Is My Gross Income On My W2 form? No, your gross income typically isn’t directly listed on your W2 form. However, understanding where to find the components of your gross income and how to calculate it is crucial for financial planning and partnership opportunities, and income-partners.net can help you navigate this. Let’s delve into how to find and calculate your gross income using the W2 form, with insights relevant to business owners, investors, and marketing professionals looking to maximize their income streams and foster strategic collaborations, including key strategies for financial success.

1. What Is Gross Income And Why Is It Important?

Gross income is not directly stated on the W2 form; it is crucial for assessing financial health, investment opportunities, and business partnerships.

Gross income represents the total amount of money you earn before any deductions, taxes, or other withholdings are taken out. It’s the initial figure from which all subsequent deductions are calculated, providing a clear picture of your earning potential before taxes. According to financial experts at the University of Texas at Austin’s McCombs School of Business, understanding gross income is fundamental for budgeting, investment planning, and accurately assessing your financial situation. Knowing your gross income helps you set realistic financial goals, make informed investment decisions, and negotiate effectively in business partnerships.

1.1. Why Gross Income Matters For Business Owners And Investors

For business owners and investors, gross income is a key indicator of revenue generation and overall business performance. A higher gross income suggests a stronger ability to cover operating expenses, invest in growth opportunities, and attract potential partners. Gross income is not just a top-line number; it’s a critical metric that influences strategic decisions, financial planning, and the pursuit of new ventures. Gross income directly impacts the ability to secure funding, attract investors, and negotiate favorable terms in business partnerships.

1.2. Gross Income and Strategic Partnerships

Understanding gross income is also vital when seeking strategic partnerships. Potential partners often evaluate your company’s financial health, and gross income is a primary factor in this assessment. Presenting a clear and accurate picture of your gross income can enhance your credibility and make your business more attractive to collaborators. Highlighting a strong gross income can lead to better negotiation positions and more advantageous partnership agreements. Gross income signals financial stability and growth potential, essential traits that attract reliable and beneficial partnerships.

2. Understanding The W2 Form: A Quick Overview

The W2 form is an essential tax document summarizing your annual earnings and deductions, and even though it does not directly state your gross income, it provides all the necessary components for its calculation.

The W2 form, officially known as the “Wage and Tax Statement,” is a document employers must provide to their employees each year, typically by January 31st. This form reports the employee’s annual wages and the amount of taxes withheld from their paycheck. The W2 form is crucial for filing your income tax return accurately. It contains several boxes, each providing specific financial details. Understanding these boxes is essential for calculating your gross income and ensuring you meet your tax obligations.

2.1. Key Boxes On The W2 Form Relevant To Gross Income

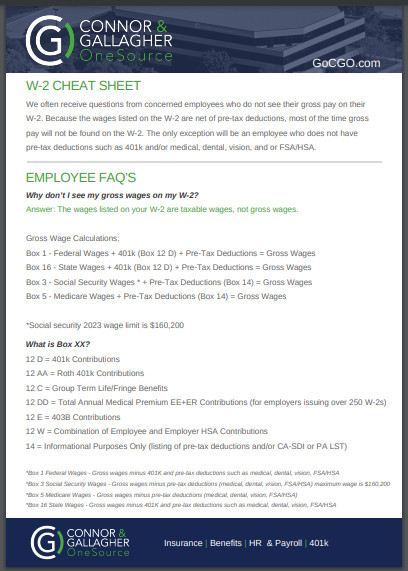

- Box 1: This box shows your total taxable wages, salaries, tips, and other compensation, which is your gross income minus certain pre-tax deductions.

- Box 3: This reflects the total wages subject to Social Security taxes, capped at a specific annual limit ($160,200 in 2023).

- Box 5: This shows the total wages subject to Medicare taxes, with no wage limit.

- Box 12: This box reports various types of deferred compensation and other benefits, often including pre-tax contributions to retirement plans such as 401(k)s.

- Box 14: This is an informational box used by employers to report additional deductions or information, such as state disability insurance or other non-taxable benefits.

2.2. Importance Of Accurate W2 Information

Ensuring the accuracy of your W2 form is critical for tax compliance and financial planning. Errors on your W2 form can lead to incorrect tax filings, potentially resulting in penalties or missed deductions. Review your W2 form carefully upon receipt and compare it with your own records to identify any discrepancies. Promptly address any errors with your employer to ensure accurate tax reporting and avoid future complications. Correct W2 information is essential for accurate financial analysis and strategic decision-making.

W-2 Cheat Sheet for 2023 Tax Year

W-2 Cheat Sheet for 2023 Tax Year

3. Calculating Gross Income From Your W2 Form: Step-By-Step

Calculating gross income from your W2 form requires adding back any pre-tax deductions to the taxable wages reported in Box 1, providing a comprehensive view of your total earnings.

While your W2 form does not explicitly state your gross income, you can easily calculate it by using the information provided in various boxes. The most common method involves adding back any pre-tax deductions to the taxable wages reported in Box 1. Pre-tax deductions are amounts deducted from your wages before taxes are calculated, such as contributions to a 401(k), health insurance premiums, or contributions to a Health Savings Account (HSA). By adding these amounts back to your taxable wages, you arrive at your gross income.

3.1. Step 1: Identify Your Taxable Wages

Locate Box 1 on your W2 form. This box shows your total taxable wages, which is your gross income minus pre-tax deductions. This figure is the starting point for calculating your gross income. It reflects the amount of your earnings that were subject to federal income tax. Knowing your taxable wages is essential for understanding your tax liability and planning your finances accordingly.

3.2. Step 2: Identify Pre-Tax Deductions

Examine Box 12 on your W2 form. This box contains codes that indicate different types of deferred compensation and benefits, some of which are pre-tax deductions. Common codes include:

- Code D: 401(k) contributions

- Code E: 403(b) contributions

- Code DD: Total annual medical premium (employer and employee contributions)

- Code W: Health Savings Account (HSA) contributions

Additionally, check Box 14 for any other pre-tax deductions that may be listed. This box is used for informational purposes and can include items like flexible spending account (FSA) contributions or other non-taxable benefits. Identifying all pre-tax deductions is essential for accurately calculating your gross income.

3.3. Step 3: Add Pre-Tax Deductions To Taxable Wages

Add the amounts listed under the relevant codes in Box 12 and any pre-tax deductions listed in Box 14 to the taxable wages in Box 1. The sum is your gross income.

Example:

- Box 1 (Taxable Wages): $60,000

- Box 12, Code D (401(k) contributions): $5,000

- Box 12, Code DD (Medical premiums): $2,000

Gross Income = $60,000 + $5,000 + $2,000 = $67,000

This calculation provides a clear picture of your total earnings before any deductions or taxes, giving you a better understanding of your financial standing.

4. Examples Of Gross Income Calculations

Illustrating gross income calculations through practical examples clarifies the process and underscores the importance of accurate W2 information.

To further clarify how to calculate gross income from your W2 form, let’s look at a few more examples:

4.1. Example 1: Employee With 401(K) And Health Insurance

Scenario:

- Box 1 (Taxable Wages): $55,000

- Box 12, Code D (401(k) contributions): $6,000

- Box 12, Code DD (Medical premiums): $3,000

Calculation:

Gross Income = $55,000 + $6,000 + $3,000 = $64,000

In this case, the employee’s gross income is $64,000, reflecting their total earnings before pre-tax deductions for retirement savings and health insurance.

4.2. Example 2: Employee With HSA And FSA Contributions

Scenario:

- Box 1 (Taxable Wages): $70,000

- Box 12, Code W (HSA contributions): $2,500

- Box 14 (FSA contributions): $1,500

Calculation:

Gross Income = $70,000 + $2,500 + $1,500 = $74,000

Here, the employee’s gross income is $74,000, taking into account contributions to both a Health Savings Account and a Flexible Spending Account.

4.3. Example 3: Employee With Multiple Deductions

Scenario:

- Box 1 (Taxable Wages): $80,000

- Box 12, Code D (401(k) contributions): $7,000

- Box 12, Code E (403(b) contributions): $3,000

- Box 12, Code DD (Medical premiums): $4,000

Calculation:

Gross Income = $80,000 + $7,000 + $3,000 + $4,000 = $94,000

In this comprehensive example, the employee’s gross income is $94,000, including deductions for both 401(k) and 403(b) retirement plans, as well as medical premiums.

These examples highlight the importance of identifying and adding all pre-tax deductions to accurately calculate your gross income, which is essential for financial planning and strategic partnerships.

5. Why Gross Income Matters For Partnerships And Collaborations

Gross income is a key indicator of financial stability and growth potential, making it crucial for attracting partners and negotiating favorable collaboration terms.

For business owners, investors, and marketing professionals, understanding and leveraging gross income is essential for forming successful partnerships and collaborations. Gross income provides a clear picture of your company’s financial health and growth potential, which are critical factors for attracting the right partners. Demonstrating a strong gross income can enhance your credibility and create opportunities for more advantageous collaborations.

5.1. Attracting Potential Partners

Potential partners are often looking for businesses that are financially stable and have a proven track record of generating revenue. A healthy gross income signals that your company is capable of meeting its financial obligations and investing in future growth. When presenting your business to potential partners, highlight your gross income trends and explain how your revenue streams are sustainable. This demonstrates your business acumen and makes your company a more attractive prospect for collaboration.

5.2. Negotiating Collaboration Terms

When entering into a partnership, the terms of the agreement will significantly impact your business’s financial outcomes. A strong gross income can give you leverage in negotiations, allowing you to secure more favorable terms. For instance, you may be able to negotiate a higher percentage of profits or gain access to better resources and support from your partners. Being able to demonstrate a robust gross income positions you as a valuable contributor and increases your influence in the collaboration.

5.3. Examples Of Successful Partnerships Driven By Gross Income

Consider a scenario where a small marketing agency seeks to partner with a larger software company. The marketing agency can demonstrate a consistent increase in gross income over the past three years, showcasing its ability to drive revenue growth for its clients. This strong financial performance makes the agency an attractive partner for the software company, which is looking to expand its market reach. The partnership could involve the marketing agency promoting the software company’s products to its existing client base, with a revenue-sharing agreement that benefits both parties.

In another example, an investor might be interested in partnering with a startup that has shown promising gross income growth. The investor could provide capital and strategic guidance to help the startup scale its operations. The startup’s strong gross income demonstrates its potential for future profitability, making it a worthwhile investment opportunity. These examples illustrate how a clear understanding and effective communication of your gross income can pave the way for successful and mutually beneficial partnerships.

6. Common Misconceptions About Gross Income On W2 Forms

Addressing common misconceptions about gross income on W2 forms ensures accuracy in financial planning and partnership evaluations, avoiding potential misunderstandings.

Many people have misconceptions about what information is included on their W2 form, particularly regarding gross income. These misunderstandings can lead to confusion when filing taxes or making financial decisions. Addressing these common misconceptions is essential for ensuring accuracy in financial planning and partnership evaluations.

6.1. Misconception 1: Gross Income Is The Same As Taxable Wages

Reality: Gross income is not the same as taxable wages. Taxable wages, reported in Box 1 of the W2 form, are your gross income minus any pre-tax deductions. This misconception can lead to an underestimation of your actual earnings. Always remember to add back pre-tax deductions to your taxable wages to calculate your true gross income.

6.2. Misconception 2: All Deductions Are Included In Box 1

Reality: Not all deductions are included in Box 1. Box 1 only reflects pre-tax deductions, such as contributions to retirement plans and health insurance premiums. Post-tax deductions, such as charitable contributions or certain investment losses, are not reflected in Box 1 and do not affect your gross income calculation. Understanding the distinction between pre-tax and post-tax deductions is crucial for accurate financial analysis.

6.3. Misconception 3: The W2 Form Shows All Income

Reality: The W2 form only shows income earned from a specific employer. If you have multiple jobs or other sources of income, such as self-employment income or investment income, these amounts will not be included on your W2 form. To get a complete picture of your total income, you need to consider all sources of earnings, including those reported on other tax forms like the 1099.

6.4. Misconception 4: Box 14 Includes All Pre-Tax Deductions

Reality: While Box 14 can include some pre-tax deductions, it is primarily used for informational purposes and may not list all deductions. The primary source for identifying pre-tax deductions is Box 12, which uses specific codes to indicate different types of deferred compensation and benefits. Always cross-reference Box 12 and Box 14 to ensure you capture all pre-tax deductions when calculating your gross income.

6.5. Misconception 5: Gross Income Is Irrelevant For Tax Planning

Reality: Gross income is highly relevant for tax planning. It serves as the foundation for calculating your adjusted gross income (AGI), which is used to determine your eligibility for various tax deductions and credits. Understanding your gross income allows you to make informed decisions about tax planning strategies, such as maximizing pre-tax deductions to reduce your taxable income. Effective tax planning can help you minimize your tax liability and optimize your financial outcomes.

7. Leveraging Income-Partners.Net For Strategic Partnerships

Income-partners.net offers resources and connections to help business owners, investors, and marketing professionals form strategic partnerships that enhance income and growth.

For individuals and businesses looking to optimize their income and forge strategic partnerships, income-partners.net provides a valuable platform. This resource offers a range of services and information designed to help you identify, evaluate, and establish beneficial collaborations.

7.1. Identifying Potential Partners

Income-partners.net hosts a diverse network of business owners, investors, and marketing professionals, creating opportunities to connect with potential partners who align with your goals and vision. The platform allows you to search for partners based on industry, expertise, and financial criteria, streamlining the process of finding the right collaborators. By leveraging the network on income-partners.net, you can tap into a wealth of talent and resources that can drive your business forward.

7.2. Evaluating Partnership Opportunities

Before entering into a partnership, it’s crucial to assess the potential benefits and risks involved. Income-partners.net offers tools and resources to help you evaluate partnership opportunities, including financial analysis templates and due diligence checklists. These resources can help you assess the financial health of potential partners, understand the terms of the agreement, and identify any potential red flags. By conducting thorough evaluations, you can make informed decisions that protect your interests and maximize the chances of a successful partnership.

7.3. Building Stronger Relationships

Once you’ve identified a potential partner, building a strong and trusting relationship is essential for long-term success. Income-partners.net provides communication tools and networking events to help you foster meaningful connections with your partners. The platform also offers resources on effective communication strategies and conflict resolution techniques, enabling you to navigate the challenges that may arise in a partnership. By investing in relationship-building, you can create a solid foundation for a mutually beneficial collaboration.

Address: 1 University Station, Austin, TX 78712, United States.

Phone: +1 (512) 471-3434.

Website: income-partners.net.

7.4. Success Stories From Income-Partners.Net

Several businesses have achieved significant growth and increased income through partnerships facilitated by income-partners.net. For example, a small e-commerce company partnered with a marketing agency found on the platform, resulting in a 30% increase in sales within six months. Another success story involves an investor who connected with a promising startup on income-partners.net, leading to a lucrative investment and long-term financial gains. These examples demonstrate the potential of income-partners.net to drive meaningful business outcomes and enhance income opportunities.

7.5. Call to Action

Are you ready to take your business to the next level through strategic partnerships? Visit income-partners.net today to explore the possibilities and connect with potential collaborators. Discover the resources and tools that can help you identify, evaluate, and build successful partnerships that drive income and growth. Don’t miss out on the opportunity to transform your business and achieve your financial goals.

8. Advanced Strategies For Maximizing Income Through Partnerships

Advanced strategies for maximizing income through partnerships involve innovative approaches, clear communication, and adaptability to ensure mutual success.

To truly maximize your income through partnerships, consider implementing these advanced strategies.

8.1. Diversifying Partnership Models

Rather than limiting yourself to one type of partnership, explore different models that align with your business goals. For example, you might consider strategic alliances, joint ventures, or licensing agreements. Each model offers unique benefits and can help you tap into new markets, access specialized expertise, or share resources. Diversifying your partnership models can create multiple revenue streams and reduce your reliance on any single collaboration.

8.2. Implementing Performance-Based Agreements

Performance-based agreements align incentives and ensure that all parties are motivated to achieve shared goals. These agreements tie compensation or revenue sharing to specific performance metrics, such as sales targets, customer acquisition rates, or project milestones. By implementing performance-based agreements, you can incentivize your partners to deliver results and drive mutual success. This approach also promotes transparency and accountability, fostering a stronger and more productive partnership.

8.3. Investing In Continuous Improvement

Partnerships require ongoing effort and commitment to thrive. Invest in continuous improvement by regularly evaluating the performance of your partnerships and identifying areas for optimization. Conduct periodic reviews to assess whether the partnership is meeting its objectives and to identify any challenges or obstacles. Use this feedback to refine your strategies, improve communication, and strengthen the relationship. Continuous improvement ensures that your partnerships remain relevant and effective over time.

8.4. Leveraging Technology For Collaboration

Technology can play a crucial role in facilitating collaboration and maximizing income through partnerships. Utilize project management tools, communication platforms, and data analytics software to streamline workflows, enhance communication, and track performance. These tools can help you monitor progress, identify trends, and make data-driven decisions that optimize your partnership outcomes. Embracing technology can improve efficiency, reduce costs, and drive greater revenue generation.

8.5. Fostering A Culture Of Innovation

Encourage a culture of innovation within your partnerships by promoting open communication, experimentation, and creative problem-solving. Create opportunities for partners to share ideas, brainstorm new strategies, and explore innovative solutions. By fostering a culture of innovation, you can unlock new opportunities for growth and generate novel approaches that drive income. This collaborative mindset can help you stay ahead of the competition and achieve sustainable success.

9. How To Avoid Common Partnership Pitfalls

Avoiding common partnership pitfalls requires careful planning, clear communication, and a commitment to addressing challenges proactively.

While partnerships can be highly beneficial, they also come with potential pitfalls that can derail your success. Here’s how to avoid them:

9.1. Conduct Thorough Due Diligence

Before entering into a partnership, conduct thorough due diligence to assess the potential partner’s financial stability, reputation, and alignment with your values. Review their financial statements, check their references, and research their track record. This due diligence can help you identify any red flags and make an informed decision about whether to proceed with the partnership.

9.2. Establish Clear Roles And Responsibilities

Clearly define the roles and responsibilities of each partner from the outset. Outline who is responsible for what tasks, how decisions will be made, and how conflicts will be resolved. Document these roles and responsibilities in a written agreement to avoid misunderstandings and ensure accountability. Clear roles and responsibilities can prevent confusion and promote a more efficient and harmonious partnership.

9.3. Maintain Open Communication

Open and honest communication is essential for a successful partnership. Establish regular communication channels and encourage partners to share information, ideas, and concerns. Be transparent about your expectations, challenges, and successes. This ongoing communication can help you build trust, resolve conflicts, and maintain a strong working relationship.

9.4. Have A Contingency Plan

Despite your best efforts, partnerships can sometimes fail. Be prepared for this possibility by having a contingency plan in place. Outline the steps you will take if the partnership does not work out, including how assets will be divided, how responsibilities will be transitioned, and how the relationship will be terminated. A contingency plan can help you minimize the disruption and financial impact of a failed partnership.

9.5. Seek Legal Counsel

Before finalizing any partnership agreement, seek legal counsel to ensure that your interests are protected. An attorney can review the agreement, advise you on potential risks and liabilities, and help you negotiate favorable terms. Legal counsel can provide invaluable guidance and help you avoid costly mistakes.

10. Staying Updated On Partnership Trends And Opportunities

Staying updated on partnership trends and opportunities is essential for remaining competitive, identifying new collaborations, and adapting to evolving market dynamics.

The business landscape is constantly evolving, and so are the trends and opportunities in partnerships. Staying informed about the latest developments can help you remain competitive and maximize your income potential.

10.1. Follow Industry Publications And Blogs

Subscribe to industry publications, blogs, and newsletters that cover partnership trends and best practices. These resources can provide valuable insights into emerging opportunities, successful partnership models, and innovative strategies. Stay informed about the latest research, case studies, and expert opinions to enhance your understanding of the partnership landscape.

10.2. Attend Industry Events And Conferences

Attend industry events and conferences to network with potential partners, learn from industry leaders, and stay updated on the latest trends. These events offer opportunities to connect with like-minded professionals, exchange ideas, and explore potential collaborations. Take advantage of workshops, seminars, and keynote speeches to expand your knowledge and gain new perspectives on partnerships.

10.3. Leverage Social Media

Follow industry influencers and thought leaders on social media platforms such as LinkedIn, Twitter, and Facebook. Engage in discussions, share your insights, and connect with other professionals in your field. Social media can be a valuable tool for staying informed about partnership trends, identifying potential opportunities, and building your professional network.

10.4. Monitor Competitor Activities

Keep an eye on what your competitors are doing in terms of partnerships. Analyze their collaborations, evaluate their strategies, and identify any lessons you can learn. Monitoring competitor activities can help you identify potential opportunities and stay ahead of the curve.

10.5. Join Professional Organizations

Join professional organizations and associations related to your industry. These organizations often provide resources, networking opportunities, and educational programs focused on partnerships. Membership can give you access to exclusive content, industry events, and a community of like-minded professionals.

By staying updated on partnership trends and opportunities, you can make informed decisions, identify new collaborations, and maximize your income potential.

Frequently Asked Questions (FAQs)

Here are some frequently asked questions about gross income and W2 forms:

1. Why is my gross income not explicitly stated on my W2 form?

Your gross income isn’t directly stated because the W2 form primarily reports taxable wages, which are your earnings after pre-tax deductions.

2. What are pre-tax deductions, and why do they affect my taxable wages?

Pre-tax deductions are amounts deducted from your wages before taxes are calculated, such as 401(k) contributions, and they reduce your taxable income.

3. Where can I find information about my pre-tax deductions on my W2 form?

You can find pre-tax deductions listed in Box 12 of your W2 form, with specific codes indicating the type of deduction.

4. How do I calculate my gross income using my W2 form?

To calculate your gross income, add the pre-tax deductions listed in Box 12 and Box 14 to the taxable wages reported in Box 1 of your W2 form.

5. What should I do if I find an error on my W2 form?

If you find an error on your W2 form, contact your employer immediately to request a corrected form (W2-C).

6. Are Social Security and Medicare wages the same as my gross income?

Social Security and Medicare wages (Boxes 3 and 5) are generally similar to your gross income but may have some differences due to specific deduction rules and wage limits.

7. How does my gross income affect my eligibility for certain tax deductions and credits?

Your gross income is used to calculate your adjusted gross income (AGI), which determines your eligibility for various tax deductions and credits.

8. Can I use my W2 form to verify my income for loan applications or other financial purposes?

Yes, you can use your W2 form to verify your income, but be sure to calculate your gross income accurately for a comprehensive view of your earnings.

9. What if I have multiple W2 forms from different employers? How do I calculate my total gross income?

To calculate your total gross income, you need to calculate the gross income from each W2 form separately and then add them together.

10. How can income-partners.net help me leverage my gross income for strategic partnerships?

income-partners.net provides resources and connections to help you identify, evaluate, and establish strategic partnerships that can enhance your income and growth potential.