Building wealth on a low income is indeed possible, and it all begins with the right strategies and a determined mindset; income-partners.net provides the insights and resources to help you achieve financial success, regardless of your starting point. Focusing on smart money management, strategic investment, and consistent savings, you can create a secure financial future; start your journey towards financial independence today by exploring wealth-building strategies and income diversification techniques.

1. Adopt a Wealth-Building Mindset

Building wealth, regardless of income, starts with believing it’s achievable. Many people feel unworthy or lack the skills and opportunities to succeed; let’s transform that mindset.

The most effective way to eliminate negative thinking is to stop comparing yourself to others in different situations. As the saying goes, “If everyone threw their troubles into a pile, you’d take your own problems back.”

It’s crucial to remember that money isn’t everything, even on a personal finance blog. Earning more doesn’t necessarily mean someone is in a better position.

It’s wise to unfollow or mute anyone on social media who makes you feel inadequate or jealous. Social media often highlights the best aspects of someone’s life, making it difficult to see what’s happening behind the scenes. For example, you might see a coworker renovating their kitchen, but not the debt they incurred to do so.

Instead of focusing on what you lack, get excited about what you have. Find inspiration in stories of people like you who have built wealth on a small income, and learn from their actions.

1.1. Success Stories of Building Wealth on a Low Income

- Geoffrey Holt: A mobile home park caretaker, Geoffrey Holt, became a secret multi-millionaire despite never earning much. His frugal habits allowed him to accumulate a large amount of wealth, eventually leaving a $3.8 million estate to his hometown for community benefits.

- Theodore Johnson: A UPS worker, Theodore Johnson, died with $70 million. This frugal legend never made more than $14,000 in a year, investing early and often to build his massive nest egg.

- Sarah Wilson (Budget Girl): Sarah Wilson, also known as Budget Girl, lives in a small town in Texas, managing a single income and gradually building wealth. She shares her income, expenses, and budgeting tips on YouTube.

There are many inspiring stories of people building wealth with limited incomes. Follow them, engage with them, and implement their ideas.

Geoffrey Holt secret multimillionaire Hinsdale New Hampshire millions

Geoffrey Holt secret multimillionaire Hinsdale New Hampshire millions

2. Understand the Difference Between Saving and Investing

What is the key to accumulating wealth on a modest income?

To build wealth with any income level, it’s essential to understand the difference between saving and investing. While both are important, they serve different purposes. Saving alone isn’t enough; you need to invest to grow wealth.

Saving money protects it for specific goals. Any money not needed for spending or emergencies should be invested to grow over time.

For example, save for an emergency fund, a car, weddings, a home down payment, or other sinking fund goals. Beyond saving for specific goals, avoid holding onto too much cash.

2.1. How Inflation Erodes Cash Savings

How can inflation impact your savings and investments?

Saving your way to retirement is nearly impossible because inflation erodes savings each year. According to research from the University of Texas at Austin’s McCombs School of Business, in July 2025, continuously rising inflation could diminish the purchasing power of savings by up to 20% over a decade if not offset by investments.

Investing your money and earning interest combats this. If you have $100 in a savings account and inflation rises by 3% in a year, that $100 now has the buying power of $97.

While this may seem minor over one year, it has a significant impact over years or decades. If inflation averages 3%, your buying power will be cut in half in just 23 years.

Compound interest can help your net worth skyrocket over a long period if your money is invested. The stock market is a great place to invest long-term (specific account types are discussed below). Since the S&P 500 has returned an average of 10% over the last 100 years, investing in highly diversified index funds hedges against inflation.

However, market returns can fluctuate greatly from year to year. While investing always involves risk, you can mitigate it by adopting a long-term strategy and keeping your money invested longer.

2.2. Why You Can’t Save Your Way to Retirement

How can compound interest help you achieve your retirement goals?

The greatest asset in building wealth on a small income is compound interest. This occurs when the interest you make on your initial investment starts to earn interest itself, helping your retirement nest egg grow faster over the years. It’s the secret ingredient behind wealth building.

For example, if you’re 20 years old and make $40,000 each year after taxes, you might have $400 left each month to save or invest after expenses. Saving $400 each month for 45 years in a savings account would give you $216,000 for retirement.

However, investing that money instead could yield $3,606,180, assuming a 10% average return on investment—over 10 times what you would save in cash.

Learning to invest is essential for building wealth on a small income. Fortunately, it’s not as daunting as it seems.

2.3. Risks of Losing Money in the Stock Market

What are the potential risks of investing in the stock market, and how can they be mitigated?

Investing in the stock market involves risks. Market fluctuations, economic downturns, and company-specific issues can lead to losses. However, these risks can be mitigated through diversification, long-term investment strategies, and continuous education. Diversifying investments across different sectors and asset classes reduces the impact of any single investment performing poorly. A long-term approach allows time for recovery from market downturns.

Chances of losing money in stock market

Chances of losing money in stock market

3. Build An Emergency Fund

Why is an emergency fund crucial for financial stability?

Unexpected costs can disrupt your finances. Creating an emergency fund protects you from going into debt or dipping into other savings when unexpected events occur.

You’ll also enjoy more peace of mind knowing you can weather whatever life throws your way. According to economists, saving just $2,467 can cover most surprises. Aim to save 3-6 months’ worth of expenses for a fully funded emergency fund.

3.1. Where to Stash Your Emergency Savings

What is the best type of account for storing an emergency fund?

Don’t stash your emergency savings in a regular bank account where fees can erode your money and interest rates won’t outpace inflation. Instead, open a High Yield Savings Account (HYSA) to earn up to 10x the national average in interest and avoid heinous fees charged by big banks.

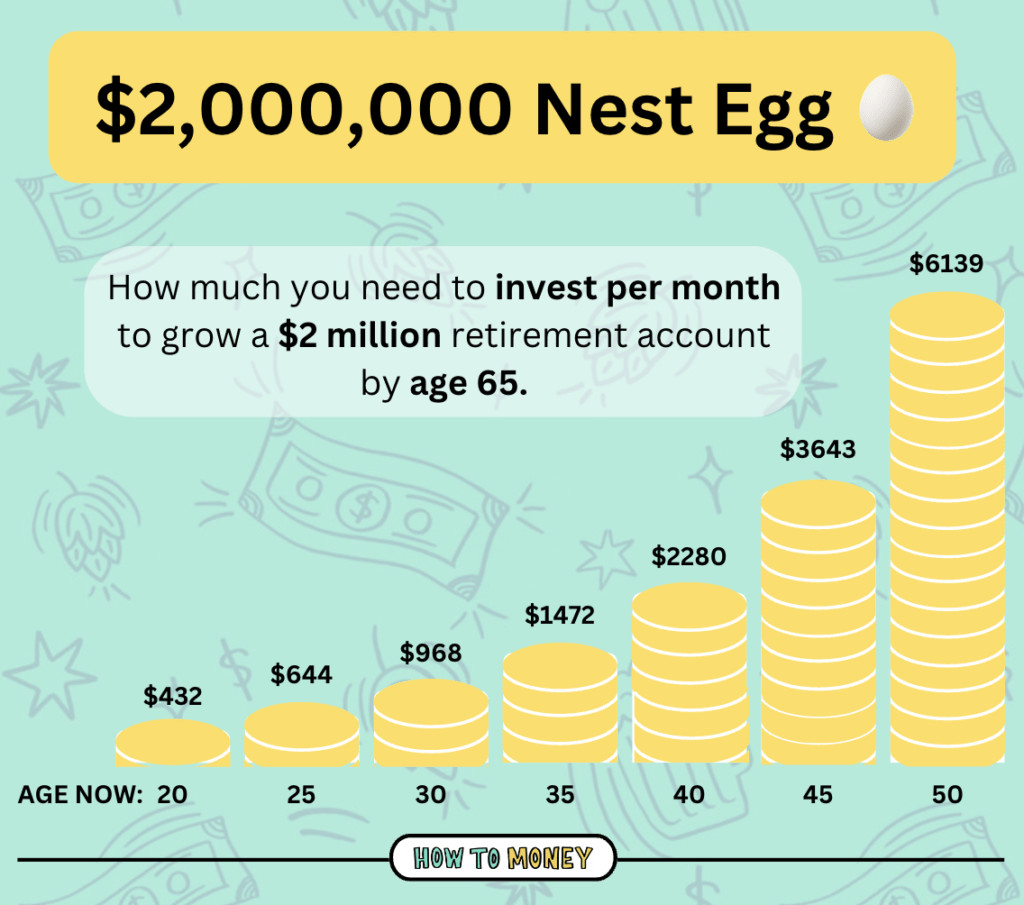

4. Start Investing Early

Why is starting to invest early a critical factor in building wealth?

Time is your biggest advantage when building wealth on a small income. Saving $1 now can be more powerful than saving $100 later.

The earlier you start, the less you need to save each month to retire comfortably.

For example, if you start investing at 20, aiming for $2 million in retirement, you’ll need to invest approximately $432 per month. Waiting until age 40 means you’ll need to invest about $2,280 each month to retire with the same amount.

4.1. Maximizing Investment Growth Over Time

How does the timing of investment impact the final retirement nest egg?

Investing early maximizes the power of compound interest, allowing your money to grow exponentially over time. The longer your investment horizon, the more significant the impact of early contributions. Starting early also allows you to take advantage of market fluctuations, buying low and selling high over the long term. This strategy can lead to substantial gains, even with smaller initial investments.

4.2. The Impact of Starting Late on Investment Goals

What are the consequences of delaying investment until later in life?

Delaying investment until later in life means needing to contribute significantly more each month to reach the same retirement goals. This is because you have less time for compound interest to work its magic. Starting late also means potentially missing out on valuable market opportunities and the benefits of long-term growth.

4.3. Best Accounts to Start Investing With

What are the best investment accounts to maximize your returns and minimize taxes?

Start with tax-advantaged accounts to lower your taxes now or later. These accounts provide significant tax benefits.

4.3.1. 401(k) Plans

What are the advantages of contributing to a 401(k) plan, especially with an employer match?

If your employer offers a 401(k), take advantage of it, especially if they offer an employer match. An employer match is essentially free money your employer contributes on your behalf towards retirement.

Neglecting a 401(k) with an employer match is a cardinal investing sin. You’re leaving money on the table, and with a low income, every penny counts.

You can contribute up to $23,000 annually into your 401(k). These contributions decrease your taxable income, saving you money now. You’ll pay taxes on withdrawals in retirement.

If you don’t have a 401k consider asking your boss or business owner to set one up. Human Interest helps businesses set up easy and affordable retirement plans for their employees. It never hurts to ask!

Company-sponsored retirement plans are a win/win, as you’ll likely stay longer if they offer these benefits.

4.3.2. Roth IRA

What are the tax benefits of a Roth IRA, and how does it differ from a 401(k)?

If you don’t have access to a 401(k), start by contributing to a Roth IRA.

Roth IRAs are excellent because you contribute with dollars you’ve already paid tax on. Then, you won’t pay any tax on withdrawals in retirement.

You can contribute up to $7,000 into a Roth IRA each year (2024 limits). If you’re over 50, you can use “catch-up contributions” to contribute an extra $1,000 each year.

4.4. Pay Yourself First

Why is paying yourself first an effective strategy for saving and investing?

Instead of saving whatever is left at the end of the month, prioritize saving and investing. When you get paid, contribute to your retirement accounts right away. Think of retirement investments and savings goals as bills to be paid at the first of every month.

If you make transfers before paying other bills and before discretionary spending, you’ll find a way to live off what’s left.

Waiting until the end of the month to save is a mistake. If you don’t prioritize savings and investing, you’ll likely have less money left over. Prioritize your financial future instead of saving just the “scraps.”

4.5. The Power of Small Amounts

How can small, consistent contributions lead to significant wealth accumulation over time?

Even if you can only spare a few dollars, every dollar counts when building wealth on a small income. When you start contributing can sometimes be more important than how much you invest.

For example, contributing $50 each month between 18 and 28, then switching jobs at 28 and contributing $400 each month after that, can result in $1,165,299 by age 65 (assuming an 8% annual return).

Waiting until 28 to start investing would leave you with only $1,009,981. Those seemingly small $50 per month contributions make a $150,000 difference by retirement.

It’s essential to start contributing now, even if it’s a tiny amount, as those few dollars can add up to thousands in retirement.

Time to build a m nest egg by age

Time to build a m nest egg by age

5. Increase Your Savings Rate

Why is increasing your savings rate crucial for wealth accumulation, regardless of income?

To build wealth, spend less than you earn and invest the difference each month. If you’re spending more than you make, you’ll never increase your net worth.

While it’s more difficult on a small income, it’s possible to slim down expenses to maintain a healthy savings rate. Aim to save 15-20% of your post-tax income each month towards debt payments, retirement contributions, or savings.

5.1. Savings Rate and Wealth Accumulation

How does a consistent savings rate impact long-term wealth accumulation?

A consistent savings rate is essential for long-term wealth accumulation. By regularly saving and investing a portion of your income, you benefit from compound interest and build a substantial nest egg over time. The higher your savings rate, the faster your wealth grows. Even small increases in your savings rate can make a significant difference over the long term.

5.2. Making a Budget

Why is budgeting an essential tool for increasing your savings rate?

Most people underestimate their expenses, preventing them from saving. Budgeting helps you stay on top of your expenses.

If you’re working with a smaller income, use the 50/30/20 budgeting method, allocating 50% of your income to needs, 30% to wants, and 20% to savings, including investing, saving, and paying off debt.

Budgeting is also a great way to track your expenses. It’s nearly impossible to manage money well if you don’t know where it’s going. Tracking expenses shows you where you’re spending the most, helping you cut back on purchases that don’t necessarily make you happier.

50 30 20 budget

50 30 20 budget

5.3. Negotiate Your Bills

How can negotiating bills free up more money for saving and investing?

Negotiating your bills is an easy way to free up money for investing. Service providers often raise prices for long-term customers without offering anything in return. Advocate for yourself by calling and asking for a discount.

Set a date to call your cable, internet, phone, and insurance providers and ask if there are any new customer offers you can take advantage of. If the representative can’t help you, ask to speak to the customer retention department.

Be willing to walk away and switch providers if they deny your requests. Although it might seem like a major pain, it’s usually less of an inconvenience than you think, and the savings can be significant. Switching from a major phone company to a budget MVNO can save you hundreds of dollars each year that you can use to bolster your savings.

5.4. Cancel Subscriptions

What is the financial impact of unused subscriptions, and how can you manage them effectively?

While subscriptions can add value, the problem comes when you keep paying for subscriptions you don’t use consistently.

The average consumer spends $219 on subscriptions each month. While not entirely against subscriptions, it can be wasteful if you’re paying for services you don’t use often.

Instead, sign up for subscriptions when you actually plan on using them. For example, if a new season of your favorite show drops on Hulu, subscribe, watch the show, and then cancel it until another show you’d like to watch premieres.

Limiting subscriptions to 2-3 at a given time can help you save hundreds every year. Schedule a subscription audit every few months to track those sneaky subscriptions that may be draining your bank account.

5.5. Change Your Lifestyle

How can significant lifestyle changes impact your ability to build wealth?

Making significant lifestyle changes can dramatically cut your budget. For example, you could save approximately $9,282 each year by ditching one of your family cars or make extra money by renting out a room in your home.

While not everyone can make major changes immediately, these bigger moves will have the most significant impact on your ability to build wealth.

5.6. Working Towards Earning More

How can increasing your income, even by small increments, impact your wealth-building potential?

Maximizing your income is crucial. Every small bump in pay can free up funds to grow your wealth. Even switching jobs to earn 10% more can significantly impact your bottom line.

For example, earning $35,000 each year and switching jobs for a 10% raise means an extra $3,500 that year before taxes. Saving half of that each year and investing it into a Roth IRA can mean an extra $453,000 at retirement if you let it stay invested for forty years.

Consider asking for a raise, switching jobs for a more significant pay bump, or starting a side hustle. You could also consider switching industries or furthering your education to make more progress in your career. income-partners.net offers resources and support for those looking to enhance their career prospects and increase their earnings.

Side hustle ideas

Side hustle ideas

6. Avoid These Wealth Killers

How can avoiding certain financial pitfalls protect and enhance your wealth-building efforts?

Protect your savings by avoiding these wealth killers at all costs.

6.1. High-Interest Debt

What is the impact of high-interest debt on wealth accumulation, and how can you avoid it?

Compound interest can work against you when it comes to high-interest debt.

High-interest rates make it difficult to escape debts like credit card debt, personal loans, and payday loans. Pay off these debts as quickly as possible and avoid them in the future.

If you want to build wealth on a small income but are carrying high-interest debt, create a debt payoff plan and stick to it.

6.2. Cars Are a Money Pit

How does car ownership impact your finances, and what are some strategies to reduce car-related expenses?

Car ownership involves hidden costs. The average monthly car payment for a new car is $725, putting a huge dent in your budget. Reducing car expenses allows you to put those dollars into wealth building instead.

You don’t need a fancy new car, especially if you’re trying to grow your wealth on a low income.

There are affordable and reliable used cars for under $10,000. Purchasing a used car means you’re less likely to stress about small dings, dents, and scratches.

Find ways to reduce your transportation expenses, whether by walking to run errands, selling a more expensive car for a more affordable one, or ditching one of your cars altogether. Living without a car isn’t hard if you live in a walkable suburb or work from home.

6.3. Big Homes Slow Financial Progress

How can the size and cost of your home impact your ability to build wealth?

While homeownership can be a smart investment, it’s not always the wisest financial choice. Be cautious when choosing your housing if you’re working with a small income. Buying a home might stretch you too much financially, leading you to become house poor.

Many homebuyers forget to factor in the hefty costs of home maintenance, which can strain your finances.

If you want to buy a home, house hacking can help, buying a home to live in and renting out a portion of it to reduce mortgage costs. You enjoy the benefits of homeownership while saving more for the future.

6.4. Risky Investing

What are the risks associated with risky investing strategies, and how can you invest wisely?

There’s a right and wrong way to invest. Protect your investments by avoiding stock picking or gambling with crypto.

Stock pickers seldom outperform the S&P 500, a basic index fund. Out of $2,132 actively managed funds (groups of professional stock-pickers), not a single one beat their index benchmark!

Luckily, there’s an easier way to invest that guarantees your fair share of growth in the stock market: investing in broad, low-cost index funds.

When you invest within your 401(k) or IRA, invest in low-cost index funds made up of many individual companies, spreading your wealth across multiple baskets.

Some companies will flop, causing you to lose money, but others (most) will be extremely successful, and you’ll reap the benefits.

6.5. Inflation

How does inflation impact your purchasing power, and what strategies can you use to protect your wealth?

Inflation impacts your buying power year over year. Hedge against inflation by investing any savings beyond your emergency fund and short-term savings goals, like a home down payment or car.

7. Use Tax-Advantaged Accounts

Why is it important to utilize tax-advantaged accounts when building wealth?

Tax-advantaged accounts were created to help people with smaller incomes, as the majority of Americans need more motivation to save for retirement.

Investing in a 401(k) or Traditional IRA can lower your upfront taxable income, meaning you’ll have more money to invest now.

Deferring taxes helps your money compound more quickly. Remember that you’ll have to pay taxes when you withdraw this money in retirement, since you deferred tax when you contributed.

If you have a low income and are in the 10% or 12% tax bracket, stick with a Roth IRA, paying tax on that income now but withdrawing it in retirement entirely tax-free. Because you’ll likely be in a lower tax bracket now than in retirement, you could save money overall when it comes to taxes.

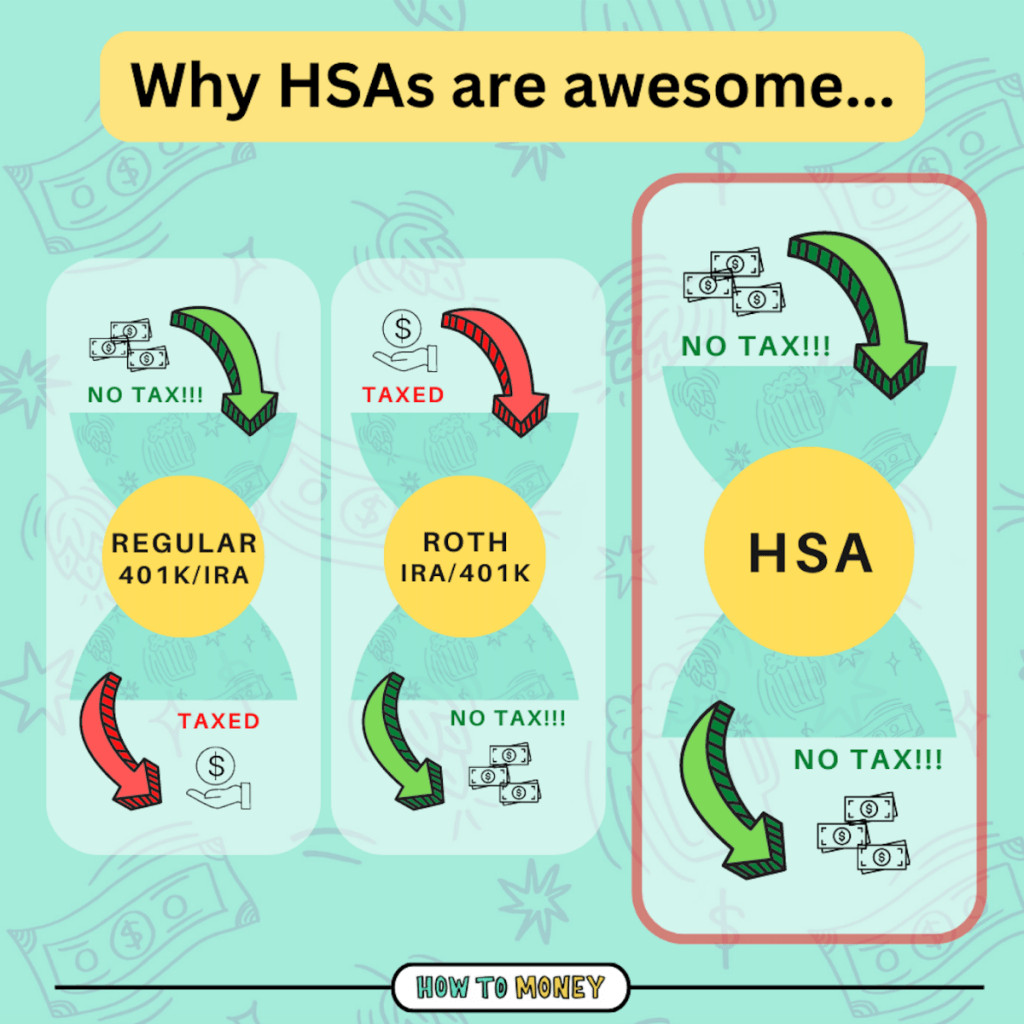

Another awesome account is the Health Savings Account (HSA), with a triple tax advantage: contributions are tax-deductible upfront, and there is no tax when you withdraw the funds later for qualified health expenses.

If you have a low income, check if you qualify for the Savers Tax Credit. If you contribute to your retirement accounts, the government might reduce your taxes for investing.

Tax advantages retirement accounts

Tax advantages retirement accounts

8. Automate Everything

How can automating your finances streamline your wealth-building process?

Automating your finances helps accelerate your wealth-building progress. This removes the need to physically move money to savings and contribute to your investment accounts. Out of sight, out of mind!

After tackling the low-hanging financial fruit, automation is the next step, ingraining wealth-building habits into your routine, so it’s one less thing to stress about.

We want finances to take up less mental space as you go about your daily life. Saving for your future and building wealth will become second nature, as long as you put in the hard work upfront and build consistency.

9. Beware of Lifestyle Creep

What is lifestyle creep, and how can you prevent it from undermining your wealth-building efforts?

As your income increases, it’s important not to fall victim to lifestyle creep, which is spending more as you earn more.

For example, if someone gets a $5,000 pay raise, they might spend $5,000 on a vacation that year, resulting in a loss after taxes. They may grow accustomed to spending that same money and taking equally great vacations every year for the rest of their lives.

Consumers are likely to start spending more even if their income and expenses remain the same because as their wealth increases and their portfolio grows, they feel more financially secure, known as the “Wealth Effect.”

To combat this, continue to track your expenses and notice any consecutive months where there is increased spending. It’s OK to spend a little more as your income increases, just make sure you’re saving more, too!

The ultimate win is increasing your income AND keeping your expenses in check, which will help you build wealth at an accelerated pace.

FAQ: Building Wealth on a Low Income

1. Is it really possible to build wealth on a low income?

Yes, it is absolutely possible. Building wealth depends more on money management skills and consistent habits than on the size of your income.

2. What is the first step to building wealth on a low income?

The first step is to change your mindset and believe that it is possible. Inspiration from success stories can help reinforce this belief.

3. What is the difference between saving and investing?

Saving is protecting money for specific short-term goals, while investing is growing money over time, primarily to outpace inflation and achieve long-term financial goals.

4. Why is it important to have an emergency fund?

An emergency fund protects you from going into debt or dipping into other savings when unexpected expenses arise. It provides peace of mind and financial stability.

5. How early should I start investing?

Start investing as early as possible. Time is your biggest advantage, allowing compound interest to work its magic.

6. What are the best accounts to start investing with?

Start with tax-advantaged accounts like 401(k) plans and Roth IRAs to maximize tax benefits and long-term growth.

7. What does it mean to pay yourself first?

Paying yourself first means prioritizing savings and investments by setting aside money as soon as you get paid, rather than waiting to see what’s left at the end of the month.

8. How can I increase my savings rate?

Increase your savings rate by making a budget, negotiating bills, canceling unused subscriptions, making lifestyle changes, and working towards earning more.

9. What are some common wealth killers to avoid?

Avoid high-interest debt, unnecessary car expenses, overspending on housing, risky investing, and the negative impacts of inflation.

10. What is lifestyle creep, and how can I avoid it?

Lifestyle creep is the tendency to spend more as you earn more. Avoid it by continuing to track your expenses and ensuring your savings rate increases along with your income.

While much traditional financial advice caters to average or high earners, you don’t need a six-figure income to grow substantial wealth. Money management is far more important than the zeros on someone’s paycheck.

By incorporating frugal habits into your daily routine, spending less than you earn, and investing the difference, you can build wealth on a small income. Remember, time, consistency, and compounding returns are your best allies.

Ready to take control of your financial future? Visit income-partners.net today to discover more strategies, find resources, and connect with experts who can help you build wealth, no matter your income level. Start building your path to financial freedom now!