Figuring out how much car you can afford based on your income is crucial for making smart financial decisions. Income-partners.net offers expert guidance to help you determine a realistic car budget, ensuring you don’t overextend your finances and can explore potential partnership opportunities to boost your income simultaneously. By carefully assessing your financial situation, you can drive off the lot with confidence, knowing you’ve made a sound investment in both transportation and your future financial well-being. Let’s dive into vehicle affordability, financial planning, and budget allocation to empower you with the knowledge to make informed decisions.

1. Assessing Your Income and Expenses

Determining the right car for your budget starts with a clear understanding of your income and expenses. Begin by calculating your monthly take-home pay and then outlining all your monthly and annual expenses to get a realistic view of your financial capacity.

Calculating how much car you can afford requires a thorough evaluation of your financial standing. This involves taking a close look at various factors to ensure you make an informed decision that aligns with your financial goals. Here’s a breakdown of the key elements:

1.1. Start with Your Net Income

Instead of focusing on your gross annual salary, start with your post-tax take-home pay, also known as net pay. This is the actual amount you receive after deductions, providing a more accurate picture of your available funds.

1.2. List Your Expenses

Next, meticulously list all your monthly expenses. This includes:

- Fixed Expenses: Rent or mortgage payments, insurance premiums, loan payments, and property taxes.

- Variable Expenses: Groceries, utilities, transportation, entertainment, and dining out.

- Annual Expenses: Property taxes (if not paid monthly), insurance renewals, and subscriptions.

Remember to account for irregular expenses such as holiday shopping, car repairs, and medical bills. According to a study by the Bureau of Labor Statistics, the average American household spends a significant portion of their income on housing, transportation, and food.

1.3. Calculate Your Discretionary Income

Subtract your total monthly expenses from your net monthly income. The remaining amount is your discretionary income, which can be allocated to savings, investments, and, of course, car payments.

Example:

- Net Monthly Income: $4,500

- Total Monthly Expenses: $3,000

- Discretionary Income: $1,500

1.4. Consult Expert Advice

Consider consulting with a financial advisor for personalized advice. According to a report from the University of Texas at Austin’s McCombs School of Business, seeking expert financial guidance can lead to better financial outcomes and more informed decision-making.

Person calculating discretionary income

Person calculating discretionary income

1.5. Set Realistic Expectations

It’s crucial to be honest about your spending habits and financial priorities. Avoid inflating your income or underestimating your expenses. A realistic assessment will help you determine a comfortable car budget that doesn’t strain your finances.

By thoroughly evaluating your income and expenses, you’ll be well-prepared to determine a suitable car budget. This will not only help you avoid financial stress but also pave the way for building a secure financial future. Visit income-partners.net for more strategies on financial planning and partnership opportunities to increase your income.

2. Establishing a Car Payment Budget

Once you know your income and expenses, establish a car payment budget. Experts recommend the 20/4/10 rule: a 20% down payment, financing the car for no more than 4 years, and ensuring that total car costs (including principal, interest, and insurance) do not exceed 10% of your gross monthly income.

After thoroughly assessing your income and expenses, the next crucial step is to establish a car payment budget. Setting a realistic budget ensures that you can comfortably afford your vehicle without straining your finances. Here’s how to determine a suitable car payment budget:

2.1. The 20/4/10 Rule

A widely recommended guideline is the 20/4/10 rule, which helps you balance affordability and financial prudence:

- 20% Down Payment: Aim to put down at least 20% of the car’s purchase price. This reduces the loan amount and your monthly payments.

- 4-Year Loan Term: Finance the car for no more than four years. Shorter loan terms mean higher monthly payments, but you’ll pay less interest overall.

- 10% of Gross Monthly Income: Ensure that your total car costs (including principal, interest, and insurance) do not exceed 10% of your gross monthly income.

2.2. Calculate the 10% Threshold

Determine your gross monthly income (before taxes and other deductions). Multiply this amount by 10% to find the maximum you should spend on car-related expenses.

Example:

- Gross Monthly Income: $6,000

- Maximum Car Costs (10%): $600

This $600 should cover your monthly car payment, insurance premiums, and any other car-related expenses.

2.3. Account for All Car-Related Expenses

When setting your car payment budget, remember to include all associated costs, not just the loan payment. Key expenses to consider are:

- Loan Payment: The monthly payment towards the principal and interest of your car loan.

- Car Insurance: Premiums can vary widely based on your location, driving history, and the type of vehicle.

- Fuel Costs: Estimate your monthly fuel expenses based on your driving habits and the car’s fuel efficiency.

- Maintenance and Repairs: Set aside money for routine maintenance (oil changes, tire rotations) and unexpected repairs.

- Registration and Taxes: Factor in annual registration fees and any applicable taxes.

2.4. Use Online Calculators

Take advantage of online car affordability calculators. These tools can help you estimate your monthly payments based on the car price, interest rate, loan term, and down payment. MarketWatch provides a useful auto loan calculator to help with this.

2.5. Consider Your Credit Score

Your credit score significantly impacts the interest rate you’ll receive on your car loan. A higher credit score typically results in a lower interest rate, reducing your overall borrowing costs. Check your credit score and take steps to improve it if necessary.

2.6. Explore Financing Options

Research different financing options to find the best terms. Compare offers from banks, credit unions, and dealerships. Look for the lowest interest rate and most favorable loan terms.

2.7. Stay Within Your Comfort Zone

Ultimately, your car payment budget should align with your personal financial situation and comfort level. Avoid stretching your budget too thin, as this can lead to financial stress and difficulty meeting other obligations.

By carefully establishing a car payment budget, you can make a responsible purchase that fits comfortably within your financial means. This ensures that you can enjoy your new vehicle without compromising your financial stability. Visit income-partners.net for more insights on budgeting, financial planning, and opportunities to grow your income through strategic partnerships.

3. Factors Influencing Affordability

Several factors influence how much car you can afford. Your credit score, down payment, loan term, and interest rate all play critical roles. A higher credit score can secure a lower interest rate, making the car more affordable over the loan term. A larger down payment reduces the loan amount, also lowering monthly payments.

Understanding the myriad factors that influence car affordability is essential for making an informed decision. These elements can significantly impact your purchasing power and long-term financial stability. Let’s explore these factors in detail:

3.1. Credit Score

Your credit score is a primary determinant of the interest rate you’ll receive on your car loan. A higher credit score indicates lower risk to lenders, resulting in more favorable loan terms.

- Excellent Credit (750+): Qualifies for the lowest interest rates.

- Good Credit (700-749): Still eligible for competitive rates.

- Fair Credit (650-699): May face higher interest rates.

- Poor Credit (Below 650): Likely to encounter high interest rates and potentially require a larger down payment.

According to Experian, the average interest rate for a new car loan in Q1 2024 was significantly lower for borrowers with excellent credit compared to those with poor credit.

Actionable Tip: Check your credit report regularly and take steps to improve your score before applying for a car loan. This can include paying down debt, correcting errors on your report, and avoiding new credit applications.

3.2. Down Payment

The amount of your down payment directly affects the loan amount and your monthly payments. A larger down payment reduces the amount you need to borrow, lowering your monthly expenses and the total interest paid over the loan term.

- Benefits of a Larger Down Payment:

- Lower monthly payments

- Reduced interest costs

- Less risk of owing more than the car is worth (being “underwater” on the loan)

Example:

- Car Price: $25,000

- Down Payment:

- 10% ($2,500)

- 20% ($5,000)

- The 20% down payment reduces the loan amount by $2,500, leading to lower monthly payments and less interest paid.

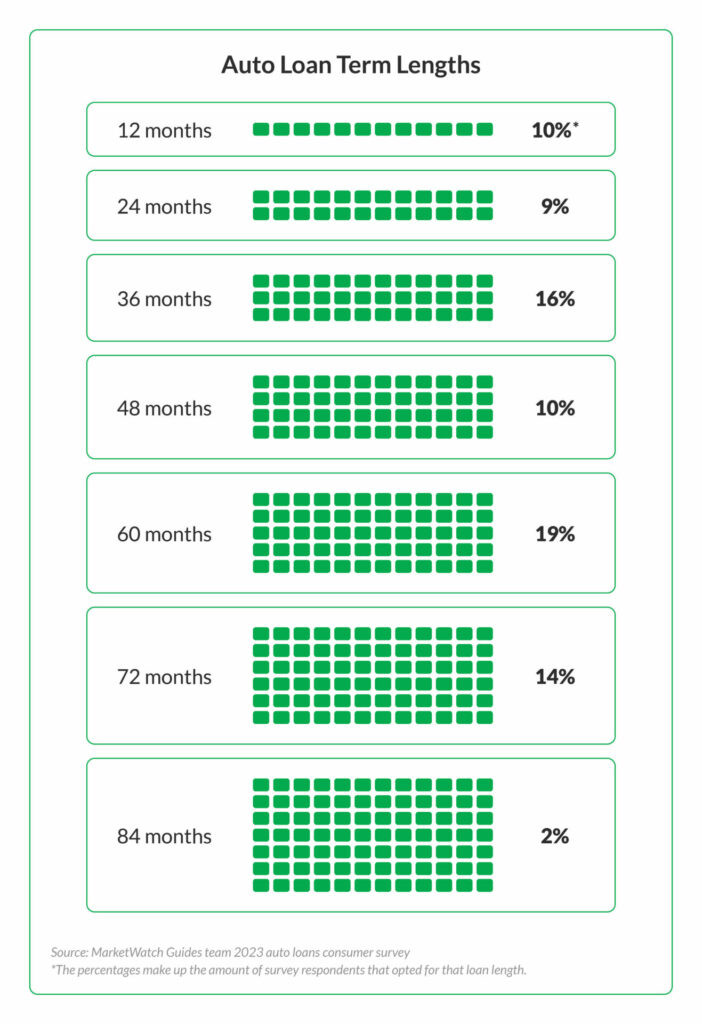

3.3. Loan Term

The loan term is the length of time you have to repay the loan. While longer loan terms result in lower monthly payments, they also mean paying more interest over the life of the loan.

- Short-Term Loans (24-48 months): Higher monthly payments but lower total interest.

- Long-Term Loans (60-84 months): Lower monthly payments but higher total interest.

Considerations:

- Choose a loan term that balances affordability with the total cost of the loan.

- Avoid excessively long loan terms (over 60 months) to minimize interest payments and the risk of being underwater on the loan.

3.4. Interest Rate

The interest rate is the cost of borrowing money, expressed as a percentage. It significantly impacts the total cost of your car loan.

- Factors Influencing Interest Rates:

- Credit score

- Loan term

- Lender (banks, credit unions, dealerships)

- Economic conditions

Actionable Tip: Shop around for the best interest rates from multiple lenders. Even a small difference in the interest rate can save you a significant amount of money over the loan term.

3.5. Additional Costs

Beyond the loan payment, consider other car-related expenses that affect affordability:

- Insurance: Premiums vary based on your age, driving history, and the type of car.

- Fuel: Calculate your monthly fuel costs based on your driving habits and the car’s fuel efficiency.

- Maintenance and Repairs: Set aside money for routine maintenance and unexpected repairs.

- Registration and Taxes: Factor in annual registration fees and any applicable taxes.

Recommendation: Estimate all car-related expenses to ensure they fit within your budget.

By carefully considering these factors, you can make a well-informed decision about how much car you can afford. This approach helps you strike a balance between enjoying your new vehicle and maintaining your financial stability. Visit income-partners.net for more strategies on managing your finances and exploring opportunities to increase your income through strategic partnerships.

4. Practical Guidelines and Rules of Thumb

Beyond the 20/4/10 rule, other guidelines can help you determine affordability. One is the 50/30/20 rule, where 50% of your income covers needs, 30% covers wants, and 20% goes to savings and debt repayment. Fit your car expenses within these percentages.

In addition to the 20/4/10 rule, several other practical guidelines and rules of thumb can help you determine how much car you can realistically afford. These rules provide different perspectives on budgeting and financial planning, ensuring a comprehensive approach to car affordability. Let’s explore these guidelines:

4.1. The 50/30/20 Rule

The 50/30/20 rule is a budgeting guideline that divides your after-tax income into three categories:

- 50% for Needs: Essential expenses like housing, utilities, groceries, transportation, and healthcare.

- 30% for Wants: Non-essential expenses such as dining out, entertainment, hobbies, and vacations.

- 20% for Savings and Debt Repayment: Contributions to savings accounts, investments, and debt repayment (including car loans).

How to Apply to Car Affordability:

- Calculate Your After-Tax Income: Determine your monthly take-home pay after taxes and other deductions.

- Allocate 50% to Needs: Ensure that your essential expenses, including housing and utilities, do not exceed 50% of your income.

- Fit Car Expenses within 20%: Allocate a portion of the 20% designated for savings and debt repayment to cover your car expenses. This includes loan payments, insurance, fuel, and maintenance.

Example:

- After-Tax Income: $5,000

- 50% for Needs: $2,500

- 30% for Wants: $1,500

- 20% for Savings and Debt Repayment: $1,000

- Car Expenses should fit within the $1,000 allocated for savings and debt repayment.

4.2. The 10% Rule for Total Car Costs

Similar to the 20/4/10 rule, another common guideline is to ensure that your total car costs (including loan payments, insurance, fuel, and maintenance) do not exceed 10% of your gross monthly income.

- Gross Monthly Income: Your income before taxes and deductions.

- Total Car Costs: Sum of all car-related expenses.

Example:

- Gross Monthly Income: $6,000

- Maximum Total Car Costs (10%): $600

4.3. The Debt-to-Income Ratio (DTI)

The debt-to-income ratio (DTI) is a financial metric that compares your total monthly debt payments to your gross monthly income. Lenders use DTI to assess your ability to manage monthly payments and repay debts.

- Calculation: DTI = (Total Monthly Debt Payments / Gross Monthly Income) x 100

- Ideal DTI: Generally, a DTI below 36% is considered healthy.

How to Apply to Car Affordability:

- Calculate Your Total Monthly Debt Payments: Include all debt payments, such as credit card debt, student loans, personal loans, and potential car loan payments.

- Calculate Your Gross Monthly Income: Determine your income before taxes and deductions.

- Calculate Your DTI: Use the formula above to calculate your DTI.

- Ensure DTI Remains Below 36%: If adding a car loan pushes your DTI above 36%, reconsider the loan amount or explore ways to reduce other debt payments.

4.4. The One-Third Rule

The one-third rule suggests that your total transportation costs should not exceed one-third of your housing costs. This rule helps ensure that your transportation expenses are proportional to your overall living expenses.

- Calculate Your Housing Costs: Determine your total monthly housing expenses, including rent or mortgage payments, property taxes, and insurance.

- Limit Transportation Costs: Ensure that your car-related expenses (loan payments, insurance, fuel, maintenance) do not exceed one-third of your housing costs.

Example:

- Monthly Housing Costs: $1,500

- Maximum Transportation Costs (One-Third): $500

4.5. Consider Future Financial Goals

When determining car affordability, consider your future financial goals, such as saving for retirement, buying a home, or starting a business. Avoid taking on a car loan that jeopardizes your ability to achieve these goals.

- Prioritize Long-Term Savings: Ensure that you continue to contribute to retirement accounts and other savings goals while making car payments.

- Avoid Depleting Emergency Funds: Do not use your emergency fund for a down payment on a car. Maintain a healthy emergency fund for unexpected expenses.

By using these practical guidelines and rules of thumb, you can gain a more comprehensive understanding of how much car you can afford. These rules help you balance your car expenses with other financial obligations and goals, ensuring long-term financial stability. Visit income-partners.net for additional resources on financial planning and strategies to grow your income through valuable partnerships.

5. Types of Vehicles to Consider

When determining how much car you can afford, consider different types of vehicles. New cars depreciate quickly, so a used car might be a more economical choice. Smaller, fuel-efficient cars can save money on gas and insurance.

When figuring out how much car you can afford, it’s wise to consider different types of vehicles. Each type comes with its own set of pros and cons, impacting your overall costs and long-term financial health. Let’s explore the various options:

5.1. New Cars

New cars offer the latest technology, safety features, and a manufacturer’s warranty, but they also come with a higher price tag and rapid depreciation.

- Pros:

- Latest features and technology

- Full manufacturer’s warranty

- Higher reliability (generally)

- Better fuel efficiency (in newer models)

- Cons:

- Higher purchase price

- Rapid depreciation in the first few years

- Higher insurance costs (typically)

Considerations:

- If you value the latest features and reliability and can afford the higher price, a new car might be a good option.

- Be aware of the depreciation hit and factor it into your long-term financial planning.

5.2. Used Cars

Used cars can be a more economical choice, as they have already undergone initial depreciation. However, they may require more maintenance and lack the latest features.

- Pros:

- Lower purchase price

- Slower depreciation

- Lower insurance costs (typically)

- Cons:

- May require more maintenance and repairs

- Lack of the latest features and technology

- Potentially lower reliability

- Limited or no warranty

Considerations:

- Used cars can be a smart choice if you’re on a budget and willing to compromise on features and technology.

- Thoroughly inspect the car and obtain a vehicle history report to assess its condition and potential maintenance needs.

5.3. Certified Pre-Owned (CPO) Cars

Certified Pre-Owned (CPO) cars offer a middle ground between new and used cars. These vehicles have been inspected and certified by the manufacturer or dealership and come with an extended warranty.

- Pros:

- Lower price than new cars

- Extended warranty

- Inspected and certified for quality

- Lower depreciation compared to new cars

- Cons:

- Higher price than non-certified used cars

- Limited selection compared to used cars

- May still require some maintenance

Considerations:

- CPO cars can be a good option if you want the peace of mind of a warranty and a certified vehicle without paying the full price of a new car.

5.4. Fuel-Efficient Cars

Fuel-efficient cars can save you money on gas and reduce your environmental impact. These cars come in various sizes and types, including hybrids and electric vehicles.

- Pros:

- Lower fuel costs

- Environmentally friendly

- Potential tax incentives (for hybrids and EVs)

- Cons:

- May have a higher initial purchase price

- Limited range (for EVs)

- Charging infrastructure limitations (for EVs)

Considerations:

- Fuel-efficient cars can be a cost-effective choice in the long run, especially if you drive frequently or live in an area with high gas prices.

- Evaluate your driving habits and needs to determine whether a hybrid or electric vehicle is right for you.

5.5. Smaller Cars

Smaller cars typically have lower purchase prices, insurance costs, and fuel consumption, making them a budget-friendly option.

- Pros:

- Lower purchase price

- Lower insurance costs

- Better fuel efficiency

- Easier to park and maneuver

- Cons:

- Less interior space

- Potentially lower safety ratings

- Less powerful engine

Considerations:

- Smaller cars can be a practical choice if you don’t need a lot of space and prioritize affordability and fuel efficiency.

By carefully considering these different types of vehicles, you can make an informed decision that aligns with your budget, needs, and preferences. Remember to research each option thoroughly and weigh the pros and cons before making a purchase. Visit income-partners.net for more insights on financial planning and strategies to grow your income through valuable partnerships, which can further expand your car-buying options.

6. Leasing vs. Buying

Decide whether leasing or buying is better for your situation. Leasing usually means lower monthly payments, but you won’t own the car at the end of the term. Buying means higher monthly payments, but you’ll own the car and can sell it later.

Deciding between leasing and buying a car is a significant financial decision that depends on your individual circumstances, preferences, and financial goals. Each option has its own set of advantages and disadvantages. Let’s explore the key considerations to help you make an informed choice:

6.1. Leasing a Car

Leasing a car involves paying for the use of the vehicle over a specified period, typically two to three years. At the end of the lease term, you return the car to the dealership.

- Pros:

- Lower Monthly Payments: Lease payments are generally lower than loan payments because you’re only paying for the depreciation of the car during the lease term.

- Lower Upfront Costs: Leasing typically requires a smaller down payment or security deposit compared to buying.

- Drive a New Car More Often: Leasing allows you to drive a new car every few years, enjoying the latest features and technology.

- Warranty Coverage: Lease terms usually coincide with the manufacturer’s warranty period, so you’re covered for most repairs.

- Cons:

- No Ownership: You don’t own the car at the end of the lease term.

- Mileage Restrictions: Leases come with mileage restrictions, and you’ll be charged extra for exceeding the limit.

- Wear and Tear Charges: You’ll be charged for excessive wear and tear on the vehicle.

- Limited Customization: You can’t customize or modify the car.

- Higher Long-Term Costs: Over the long term, leasing can be more expensive than buying, as you’re essentially paying for the car’s depreciation without ever owning it.

Considerations:

- Leasing is a good option if you want to drive a new car every few years, don’t drive a lot of miles, and don’t want to worry about maintenance and repairs.

6.2. Buying a Car

Buying a car involves taking out a loan to pay for the vehicle. Once the loan is paid off, you own the car and can sell it later.

- Pros:

- Ownership: You own the car and can keep it for as long as you want.

- No Mileage Restrictions: You can drive as many miles as you want without incurring extra charges.

- Customization: You can customize and modify the car to your liking.

- Potential for Resale Value: You can sell the car later and recoup some of your investment.

- Lower Long-Term Costs: Over the long term, buying a car can be more economical than leasing, as you eventually own the vehicle.

- Cons:

- Higher Monthly Payments: Loan payments are generally higher than lease payments.

- Higher Upfront Costs: Buying typically requires a larger down payment compared to leasing.

- Depreciation: Cars depreciate over time, reducing their value.

- Maintenance and Repairs: You’re responsible for all maintenance and repair costs after the warranty expires.

Considerations:

- Buying is a good option if you want to own a car, drive a lot of miles, and plan to keep the vehicle for many years.

6.3. Key Differences

| Feature | Leasing | Buying |

|---|---|---|

| Monthly Payments | Lower | Higher |

| Upfront Costs | Lower | Higher |

| Ownership | No | Yes |

| Mileage | Restricted | Unlimited |

| Maintenance | Mostly Covered by Warranty | Owner’s Responsibility |

| Customization | Limited | Unlimited |

| Long-Term Costs | Higher | Lower |

6.4. Make the Right Choice for You

Consider your financial situation, driving habits, and preferences when deciding between leasing and buying. If you value driving a new car every few years and don’t drive a lot of miles, leasing might be a good option. If you want to own a car, drive a lot of miles, and plan to keep the vehicle for many years, buying might be a better choice.

By carefully evaluating these factors, you can make an informed decision that aligns with your financial goals and lifestyle. Visit income-partners.net for more insights on financial planning and strategies to grow your income through valuable partnerships, which can further enhance your car-buying or leasing options.

7. Negotiating the Best Deal

Negotiating the best deal is crucial when buying or leasing a car. Research the car’s market value, get pre-approved for a loan, and be prepared to walk away if the deal isn’t right.

Negotiating the best possible deal when buying or leasing a car can save you a significant amount of money. Effective negotiation requires research, preparation, and a clear understanding of your priorities. Here are some strategies to help you negotiate the best deal:

7.1. Research the Car’s Market Value

Before you start negotiating, research the car’s market value to know what a fair price is. Use online resources like Kelley Blue Book (KBB), Edmunds, and NADAguides to determine the car’s invoice price and the average price paid in your area.

- Invoice Price: The price the dealer paid for the car from the manufacturer.

- Market Value: The average price consumers are paying for the car in your area.

Actionable Tip: Knowing the invoice price gives you an advantage in negotiations, as you know the dealer’s cost.

7.2. Get Pre-Approved for a Loan

Getting pre-approved for a car loan from a bank or credit union gives you negotiating power at the dealership. You’ll know the interest rate and loan terms you qualify for, allowing you to focus on negotiating the car’s price.

- Benefits of Pre-Approval:

- Knowing your interest rate and loan terms

- Negotiating with confidence

- Avoiding high-pressure financing tactics at the dealership

Actionable Tip: Shop around for the best interest rates from multiple lenders before getting pre-approved.

7.3. Shop Around and Get Multiple Quotes

Contact multiple dealerships to get quotes for the car you want. Let each dealer know that you’re shopping around and are looking for the best price. This can create competition among dealers, leading to better offers.

- Strategies:

- Contact dealerships online or by phone to get initial quotes.

- Visit dealerships in person to inspect the cars and negotiate in person.

- Be prepared to walk away if you’re not satisfied with the offer.

Actionable Tip: Don’t be afraid to walk away if the dealer isn’t willing to meet your price. There are plenty of other dealerships willing to earn your business.

7.4. Negotiate the Price, Not the Payment

Focus on negotiating the car’s price rather than the monthly payment. Dealers may try to focus on the monthly payment to make the deal seem more affordable, but this can hide other costs, such as a higher interest rate or a longer loan term.

- Strategies:

- Ask for the car’s out-the-door price, including all taxes and fees.

- Negotiate each component of the deal separately (price, trade-in value, financing).

- Be wary of add-ons and extras that you don’t need.

Actionable Tip: Always focus on the total cost of the car, not just the monthly payment.

7.5. Be Aware of Dealer Add-Ons and Fees

Dealers often try to add on extra products and services, such as extended warranties, paint protection, and fabric protection. These add-ons can significantly increase the cost of the car.

- Strategies:

- Carefully review the list of add-ons and fees.

- Decline any add-ons that you don’t need or want.

- Negotiate the price of add-ons if you’re interested in them.

Actionable Tip: Don’t feel pressured to buy add-ons. You can often purchase them later from third-party providers at a lower price.

7.6. Take Your Time and Be Patient

Don’t rush into a deal. Take your time to evaluate the offer and make sure you’re comfortable with it. Dealers may try to pressure you into making a quick decision, but it’s important to stay calm and patient.

- Strategies:

- Visit the dealership at the end of the month or quarter, when dealers are trying to meet sales quotas.

- Bring a friend or family member with you for support.

- Sleep on it and make your decision the next day.

Actionable Tip: The more time you spend making the right decision, the better chances you will get.

By following these negotiation strategies, you can increase your chances of getting the best possible deal on your next car. Visit income-partners.net for more insights on financial planning and strategies to grow your income through valuable partnerships, which can further enhance your car-buying options.

8. Considering Long-Term Costs

Beyond the sticker price and monthly payments, consider long-term costs like maintenance, insurance, and potential repairs. These can significantly impact the overall affordability of a vehicle.

When determining how much car you can afford, it’s crucial to look beyond the initial purchase price and monthly payments. Long-term costs, such as maintenance, insurance, and potential repairs, can significantly impact the overall affordability of a vehicle. Let’s explore these factors in detail:

8.1. Maintenance Costs

Regular maintenance is essential to keep your car running smoothly and prevent costly repairs. Maintenance costs vary depending on the make and model of the vehicle.

-

Routine Maintenance:

- Oil changes

- Tire rotations

- Fluid checks and top-ups

- Brake inspections

- Filter replacements

-

Factors Affecting Maintenance Costs:

- Vehicle make and model

- Driving habits

- Maintenance schedule

- Repair shop rates

Actionable Tip: Follow the manufacturer’s recommended maintenance schedule to keep your car in good condition and avoid major repairs.

8.2. Insurance Costs

Car insurance is a necessary expense that protects you financially in case of an accident or other covered event. Insurance costs vary depending on several factors.

- Factors Affecting Insurance Costs:

- Driving record

- Age

- Gender

- Location

- Vehicle make and model

- Coverage levels

Actionable Tip: Shop around for car insurance quotes from multiple providers to find the best rates.

8.3. Potential Repairs

Even with regular maintenance, cars can experience unexpected repairs. Planning for potential repairs can help you avoid financial stress when they occur.

-

Common Repairs:

- Brake repairs

- Engine repairs

- Transmission repairs

- Suspension repairs

- Electrical repairs

-

Strategies for Managing Repair Costs:

- Set aside an emergency fund for car repairs.

- Consider purchasing an extended warranty.

- Choose a reliable car with a good repair history.

Actionable Tip: Research the reliability ratings of different car models before making a purchase.

8.4. Fuel Costs

Fuel costs can be a significant expense, especially if you drive frequently or own a gas-guzzling vehicle.

-

Factors Affecting Fuel Costs:

- Fuel efficiency of the car

- Driving habits

- Gas prices

- Distance driven

-

Strategies for Reducing Fuel Costs:

- Choose a fuel-efficient car.

- Drive conservatively.

- Keep your tires properly inflated.

- Combine errands to reduce trips.

Actionable Tip: Consider a hybrid or electric vehicle to save on fuel costs.

8.5. Depreciation

Depreciation is the decrease in a car’s value over time. It’s an important factor to consider when buying a car, as it affects the car’s resale value.

-

Factors Affecting Depreciation:

- Vehicle make and model

- Age

- Mileage

- Condition

- Market demand

-

Strategies for Minimizing Depreciation:

- Choose a car with a good resale value.

- Keep the car in good condition.

- Limit mileage.

- Consider buying a used car.

Actionable Tip: Research the depreciation rates of different car models before making a purchase.

By carefully considering these long-term costs, you can make a more informed decision about how much car you can afford. This approach helps you avoid financial surprises and ensures that you can enjoy your vehicle without straining your budget. Visit income-partners.net for more insights on financial planning and strategies to grow your income through valuable partnerships, which can further enhance your car-buying options.

9. Utilizing Online Affordability Calculators

Online affordability calculators can provide a quick estimate of how much car you can afford based on your income, expenses, and other financial factors. These tools can help you narrow down your options and make informed decisions.

Utilizing online car affordability calculators is a great way to get a quick estimate of how much car you can realistically afford. These tools consider your income, expenses, and other financial factors to provide a personalized estimate. Here’s how to make the most of these calculators:

9.1. Understanding Car Affordability Calculators

Car affordability calculators are designed to estimate the maximum car price and monthly payment you can comfortably afford based on your financial situation. They typically ask for the following information:

- Gross Monthly Income: Your income before taxes and deductions.

- Monthly Expenses: Including rent/mortgage, utilities, credit card debt, student loans, and other recurring expenses.

- Down Payment: The amount of money you plan to put down on the car.

- Loan Term: The length of time you’ll be paying off the loan (e.g., 36, 48, 60 months).

- Interest Rate: The annual interest rate you expect to receive on the car loan.

- Trade-In Value: The estimated value of your current car if you plan to trade it in.

9.2. Finding Reliable Calculators

There are many car affordability calculators available online. Some reputable sources include:

- Bankrate

- NerdWallet

- Edmunds

- Kelley Blue Book (KBB)

Actionable Tip: Use multiple calculators to get a range of estimates and compare the results.

9.3. How to Use the Calculators Effectively

- Gather Your Financial Information: Collect all the necessary information, including your income, expenses, and credit score.

- Enter Accurate Data: Provide accurate and up-to-date information to get the most reliable estimate.

- Adjust the Variables: Experiment with different down payment amounts, loan