Individual income taxes are a crucial aspect of the financial landscape, influencing both individual prosperity and the economic vitality of nations. At income-partners.net, we help you navigate this complex world while also providing opportunities to increase your income through strategic partnerships. Let’s explore the ins and outs of individual income taxes, and how strategic partnerships can lead to financial empowerment.

1. What Exactly Are Individual Income Taxes?

Individual income taxes are taxes imposed on the earnings of individuals or households, encompassing wages, salaries, investments, and other forms of income. These taxes form a cornerstone of government revenue, funding public services and infrastructure.

In essence, individual income tax is a levy on the financial gains you make. It’s a fundamental element of how governments fund essential services.

1.1 How Individual Income Taxes Work in the U.S.

The United States employs a progressive income tax system, meaning higher earners pay a larger percentage of their income in taxes. This system is implemented at both the federal and state levels.

- Federal Income Tax: The federal income tax in the U.S. is structured around tax brackets, where different income levels are taxed at different rates. In 2024, these rates range from 10% to 37%, depending on your taxable income and filing status (single, married filing jointly, head of household).

- State Income Tax: In addition to federal income tax, most states also levy an income tax. The structure and rates of these taxes vary widely by state, with some states having a flat tax rate and others having a graduated tax system similar to the federal system. As of 2024, 43 states impose individual income taxes.

- Progressive Tax System: The progressive nature of the U.S. income tax code means that as your income increases, the percentage of your income paid in taxes also increases. This is because higher income levels fall into higher tax brackets with higher tax rates.

Example:

Let’s say you’re filing as a single individual in 2024.

- If your taxable income is $10,000, you would be taxed at a rate of 10%.

- If your taxable income is $50,000, you would be taxed at a rate of 22%.

1.2 Understanding Tax Brackets and Marginal Tax Rates

Tax brackets define the income ranges subject to specific tax rates. The marginal tax rate is the rate applied to each additional dollar of income earned above a certain threshold. It’s important to understand that your marginal tax rate doesn’t apply to all of your income, only the portion that falls within that specific tax bracket.

Imagine tax brackets as steps on a ladder. Each step represents a range of income, and each has its own tax rate. You only pay the rate associated with that step for the portion of your income that falls on it.

2024 Federal Income Tax Brackets and Rates

| Tax Rate | Single Filers | Married Filing Jointly | Heads of Households |

|---|---|---|---|

| 10% | $0 to $11,600 | $0 to $23,200 | $0 to $16,550 |

| 12% | $11,600 to $47,150 | $23,200 to $94,300 | $16,550 to $63,100 |

| 22% | $47,150 to $100,525 | $94,300 to $201,050 | $63,100 to $100,500 |

| 24% | $100,525 to $191,950 | $201,050 to $383,900 | $100,500 to $191,950 |

| 32% | $191,950 to $243,725 | $383,900 to $487,450 | $191,950 to $243,700 |

| 35% | $243,725 to $609,350 | $487,450 to $731,200 | $243,700 to $609,350 |

| 37% | $609,350 or more | $731,200 or more | $609,350 or more |

Source: Internal Revenue Service

1.3 Deductions and Credits: Reducing Your Tax Burden

Tax deductions and credits offer avenues to lower your tax liability. Deductions reduce your taxable income, while credits directly reduce the amount of tax you owe.

- Standard Deduction: A fixed amount that most taxpayers can deduct from their income, simplifying the tax process.

- Itemized Deductions: Allow taxpayers to deduct specific expenses, such as medical expenses, state and local taxes (SALT), and charitable contributions, if they exceed the standard deduction.

- Earned Income Tax Credit (EITC): A credit for low- to moderate-income workers and families, particularly beneficial for those with children.

- Child Tax Credit (CTC): A credit for taxpayers with qualifying children, providing financial relief to families.

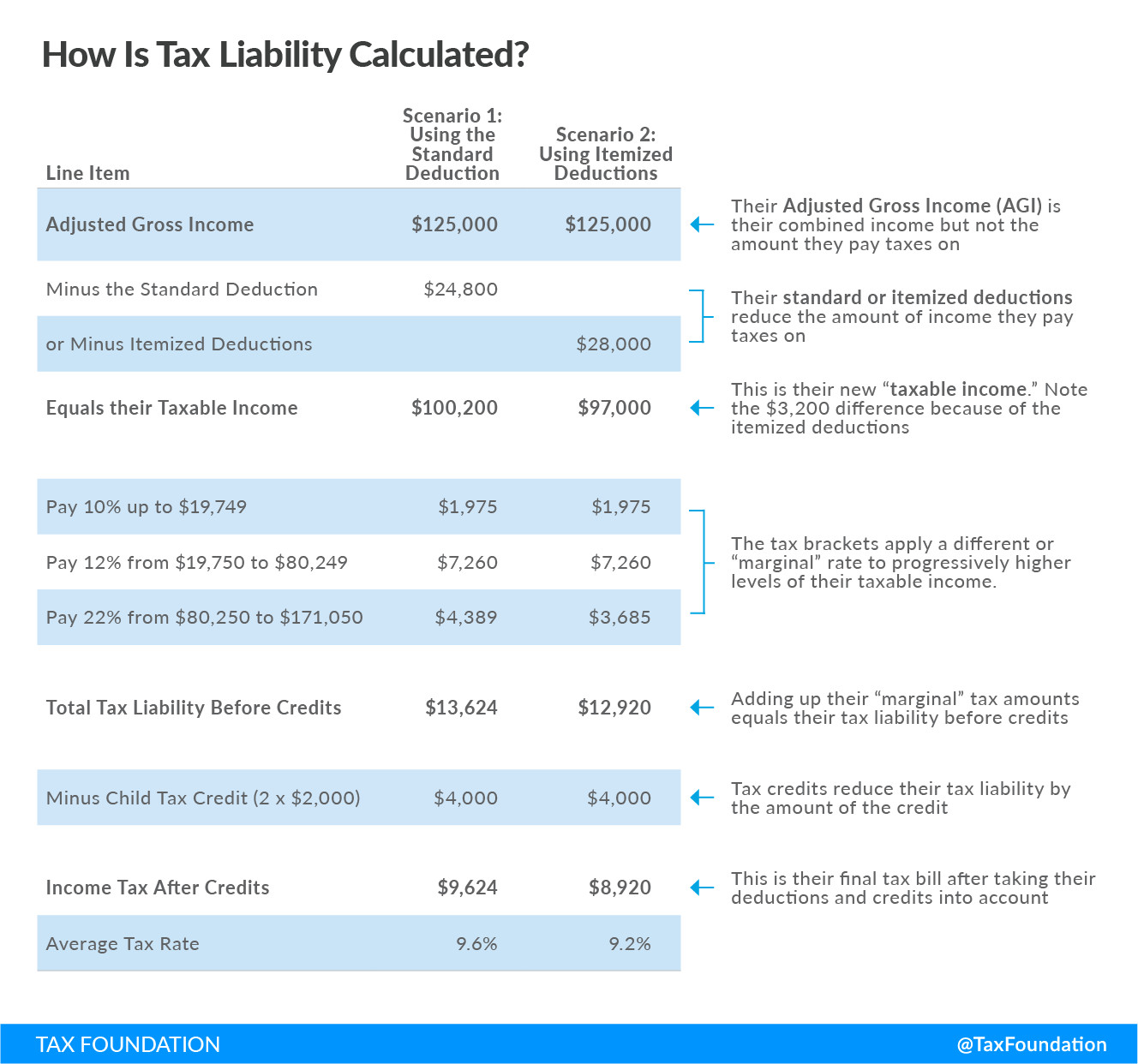

According to the Tax Foundation, a variety of deductions and credits in the tax code mean that most taxpayers don’t pay federal income taxes on all of their income.

Tax Basics – How Is Tax Liability Calculated, adjusted gross income, average tax rate, child tax credit, earned income tax credit, individual income tax, itemized deduction, marginal tax rate, standard deduction, tax credit, tax deduction, taxable income

Tax Basics – How Is Tax Liability Calculated, adjusted gross income, average tax rate, child tax credit, earned income tax credit, individual income tax, itemized deduction, marginal tax rate, standard deduction, tax credit, tax deduction, taxable income

2. Who Is Required to Pay Federal Income Tax?

Generally, if your income exceeds a certain threshold, you are required to file a federal income tax return. The specific threshold depends on your filing status, age, and whether you can be claimed as a dependent on someone else’s return. For example, in 2024, the standard deduction for a single individual is $14,600. If your income is below this amount, you may not be required to file a return.

2.1 Income Thresholds and Filing Requirements

The IRS sets specific income thresholds that determine whether you need to file a tax return. These thresholds vary depending on your filing status (single, married filing jointly, head of household, etc.) and age. Generally, if your income exceeds the standard deduction for your filing status, you are required to file a tax return.

- Single: For single filers, the threshold is generally the standard deduction amount ($14,600 in 2024).

- Married Filing Jointly: For married couples filing jointly, the threshold is twice the standard deduction amount ($29,200 in 2024).

- Head of Household: For head of household filers, the threshold is higher than for single filers but lower than for married couples.

2.2 Exceptions and Special Cases

There are certain exceptions to the general filing requirements. For example, if you are self-employed and your net earnings are $400 or more, you are required to file a tax return, regardless of your total income. Additionally, if you have certain types of income, such as Social Security benefits or unearned income (e.g., dividends or interest), you may be required to file a return even if your total income is below the standard deduction amount.

2.3 Understanding Your Filing Status

Your filing status affects your tax bracket, standard deduction, and eligibility for certain credits and deductions. Common filing statuses include:

- Single: For unmarried individuals.

- Married Filing Jointly: For married couples who file a joint tax return.

- Married Filing Separately: For married individuals who choose to file separate tax returns.

- Head of Household: For unmarried individuals who pay more than half the costs of keeping up a home for a qualifying child.

- Qualifying Widow(er): For surviving spouses who meet certain requirements.

3. The Significance of Individual Income Taxes

Individual income taxes are the U.S. government’s largest source of revenue, far outpacing corporate income taxes and payroll taxes. These funds support essential government services, including:

- Infrastructure: Roads, bridges, airports, and other public works projects.

- Education: Funding for public schools, colleges, and universities.

- Healthcare: Programs like Medicare and Medicaid that provide healthcare to seniors, low-income individuals, and people with disabilities.

- National Defense: Military spending and defense-related activities.

- Social Security: Payments to retired workers, disabled workers, and their families.

3.1 How Income Taxes Fund Government Services

Individual income taxes play a vital role in funding government services at the federal, state, and local levels. According to the Tax Foundation, individual income taxes account for a substantial portion of total tax revenue in the United States.

- Federal Level: Federal income taxes are the primary source of revenue for the U.S. government, funding a wide range of programs and services, including national defense, Social Security, Medicare, and infrastructure.

- State Level: State income taxes are a significant source of revenue for state governments, funding education, healthcare, transportation, and other state-level programs.

- Local Level: Local income taxes, such as city or county income taxes, are less common than state income taxes but can be an important source of revenue for local governments, funding local services like schools, police, and fire departments.

3.2 Comparing the U.S. to Other Countries

The U.S. relies more heavily on individual income taxes compared to the average of OECD (Organisation for Economic Co-operation and Development) countries. Individual income taxes make up a larger percentage of total tax revenue in the U.S. than in many other developed nations.

3.3 State and Local Reliance on Income Taxes

Many state and local governments also depend significantly on individual income taxes to fund their operations. The level of reliance on income taxes varies widely by state.

According to the Tax Foundation, individual income taxes comprised 22.8% of total U.S. state and local tax collections in fiscal year 2020, the latest year of available data.

4. State Income Taxes: A Closer Look

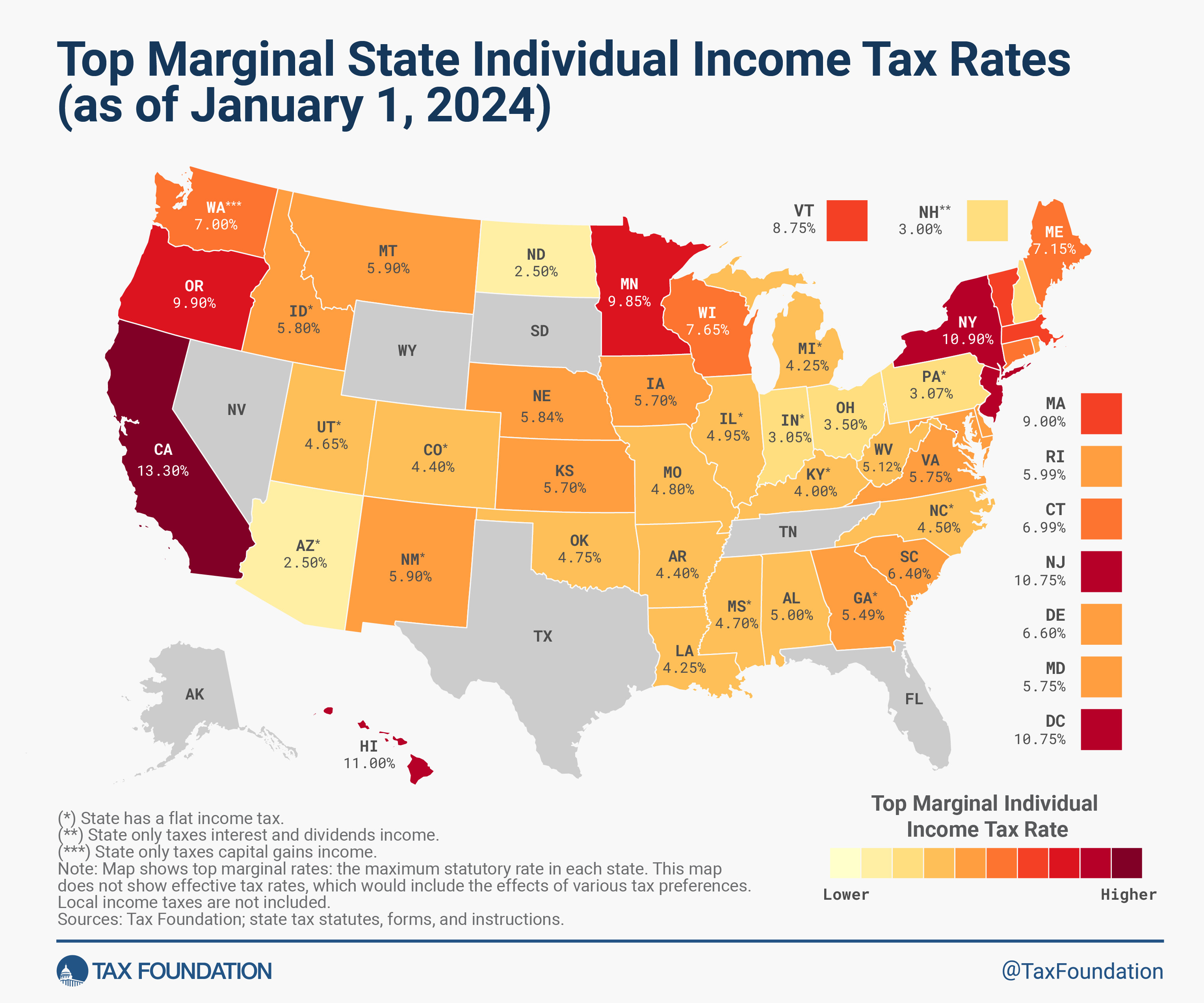

While the federal government imposes an income tax, most states do too. As of 2024, 43 states levy individual income taxes. However, the specifics vary widely.

4.1 States with and without Income Taxes

Seven states do not have individual income taxes: Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington, and Wyoming. New Hampshire taxes only dividend and interest income, while Washington taxes capital gains income.

4.2 Flat vs. Graduated Income Tax Systems

States with income taxes use either a flat tax system, where all income is taxed at the same rate, or a graduated tax system, where different income levels are taxed at different rates.

- Flat Tax: In a flat tax system, everyone pays the same percentage of their income in taxes, regardless of how much they earn.

- Graduated Tax: In a graduated tax system, tax rates increase as income increases, similar to the federal income tax system.

4.3 Key Differences in State Income Tax Policies

State income tax policies differ in several ways:

- Tax Rates: State income tax rates vary widely, from less than 1% to over 13%.

- Tax Brackets: The number of tax brackets in graduated tax systems varies by state, with some states having just a few brackets and others having many.

- Deductions and Exemptions: States offer different deductions and exemptions, such as standard deductions, personal exemptions, and deductions for specific expenses.

- Indexing for Inflation: Some states adjust their tax brackets, exemptions, and deductions for inflation, while others do not.

According to the Tax Foundation, Hawaii has the most tax brackets in the country, with 12.

2024 state income tax rates and states with no income tax

2024 state income tax rates and states with no income tax

5. Strategies to Optimize Your Income Tax Liability

Navigating individual income taxes effectively involves understanding the rules and employing strategies to minimize your tax burden.

5.1 Maximizing Deductions and Credits

Take full advantage of available deductions and credits to reduce your taxable income and tax liability. This may involve itemizing deductions instead of taking the standard deduction if your itemized deductions exceed the standard deduction amount.

- Track Expenses: Keep detailed records of your expenses throughout the year to ensure you don’t miss any eligible deductions.

- Consult a Tax Professional: Consider consulting with a tax professional to identify all available deductions and credits and ensure you are taking full advantage of them.

- Stay Informed: Stay up-to-date on changes to tax laws and regulations to ensure you are aware of any new deductions or credits that may be available to you.

5.2 Tax-Advantaged Investments

Utilize tax-advantaged investment accounts, such as 401(k)s, IRAs, and 529 plans, to save for retirement, education, and other goals while reducing your current tax liability.

- 401(k)s: Contributions to a 401(k) are typically tax-deductible, and earnings grow tax-deferred until retirement.

- IRAs: Traditional IRAs offer tax-deductible contributions, while Roth IRAs offer tax-free withdrawals in retirement.

- 529 Plans: Contributions to a 529 plan are not tax-deductible at the federal level, but earnings grow tax-free and can be used for qualified education expenses.

5.3 Strategic Business Partnerships for Income Growth

Consider forming strategic business partnerships to increase your income and potentially reduce your tax burden. Partnerships can provide access to new markets, resources, and expertise, leading to increased revenue and profitability.

- Identify Synergies: Look for potential partners whose businesses complement yours and offer synergies that can benefit both parties.

- Establish Clear Agreements: Establish clear agreements and expectations upfront to avoid misunderstandings and conflicts down the road.

- Regular Communication: Maintain regular communication with your partners to ensure the partnership is running smoothly and to address any issues that may arise.

At income-partners.net, we specialize in connecting businesses and individuals for mutually beneficial partnerships.

6. Common Mistakes to Avoid When Filing Income Taxes

Filing income taxes can be complex, and it’s easy to make mistakes that can result in penalties, interest, or missed deductions and credits.

6.1 Overlooking Deductions and Credits

One of the most common mistakes is overlooking eligible deductions and credits. Many taxpayers miss out on valuable tax breaks simply because they are not aware of them or don’t keep adequate records.

- Commonly Missed Deductions:

- Home office deduction

- Self-employment tax deduction

- Student loan interest deduction

- Medical expense deduction

- Charitable contribution deduction

- Commonly Missed Credits:

- Earned Income Tax Credit (EITC)

- Child Tax Credit (CTC)

- Child and Dependent Care Credit

- Education Credits (American Opportunity Credit and Lifetime Learning Credit)

- Energy Credits

6.2 Incorrect Filing Status

Choosing the wrong filing status can have a significant impact on your tax liability. Make sure you understand the requirements for each filing status and choose the one that is most appropriate for your situation.

- Single: Unmarried individuals who do not qualify for another filing status.

- Married Filing Jointly: Married couples who file a joint tax return.

- Married Filing Separately: Married individuals who choose to file separate tax returns.

- Head of Household: Unmarried individuals who pay more than half the costs of keeping up a home for a qualifying child.

- Qualifying Widow(er): Surviving spouses who meet certain requirements.

6.3 Math Errors and Typos

Simple math errors and typos can lead to inaccurate tax returns and potential penalties. Double-check all calculations and ensure that all information is entered correctly before submitting your return.

- Use Tax Software: Consider using tax software to help minimize the risk of math errors and ensure that all calculations are accurate.

- Review Your Return: Take the time to carefully review your tax return before submitting it to the IRS to catch any errors or typos.

- Seek Professional Assistance: If you are unsure about any aspect of your tax return, seek professional assistance from a tax preparer or accountant.

7. How Individual Income Taxes Impact Business Partnerships

Business partnerships can have a significant impact on individual income taxes for both the partners and the business.

7.1 Partnership Income and Individual Tax Returns

Partnerships are pass-through entities, meaning that the income and losses of the partnership are passed through to the individual partners and reported on their individual tax returns.

- Schedule K-1: Partners receive a Schedule K-1 from the partnership, which reports their share of the partnership’s income, deductions, and credits.

- Self-Employment Tax: Partners are subject to self-employment tax on their share of the partnership’s income.

- Deductibility of Losses: Partners may be able to deduct their share of the partnership’s losses on their individual tax returns, subject to certain limitations.

7.2 Tax Implications of Partnership Structures

The structure of a partnership can have tax implications for the partners. Different types of partnerships, such as general partnerships, limited partnerships, and limited liability partnerships, have different tax rules.

- General Partnerships: In a general partnership, all partners share in the profits and losses of the business and have unlimited liability for the debts of the partnership.

- Limited Partnerships: In a limited partnership, there are general partners who manage the business and have unlimited liability, and limited partners who have limited liability and do not participate in the management of the business.

- Limited Liability Partnerships (LLPs): In an LLP, partners have limited liability for the debts of the partnership, similar to shareholders in a corporation.

7.3 Seeking Professional Advice for Partnership Taxes

Due to the complexity of partnership taxes, it’s important to seek professional advice from a tax advisor or accountant. A tax professional can help you understand the tax implications of your partnership and ensure that you are complying with all applicable tax laws.

- Tax Planning: A tax professional can help you develop a tax plan that minimizes your tax liability and maximizes your after-tax income.

- Tax Compliance: A tax professional can help you prepare and file your partnership tax returns and ensure that you are complying with all applicable tax laws.

- Audit Representation: If your partnership is audited by the IRS, a tax professional can represent you and help you navigate the audit process.

8. The Future of Individual Income Taxes

The landscape of individual income taxes is constantly evolving, with changes to tax laws, regulations, and policies occurring regularly.

8.1 Potential Tax Reforms and Changes

Tax reform is a frequent topic of debate in the United States, and there is always the potential for changes to individual income tax laws. Potential changes could include:

- Changes to Tax Rates and Brackets: Tax rates and brackets could be adjusted, potentially leading to higher or lower taxes for certain income levels.

- Changes to Deductions and Credits: Deductions and credits could be modified or eliminated, impacting the tax liability of individuals and businesses.

- Simplification of the Tax Code: Efforts could be made to simplify the tax code, making it easier for taxpayers to understand and comply with the rules.

8.2 Economic Factors Influencing Tax Policy

Economic factors, such as inflation, unemployment, and economic growth, can influence tax policy decisions. For example, during times of economic recession, policymakers may consider tax cuts to stimulate the economy.

- Inflation: Inflation can erode the value of tax brackets and deductions, leading to higher taxes for individuals and businesses.

- Unemployment: High unemployment rates may prompt policymakers to consider tax incentives to encourage job creation.

- Economic Growth: Strong economic growth may lead to higher tax revenues, giving policymakers more flexibility to consider tax cuts or spending increases.

8.3 Staying Informed About Tax Law Updates

It’s essential to stay informed about tax law updates to ensure that you are complying with the latest rules and regulations.

- IRS Website: The IRS website is a valuable resource for tax information, including tax forms, publications, and updates on tax law changes.

- Tax Professionals: Consulting with a tax professional can help you stay informed about tax law updates and ensure that you are complying with all applicable rules.

- Tax Newsletters and Publications: Subscribing to tax newsletters and publications can provide you with timely updates on tax law changes and other important tax-related information.

9. Frequently Asked Questions (FAQs) About Individual Income Taxes

9.1 What is the difference between a tax deduction and a tax credit?

A tax deduction reduces your taxable income, while a tax credit directly reduces the amount of tax you owe.

9.2 How do I determine my filing status?

Your filing status depends on your marital status and family situation. Common filing statuses include single, married filing jointly, married filing separately, head of household, and qualifying widow(er).

9.3 What is the standard deduction?

The standard deduction is a fixed amount that most taxpayers can deduct from their income. The amount of the standard deduction varies depending on your filing status, age, and whether you are blind.

9.4 What are itemized deductions?

Itemized deductions are specific expenses that you can deduct from your income, such as medical expenses, state and local taxes (SALT), and charitable contributions.

9.5 How do I know if I should itemize or take the standard deduction?

You should itemize if your total itemized deductions exceed the standard deduction amount for your filing status.

9.6 What is the Earned Income Tax Credit (EITC)?

The Earned Income Tax Credit (EITC) is a credit for low- to moderate-income workers and families, particularly beneficial for those with children.

9.7 What is the Child Tax Credit (CTC)?

The Child Tax Credit (CTC) is a credit for taxpayers with qualifying children, providing financial relief to families.

9.8 How do I file my income taxes?

You can file your income taxes online, by mail, or through a tax professional.

9.9 What is the deadline for filing income taxes?

The deadline for filing income taxes is typically April 15th, unless it falls on a weekend or holiday, in which case the deadline is extended to the next business day.

9.10 What happens if I don’t file my taxes on time?

If you don’t file your taxes on time, you may be subject to penalties and interest.

10. Partner With Income-Partners.net for Financial Growth

Understanding individual income taxes is crucial for financial well-being, and strategic partnerships can significantly enhance your income potential. income-partners.net offers a platform to connect with like-minded individuals and businesses, fostering collaborations that drive revenue growth.

- Access a Network of Potential Partners: Connect with businesses and individuals seeking collaboration opportunities in various industries.

- Discover New Revenue Streams: Explore partnership opportunities that can diversify your income streams and increase your overall earnings.

- Leverage Expertise and Resources: Partner with individuals and businesses that possess complementary skills, knowledge, and resources to achieve mutual success.

Ready to take your income to the next level? Visit income-partners.net today to explore partnership opportunities, learn effective relationship-building strategies, and connect with potential partners in the USA. Don’t miss out on the chance to forge lucrative collaborations and unlock your full earning potential.