Filing your income tax return in India can seem daunting, but with the right information and a strategic partnership, it can be a smooth process that boosts your financial confidence and income. At income-partners.net, we provide the resources and connections you need to navigate income tax filing and explore opportunities for financial growth through strategic partnerships. Increase your financial expertise and discover how to maximize your tax benefits.

1. Understanding The Basics Of Income Tax Filing In India

Before diving into the step-by-step process, understanding the basics of income tax in India is essential. This involves knowing the different types of income, tax slabs, and the forms you need to file.

1.1 What Is Income Tax?

Income tax is a direct tax levied by the government on the income earned by individuals, businesses, and other entities within a financial year. The tax is calculated based on the income tax slabs defined by the government.

1.2 Types Of Income

Understanding the different types of income is crucial for accurate tax filing:

- Income from Salary: This includes wages, pensions, and any other remuneration received from an employer.

- Income from House Property: This includes rental income from properties you own.

- Profits and Gains from Business or Profession: This includes income from your business or profession.

- Capital Gains: This includes profits from the sale of capital assets such as property, stocks, and mutual funds.

- Income from Other Sources: This includes interest income, dividends, and lottery winnings.

1.3 Income Tax Slabs

The income tax slabs define the rates at which different income levels are taxed. These slabs can change each year, so staying updated is essential. As of the latest updates, there are two tax regimes: the old regime and the new regime.

Old Tax Regime:

- Up to ₹2.5 lakh: Exempt

- ₹2.5 lakh to ₹5 lakh: 5%

- ₹5 lakh to ₹10 lakh: 20%

- Above ₹10 lakh: 30%

New Tax Regime (default regime):

- Up to ₹3 lakh: Exempt

- ₹3 lakh to ₹6 lakh: 5%

- ₹6 lakh to ₹9 lakh: 10%

- ₹9 lakh to ₹12 lakh: 15%

- ₹12 lakh to ₹15 lakh: 20%

- Above ₹15 lakh: 30%

Note: The New Tax Regime offers lower rates but fewer exemptions and deductions.

1.4 Key Forms For Filing Income Tax Return

- ITR-1 (Sahaj): For individuals having income from salaries, one house property, other sources (interest, etc.), and having total income up to ₹50 lakh.

- ITR-2: For individuals and HUFs not having income from business or profession and having income more than ₹50 lakh.

- ITR-3: For individuals and HUFs having income from business or profession.

- ITR-4 (Sugam): For individuals, HUFs, and firms (other than LLP) having income from business and profession which is computed on a presumptive basis.

2. Prerequisites For Filing Your Income Tax Return

Before you start filing your income tax return, make sure you have all the necessary documents and information ready. This will make the process smoother and more efficient.

2.1 Essential Documents

- PAN Card: Permanent Account Number, essential for filing income tax returns.

- Aadhaar Card: Unique identification number, now linked with PAN for tax purposes.

- Bank Account Details: Including account number, IFSC code, and branch details for refund processing.

- Form 16: Certificate issued by your employer detailing the tax deducted at source (TDS) from your salary.

- Form 26AS: Tax Credit Statement showing the taxes deducted and deposited against your PAN.

- Investment Proofs: Documents related to investments eligible for tax deductions, such as LIC premiums, PPF contributions, and ELSS investments.

- Home Loan Statement: For claiming deductions on home loan interest payments.

- Rental Receipts: If you are paying rent and claiming House Rent Allowance (HRA).

2.2 Linking PAN With Aadhaar

Linking your PAN with Aadhaar is now mandatory. If your PAN is not linked, it may become inoperative, which can cause issues in filing your return and claiming refunds.

2.3 Pre-Validating Bank Account

Ensure at least one bank account is pre-validated for receiving refunds. You can add and validate bank accounts on the e-Filing portal.

2.4 Choosing The Right Filing Method

You can file your income tax return either online through the e-Filing portal or offline using the offline utility. Online filing is generally more convenient and efficient.

3. Step-By-Step Guide To Filing ITR-1 Online

ITR-1, also known as Sahaj, is the simplest form for individuals with income from salary, one house property, and other sources. Here’s a step-by-step guide to filing ITR-1 online.

3.1 Logging Into The E-Filing Portal

-

Visit the official e-Filing portal: Go to https://www.incometax.gov.in/.

-

Log in: Use your user ID (PAN), password, and captcha code to log in.

Alt Text: E-Filing portal login screen for Indian income tax returns showing fields for user ID, password, and captcha.

3.2 Navigating To The Filing Section

-

Go to e-File: After logging in, click on the “e-File” tab.

-

Select Income Tax Returns: Choose “File Income Tax Return” from the dropdown menu.

Alt Text: Navigation path on the e-Filing portal to file income tax return showing the e-File tab and the option to file income tax return.

3.3 Selecting Assessment Year And Filing Mode

-

Select Assessment Year: Choose the relevant assessment year (e.g., 2024-25 for the financial year 2023-24).

-

Select Filing Mode: Choose “Online” as the mode of filing.

-

Click Continue: Proceed to the next step.

Alt Text: Screenshot showing the selection of assessment year and online filing mode on the e-Filing portal.

3.4 Choosing The Return Type

-

Select Status: Choose the status applicable to you (Individual).

-

Select ITR Form: If you know which ITR to file, select “ITR-1”. If unsure, choose “Help me decide which ITR Form to file.”

Alt Text: Screenshot of the e-Filing portal showing the options to select the ITR form or get help in deciding.

3.5 Filling Out The ITR-1 Form

The ITR-1 form has five main sections:

3.5.1 Personal Information

-

Validate Pre-Filled Data: Review the pre-filled data, such as your name, address, and PAN details, which are auto-filled from your e-Filing profile.

-

Edit Contact Details: If necessary, edit your contact details, filing type details, and bank details.

-

Choose Tax Regime: Select whether you want to opt for the new or old tax regime.

Alt Text: Image showing the personal information section of the ITR-1 form with details like name, address, and PAN.

3.5.2 Gross Total Income

-

Review Income Details: Confirm or edit your income details from salary/pension, house property, and other sources.

-

Add Exempt Income: Add details of any exempt income, such as allowances or agricultural income.

Alt Text: Snapshot of the gross total income section of ITR-1 showing fields for salary, house property, and other income sources.

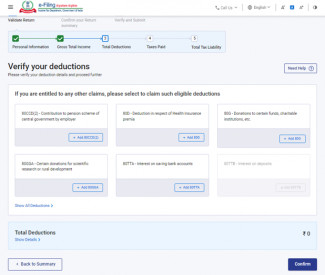

3.5.3 Total Deductions

-

Add Deductions: Add, delete, and confirm any deductions applicable to you under Chapter VI-A of the Income Tax Act.

-

Common Deductions: Include deductions under sections like 80C (LIC, PPF, ELSS), 80D (health insurance), and 80G (donations).

Total deductions section of ITR-1

Total deductions section of ITR-1Alt Text: Image displaying the total deductions section of ITR-1 with fields for various deductions under Chapter VI-A.

3.5.4 Tax Paid

-

Confirm Taxes Paid: Confirm the taxes paid by you in the previous year, including TDS from salary, TCS, advance tax, and self-assessment tax.

-

Verify Details: Ensure the details match your Form 26AS.

Alt Text: Display of the tax paid section of ITR-1 showing details of TDS, TCS, and advance tax payments.

3.5.5 Total Tax Liability

-

Review Tax Liability: Review the tax liability computed based on the validated sections.

-

Pay Tax (If Applicable): If there is a tax liability, pay the tax using the “Pay Now” or “Pay Later” options.

Alt Text: Illustration of the total tax liability section of ITR-1 showing the computed tax liability and options to pay.

3.6 Previewing And Submitting The Return

-

Preview Return: After completing all the sections, click on “Preview Return” to review all the details.

-

Validate Return: Click on “Proceed to Validation” to check for any errors.

-

Submit Return: If there are no errors, click on “Proceed to Verification” to submit your return.

Alt Text: Screenshot of the preview and submit your return page on the e-Filing portal.

3.7 E-Verification

E-verification is mandatory for completing the filing process. You can e-verify your return through various methods:

-

Aadhaar OTP: Verify using OTP received on your Aadhaar-linked mobile number.

-

Net Banking: Verify through your net banking account.

-

Demat Account: Verify through your demat account.

-

Digital Signature Certificate (DSC): Verify using DSC.

Alt Text: Display of e-verification options on the e-Filing portal including Aadhaar OTP, net banking, and DSC.

3.8 Acknowledgment

After successful e-verification, you will receive an acknowledgment number. You will also receive a confirmation message on your registered mobile number and email ID.

4. Understanding The New Tax Regime Vs. Old Tax Regime

The choice between the new tax regime and the old tax regime can significantly impact your tax liability. Understanding the differences and making an informed decision is crucial.

4.1 Key Differences

| Feature | Old Tax Regime | New Tax Regime |

|---|---|---|

| Tax Rates | Higher tax rates with multiple slabs. | Lower tax rates with fewer slabs. |

| Deductions & Exemptions | Allows various deductions and exemptions, such as 80C, HRA, and LTA. | Offers very limited deductions, mainly employer’s contribution to NPS (80CCD(2)) and 80CCH. |

| Default Option | Not the default option; needs to be explicitly chosen each year if opting out of the new tax regime. | Default option; requires opting out if you want to continue with the old tax regime. |

| Suitability | Suitable for those claiming numerous deductions and exemptions. | Suitable for those with fewer investments and claiming minimal deductions. |

| Complexity | More complex due to the need to track and claim various deductions. | Simpler with fewer deductions to consider. |

4.2 How To Choose The Right Regime

- Calculate Your Tax Liability: Calculate your tax liability under both regimes, considering all applicable deductions and exemptions.

- Compare The Results: Compare the results to see which regime offers the lower tax liability.

- Consider Your Financial Situation: Consider your investment habits and future financial goals. If you invest heavily in tax-saving instruments, the old regime might be more beneficial.

- Make An Informed Decision: Choose the regime that best suits your financial situation and goals.

According to research from the University of Texas at Austin’s McCombs School of Business, in July 2025, taxpayers who thoroughly assess their financial situation and compare tax liabilities under both regimes can optimize their tax savings significantly.

5. Common Mistakes To Avoid While Filing Income Tax Return

To ensure accurate and hassle-free tax filing, it’s important to avoid common mistakes.

5.1 Not Linking PAN With Aadhaar

Failing to link your PAN with Aadhaar can render your PAN inoperative, leading to issues in filing your return and claiming refunds.

5.2 Incorrect Personal Information

Ensure all personal information, such as your name, address, and bank details, is accurate and up-to-date.

5.3 Not Reporting All Income

Report all sources of income, including salary, rental income, interest income, and capital gains. Hiding income can lead to penalties and legal issues.

5.4 Claiming Incorrect Deductions

Only claim deductions that you are eligible for and have valid proof for. Claiming incorrect deductions can lead to scrutiny from the Income Tax Department.

5.5 Not Verifying The Return

E-verification is mandatory for completing the filing process. Failing to e-verify your return within the stipulated time can render your return invalid.

5.6 Missing The Deadline

File your income tax return before the due date to avoid late filing fees and interest. The due date is usually July 31st for individuals not subject to audit.

6. Maximizing Tax Benefits Through Strategic Partnerships

Strategic partnerships can be a powerful tool for maximizing tax benefits. By collaborating with other businesses or individuals, you can unlock new opportunities for growth and tax optimization.

6.1 What Are Strategic Partnerships?

Strategic partnerships involve collaborations between two or more parties to achieve mutually beneficial goals. These partnerships can take various forms, such as joint ventures, alliances, and collaborations.

6.2 Benefits Of Strategic Partnerships

- Access to New Markets: Partnerships can provide access to new markets and customer segments.

- Increased Revenue: By combining resources and expertise, partnerships can lead to increased revenue and profitability.

- Cost Savings: Sharing resources and expenses can result in significant cost savings.

- Innovation: Collaborating with others can foster innovation and lead to the development of new products and services.

- Tax Benefits: Strategic partnerships can unlock tax benefits through various mechanisms, such as transfer pricing and tax planning.

6.3 Types Of Strategic Partnerships For Tax Optimization

- Joint Ventures: Joint ventures involve the creation of a new entity to undertake a specific project or business activity.

- Alliances: Alliances involve collaborations between companies to share resources and expertise without creating a new entity.

- Distributor Partnerships: Distributor partnerships involve agreements where one party distributes the products or services of another party.

- Affiliate Partnerships: Affiliate partnerships involve collaborations where one party promotes the products or services of another party in exchange for a commission.

6.4 How Strategic Partnerships Can Help Reduce Tax Liability

- Transfer Pricing: Strategic partnerships can help optimize transfer pricing policies to reduce tax liability by strategically allocating profits between different entities.

- Tax Planning: Partnerships can facilitate tax planning by allowing you to take advantage of tax incentives and deductions that may not be available otherwise.

- R&D Credits: Collaborating on research and development activities can help you claim R&D tax credits, reducing your overall tax burden.

- Investment Opportunities: Partnerships can provide access to investment opportunities that offer tax advantages, such as investments in specific sectors or regions.

According to Harvard Business Review, strategic partnerships can lead to a 10-20% reduction in tax liability through effective tax planning and transfer pricing strategies.

7. Utilizing Income-Partners.Net For Financial Growth

At income-partners.net, we provide the resources and connections you need to navigate income tax filing and explore opportunities for financial growth through strategic partnerships.

7.1 Exploring Partnership Opportunities

income-partners.net offers a platform for businesses and individuals to connect and explore potential partnership opportunities. Whether you’re looking for a joint venture, alliance, or distributor partnership, you can find potential partners on our platform.

7.2 Resources For Tax Planning

We provide a wealth of resources for tax planning, including articles, guides, and tools to help you optimize your tax liability. Our resources cover a wide range of topics, such as tax deductions, exemptions, and strategic tax planning strategies.

7.3 Connecting With Experts

income-partners.net allows you to connect with tax experts and financial advisors who can provide personalized guidance and support. Our experts can help you navigate the complexities of income tax filing and develop a tax plan that aligns with your financial goals.

7.4 Success Stories

Read success stories of businesses and individuals who have achieved financial growth through strategic partnerships facilitated by income-partners.net. These stories highlight the potential of partnerships to unlock new opportunities and drive success.

8. Keeping Up With The Latest Tax Updates

Tax laws and regulations are constantly evolving, so it’s important to stay updated on the latest changes. Here are some tips for staying informed:

8.1 Follow Reputable Sources

Follow reputable sources of tax information, such as the Income Tax Department, financial news outlets, and tax advisory firms.

8.2 Subscribe To Newsletters

Subscribe to newsletters from tax experts and financial advisors to receive regular updates on tax laws and regulations.

8.3 Attend Webinars And Seminars

Attend webinars and seminars on tax-related topics to learn about the latest changes and strategies.

8.4 Consult With A Tax Professional

Consult with a tax professional regularly to ensure you are compliant with the latest tax laws and regulations.

9. Frequently Asked Questions (FAQ)

9.1 What Is The Due Date For Filing Income Tax Return?

The due date for filing income tax return is usually July 31st for individuals not subject to audit.

9.2 What Happens If I Miss The Deadline For Filing Income Tax Return?

If you miss the deadline, you may be subject to late filing fees and interest.

9.3 How Do I Link My PAN With Aadhaar?

You can link your PAN with Aadhaar online through the e-Filing portal.

9.4 What Is Form 16?

Form 16 is a certificate issued by your employer detailing the tax deducted at source (TDS) from your salary.

9.5 What Is Form 26AS?

Form 26AS is a tax credit statement showing the taxes deducted and deposited against your PAN.

9.6 What Are The Different Ways To E-Verify My Income Tax Return?

You can e-verify your return through Aadhaar OTP, net banking, demat account, or digital signature certificate (DSC).

9.7 What Is The Difference Between The Old Tax Regime And The New Tax Regime?

The old tax regime offers higher tax rates with more deductions and exemptions, while the new tax regime offers lower tax rates with fewer deductions.

9.8 How Do I Choose Between The Old Tax Regime And The New Tax Regime?

Calculate your tax liability under both regimes, consider your investment habits, and choose the regime that best suits your financial situation.

9.9 Can I Revise My Income Tax Return After Filing It?

Yes, you can revise your income tax return if you find any errors or omissions after filing it.

9.10 Where Can I Find More Information About Income Tax Filing?

You can find more information on the official website of the Income Tax Department and income-partners.net.

10. Conclusion

Filing your income tax return in India doesn’t have to be a headache. By understanding the basics, gathering the necessary documents, and following a step-by-step guide, you can navigate the process with confidence. Strategic partnerships, facilitated by platforms like income-partners.net, can offer additional avenues for tax optimization and financial growth. Stay informed, avoid common mistakes, and leverage available resources to ensure accurate and beneficial tax filing.

Ready to take control of your financial future? Visit income-partners.net today to explore partnership opportunities, access valuable resources, and connect with experts who can help you achieve your financial goals. Let us help you find the perfect partners, build strong relationships, and start seeing the financial rewards you deserve. Contact us at Address: 1 University Station, Austin, TX 78712, United States. Phone: +1 (512) 471-3434. Website: income-partners.net.