Does Household Income Include Boyfriend? Yes, generally, when determining eligibility for programs like Medicaid or CHIP, a boyfriend’s income can be considered part of the household income if you file taxes together or if he is considered a part of your family unit. Understanding these rules is crucial for accurately reporting your income and navigating the complexities of eligibility requirements. Explore income-partners.net for expert insights and partnership opportunities that can help you navigate income-related decisions.

Navigating the complexities of household income can be challenging, especially when considering the financial implications of various relationships. IncomePartners.net offers expert guidance and partnership opportunities to help you understand and optimize your financial strategies.

1. Defining Modified Adjusted Gross Income (MAGI) for Medicaid and CHIP

What exactly is MAGI, and how does it play a role in determining eligibility for Medicaid and CHIP?

MAGI, or Modified Adjusted Gross Income, is a specific methodology utilized to ascertain income for Medicaid or CHIP eligibility, anchored in tax definitions of both income and household. It does not consider assets but primarily focuses on income.

Understanding MAGI is crucial for accurately determining your eligibility for Medicaid and CHIP. According to research from the University of Texas at Austin’s McCombs School of Business, in July 2025, accurate income assessment is key to accessing vital healthcare programs. This methodology aligns income definitions for Medicaid, CHIP, and premium tax credits but varies in rules for determining household composition.

1.1 The Relevance of MAGI

Why is MAGI important, and how does it affect various individuals and families?

MAGI’s importance lies in its standardized approach to income assessment for healthcare eligibility.

- Standardization: It provides a uniform method for determining income eligibility.

- Healthcare Access: Ensures fair access to Medicaid and CHIP based on income levels.

- Tax Alignment: Aligns with tax definitions, simplifying income reporting.

1.2 Income Calculation Under MAGI

What types of income are considered under MAGI rules?

MAGI includes various forms of income, aligning with tax definitions to provide a comprehensive assessment.

| Income Type | Inclusion in MAGI |

|---|---|

| Wages | Included in MAGI, reflecting earned income. |

| Salaries | Considered as part of gross income. |

| Investment Income | Dividends, interest, and capital gains are included. |

| Business Income | Revenue from self-employment or businesses, minus expenses. |

| Retirement Distributions | Distributions from retirement accounts, such as 401(k)s and IRAs, are counted. |

| Social Security Benefits | Included, especially if they are taxable. |

This comprehensive approach ensures that all relevant income sources are considered when determining eligibility for healthcare programs.

2. MAGI Rules and Their Application

To whom do the MAGI rules apply, and which Medicaid categories are affected?

MAGI rules apply universally across all states for specific Medicaid eligibility categories, irrespective of Medicaid expansion decisions.

These categories include:

- Parents and caregiver relatives

- Children

- Pregnant women

- The adult expansion group

It is vital to note that pre-existing rules for income and household assessment continue to apply to the elderly, disabled, and children in foster care.

2.1 State Implementation of MAGI Rules

How do states implement MAGI rules, and what flexibilities do they have?

States implement MAGI rules with some flexibility, particularly concerning age limits and the treatment of pregnant individuals within a household.

- Age Limit: States may extend the age limit to 21 for full-time students.

- Pregnant Individuals: States have options to count a pregnant person as one, two, or one plus the number of expected children.

2.2 Understanding Household Rules

How does Medicaid determine who is included in a household?

Medicaid determines household composition based on an individual’s plan to file a tax return, regardless of actual filing. It also doesn’t necessitate prior federal income tax return filings.

For each applicant, Medicaid assesses their planned status as:

- Tax filer

- Tax dependent

- Neither a tax filer nor a dependent

An individual’s intended tax filing status dictates the Medicaid household rules applied for household determination.

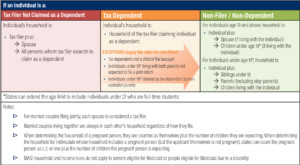

MAGI Rules for Determining Medicaid and CHIP Households

MAGI Rules for Determining Medicaid and CHIP Households

3. Medicaid vs. Premium Tax Credit Household Rules

How do Medicaid and premium tax credit household rules differ, and what are the key distinctions?

Medicaid and CHIP households are defined by family, tax relationships, and living arrangements. While tax filing influences Medicaid household rules, it doesn’t always dictate household composition. Conversely, premium tax credit household rules rely solely on tax relationships.

Key differences:

- Individual Assessment: Medicaid assesses household size and composition separately for each member.

- Tax Unit: Premium tax credits treat all members of a tax unit as a single household.

- State Options: Medicaid offers states flexibility in defining households, while premium tax credits are federally standardized.

3.1 Implications of Differing Rules

What are the implications of these differing rules for families?

The differing rules can lead to variations in household size and eligibility for family members, even when filing taxes together.

| Aspect | Medicaid | Premium Tax Credit |

|---|---|---|

| Household Assessment | Individual assessment based on tax status and living arrangements. | Unified assessment based on tax relationships. |

| Household Size | May vary among family members. | Consistent across all members of a tax unit. |

| Rule Determination | Influenced by state-specific options. | Federally standardized rules. |

| Example Scenario | A family of three might have varying household sizes for Medicaid purposes. | All members are treated as one household for tax credits. |

3.2 Medicaid Household Determination

How does Medicaid determine household membership?

Medicaid determines household membership based on an individual’s planned tax filing status, irrespective of actual filing. This status dictates the applicable household rules.

Individuals are classified as:

- Tax filers

- Tax dependents

- Neither tax filers nor dependents

This classification is pivotal in applying the appropriate Medicaid household rules.

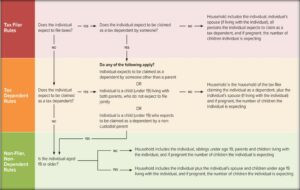

How to Determine An Individual’s Medicaid Household

How to Determine An Individual’s Medicaid Household

4. Household Rules for Tax Filers

What are the specific household rules for individuals who file taxes?

For tax filers who claim their own exemption and cannot be claimed as a tax dependent, the household includes the filer, their spouse (if filing jointly), and all claimed tax dependents.

This rule is straightforward:

- Tax Filer + Spouse (if filing jointly) + Tax Dependents = Household

4.1 Examples of Tax Filer Households

Could you provide examples to illustrate these rules?

- Example 1: John files taxes, claims his wife and two children as dependents. His Medicaid household includes himself, his wife, and his two children.

- Example 2: Sarah files taxes jointly with her husband and claims one child as a dependent. Her Medicaid household includes herself, her husband, and their child.

4.2 Importance of Accurate Filing

Why is accurate tax filing crucial in determining Medicaid eligibility?

Accurate tax filing is vital because it directly influences the determination of household composition and, consequently, Medicaid eligibility. Inaccurate filing can lead to incorrect eligibility assessments and potential complications.

5. Household Rules for Tax Dependents

What are the household rules for individuals who are claimed as tax dependents?

For tax dependents, the household mirrors that of the tax filer claiming them, with three key exceptions where the non-filer rule applies.

These exceptions are:

- Individuals expecting to be claimed by someone other than a parent

- Individuals under 19 living with parents not filing jointly

- Individuals under 19 claimed by a non-custodial parent

5.1 Exceptions to Tax Dependent Rules

Why are these exceptions in place?

These exceptions ensure fair and accurate household assessments for specific situations.

- Non-Parent Claimants: Prevents misrepresentation when a non-parent claims a dependent.

- Non-Joint Filing Parents: Accounts for separate households within the same residence.

- Non-Custodial Parents: Addresses dependencies in separated family structures.

5.2 Non-Filer Rule Application

How does the non-filer rule apply to these exceptions?

The non-filer rule applies to these exceptions to provide a more accurate representation of the individual’s household. This ensures that the individual’s actual living situation and family relationships are considered.

6. Household Rules for Non-Filers and Non-Dependents

What are the household rules for individuals who neither file a tax return nor are claimed as a tax dependent?

Household rules for non-filers and non-dependents differ based on age:

- Adults (19+): The household includes the individual, spouse (if living together), and children under 19.

- Minors (Under 19): The household includes the individual, siblings under 19, children of the individual, and parents living with them.

6.1 Implications for Young Adults

How do these rules affect young adults who are neither filers nor dependents?

For young adults, these rules can impact their Medicaid eligibility based on their living situation and family relationships. It accounts for scenarios where young adults live with their spouses and children, ensuring they are appropriately included in the household.

6.2 Household Composition for Minors

How does Medicaid determine the household size for minors under these rules?

For minors, the household composition includes siblings, children, and parents, reflecting the interconnected nature of their living situations. This ensures that all relevant family members are considered in the Medicaid eligibility assessment.

7. Adjustments to Household Rules

Are there any adjustments to the three main rules based on people’s tax filing status?

Yes, adjustments are made in specific situations:

- Married couples living together are always included in each other’s household, irrespective of filing status.

- Family size adjustments are necessary for pregnant individuals, counting them as themselves plus the expected number of children.

7.1 Married Couples Filing Separately

How does Medicaid treat married couples who file taxes separately?

Married couples living together are always considered part of the same household, regardless of whether they file taxes jointly or separately.

7.2 Adjustments for Pregnancy

How does pregnancy affect household size determination?

When determining the household size of a pregnant person, they are counted as themselves plus the number of children they are expected to deliver. This ensures that the unborn child is considered in the Medicaid eligibility assessment.

8. State Options in Implementing MAGI

What options do states have in implementing MAGI rules, and how do these options affect eligibility?

States have flexibility in two key areas:

- Extending the age limit for students to 21

- Counting pregnant individuals in various ways

These options can significantly impact Medicaid eligibility, providing states with the means to tailor their programs to specific populations.

8.1 Extending Age Limits

How does extending the age limit to 21 affect students?

Extending the age limit to 21 allows more full-time students to be included in their parents’ household, potentially increasing their access to Medicaid benefits.

8.2 Counting Pregnant Individuals

What are the different ways states can count pregnant individuals?

States can count pregnant individuals as one, two, or one plus the number of children they are expecting. This flexibility allows states to address the varying needs of pregnant individuals and their families.

9. Married Couples and Separate Households

Are married couples who file taxes separately considered to be in separate households?

Generally, no. Married couples who live together are always considered part of the same household, regardless of their tax filing status. However, if they do not live together, they are treated as separate households.

9.1 Living Arrangements Matter

Why does living arrangement play such a crucial role?

Living arrangement is critical because it reflects the actual financial and familial interdependencies between individuals. Couples living together generally share resources and responsibilities, justifying their inclusion in the same household.

9.2 Implications for Medicaid Eligibility

How does this rule affect Medicaid eligibility for married couples?

This rule ensures that married couples living together are evaluated as a single economic unit, providing a more accurate assessment of their Medicaid eligibility.

10. Non-Married Parents Living Together

How does Medicaid determine the household size of family members when the parents live together but are not married?

If both non-married parents file taxes, each parent’s Medicaid household includes themselves and anyone they claim as a dependent on their tax return. A child under 19 living with non-married parents and claimed as a dependent by one parent falls under the non-filer rule.

10.1 Applying Tax Filer and Non-Filer Rules

How do these rules interact in determining household size?

The tax filer rule applies to the parents, while the non-filer rule applies to the child, ensuring a comprehensive assessment of the family’s household size for Medicaid purposes.

10.2 Example Scenario

Could you provide an example to illustrate this scenario?

- Dan and Jen live with their two children, Drew and Mary. They are not married and file separate returns. Jen claims Drew and Mary as dependents. Dan claims no dependents.

| Filing Status | Counted in Household | Household Size | Medicaid Rule Applied |

|---|---|---|---|

| Dan | Jen | Drew | |

| Dan (Tax filer) | X | ||

| Jen (Tax filer) | X | X | X |

| Drew (Dependent) | X | X | X |

| Mary (Dependent) | X | X | X |

11. Adult Child Claimed as a Tax Dependent

How does Medicaid determine the household of an adult child who is claimed as a tax dependent by his parents?

The household of an adult child (19+) claimed as a tax dependent by their parents is always the same as the parents’ household. This applies even if the child is much older, such as 35.

11.1 Dependency Status

Why is dependency status so critical in these determinations?

Dependency status is critical because it indicates financial reliance on the tax filer, which influences the household composition for Medicaid purposes.

11.2 Example Cases

Could you provide example cases to illustrate this rule?

- Barry, 29, is claimed as a tax dependent by his parents, who also claim his younger siblings (15 and 17). Barry’s Medicaid household includes himself, both parents, and his siblings.

- Carla, 28, lives with her married parents. Her father claims her as a dependent. Carla’s father’s household includes himself, his spouse, and Carla. Thus, Carla’s household also includes these three individuals.

12. Non-Child Tax Dependents

Does the exception to the tax dependent rule for tax dependents who are not a child of the taxpayer only apply to adult tax dependents?

No, this exception applies to minors as well. Anytime an individual, regardless of age, is claimed as a tax dependent by someone other than their parents, the non-filer rules apply.

12.1 Application to Minors

How does this rule apply to minors who are claimed as tax dependents by non-parents?

When a minor is claimed as a tax dependent by someone other than their parents, the non-filer rules are used to determine their household, ensuring a more accurate representation of their living situation.

12.2 Scenario Illustration

Could you provide an example scenario?

- Leena, 5, lives with her aunt, who is her guardian. Leena’s aunt claims her as a qualifying relative. Leena’s household consists only of herself because she is a tax dependent who is not the tax dependent of her parents.

13. Navigating Medicaid and Partnership Opportunities

Understanding these Medicaid rules is crucial for accurately determining your eligibility and accessing necessary healthcare benefits. At income-partners.net, we provide resources and partnership opportunities to help you navigate the complexities of income-related decisions.

13.1 Maximizing Partnership Benefits

How can individuals leverage partnerships to enhance their financial well-being?

Partnerships offer opportunities for shared resources, increased income, and mutual support, which can significantly impact financial stability. IncomePartners.net provides a platform to explore and establish these beneficial relationships.

13.2 Final Thoughts

Navigating the complexities of household income and Medicaid eligibility requires a thorough understanding of the rules and regulations. Whether you are a tax filer, a dependent, or a non-filer, knowing how Medicaid determines your household size is essential for accessing the healthcare benefits you need.

Ready to explore partnership opportunities and enhance your income potential? Visit income-partners.net today and discover how strategic alliances can transform your financial future.

FAQ: Household Income and Medicaid Eligibility

1. Does Household Income Include Boyfriend?

Yes, it can. If you file taxes together or if he is considered part of your family unit, his income may be included in your household income for Medicaid eligibility purposes.

2. What is MAGI, and how does it affect Medicaid eligibility?

MAGI, or Modified Adjusted Gross Income, is a methodology used to determine income for Medicaid eligibility based on tax definitions of income and household. It affects eligibility by setting income thresholds.

3. How does Medicaid determine who is included in a household?

Medicaid determines household membership based on an individual’s plan to file a tax return, irrespective of actual filing.

4. Are married couples who file taxes separately considered separate households?

Generally, no. Married couples who live together are always considered part of the same household, regardless of filing status.

5. What are the household rules for tax filers?

For tax filers, the household includes the filer, their spouse (if filing jointly), and all claimed tax dependents.

6. How does pregnancy affect household size determination for Medicaid?

When determining the household size of a pregnant person, they are counted as themselves plus the number of children they are expected to deliver.

7. What happens if an adult child is claimed as a tax dependent by their parents?

The household of an adult child claimed as a tax dependent by their parents is the same as the parents’ household.

8. How do Medicaid and premium tax credit household rules differ?

Medicaid assesses household size individually based on tax status and living arrangements, while premium tax credits treat all members of a tax unit as a single household.

9. Do states have options in implementing MAGI rules?

Yes, states have flexibility in extending age limits for students and counting pregnant individuals in various ways.

10. What if non-married parents live together?

If both parents file taxes, each parent’s Medicaid household includes themselves and anyone they claim as a dependent. A child under 19 is subject to the non-filer rule.