It’s natural to wonder, What Percentage Of Income For Medical Deduction can I claim? Generally, you can deduct the amount of your medical expenses exceeding 7.5% of your adjusted gross income (AGI) on Schedule A (Form 1040). At income-partners.net, we aim to guide you through the complexities of tax deductions, helping you maximize your financial benefits through strategic partnerships and informed decisions. We’ll dive into how to calculate this deduction, explore includible and excludible expenses, and offer insights to optimize your tax strategy with medical expense deductions, cost-effective healthcare partnerships, and maximizing tax savings opportunities.

1. Understanding Medical Expense Deductions

What are medical expenses, and how do they translate into tax deductions? Let’s break down the essentials of medical expense deductions so you’re ready to optimize your tax strategy.

1.1 What Qualifies as a Medical Expense?

According to IRS Publication 502, medical expenses are defined as the costs of diagnosis, cure, mitigation, treatment, or prevention of disease, and for the purpose of affecting any part or function of the body. These expenses encompass a wide array of services and items, including payments for:

- Legal medical services provided by physicians, surgeons, dentists, and other medical practitioners.

- Equipment, supplies, and diagnostic devices needed for medical purposes.

- Insurance premiums that cover medical care expenses.

- Transportation costs to get medical care.

- Qualified long-term care services and insurance contracts.

It’s important to note that medical care expenses must primarily aim to alleviate or prevent a physical or mental disability or illness. Expenses that are merely beneficial to general health, such as vitamins or a vacation, do not qualify.

1.2 The 7.5% AGI Threshold

You can only deduct the amount of your medical and dental expenses that exceeds 7.5% of your Adjusted Gross Income (AGI). AGI is your gross income minus certain deductions, such as contributions to traditional IRAs, student loan interest, and alimony payments.

Here’s how to calculate the deductible amount:

- Calculate your AGI: Subtract above-the-line deductions from your gross income.

- Multiply your AGI by 7.5%: This is the threshold you must exceed.

- Determine your total medical expenses: Sum up all eligible medical expenses.

- Subtract the threshold from your total medical expenses: The result is the amount you can deduct.

Example:

Let’s say your AGI is $60,000, and your total medical expenses for the year amount to $8,000.

- AGI: $60,000

-

- 5% AGI Threshold: $60,000 * 0.075 = $4,500

- Total Medical Expenses: $8,000

- Deductible Amount: $8,000 – $4,500 = $3,500

In this scenario, you can deduct $3,500 from your taxable income.

1.3 Timing of Expenses

You can only include medical and dental expenses you paid this year. Payments for medical or dental care you will receive in a future year are generally not deductible in the current year. However, there are exceptions, such as when you prepay for lifetime care at a retirement home.

If you pay medical expenses by check, the date you mail or deliver the check is generally the date of payment. For “pay-by-phone” or “online” accounts, the date reported on the financial institution’s statement is the date of payment. If you use a credit card, include medical expenses in the year the charge is made, not when you pay the amount charged.

1.4 Whose Medical Expenses Can You Include?

You can generally include medical expenses you pay for yourself, your spouse, and your dependents. A person qualifies as your dependent for the medical expense deduction if they meet certain requirements, including:

- They are your qualifying child or qualifying relative.

- You provided over half of their support for the year.

- They did not file a joint return (with some exceptions).

Special Cases:

- Child of Divorced or Separated Parents: A child can be treated as a dependent of both parents for medical expense purposes if they meet certain criteria, such as receiving over half of their support from the parents and being in the custody of one or both parents for more than half the year.

- Decedent: Medical expenses paid before death by the decedent are included in figuring any deduction for medical and dental expenses on the decedent’s final income tax return.

1.5 Substantiating Your Medical Expenses

To support your medical expense deduction, it’s crucial to maintain detailed records. These records should include:

- Receipts from healthcare providers.

- Explanation of Benefits (EOB) statements from insurance companies.

- Prescriptions from doctors.

- Transportation logs.

- Any other documentation that proves the medical expense.

1.6 IRS Resources and Further Information

For more detailed information on medical expense deductions, consult the following IRS resources:

- IRS Publication 502: Medical and Dental Expenses

- Schedule A (Form 1040): Itemized Deductions

By understanding what qualifies as a medical expense, how to calculate the deductible amount, and whose expenses you can include, you can effectively navigate the complexities of medical expense deductions and optimize your tax strategy.

2. What Medical Expenses Are Includible?

Knowing what qualifies as a medical expense is crucial for maximizing your deductions. Here’s an extensive list of includible medical expenses, as defined by the IRS, to help you accurately calculate your deductions.

2.1 General Medical Expenses

- Abortion: You can include the amount you pay for a legal abortion.

- Acupuncture: Include amounts you pay for acupuncture.

- Alcoholism Treatment: Amounts paid for inpatient treatment at a therapeutic center for alcohol addiction, including meals and lodging. Transportation to and from Alcoholics Anonymous meetings when recommended by a doctor.

- Ambulance: Amounts paid for ambulance services.

- Artificial Limbs: The cost of an artificial limb.

- Artificial Teeth: The cost of artificial teeth.

- Bandages: The cost of medical supplies like bandages.

- Birth Control Pills: Amounts paid for birth control pills prescribed by a doctor.

- Body Scan: The cost of an electronic body scan.

- Braille Books and Magazines: The part of the cost exceeding the price of regular printed editions.

- Breast Pumps and Supplies: Costs of breast pumps and supplies that assist lactation.

- Breast Reconstruction Surgery: Amounts paid for breast reconstruction surgery following a mastectomy for cancer.

2.2 Capital Expenses

- Capital Expenses: Amounts paid for special equipment installed in a home, or for improvements, if their main purpose is medical care for you, your spouse, or your dependent. The cost is reduced by any increase in the value of your property.

- Home Modifications for Disability: Costs for constructing entrance or exit ramps, widening doorways, installing railings in bathrooms, lowering kitchen cabinets, modifying fire alarms, and grading the ground for access.

2.3 Transportation and Vehicle-Related Expenses

- Car Modifications for Disability: Costs for special hand controls and other equipment installed in a car for a person with a disability.

- Car (Special Design): The difference between the cost of a regular car and a car specially designed to hold a wheelchair.

- Transportation: Bus, taxi, train, or plane fares, ambulance service, and transportation expenses of a parent accompanying a child needing medical care. Also includes transportation for regular visits to see a mentally ill dependent if recommended as part of treatment.

- Car Expenses: Out-of-pocket expenses, such as gas and oil, when using a car for medical reasons, or the standard medical mileage rate of 21 cents a mile (for 2024), plus parking fees and tolls.

2.4 Professional Medical Services

- Chiropractor: Fees paid to a chiropractor for medical care.

- Christian Science Practitioner: Fees paid to Christian Science practitioners for medical care.

- Contact Lenses: Amounts paid for contact lenses needed for medical reasons and the cost of equipment and materials required for using contact lenses, such as saline solution and enzyme cleaner.

- Crutches: Amounts to buy or rent crutches.

- Dental Treatment: Amounts for the prevention and alleviation of dental disease, including teeth cleaning, sealants, fluoride treatments, X-rays, fillings, braces, extractions, and dentures.

- Diagnostic Devices: The cost of devices used in diagnosing and treating illness and disease, such as blood sugar test kits for diabetics.

2.5 Care and Support Services

- Disabled Dependent Care Expenses: Some expenses may qualify as either medical expenses or work-related expenses for taking a credit for dependent care. You can choose to apply them either way, but not for both.

- Drug Addiction Treatment: Amounts paid for inpatient treatment at a therapeutic center for drug addiction, including meals and lodging, and transportation to and from drug treatment meetings.

- Guide Dog or Other Service Animal: Costs of buying, training, and maintaining a guide dog or other service animal to assist a visually impaired or hearing-disabled person, or a person with other physical disabilities.

- Health Institute: Fees paid for treatment at a health institute if prescribed by a physician who states that the treatment is necessary to alleviate a physical or mental disability or illness.

- Health Maintenance Organization (HMO): Amounts paid to entitle you, your spouse, or a dependent to receive medical care from an HMO, treated as medical insurance premiums.

- Home Care: Wages and other amounts paid for nursing services, even if not performed by a nurse, as long as the services are of a kind generally performed by a nurse. Includes services like giving medication, changing dressings, bathing, and grooming.

- Hospital Services: Costs of inpatient care at a hospital or similar institution if a principal reason for being there is to receive medical care, including meals and lodging.

- Medicare Part A: Premiums paid for Medicare Part A if you aren’t covered under social security.

- Medicare Part B: Premiums you pay for Medicare Part B.

- Medicare Part D: Premiums you pay for Medicare Part D.

- Nursing Home: Costs of medical care in a nursing home, home for the aged, or similar institution if a principal reason for being there is to get medical care, including meals and lodging.

- Nursing Services: Wages and other amounts you pay for nursing services, including services connected with caring for the patient’s condition, such as giving medication or changing dressings, as well as bathing and grooming the patient.

- Special Home for Intellectually and Developmentally Disabled: Cost of keeping a person who is intellectually and developmentally disabled in a special home, not the home of a relative, on the recommendation of a psychiatrist.

2.6 Vision and Fertility-Related Expenses

- Eye Exam: Amounts paid for eye examinations.

- Eyeglasses: Amounts paid for eyeglasses and contact lenses needed for medical reasons.

- Eye Surgery: Amounts paid for eye surgery to treat defective vision, such as laser eye surgery or radial keratotomy.

- Fertility Enhancement: Costs of procedures such as in vitro fertilization and surgery to overcome an inability to have children.

2.7 Other Includible Expenses

- Hearing Aids: The cost of a hearing aid and batteries, repairs, and maintenance needed to operate it.

- Laboratory Fees: Amounts paid for laboratory fees that are part of medical care.

- Lead-Based Paint Removal: Costs of removing lead-based paints from surfaces in your home to prevent a child who has or had lead poisoning from eating the paint.

- Legal Fees: Fees necessary to authorize treatment for mental illness, but not fees for managing a guardianship estate or conducting the affairs of the person being treated.

- Lifetime Care—Advance Payments: A part of a life-care fee or “founder’s fee” you pay either monthly or as a lump sum under an agreement with a retirement home, properly allocable to medical care.

- Lodging: Cost of lodging (up to $50 per night per person) while away from home if primarily for and essential to medical care, the medical care is provided by a doctor in a licensed hospital or equivalent, and there is no significant element of personal pleasure, recreation, or vacation.

- Long-Term Care: Amounts paid for qualified long-term care services and certain amounts of premiums paid for qualified long-term care insurance contracts.

- Medical Conferences: Amounts paid for admission and transportation to a medical conference concerning the chronic illness of yourself, your spouse, or your dependent, primarily for and necessary to medical care.

- Medicines: Amounts paid for prescribed medicines and drugs, and insulin.

- Operations: Amounts paid for legal operations that aren’t for cosmetic surgery.

- Organ Donors: Amounts paid for medical care you receive because you are a donor or a possible donor of a kidney or other organ.

- Osteopath: Amounts you pay to an osteopath for medical care.

- Oxygen: Amounts you pay for oxygen and oxygen equipment to relieve breathing problems caused by a medical condition.

- Personal Protective Equipment: Amounts you pay for personal protective equipment, such as masks and hand sanitizer, for the primary purpose of preventing the spread of COVID-19.

- Physical Examination: Amounts you pay for an annual physical examination and diagnostic tests by a physician.

- Pregnancy Test Kit: Amounts you pay to purchase a pregnancy test kit.

- Psychiatric Care: Amounts you pay for psychiatric care, including the cost of supporting a mentally ill dependent at a specially equipped medical center.

- Psychoanalysis: Payments for psychoanalysis, unless part of required training to be a psychoanalyst.

- Psychologist: Amounts you pay to a psychologist for medical care.

- Special Education: Fees you pay on a doctor’s recommendation for a child’s tutoring by a teacher who is specially trained and qualified to work with children who have learning disabilities, and the cost (tuition, meals, and lodging) of attending a school that furnishes special education.

- Sterilization: The cost of a legal sterilization (a legally performed operation to make a person unable to have children).

- Stop-Smoking Programs: Amounts you pay for a program to stop smoking (but not for non-prescription drugs like nicotine gum or patches).

- Telephone Equipment: Cost of special telephone equipment that lets a person who is deaf, hard of hearing, or has a speech disability communicate over a regular telephone.

- Television Equipment: Cost of equipment that displays the audio part of television programs as subtitles for persons with a hearing disability.

- Therapy: Amounts you pay for therapy received as medical treatment.

- Transplants: Amounts paid for medical care you receive because you are a donor or a possible donor of a kidney or other organ.

- Trips: Amounts you pay for transportation to another city if the trip is primarily for, and essential to, receiving medical services.

- Vasectomy: The amount you pay for a vasectomy.

- Vision Correction Surgery: Amounts paid for eye surgery to treat defective vision.

- Weight-Loss Program: Amounts you pay to lose weight if it is a treatment for a specific disease diagnosed by a physician (such as obesity, hypertension, or heart disease).

- Wheelchair: Amounts you pay for a wheelchair used for the relief of a sickness or disability, including the cost of operating and maintaining the wheelchair.

- Wig: Cost of a wig purchased upon the advice of a physician for the mental health of a patient who has lost all their hair from disease.

- X-ray: Amounts you pay for X-rays for medical reasons.

By carefully reviewing this list and maintaining detailed records, you can ensure that you are including all eligible medical expenses when calculating your deduction.

Understanding Tax Deductions

Understanding Tax Deductions

3. What Expenses Aren’t Includible?

While many medical expenses can be included in your itemized deductions, the IRS also specifies certain expenses that are not eligible. Being aware of these exclusions can help you avoid miscalculations and ensure your tax return is accurate. Here’s a rundown of medical expenses that aren’t includible:

3.1 General Exclusions

- Baby Sitting, Childcare, and Nursing Services for a Normal, Healthy Baby: You can’t include amounts you pay for the care of children, even if the expenses enable you, your spouse, or your dependent to get medical or dental treatment.

- Controlled Substances: Amounts you pay for controlled substances (such as marijuana, laetrile, etc.) that aren’t legal under federal law, even if such substances are legalized by state law.

- Cosmetic Surgery: Generally, you can’t include amounts you pay for cosmetic surgery. This includes any procedure that is directed at improving the patient’s appearance and doesn’t meaningfully promote the proper function of the body or prevent or treat illness or disease.

- Dancing Lessons: The cost of dancing lessons, swimming lessons, etc., even if they are recommended by a doctor, if they are only for the improvement of general health.

- Diaper Service: The amount you pay for diapers or diaper services, unless they are needed to relieve the effects of a particular disease.

- Electrolysis or Hair Removal: See Cosmetic Surgery, earlier.

- Flexible Spending Arrangement: Amounts for which you are fully reimbursed by your flexible spending arrangement if you contribute a part of your income on a pre-tax basis to pay for the qualified benefit.

- Funeral Expenses: Amounts you pay for funerals.

- Future Medical Care: Current payments for medical care (including medical insurance) to be provided substantially beyond the end of the year.

- Hair Transplant: See Cosmetic Surgery, earlier.

- Health Club Dues: Health club dues or amounts paid to improve one’s general health or to relieve physical or mental discomfort not related to a particular medical condition.

- Health Savings Accounts: Amounts you contribute to a health savings account. You can’t include expenses you pay for with a tax-free distribution from your health savings account.

- Household Help: The cost of household help, even if such help is recommended by a doctor.

- Illegal Operations and Treatments: Amounts you pay for illegal operations, treatments, or controlled substances whether rendered or prescribed by licensed or unlicensed practitioners.

- Insurance Premiums (Certain): Premiums you pay for life insurance policies, policies providing payment for loss of earnings, policies for loss of life, limb, sight, etc., or the part of your car insurance that provides medical insurance coverage for all persons injured in or by your car.

- Maternity Clothes: Amounts you pay for maternity clothes.

- Medical Savings Account (MSA): Amounts you contribute to an Archer MSA. You can’t include expenses you pay for with a tax-free distribution from your Archer MSA.

- Medicines and Drugs From Other Countries: The cost of a prescribed drug brought in (or ordered and shipped) from another country, unless it is legally imported.

- Nonprescription Drugs and Medicines: Amounts you pay for a drug that isn’t prescribed, except for insulin.

- Nutritional Supplements: The cost of nutritional supplements, vitamins, herbal supplements, “natural medicines,” etc., unless they are recommended by a medical practitioner as treatment for a specific medical condition diagnosed by a physician.

- Personal Use Items: The cost of an item ordinarily used for personal, living, or family purposes unless it is used primarily to prevent or alleviate a physical or mental disability or illness.

- Premium Tax Credit: The amount of health insurance premiums paid by or through the premium tax credit, or any amount of advance payments of the premium tax credit made that you did not have to pay back.

- Surrogacy Expenses: The amounts you pay for the identification, retention, compensation, and medical care of a gestational surrogate because they are paid for an unrelated party who is not you, your spouse, or your dependent.

- Swimming Lessons: See Dancing Lessons, earlier.

- Teeth Whitening: Amounts paid to whiten teeth.

- Veterinary Fees: Generally, you can’t include veterinary fees in your medical expenses, but see Guide Dog or Other Service Animal under What Medical Expenses Are Includible, earlier.

- Weight-Loss Program (General Improvement): The cost of a weight-loss program if the purpose of the weight loss is the improvement of appearance, general health, or sense of well-being.

3.2 Specific Examples and Scenarios

To further clarify, here are some specific examples and scenarios of expenses that are not includible:

- Vitamins: Unless specifically prescribed by a doctor for a diagnosed medical condition, over-the-counter vitamins are not deductible.

- Cosmetic Procedures: Procedures like Botox injections or routine teeth whitening are generally not deductible unless required to correct a deformity arising from a congenital abnormality, a personal injury, or a disfiguring disease.

- Gym Memberships: General gym memberships or health club dues are not deductible unless they are part of a weight-loss program prescribed by a physician for a specific medical condition.

- Non-Prescription Medications: Over-the-counter medications, such as pain relievers or cold remedies, are not deductible unless prescribed by a doctor.

- Travel for General Health Improvement: Trips or vacations taken merely for a change in environment, improvement of morale, or general improvement of health, even if made on the advice of a doctor, are not deductible.

3.3 Understanding the Nuances

Several exclusions come with nuances. For instance, cosmetic surgery is deductible if it corrects a deformity related to a congenital abnormality, injury, or disease. Weight-loss programs are deductible if they treat a specific disease diagnosed by a physician. Therefore, it’s essential to understand the context and purpose of the expense.

3.4 Why Accurate Record-Keeping Matters

Maintaining accurate records is essential not only for identifying includible expenses but also for avoiding the inclusion of non-deductible items. This includes keeping receipts, doctor’s notes, and any other documentation that substantiates the medical purpose of the expense.

3.5 Resources for Further Information

For comprehensive details on medical expense deductions and exclusions, refer to the following IRS resources:

- IRS Publication 502: Provides detailed information on medical and dental expenses, including examples and specific guidelines.

- IRS Website: The official IRS website offers updates and clarifications on tax laws and regulations.

By understanding these exclusions, you can refine your approach to medical expense deductions, ensuring compliance and accuracy in your tax filings.

4. How Do You Treat Reimbursements?

When calculating your medical expense deduction, it’s crucial to account for reimbursements you receive from insurance companies or other sources. Here’s how to handle these reimbursements to ensure you’re accurately reporting your deductible expenses.

4.1 General Rule: Reduce Expenses by Reimbursements

The general rule is that you can include in medical expenses only those amounts paid during the tax year for which you received no insurance or other reimbursement. This means that you must reduce your total medical expenses for the year by all reimbursements for medical expenses that you receive from insurance or other sources during the year.

4.2 Types of Reimbursements

Reimbursements can come from various sources, including:

- Health Insurance: Payments from your health insurance policy covering medical expenses.

- Medicare: Payments from Medicare for covered medical services.

- Health Reimbursement Arrangement (HRA): Employer-funded plans that reimburse employees for medical care expenses.

- Flexible Spending Arrangement (FSA): Employer-sponsored plans that allow employees to set aside pre-tax dollars for eligible medical expenses.

- Other Sources: Payments from legal settlements, workers’ compensation, or other third-party payers.

4.3 Example Scenario

Suppose you incurred $10,000 in medical expenses during the year. Your health insurance policy reimbursed you $6,000 for those expenses. In this case, you can only include $4,000 ($10,000 – $6,000) in your medical expense calculation.

4.4 Specific Guidance for Different Reimbursement Types

- Health Insurance:

- Even if a policy provides reimbursement only for certain specific medical expenses, you must use amounts you receive from that policy to reduce your total medical expenses, including those it doesn’t reimburse.

- Health Reimbursement Arrangement (HRA):

- An HRA is an employer-funded plan that reimburses employees for medical care expenses and allows unused amounts to be carried forward. Since an HRA is funded solely by the employer, the reimbursements for medical expenses, up to a maximum dollar amount for a coverage period, aren’t included in your income. You can’t include medical expenses reimbursed by an HRA in your medical expenses.

- Flexible Spending Arrangement (FSA):

- If you are fully reimbursed for medical expenses by your flexible spending arrangement, you can’t include those amounts in your medical expense deduction. This is because you contributed to the FSA on a pre-tax basis.

- Other Reimbursements:

- Generally, you don’t reduce medical expenses by payments you receive for:

- Permanent loss or loss of use of a member or function of the body (loss of limb, sight, hearing, etc.) or disfigurement to the extent the payment is based on the nature of the injury without regard to the amount of time lost from work.

- Loss of earnings.

- Generally, you don’t reduce medical expenses by payments you receive for:

4.5 What If Your Insurance Reimbursement Is More Than Your Medical Expenses?

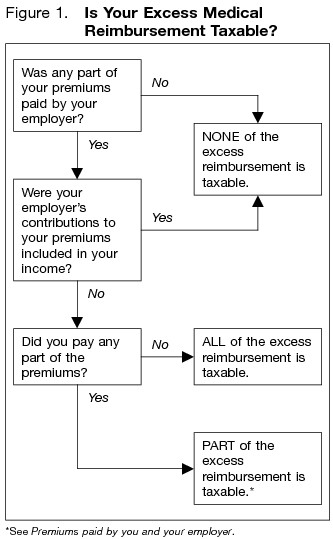

If you are reimbursed more than your medical expenses, you may have to include the excess in income. This depends on whether any part of your premiums was paid by your employer and whether those contributions were included in your income.

Premiums Paid by You:

- If you pay the entire premium for your medical insurance, you generally don’t include the excess reimbursement in your gross income.

Premiums Paid by You and Your Employer:

- If both you and your employer contribute to your medical insurance plan and your employer’s contributions aren’t included in your gross income, you must include in your gross income the part of your excess reimbursement that is from your employer’s contribution.

Premiums Paid by Your Employer:

- If your employer or your former employer pays the total cost of your medical insurance plan and your employer’s contributions aren’t included in your income, you must report all of your excess reimbursement as other income.

4.6 What if You Receive Insurance Reimbursement in a Later Year?

If you are reimbursed in a later year for medical expenses you deducted in an earlier year, you must generally report the reimbursement as income up to the amount you previously deducted as medical expenses. However, don’t report as income the amount of reimbursement you received up to the amount of your medical deductions that didn’t reduce your tax for the earlier year.

4.7 What if You Are Reimbursed for Medical Expenses You Didn’t Deduct?

If you didn’t deduct a medical expense in the year you paid it because your medical expenses weren’t more than 7.5% of your AGI or because you didn’t itemize deductions, don’t include the reimbursement, up to the amount of the expense, in income. However, if the reimbursement is more than the expense, see What if Your Insurance Reimbursement Is More Than Your Medical Expenses?

4.8 Accurate Record-Keeping for Reimbursements

Keep detailed records of all reimbursements received for medical expenses. This includes:

- Explanation of Benefits (EOB) statements from insurance companies.

- Statements from HRAs or FSAs.

- Settlement documents from legal cases.

- Any other documentation that shows the amount and source of reimbursement.

By meticulously accounting for reimbursements, you can ensure the accuracy of your medical expense deduction and avoid potential issues with the IRS.

5. Figuring and Reporting the Deduction on Your Tax Return

Once you’ve gathered all the necessary information about your medical expenses and reimbursements, the next step is to calculate and report the deduction on your tax return. Here’s how to do it accurately.

5.1 What Tax Form Do You Use?

You report your medical expense deduction on Schedule A (Form 1040), Itemized Deductions.

5.2 Steps to Calculate Your Medical Expense Deduction

- Determine Your Adjusted Gross Income (AGI):

- Your AGI is your gross income minus certain deductions. You can find your AGI on Form 1040.

- Calculate the 7.5% AGI Threshold:

- Multiply your AGI by 0.075 (7.5%). This is the amount of medical expenses you must exceed to take a deduction.

- Total Your Includible Medical Expenses:

- Sum all medical expenses you paid during the year that are includible, as discussed earlier.

- Subtract Reimbursements:

- Reduce your total medical expenses by any reimbursements you received from insurance or other sources.

- Calculate Your Deduction:

- Subtract the 7.5% AGI threshold from your total medical expenses (after subtracting reimbursements). The result is the amount you can deduct.

Formula:

Deductible Medical Expenses = (Total Medical Expenses – Reimbursements) – (AGI x 0.075)

5.3 Example Calculation

Let’s walk through an example to illustrate the calculation:

- AGI: $70,000

- Total Medical Expenses: $12,000

- Reimbursements: $3,000

- Calculate the 7.5% AGI Threshold:

- $70,000 (AGI) x 0.075 = $5,250

- Subtract Reimbursements from Total Medical Expenses:

- $12,000 (Total Medical Expenses) – $3,000 (Reimbursements) = $9,000

- Calculate Your Deduction:

- $9,000 – $5,250 (7.5% AGI Threshold) = $3,750

In this case, you can deduct $3,750 as medical expenses on Schedule A (Form 1040).

5.4 Completing Schedule A (Form 1040)

- Line 1: Enter the total amount you paid for medical and dental insurance premiums.

- Line 2: Enter the total amount of other medical expenses (including those not covered by insurance).

- Line 3: Add lines 1 and 2. This is your total medical expenses.

- Line 4: Enter your adjusted gross income from Form 1040.

- Line 5: Multiply the amount on line 4 by 0.075 (7.5%).

- Line 6: Subtract line 5 from line 3. If the result is zero or less, enter -0-. This is the amount of medical expense deduction you can claim.

5.5 Record-Keeping Requirements

It’s crucial to keep detailed records to support your medical expense deduction. These records should include:

- Receipts from healthcare providers.

- Explanation of Benefits (EOB) statements from insurance companies.

- Prescriptions from doctors.

- Transportation logs.

- Any other documentation that proves the medical expense.

5.6 Sale of Medical Equipment or Property

If you deduct the cost of medical equipment or property in one year and sell it in a later year, you may have a taxable gain. The taxable gain is the amount of the selling price that is more than the adjusted basis of the equipment or property. The IRS provides worksheets to help you calculate the adjusted basis and the gain or loss on the sale.

5.7 Resources for Additional Guidance

- IRS Publication 502: Medical and Dental Expenses

- Schedule A (Form 1040): Itemized Deductions

- Instructions for Schedule A (Form 1040): Provides detailed guidance on completing the form.

6. Special Situations and Considerations

Certain circumstances require special attention when claiming medical expense deductions. Understanding these situations ensures you accurately report your expenses and maximize your tax benefits.

6.1 Damages for Personal Injuries

If you receive an amount in settlement of a personal injury suit, part of that award may be for medical expenses that you deducted in an earlier year. If it is, you must include that part in your income in the year you receive it to the extent it reduced your taxable income in the earlier year.

Example:

You sued for injuries you suffered in an accident last year. Last year, you paid $500 for medical expenses for your injuries and deducted those expenses on last year’s tax return. This year, you settled your lawsuit for $2,000. The $500 is includible in your income this year because you deducted the entire $500 as a medical expense deduction last year.

Future Medical Expenses:

If you receive an amount in settlement of a damage suit for personal injuries, part of that award may be for future medical expenses. If it is, you must reduce any future medical expenses for these injuries until the amount you received has been completely used.

6.2 Workers’ Compensation

If you received workers’ compensation and deducted medical expenses related to that injury, you must include the workers’ compensation in income up to the amount you deducted. If you received workers’ compensation but didn’t deduct medical expenses related to that injury, don’t include the workers’ compensation in your income.

6.3 Impairment-Related Work Expenses

If you are a person with disabilities, you can take a business deduction for expenses that are necessary for you to be able to work. If you take a business deduction for these impairment-related work expenses, they aren’t subject to the 7.5% limit that applies to medical expenses.

Impairment-related expenses are those ordinary and necessary business expenses that are:

- Necessary for you to do your work satisfactorily.

- For goods and services not required or used, other than incidentally, in your personal activities.

- Not specifically covered under other income tax laws.

6.4 Health Insurance Costs for Self-Employed Persons

If you were self-employed and had a net profit for the year, you may be able to deduct, as an adjustment to income, amounts paid for health insurance (which includes medical, dental, and vision insurance and qualified long-term care insurance) on behalf of yourself, your spouse, your dependents, and your children who were under age 27 at the end of the year. The insurance plan must be established under your trade or business, and the deduction can’t be more than your earned income from that trade or business.

If you qualify to take the deduction, use the Self-Employed Health Insurance Deduction Worksheet in the Instructions for Form 1040 to figure the amount you can deduct.

6.5 Health Coverage Tax Credit (HCTC)

The Health Coverage Tax Credit (HCTC) helps eligible individuals pay for health coverage. If you are eligible for the HCTC, you can’t include the amount of health insurance premiums paid by or through the HCTC in your medical expense deduction.

6.6 Qualified Long-Term Care Services and Insurance Contracts

You can include in medical expenses amounts paid for qualified long-term care services and certain amounts of premiums paid for qualified long-term care insurance contracts.

Qualified Long-Term Care Services:

Qualified long-term care services are necessary diagnostic, preventive, therapeutic, curing, treating, mitigating, rehabilitative services, and maintenance and personal care services required by a chronically ill individual and provided pursuant to a plan of care prescribed by a licensed health care practitioner.

Qualified Long-Term Care Insurance Contracts:

A qualified long-term care insurance contract is an insurance contract that provides only coverage of qualified long-term care services. The amount of qualified long-term care premiums you can include is limited based on your age.

6.7 State and Local Taxes

Some states allow a deduction or credit for medical expenses on your state income tax return. Check with your state’s tax agency for more information.

6.8 More Information and Resources

For further information and detailed guidance on these special situations, refer to the following resources:

- IRS Publication 502: Medical and Dental Expenses

- IRS Publication 525: Taxable and Nontaxable Income

- **Instructions for Form 104