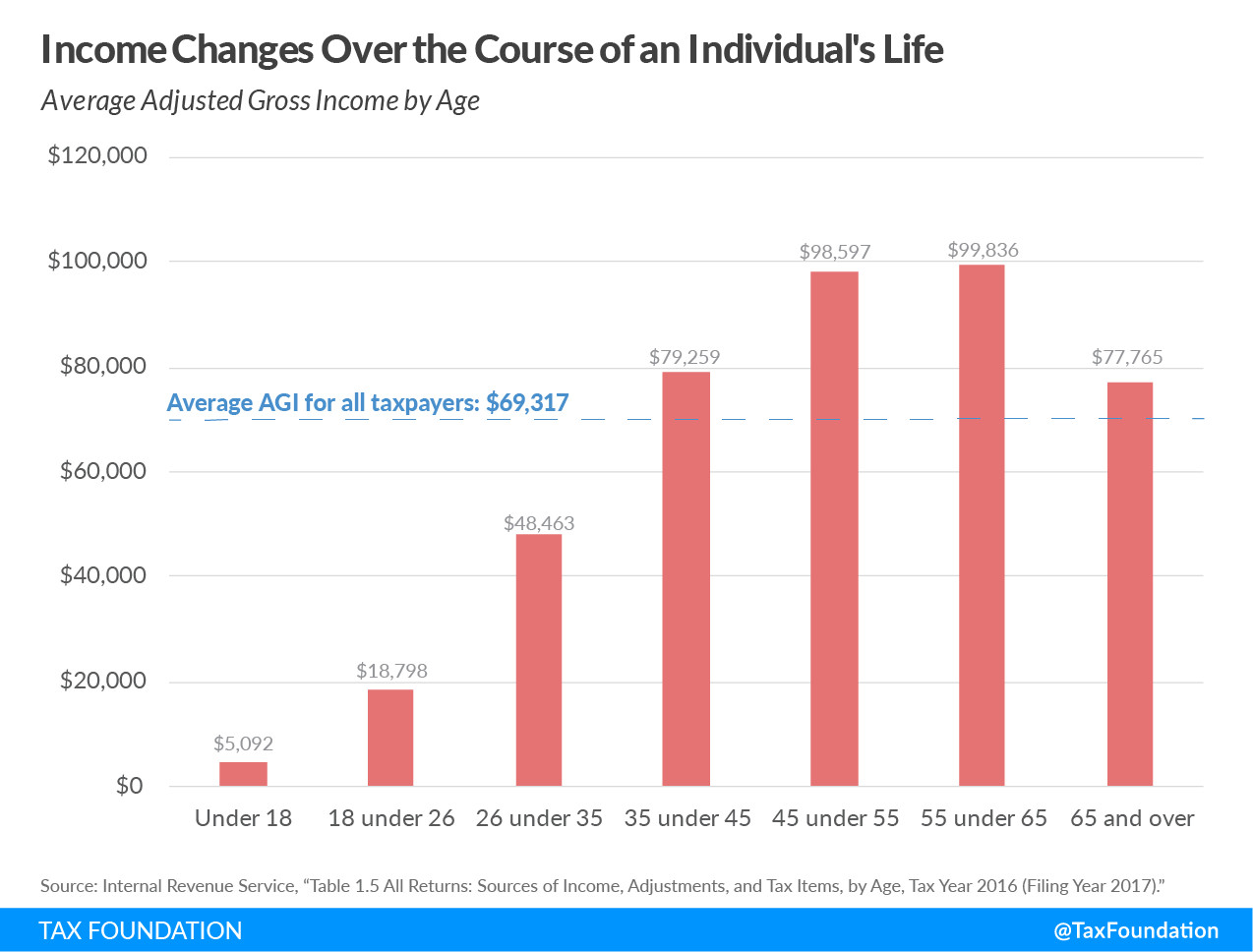

The relationship between age and income generally follows an inverted U-shaped curve, with income rising during the early and middle stages of a career and then gradually declining near retirement age. According to data from the Internal Revenue Service (IRS) and studies by institutions like the University of Texas at Austin’s McCombs School of Business, income tends to increase as individuals gain more work experience and expertise, often peaking in the years leading up to retirement. This pattern reflects the accumulation of skills, knowledge, and professional networks that contribute to higher earning potential. However, this is a general trend, and individual experiences can vary widely based on factors like education, occupation, industry, and economic conditions.

1.1. How Does Work Experience Influence Income at Different Ages?

Work experience is a primary driver of income growth as individuals progress through their careers. In their early career stages (25-35), increased work experience translates to improved skills, greater efficiency, and higher productivity, which employers often reward with promotions and salary increases. As individuals move into their mid-career (35-50), their accumulated experience and expertise enable them to take on more complex projects, assume leadership roles, and make strategic decisions that significantly impact their organizations’ performance, leading to further income growth. By late career (50-65), many professionals reach the peak of their earning potential, leveraging their extensive experience to command higher salaries, consulting fees, or business profits. However, continuous learning and adaptation are crucial to maintaining their value and relevance in a rapidly changing job market.

1.2. What Role Does Education Play in the Age-Income Relationship?

Education is a critical factor influencing the relationship between age and income. Higher levels of education often lead to greater earning potential and faster career advancement. Individuals with bachelor’s degrees, master’s degrees, or professional certifications typically have access to more job opportunities and higher-paying positions compared to those with lower levels of education. According to the U.S. Bureau of Labor Statistics, median weekly earnings are significantly higher for individuals with higher educational attainment. For example, in 2020, the median weekly earnings for those with a bachelor’s degree were $1,305, compared to $781 for those with only a high school diploma. Furthermore, education can enhance an individual’s ability to adapt to changing job market demands and acquire new skills, enabling them to remain competitive and continue growing their income throughout their career.

1.3. Are There Any Demographic Factors That Influence the Age-Income Dynamic?

Demographic factors such as gender, race, and ethnicity can significantly influence the age-income dynamic. Studies have consistently shown that women and underrepresented minority groups often face systemic barriers that limit their access to education, job opportunities, and promotions, resulting in lower earnings compared to their male and white counterparts. The gender pay gap, for example, persists across various industries and occupations, with women earning approximately 82 cents for every dollar earned by men, according to the U.S. Census Bureau. Similarly, racial and ethnic disparities in income are well-documented, with Black and Hispanic workers earning less than white and Asian workers, even with similar levels of education and experience. Addressing these demographic disparities requires comprehensive efforts to promote equal opportunity, eliminate discriminatory practices, and foster inclusive workplaces that value diversity.

2. How Does Income Fluctuate Across Different Age Groups?

Income levels vary significantly across different age groups, reflecting the different stages of career development and life priorities. Examining income fluctuations across age groups provides valuable insights into the economic well-being and financial challenges faced by individuals at different points in their lives.

2.1. What Is the Typical Income for Young Adults (Ages 25-34)?

Young adults (ages 25-34) are typically in the early stages of their careers, building their skills and gaining experience. Their income levels tend to be lower compared to older age groups, but they often experience rapid income growth as they advance in their professions. According to recent data from the U.S. Census Bureau, the median income for individuals in this age group is around $50,000 to $70,000 per year. This income level can vary significantly based on factors like education, occupation, and geographic location. Young adults often face financial challenges such as student loan debt, high housing costs, and the need to save for retirement, making it crucial for them to develop sound financial habits and explore opportunities for income growth. Joining income-partners.net can provide valuable resources and connections for young adults looking to enhance their earning potential through strategic partnerships.

2.2. How Much Do Middle-Aged Professionals (Ages 35-54) Earn on Average?

Middle-aged professionals (ages 35-54) are typically at the peak of their earning potential, having accumulated significant work experience and expertise. Their income levels tend to be higher compared to younger age groups, reflecting their increased responsibilities, leadership roles, and contributions to their organizations. The median income for individuals in this age group ranges from $70,000 to $120,000 per year. Middle-aged professionals often have greater financial stability and may be focused on saving for retirement, funding their children’s education, and investing in their future. This stage of life also presents opportunities for entrepreneurship and business partnerships, allowing individuals to leverage their skills and networks to generate additional income.

2.3. What Income Can Be Expected Near Retirement Age (Ages 55-64)?

Individuals approaching retirement age (ages 55-64) typically have high earning potential, although their income may begin to stabilize or gradually decline as they transition towards retirement. The median income for this age group ranges from $60,000 to $100,000 per year. Many individuals in this age group have reached the peak of their careers and are focused on maximizing their retirement savings, managing their investments, and planning for their future financial security. Some may choose to work part-time or pursue encore careers to supplement their retirement income and stay active. This stage of life also presents opportunities for mentoring younger professionals and sharing their expertise through consulting or advisory roles.

Income changes over the course of an individual

Income changes over the course of an individual

Income changes over the course of an individual and the typical inverted-U-shape pattern.

3. How Can Strategic Partnerships Mitigate the Impact of Age on Income?

Strategic partnerships can be a powerful tool for mitigating the impact of age on income and maximizing earning potential at any stage of a career. By collaborating with others, individuals can leverage complementary skills, resources, and networks to achieve greater success than they could on their own.

3.1. What Types of Partnerships Are Beneficial for Young Professionals?

For young professionals, strategic partnerships can provide valuable learning opportunities, mentorship, and access to new markets and networks. Some beneficial types of partnerships include:

- Mentorship Programs: Pairing with experienced professionals who can provide guidance, advice, and support.

- Networking Groups: Joining industry-specific or professional networking groups to connect with peers, potential employers, and collaborators.

- Skill-Sharing Communities: Participating in communities where individuals can share their expertise and learn from others.

- Startup Incubators and Accelerators: Joining programs that provide resources, mentorship, and funding opportunities for aspiring entrepreneurs.

- Joint Ventures: Collaborating with other young professionals to launch new products, services, or businesses.

These partnerships can help young professionals accelerate their career growth, expand their professional networks, and increase their earning potential.

3.2. How Can Mid-Career Professionals Leverage Partnerships for Income Growth?

Mid-career professionals can leverage strategic partnerships to expand their businesses, enter new markets, and generate additional revenue streams. Some effective partnership strategies include:

- Strategic Alliances: Forming alliances with complementary businesses to offer bundled products or services.

- Joint Marketing Campaigns: Collaborating with other companies to promote each other’s products or services to a wider audience.

- Referral Partnerships: Establishing referral agreements with other businesses to generate leads and sales.

- Affiliate Marketing Programs: Partnering with influencers or bloggers to promote products or services and earn commissions on sales.

- Co-Branding Initiatives: Collaborating with other brands to create co-branded products or services that appeal to a broader customer base.

These partnerships can help mid-career professionals diversify their income sources, increase their brand awareness, and achieve greater business success.

3.3. What Partnership Opportunities Exist for Those Approaching Retirement?

Individuals approaching retirement can leverage their expertise and experience through strategic partnerships that provide income opportunities and personal fulfillment. Some potential partnership opportunities include:

- Consulting Services: Offering consulting services to businesses or organizations in their area of expertise.

- Advisory Boards: Serving on advisory boards for companies or non-profit organizations.

- Mentoring Programs: Mentoring younger professionals and sharing their knowledge and experience.

- Freelance Projects: Taking on freelance projects that allow them to work on a flexible schedule and earn income.

- E-learning Platforms: Creating and selling online courses or workshops based on their expertise.

These partnerships can provide individuals approaching retirement with income opportunities, intellectual stimulation, and a sense of purpose.

4. What Role Does Continuous Learning Play in Maximizing Income Potential?

Continuous learning is essential for maximizing income potential at any age. In today’s rapidly changing job market, individuals must continuously update their skills, knowledge, and expertise to remain competitive and relevant.

4.1. How Can Individuals Stay Relevant in a Changing Job Market?

To stay relevant in a changing job market, individuals should:

- Identify Emerging Trends: Stay informed about the latest trends and technologies in their industry.

- Acquire New Skills: Develop new skills that are in demand by employers.

- Seek Out Training Opportunities: Participate in workshops, seminars, and online courses to enhance their knowledge and skills.

- Network with Industry Leaders: Connect with industry leaders and experts to learn about new developments and opportunities.

- Embrace Lifelong Learning: Commit to lifelong learning and continuously seek out new knowledge and experiences.

By staying proactive and embracing continuous learning, individuals can remain competitive and increase their earning potential.

4.2. What Types of Skills Are Most Valuable for Income Growth?

Certain skills are particularly valuable for income growth in today’s job market. These include:

| Skill Category | Specific Skills | Why They Are Valuable |

|---|---|---|

| Technical Skills | Data Analysis, Programming, Digital Marketing, Cloud Computing | These skills are in high demand across various industries and can command higher salaries. |

| Soft Skills | Communication, Leadership, Problem-Solving, Creativity | These skills are essential for effective collaboration, management, and innovation. |

| Business Skills | Financial Management, Project Management, Sales, Negotiation | These skills are critical for business success and can lead to higher earning potential in management and leadership roles. |

| Industry-Specific Skills | Healthcare Management, Cybersecurity, Artificial Intelligence | These skills are valuable in specific industries that are experiencing rapid growth and demand for specialized expertise. |

Developing these skills can significantly enhance an individual’s earning potential and career prospects.

4.3. How Can Online Resources Support Continuous Learning?

Online resources provide a wealth of opportunities for continuous learning and skill development. Some popular online learning platforms include:

- Coursera: Offers courses, specializations, and degrees from top universities and institutions around the world.

- edX: Provides access to high-quality courses from leading universities and organizations.

- Udemy: Features a wide range of courses on various topics, taught by industry experts.

- LinkedIn Learning: Offers courses and training videos focused on professional development and career advancement.

- Khan Academy: Provides free educational resources for learners of all ages.

These online resources make it easier than ever for individuals to access high-quality education and training, regardless of their location or financial situation.

5. How Does Entrepreneurship Affect the Age-Income Relationship?

Entrepreneurship can significantly alter the age-income relationship, offering individuals the potential to earn higher incomes and achieve greater financial independence.

5.1. What Are the Income Opportunities for Entrepreneurs of Different Ages?

Entrepreneurship offers income opportunities for individuals of all ages, but the types of opportunities and the potential for success may vary depending on their stage of life.

- Young Entrepreneurs (25-34): Often have the energy, creativity, and risk tolerance to launch innovative startups. They may face challenges in securing funding and building a strong network, but they can benefit from mentorship and accelerator programs.

- Mid-Career Entrepreneurs (35-54): Typically have accumulated significant experience, expertise, and capital, which can give them a competitive advantage in starting and growing a business. They may be more risk-averse than younger entrepreneurs, but they can leverage their networks and resources to achieve success.

- Late-Career Entrepreneurs (55-64): Can leverage their years of experience and industry knowledge to launch consulting businesses, advisory services, or encore career ventures. They may have more financial security and flexibility than younger entrepreneurs, allowing them to pursue passion projects and give back to their communities.

Entrepreneurship can provide individuals of all ages with the opportunity to earn higher incomes, achieve greater financial independence, and pursue their passions.

5.2. How Can Business Ownership Impact Long-Term Earning Potential?

Business ownership can have a significant impact on long-term earning potential. Successful entrepreneurs have the potential to earn substantially more than they would as employees, and they can build wealth through equity ownership in their businesses. Business ownership also provides opportunities for passive income through dividends, royalties, and licensing agreements. However, entrepreneurship also involves risks, and not all businesses succeed. Entrepreneurs must be prepared to work hard, take calculated risks, and adapt to changing market conditions to achieve long-term financial success.

5.3. What Resources Are Available to Support Aspiring Entrepreneurs?

A wealth of resources is available to support aspiring entrepreneurs, including:

- Small Business Administration (SBA): Provides resources, loans, and counseling services for small businesses.

- SCORE: Offers free mentoring and business advice from experienced entrepreneurs.

- Local Chambers of Commerce: Provide networking opportunities and resources for businesses in their communities.

- Startup Incubators and Accelerators: Offer resources, mentorship, and funding opportunities for early-stage startups.

- Online Business Courses: Provide training and education on various aspects of entrepreneurship.

These resources can help aspiring entrepreneurs develop their business plans, secure funding, and launch successful ventures.

6. How Do Economic Conditions Affect the Age-Income Relationship?

Economic conditions can significantly impact the age-income relationship, influencing job opportunities, wage growth, and investment returns.

6.1. How Do Recessions and Economic Downturns Impact Income Across Age Groups?

Recessions and economic downturns can have a disproportionate impact on income across different age groups. Young workers often face higher unemployment rates and lower wages during recessions, as they have less experience and seniority than older workers. Middle-aged workers may experience job losses or wage cuts, but they may have more savings and assets to cushion the impact. Older workers may face challenges in finding new jobs if they are laid off, and their retirement savings may be negatively affected by market downturns.

6.2. How Does Inflation Impact Purchasing Power for Different Age Groups?

Inflation can erode purchasing power for all age groups, but it can have a particularly significant impact on those with fixed incomes, such as retirees. As prices rise, individuals must spend more money to maintain their standard of living. Inflation can also reduce the real value of savings and investments, making it more difficult for individuals to achieve their financial goals.

6.3. How Can Individuals Protect Their Income During Economic Uncertainty?

To protect their income during economic uncertainty, individuals should:

- Diversify Their Income Sources: Explore multiple income streams, such as freelance work, part-time jobs, or investments.

- Build an Emergency Fund: Save at least three to six months’ worth of living expenses in a readily accessible account.

- Reduce Debt: Pay down high-interest debt to reduce monthly expenses and improve financial flexibility.

- Invest Wisely: Diversify investments across different asset classes to reduce risk and maximize returns.

- Stay Informed: Stay up-to-date on economic trends and financial news to make informed decisions.

By taking these steps, individuals can better protect their income and financial security during economic uncertainty.

7. What Are the Long-Term Financial Planning Considerations Related to Age and Income?

Long-term financial planning is essential for ensuring financial security and achieving financial goals throughout life. The age-income relationship plays a crucial role in financial planning, as income levels and financial priorities change over time.

7.1. How Should Young Adults Plan for Retirement with Varying Income Levels?

Young adults should start planning for retirement as early as possible, even if they have varying income levels. Some key retirement planning considerations for young adults include:

- Start Saving Early: The earlier you start saving, the more time your investments have to grow.

- Take Advantage of Employer-Sponsored Retirement Plans: Contribute to 401(k) or other retirement plans offered by your employer, especially if they offer matching contributions.

- Open an IRA: Consider opening a Roth IRA or traditional IRA to supplement your retirement savings.

- Invest Wisely: Diversify your investments across different asset classes to reduce risk and maximize returns.

- Increase Savings Over Time: As your income grows, increase your retirement savings to stay on track for your goals.

By starting early and saving consistently, young adults can build a solid foundation for retirement security.

7.2. What Strategies Can Mid-Career Professionals Use to Maximize Retirement Savings?

Mid-career professionals should focus on maximizing their retirement savings and ensuring they are on track to meet their retirement goals. Some strategies for maximizing retirement savings include:

- Increase Contributions: Increase contributions to employer-sponsored retirement plans and IRAs to the maximum allowable amount.

- Catch-Up Contributions: If you are age 50 or older, take advantage of catch-up contributions to boost your retirement savings.

- Review Investment Allocations: Review your investment allocations to ensure they are aligned with your risk tolerance and time horizon.

- Consider a Financial Advisor: Consult with a financial advisor to develop a comprehensive retirement plan.

- Pay Down Debt: Pay down high-interest debt to free up more cash flow for retirement savings.

By maximizing their retirement savings and managing their investments wisely, mid-career professionals can ensure they are well-prepared for retirement.

7.3. How Should Individuals Approaching Retirement Adjust Their Financial Plans?

Individuals approaching retirement should adjust their financial plans to prepare for the transition from working to retirement. Some key considerations for adjusting financial plans include:

- Estimate Retirement Expenses: Estimate your retirement expenses to determine how much income you will need to cover your living expenses.

- Assess Retirement Income Sources: Assess your retirement income sources, including Social Security, pensions, and retirement savings.

- Adjust Investment Allocations: Adjust your investment allocations to reduce risk and preserve capital.

- Consider Healthcare Costs: Factor in healthcare costs, including Medicare premiums and out-of-pocket expenses.

- Plan for Long-Term Care: Consider long-term care insurance or other strategies to protect against the costs of long-term care.

By carefully planning for retirement and adjusting their financial plans accordingly, individuals can ensure they have the financial resources they need to enjoy a comfortable and secure retirement.

8. Legal and Tax Implications Related to Age and Income

Age and income can have significant legal and tax implications, particularly regarding retirement planning, Social Security benefits, and estate planning.

8.1. How Does Age Affect Eligibility for Social Security Benefits?

Age affects eligibility for Social Security benefits in several ways:

- Early Retirement: Individuals can begin receiving Social Security retirement benefits as early as age 62, but their benefits will be reduced.

- Full Retirement Age: The full retirement age is the age at which individuals can receive their full Social Security retirement benefits. The full retirement age is 66 for those born between 1943 and 1954, and it gradually increases to 67 for those born in 1960 or later.

- Delayed Retirement: Individuals can delay receiving Social Security retirement benefits beyond their full retirement age, and their benefits will increase for each year they delay, up to age 70.

The age at which individuals choose to begin receiving Social Security benefits can have a significant impact on their lifetime benefits.

8.2. What Are the Tax Implications of Different Retirement Account Withdrawals?

The tax implications of retirement account withdrawals vary depending on the type of account:

- Traditional 401(k) and IRA: Withdrawals from traditional 401(k)s and IRAs are taxed as ordinary income.

- Roth 401(k) and IRA: Qualified withdrawals from Roth 401(k)s and IRAs are tax-free.

- Taxable Accounts: Withdrawals from taxable accounts are subject to capital gains taxes.

It is important to understand the tax implications of different retirement account withdrawals to minimize taxes and maximize retirement income.

8.3. How Does Estate Planning Relate to Age and Income?

Estate planning is the process of planning for the management and distribution of assets after death. Age and income are important considerations in estate planning, as individuals with higher incomes and more assets typically have more complex estate planning needs. Estate planning can help individuals:

- Minimize Estate Taxes: Reduce or eliminate estate taxes through careful planning and the use of trusts and other estate planning tools.

- Protect Assets: Protect assets from creditors and lawsuits.

- Ensure Wishes Are Followed: Ensure that assets are distributed according to their wishes.

- Provide for Loved Ones: Provide for the financial security of their loved ones.

Estate planning is an important part of financial planning for individuals of all ages and income levels.

9. How Does Gender Impact the Age-Income Trajectory?

Gender significantly influences the age-income trajectory, with women often facing unique challenges and opportunities in the workforce.

9.1. What Is the Gender Pay Gap and How Does It Evolve with Age?

The gender pay gap refers to the difference in earnings between men and women. Women consistently earn less than men, and the pay gap widens with age. According to the U.S. Census Bureau, women earn approximately 82 cents for every dollar earned by men. The pay gap is even wider for women of color. The gender pay gap is attributed to a variety of factors, including discrimination, occupational segregation, and work-life balance challenges.

9.2. What Are the Common Career Challenges Faced by Women at Different Ages?

Women face unique career challenges at different ages, including:

- Early Career: Women may face challenges in negotiating salaries and promotions, and they may experience bias and discrimination in hiring and advancement decisions.

- Mid-Career: Women may face challenges in balancing work and family responsibilities, and they may experience a “motherhood penalty” in terms of earnings and career advancement.

- Late Career: Women may face challenges in staying relevant and competitive in the workforce, and they may experience ageism and sexism.

These challenges can significantly impact women’s earning potential and career trajectories.

9.3. What Strategies Can Women Use to Overcome Income Disparities?

Women can use a variety of strategies to overcome income disparities, including:

- Negotiate Salaries and Promotions: Advocate for fair pay and promotions based on their skills, experience, and contributions.

- Seek Out Mentors and Sponsors: Build relationships with mentors and sponsors who can provide guidance, support, and advocacy.

- Develop Leadership Skills: Develop leadership skills and seek out leadership opportunities to advance their careers.

- Network and Build Relationships: Network with other professionals to expand their professional networks and access new opportunities.

- Pursue Continuous Learning: Continuously update their skills and knowledge to stay relevant and competitive in the workforce.

By taking these steps, women can increase their earning potential and overcome income disparities.

10. How Do Different Geographic Locations Affect the Age-Income Relationship?

Geographic location can significantly impact the age-income relationship, as income levels and cost of living vary across different regions.

10.1. How Do Income Levels Vary Across Different States in the U.S.?

Income levels vary significantly across different states in the U.S. States with strong economies, high levels of education, and concentrations of high-paying industries tend to have higher income levels. According to the U.S. Bureau of Economic Analysis, the states with the highest per capita personal income in 2020 were:

- Massachusetts

- Connecticut

- New York

- New Jersey

- Washington

States with weaker economies, lower levels of education, and concentrations of low-paying industries tend to have lower income levels.

10.2. What Are the Most Affordable and Expensive Cities for Different Age Groups?

The affordability of cities varies depending on factors such as housing costs, transportation costs, and cost of living. Some of the most affordable cities for young adults include:

- Austin, TX

- Columbus, OH

- Oklahoma City, OK

- Indianapolis, IN

- Kansas City, MO

Some of the most expensive cities for young adults include:

- San Francisco, CA

- New York, NY

- Boston, MA

- Los Angeles, CA

- Washington, D.C.

The affordability of cities can significantly impact the financial well-being of individuals in different age groups.

10.3. How Can Relocating Impact Earning Potential at Different Stages of Life?

Relocating can have a significant impact on earning potential at different stages of life. Young adults may relocate to cities with more job opportunities and higher salaries to advance their careers. Mid-career professionals may relocate to cities with lower costs of living to improve their financial situations. Individuals approaching retirement may relocate to cities with warmer climates or lower taxes to enjoy a more comfortable retirement. Relocating can be a strategic move for individuals looking to improve their earning potential and quality of life.

Ready to Unlock Your Earning Potential?

Don’t let age define your income trajectory. Explore the diverse partnership opportunities and proven strategies at income-partners.net. Whether you’re a young professional, a mid-career expert, or approaching retirement, we’ll help you find the perfect partners to boost your income and achieve your financial goals. Visit income-partners.net today and take control of your financial future. Address: 1 University Station, Austin, TX 78712, United States. Phone: +1 (512) 471-3434. Website: income-partners.net.

Income Growth

Financial Planning

Career Development

FAQ: How Does Age Affect Income?

- How does age typically influence income levels?

Income generally rises with age and experience, peaking near retirement and then slightly declining. - What role does education play in the age-income relationship?

Higher education levels typically lead to greater earning potential and faster career advancement. - Are there demographic factors that affect the age-income dynamic?

Yes, gender, race, and ethnicity can significantly influence income levels across different age groups. - What types of partnerships are beneficial for young professionals to boost their income?

Mentorship programs, networking groups, and skill-sharing communities can provide valuable opportunities. - How can mid-career professionals leverage partnerships for income growth?

Strategic alliances, joint marketing campaigns, and referral partnerships can expand business and revenue streams. - What income can be expected near retirement age, and how can it be supplemented?

Income may stabilize, but consulting services, advisory boards, and freelance projects can supplement earnings. - How can individuals stay relevant in a rapidly changing job market?

By identifying emerging trends, acquiring new skills, and embracing lifelong learning. - What strategies can women use to overcome income disparities?

Negotiating salaries, seeking mentors, and developing leadership skills can help close the gender pay gap. - How do economic conditions affect the age-income relationship?

Recessions and inflation can impact job opportunities and purchasing power across different age groups. - How should young adults plan for retirement with varying income levels?

Start saving early, take advantage of employer-sponsored plans, and increase savings over time.