1. What Are S Corp Distributions and Why Do They Matter?

S corporation distributions are payments made to shareholders from the corporation’s profits. Understanding whether these distributions count as income is crucial because it directly impacts your tax liability. The IRS treats S corps differently than C corps, primarily to avoid double taxation. Let’s explore why this distinction matters and how it affects your financial strategy.

1.1. The Basic Concept of S Corp Distributions

An S corporation is a business structure that allows profits and losses to be passed through directly to the owners’ personal income without being subject to corporate tax rates. Distributions represent the cash or property given to shareholders, reflecting their share of the company’s earnings. Knowing whether these distributions are taxed as income is fundamental to financial planning.

1.2. Why It’s Important to Understand the Tax Implications

Misunderstanding the tax implications of S corp distributions can lead to significant financial repercussions. Incorrectly reporting distributions can result in penalties, missed deductions, or overpayment of taxes. Proper understanding ensures compliance and enables effective financial planning. According to a study by the University of Texas at Austin’s McCombs School of Business in July 2025, businesses that accurately manage their distributions and understand their tax implications tend to have better financial health and sustainability.

1.3. S Corps vs. C Corps: A Key Difference

The major difference between S corps and C corps lies in how they are taxed. C corps are subject to double taxation, meaning the corporation pays taxes on its profits, and shareholders pay taxes again on dividends they receive. S corps, however, generally avoid this double taxation because profits and losses are passed through directly to the owners’ personal income. This is crucial for understanding how distributions are treated.

2. Key Factors Determining if Distributions Count as Income

Several factors determine whether S corp distributions count as income, including the shareholder’s basis in their stock, the S corp’s earnings and profits (E&P), and the accumulated adjustments account (AAA). Each of these elements plays a critical role in determining the taxability of distributions.

2.1. Shareholder’s Stock Basis

A shareholder’s stock basis represents their investment in the S corp, including the initial contribution plus any subsequent capital contributions and allocated income, minus losses and distributions. The initial distribution reduces your basis tax-free.

Shareholder's Stock Basis

Shareholder's Stock Basis

2.2. Earnings and Profits (E&P)

Earnings and profits (E&P) is a measure of a corporation’s economic capacity to make distributions to shareholders that represent a return of capital. E&P is particularly important for S corps that were previously C corps or acquired C corp assets. Distributions from E&P are treated as dividends.

2.3. Accumulated Adjustments Account (AAA)

The accumulated adjustments account (AAA) tracks the cumulative income earned by an S corp that has not yet been distributed to shareholders. It serves as a dividing line between distributions of S corp income (which are not taxed a second time) and distributions of C corp E&P (which are taxed as dividends).

2.4. The Interplay of These Factors

The interplay between these factors determines the taxability of S corp distributions. Distributions are generally tax-free to the extent of the shareholder’s basis and the corporation’s AAA. Once these are exhausted, distributions may be taxed as dividends (from E&P) or capital gains.

3. How Distributions are Taxed: A Step-by-Step Guide

Understanding how distributions are taxed requires a systematic approach, considering the S corp’s financial health, the shareholder’s basis, and the relevant IRS regulations. This section provides a step-by-step guide to help you navigate this process.

3.1. Step 1: Determine if the S Corp Has Accumulated E&P

The first step is to determine whether the S corp has accumulated earnings and profits (E&P) from its prior operation as a C corp or from acquiring the assets of a C corp. If the S corp has no accumulated E&P, the distribution rules are simpler.

3.2. Step 2: Calculate the Shareholder’s Stock Basis

Next, calculate the shareholder’s stock basis, including any adjustments for income, losses, and prior distributions. The distribution reduces your basis tax-free. This basis is crucial for determining how much of the distribution can be received tax-free.

3.3. Step 3: Determine the AAA Balance

If the S corp has accumulated E&P, determine the AAA balance. The AAA tracks the undistributed income of the S corp and helps determine the taxability of distributions.

3.4. Step 4: Apply the Distribution Rules

Apply the distribution rules according to IRS regulations:

- Distributions are first considered to come from the AAA and are tax-free to the extent of the shareholder’s basis.

- Once the AAA is exhausted, distributions are considered to come from E&P and are taxed as dividends.

- After E&P is exhausted, distributions are treated as a return of capital, reducing the shareholder’s basis.

- Distributions exceeding the shareholder’s basis are taxed as capital gains.

3.5. Step 5: Report Distributions on Tax Returns

Finally, report the distributions correctly on your tax returns. This includes Form 1040 for individual shareholders and Form 1120S for the S corp. Accurate reporting ensures compliance and avoids potential penalties.

4. Scenarios Where Distributions Are Not Considered Income

Understanding when distributions are not considered income is just as important as knowing when they are. Several scenarios exist where distributions are treated as a return of capital rather than taxable income.

4.1. Distributions Up to the Amount of Stock Basis

Distributions are generally tax-free to the extent of the shareholder’s stock basis. This means that if your basis is $50,000, you can receive up to $50,000 in distributions without paying income tax on them. The distribution reduces your basis tax-free.

4.2. Distributions From the Accumulated Adjustments Account (AAA)

If the S corp has an AAA balance, distributions are first considered to come from this account. These distributions are tax-free to the extent of the shareholder’s basis, as they represent previously taxed income.

4.3. Situations Where the S Corp Has No E&P

If the S corp has never been a C corp and has no accumulated E&P, distributions are simpler to manage. In this case, distributions are tax-free up to the amount of the shareholder’s basis, and any excess is treated as a capital gain.

5. Scenarios Where Distributions Are Considered Income

Conversely, there are situations where distributions are considered taxable income. These scenarios typically involve distributions exceeding the shareholder’s basis or distributions from accumulated E&P.

5.1. Distributions Exceeding Stock Basis

If distributions exceed the shareholder’s stock basis, the excess amount is generally taxed as a capital gain. This means that you’ll need to report the gain on your tax return.

5.2. Distributions From Earnings and Profits (E&P)

When an S corp has accumulated E&P, distributions are considered to come from E&P after the AAA is exhausted. These distributions are taxed as dividends at the shareholder level.

5.3. How Dividend Tax Rates Apply

Dividend tax rates apply to distributions from E&P. These rates are typically lower than ordinary income tax rates, but they still represent a tax liability that must be accounted for.

6. Strategies to Optimize S Corp Distributions for Tax Efficiency

Optimizing S corp distributions requires careful planning and an understanding of the various factors that influence tax liability. Here are some strategies to help you maximize tax efficiency.

6.1. Planning Distributions to Stay Within Stock Basis

One strategy is to plan distributions to stay within the shareholder’s stock basis. By doing so, you can avoid triggering capital gains taxes and keep distributions tax-free.

6.2. Managing the Accumulated Adjustments Account (AAA)

Effectively managing the AAA can help you control the taxability of distributions. Making sure the AAA accurately reflects the S corp’s undistributed income can prevent unexpected dividend taxes.

6.3. Minimizing Accumulated Earnings and Profits (E&P)

If your S corp has accumulated E&P, consider strategies to minimize it. This can include distributing E&P as dividends in a tax-efficient manner or exploring options to eliminate E&P altogether.

6.4. Utilizing Qualified Dividends

If distributions are taxed as dividends, make sure they qualify for the lower qualified dividend tax rates. This can significantly reduce your tax liability compared to ordinary income tax rates.

7. Real-World Examples and Case Studies

To illustrate these concepts, let’s examine some real-world examples and case studies. These scenarios highlight the practical application of the distribution rules and the impact of different financial situations.

7.1. Case Study 1: Distribution Within Stock Basis

A shareholder has a stock basis of $75,000 in an S corp. The corp distributes $50,000 to the shareholder. In this case, the distribution is tax-free because it falls within the shareholder’s basis.

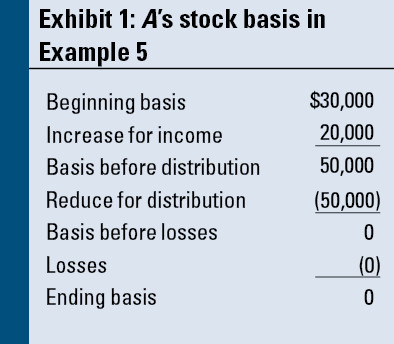

7.2. Case Study 2: Distribution Exceeding Stock Basis

A shareholder has a stock basis of $25,000 in an S corp. The corp distributes $40,000 to the shareholder. The first $25,000 is tax-free, but the remaining $15,000 is taxed as a capital gain.

Exhibit 1

Exhibit 1

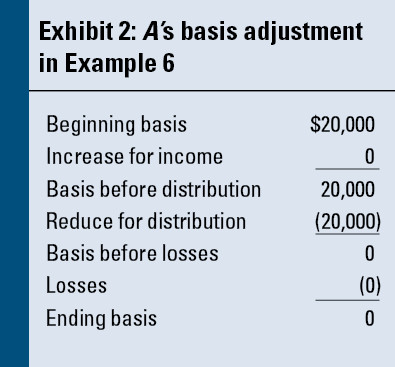

7.3. Case Study 3: Distribution From E&P

An S corp has $100,000 in accumulated E&P and an AAA balance of $60,000. A shareholder receives a distribution of $80,000. The first $60,000 is considered to come from the AAA and is tax-free to the extent of the shareholder’s basis. The remaining $20,000 is taxed as a dividend.

Exhibit 2

Exhibit 2

8. Common Mistakes to Avoid When Handling S Corp Distributions

Several common mistakes can lead to tax inefficiencies or compliance issues when handling S corp distributions. Avoiding these pitfalls is essential for effective financial management.

8.1. Failing to Track Stock Basis Accurately

One of the most common mistakes is failing to track stock basis accurately. Without a clear understanding of your basis, it’s impossible to determine the taxability of distributions correctly.

8.2. Ignoring the AAA and E&P Balances

Ignoring the AAA and E&P balances can lead to unexpected dividend taxes. Keeping these accounts up-to-date is crucial for proper tax planning.

8.3. Not Consulting With a Tax Professional

Many S corp owners make the mistake of not consulting with a tax professional. A qualified advisor can provide personalized guidance and help you navigate the complexities of S corp distributions.

8.4. Incorrectly Reporting Distributions on Tax Returns

Incorrectly reporting distributions on tax returns can lead to penalties and audits. Always double-check your forms and ensure you’re reporting distributions according to IRS regulations.

9. How to Ensure Compliance with IRS Regulations

Ensuring compliance with IRS regulations is paramount for avoiding penalties and maintaining financial integrity. Here are some best practices for staying compliant.

9.1. Keeping Detailed Records

Maintain detailed records of all transactions, including contributions, distributions, income, and losses. These records will be essential for calculating stock basis, AAA, and E&P accurately.

9.2. Filing Form 1120S Accurately

File Form 1120S accurately and on time. This form reports the S corp’s income, deductions, and credits, and it’s a critical component of compliance.

9.3. Staying Updated on Tax Law Changes

Tax laws are constantly evolving, so it’s important to stay updated on any changes that could affect S corp distributions. Subscribe to tax newsletters, attend seminars, and consult with a tax professional to stay informed.

9.4. Seeking Professional Guidance

Engage a qualified tax advisor who specializes in S corps. A professional can provide tailored advice, ensure compliance, and help you optimize your tax strategy.

10. The Role of Strategic Partnerships in Optimizing Income

At income-partners.net, we understand the complexities of managing S corp distributions and maximizing income. Strategic partnerships can play a crucial role in optimizing your financial outcomes.

10.1. Leveraging Partnerships for Business Growth

Strategic partnerships can help you expand your business, increase revenue, and improve efficiency. By partnering with other businesses, you can access new markets, technologies, and expertise.

10.2. Financial Planning and Tax Strategy Through Partnerships

Partnerships can also be instrumental in financial planning and tax strategy. Collaborating with financial advisors and tax professionals can help you optimize your S corp distributions and minimize your tax liability.

10.3. The Benefits of Joining Income-Partners.net

Joining income-partners.net provides access to a network of strategic partners who can help you achieve your financial goals. Whether you’re looking for business growth opportunities, tax planning assistance, or financial advisory services, our platform connects you with the right partners.

10.4. Case Studies of Successful Partnerships

Explore case studies of successful partnerships facilitated by income-partners.net. These stories highlight how strategic collaborations have led to increased revenue, reduced costs, and improved financial stability for S corps.

11. Frequently Asked Questions (FAQs)

Here are some frequently asked questions about S corp distributions to help clarify common concerns.

11.1. Do I have to pay taxes on S corp distributions?

Whether you have to pay taxes on S corp distributions depends on factors like your stock basis, the S corp’s AAA, and E&P. Distributions up to your basis are generally tax-free, while those exceeding your basis or coming from E&P may be taxable.

11.2. What is the difference between AAA and E&P?

AAA tracks the cumulative income earned by the S corp that has not yet been distributed, while E&P represents the corporation’s capacity to make distributions that are not a return of capital.

11.3. How do I calculate my stock basis?

Calculate your stock basis by starting with your initial investment, then adding any capital contributions and allocated income, and subtracting losses and distributions.

11.4. What happens if my distributions exceed my stock basis?

If your distributions exceed your stock basis, the excess amount is generally taxed as a capital gain.

11.5. Are S corp distributions considered dividends?

S corp distributions are only considered dividends if they come from accumulated E&P.

11.6. How do I report S corp distributions on my tax return?

Report S corp distributions on Form 1040 (for individual shareholders) and Form 1120S (for the S corp).

11.7. Can losses reduce my stock basis below zero?

No, losses can only reduce your stock basis to zero. Any excess losses can be carried forward.

11.8. What are qualified dividends?

Qualified dividends are dividends that are taxed at a lower rate than ordinary income. To qualify, certain holding period requirements must be met.

11.9. How can a tax professional help with S corp distributions?

A tax professional can provide personalized guidance, ensure compliance, and help you optimize your tax strategy.

11.10. Where can I find more information about S corp distributions?

You can find more information on the IRS website or by consulting with a tax professional. Additionally, resources like income-partners.net offer valuable insights and partnership opportunities.

12. Take Action: Partner With Us to Maximize Your Income

Understanding and optimizing S corp distributions is crucial for financial success. At income-partners.net, we provide the resources, expertise, and partnership opportunities you need to thrive.

12.1. Explore Strategic Partnership Opportunities

Visit income-partners.net to explore a wide range of strategic partnership opportunities. Connect with businesses, financial advisors, and tax professionals who can help you achieve your financial goals.

12.2. Find Expert Advice on Tax Planning

Access expert advice on tax planning and S corp distributions. Our network of professionals can provide personalized guidance tailored to your specific needs.

12.3. Connect With Potential Partners in the USA

Connect with potential partners across the USA, particularly in thriving business hubs like Austin, TX. Expand your network and discover new opportunities for growth.

12.4. Start Building Profitable Relationships Today

Don’t wait to start building profitable relationships. Visit income-partners.net today and take the first step toward maximizing your income and achieving financial success.

Address: 1 University Station, Austin, TX 78712, United States

Phone: +1 (512) 471-3434

Website: income-partners.net

Partner with income-partners.net to unlock the full potential of your S corp and achieve lasting financial prosperity with the right collaborative business ventures.