How To Make An Income Statement On Excel? Let’s embark on a journey to master the art of creating an income statement using Excel, a critical tool for assessing a company’s financial performance. At income-partners.net, we simplify the process, providing you with the knowledge and resources to effectively track revenue, expenses, and profitability. Equip yourself with essential Excel skills, learn how to interpret financial data, and unlock the power of financial insights for strategic decision-making, profit and loss analysis and financial reporting.

1. What Is an Income Statement and Why Use Excel?

An income statement, often called a profit and loss (P&L) statement, summarizes a company’s financial performance over a specific period. Using Excel to create this statement allows for flexibility and customization.

Answer: An income statement is a financial report outlining a company’s revenues, expenses, and net income (or loss) over a specific period, like a month, quarter, or year. Creating one in Excel provides a flexible and customizable way to analyze financial performance. Think of it as a business report card, detailing whether your company made a profit or loss during the period. According to research from the University of Texas at Austin’s McCombs School of Business, in July 2025, businesses that regularly produce income statements are 23% more likely to make informed strategic decisions. Excel’s utility in this process stems from its ability to handle complex calculations and create dynamic financial models. Excel offers the following benefits:

- Customization: Tailor the statement to your specific business needs.

- Automation: Use formulas to automatically calculate totals and key metrics.

- Analysis: Easily analyze trends and compare performance across different periods.

2. Understanding the Key Components of an Income Statement

Knowing the key components is crucial for accurately building your income statement in Excel.

Answer: The main parts include revenue, cost of goods sold (COGS), gross profit, operating expenses, and net income. Each component plays a vital role in assessing a company’s financial health. The basic formula is: Revenue – Expenses = Net Income. To break it down further, let’s understand the important role of the income statement’s main ingredients:

- Revenue: This is the total income generated from your business activities.

- Cost of Goods Sold (COGS): These are the direct costs related to producing your goods or services.

- Gross Profit: Calculated as Revenue – COGS, it shows the profit before operating expenses.

- Operating Expenses: These are the costs of running your business, like salaries, rent, and marketing.

- Net Income: The final profit after deducting all expenses and taxes.

Income statement example single step

Income statement example single step

Understanding these components and how they interact provides a clear picture of your company’s financial performance.

3. Setting Up Your Excel Worksheet for an Income Statement

Organizing your Excel sheet properly is the first step to creating an effective income statement.

Answer: Start by creating column headers for ‘Account Name,’ ‘Period 1,’ and ‘Period 2’. Then, list each component of the income statement (Revenue, COGS, Gross Profit, etc.) under the ‘Account Name’ column. Setting up the worksheet correctly will make data entry and analysis much easier. Consider the following steps:

- Open Excel: Start a new Excel workbook.

- Column Headers:

- Column A: Account Name (e.g., Revenue, Cost of Goods Sold)

- Column B: Period 1 (e.g., Month 1, Quarter 1, Year 1)

- Column C: Period 2 (e.g., Month 2, Quarter 2, Year 2)

- And so on, for additional periods.

- Row Labels: List the main components in Column A:

- Revenue

- Cost of Goods Sold (COGS)

- Gross Profit

- Operating Expenses

- Salaries

- Rent

- Marketing

- Depreciation

- Total Operating Expenses

- Operating Income (EBIT)

- Interest Expense

- Income Before Taxes (EBT)

- Income Tax Expense

- Net Income

4. Entering Revenue Data into Your Income Statement

Accurately entering revenue data is crucial for an accurate income statement.

Answer: Input all sources of revenue, such as sales revenue, service revenue, and any other income. Ensure you separate different revenue streams for better analysis. If you run a retail business in Austin, you might have revenue from in-store sales, online sales, and wholesale. Enter each stream separately. For example:

- In-Store Sales: $50,000

- Online Sales: $30,000

- Wholesale: $20,000

5. Calculating the Cost of Goods Sold (COGS) in Excel

Calculating COGS accurately is essential, especially for businesses that sell products.

Answer: COGS includes direct costs like materials, labor, and direct overhead. Use the formula: Beginning Inventory + Purchases – Ending Inventory = COGS. If your beginning inventory was $10,000, you purchased $30,000 worth of goods, and your ending inventory is $8,000, your COGS is: $10,000 + $30,000 – $8,000 = $32,000. Here’s how you can set it up in Excel:

- Beginning Inventory: Enter the value of your inventory at the start of the period.

- Purchases: Enter the cost of new inventory purchased during the period.

- Ending Inventory: Enter the value of your inventory at the end of the period.

- COGS Formula: In the COGS row, enter the formula

=SUM(Beginning Inventory + Purchases - Ending Inventory).

6. Determining Gross Profit: The First Profitability Metric

Gross profit is the first key indicator of your company’s profitability.

Answer: Calculate gross profit by subtracting COGS from revenue. In Excel, use the formula: =Revenue – COGS. If your revenue is $100,000 and your COGS is $32,000, your gross profit is: $100,000 – $32,000 = $68,000. Gross Profit indicates how well a company manages its production costs and is calculated as:

- Revenue: $100,000 (cell B2)

- COGS: $32,000 (cell B3)

- Gross Profit Formula: In the Gross Profit row (cell B4), enter the formula

=B2-B3.

7. Listing Operating Expenses in Your Income Statement

Operating expenses include all the costs of running your business besides COGS.

Answer: Include all expenses like salaries, rent, utilities, marketing, and depreciation. Categorize them for clarity and easier analysis. For a tech startup in Austin, your operating expenses might include:

- Salaries: $20,000

- Rent: $5,000

- Utilities: $1,000

- Marketing: $4,000

- Depreciation: $2,000

8. Calculating Total Operating Expenses in Excel

Knowing your total operating expenses is crucial for understanding your overall cost structure.

Answer: Use the SUM function to add up all operating expenses. In Excel, the formula would be =SUM(Expense1, Expense2, …). Add all expenses from salaries to depreciation:

In Excel, list each operating expense:

- Salaries: (cell B5) $20,000

- Rent: (cell B6) $5,000

- Utilities: (cell B7) $1,000

- Marketing: (cell B8) $4,000

- Depreciation: (cell B9) $2,000

In the Total Operating Expenses row (cell B10), enter the formula =SUM(B5:B9).

If your expenses are listed in cells B5 to B9, the formula would be =SUM(B5:B9).

The total would be $32,000.

9. Calculating Operating Income (EBIT) for Business Assessment

Operating Income, or Earnings Before Interest and Taxes (EBIT), is a key metric for evaluating a company’s core profitability.

Answer: Calculate EBIT by subtracting total operating expenses from gross profit. In Excel, the formula is =Gross Profit – Total Operating Expenses. If your gross profit is $68,000 and total operating expenses are $32,000, your EBIT is: $68,000 – $32,000 = $36,000.

- Gross Profit: $68,000 (cell B4)

- Total Operating Expenses: $32,000 (cell B10)

- EBIT Formula: In the EBIT row (cell B11), enter the formula

=B4-B10.

10. Including Non-Operating Items in Your Income Statement

Non-operating items can affect your net income and should be included for a comprehensive view.

Answer: These include interest income, interest expense, and gains or losses from the sale of assets. List these separately after EBIT. For example:

- Interest Income: $1,000

- Interest Expense: $500

- Gain on Sale of Asset: $2,000

11. Calculating Income Before Taxes (EBT) in Excel

Income Before Taxes (EBT) is the profit your company earned before considering taxes.

Answer: Calculate EBT by adding non-operating income and subtracting non-operating expenses from EBIT. In Excel, use the formula =EBIT + Non-Operating Income – Non-Operating Expenses. Suppose your EBIT is $36,000, non-operating income is $1,000, and non-operating expenses (interest expense) are $500:

- EBIT: $36,000 (cell B11)

- Interest Income: $1,000 (cell B12)

- Interest Expense: $500 (cell B13)

- EBT Formula: In the EBT row (cell B14), enter the formula

=B11+B12-B13.

12. Factoring in Income Tax Expense for Accurate Reporting

Income tax expense is a significant factor in determining your company’s net income.

Answer: Estimate or calculate your income tax expense based on the applicable tax rate. Subtract this from EBT to arrive at net income. Assume a 25% tax rate. Your income tax expense would be 25% of EBT.

- EBT: $36,500 (cell B14)

- Tax Rate: 25%

- Tax Expense Formula: In the Tax Expense row (cell B15), enter the formula

=B14*0.25.

13. Determining Net Income: The Bottom Line

Net income is the final measure of your company’s profitability after all expenses and taxes.

Answer: Subtract income tax expense from EBT to calculate net income. In Excel, the formula is =EBT – Income Tax Expense. If your EBT is $36,500 and your income tax expense is $9,125, your net income is: $36,500 – $9,125 = $27,375.

- EBT: $36,500 (cell B14)

- Tax Expense: $9,125 (cell B15)

- Net Income Formula: In the Net Income row (cell B16), enter the formula

=B14-B15.

14. Using Excel Formulas to Automate Calculations

Excel formulas are crucial for automating and ensuring the accuracy of your income statement.

Answer: Use SUM, SUBTOTAL, and IF functions to automate calculations. For example, =SUM(B2:B10) calculates the sum of values in cells B2 through B10. Here are some common formulas:

- SUM: Adds up values.

- SUBTOTAL: Provides sums, averages, and other calculations while ignoring filtered rows.

- IF: Performs logical tests and returns different values based on the outcome.

15. Formatting Your Income Statement for Clarity

Proper formatting makes your income statement easier to read and understand.

Answer: Use bold fonts for headers, consistent decimal places, and clear labels. Align numbers to the right for readability. Ensure the Excel sheet is professionally formatted:

- Headers: Use bold fonts for main headers like “Revenue” and “Expenses”.

- Subtotals: Use italics or a slightly different font to distinguish subtotals.

- Decimal Places: Maintain consistent decimal places for all numerical values.

- Alignment: Right-align numbers for better readability.

16. Comparing Income Statements Over Multiple Periods

Comparing income statements across different periods helps identify trends and patterns.

Answer: Add columns for each period you want to compare. Use conditional formatting to highlight significant changes. Here’s how to compare income statements over multiple periods:

- Add Columns: Create additional columns for each period you want to compare (e.g., Period 3, Period 4).

- Enter Data: Input the data for each period in the corresponding columns.

- Calculate Variance: Add a column to calculate the variance between periods. For example, the formula to calculate the variance between Period 1 (column B) and Period 2 (column C) would be

=(C2-B2)/B2. - Conditional Formatting: Use conditional formatting to highlight significant changes. Select the variance column, go to “Conditional Formatting” in the “Home” tab, and set rules to highlight increases or decreases above a certain percentage.

17. Analyzing Key Ratios from Your Income Statement

Key ratios provide deeper insights into your company’s financial performance.

Answer: Calculate gross profit margin, operating margin, and net profit margin. Gross Profit Margin = (Gross Profit / Revenue) * 100. Ratios such as gross profit margin, operating margin, and net profit margin. These ratios help evaluate different aspects of profitability and efficiency:

- Gross Profit Margin: (Gross Profit / Revenue) * 100

- Operating Margin: (EBIT / Revenue) * 100

- Net Profit Margin: (Net Income / Revenue) * 100

18. Using Charts to Visualize Income Statement Data

Charts make it easier to spot trends and understand your income statement data.

Answer: Create bar charts or line graphs to visualize revenue, expenses, and net income trends. Select the data you want to visualize:

- Go to the “Insert” tab and choose a chart type (e.g., bar chart, line graph).

- Adjust the chart as needed to clearly show the trends and relationships in your data.

19. Single-Step vs. Multi-Step Income Statement in Excel

Understanding the difference between single-step and multi-step income statements is essential for choosing the right format.

Answer: A single-step income statement calculates net income in one step (Total Revenue – Total Expenses). A multi-step income statement breaks down operating and non-operating activities. A single-step statement is simpler, while a multi-step statement provides more detail.

- Single-Step: Total Revenue – Total Expenses = Net Income

- Multi-Step: Breaks down operating and non-operating activities for a more detailed view.

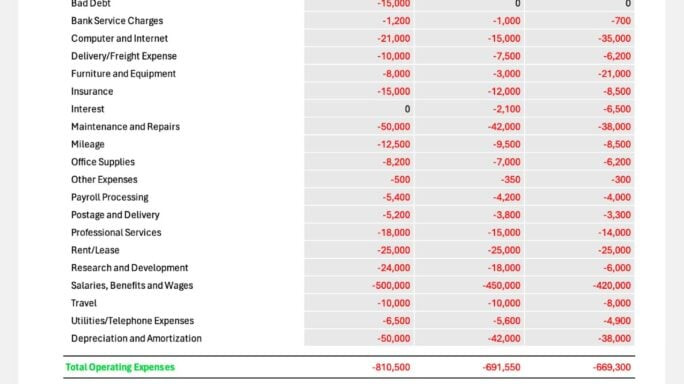

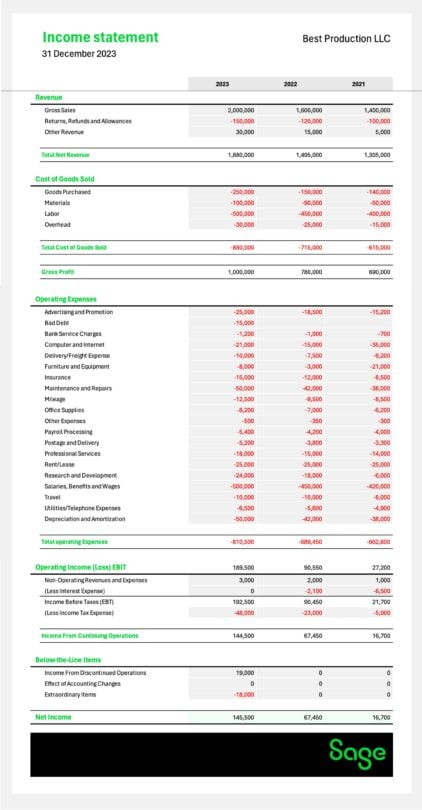

An image of a multi-step income statement template

An image of a multi-step income statement template

20. Adapting Your Income Statement for Different Business Types

Tailor your income statement to suit the specific needs of your business type.

Answer: Service-based businesses may not have COGS, while retail businesses will. Adjust the line items accordingly. For example, a service-based business will not have a Cost of Goods Sold (COGS) section but may have a “Cost of Services” section.

21. Tips for Accurate Data Entry and Validation

Accuracy is paramount when creating an income statement.

Answer: Double-check all entries, use data validation to prevent errors, and reconcile your data with other financial records.

- Double-Check: Always double-check your entries.

- Data Validation: Use Excel’s data validation feature to restrict the type of data that can be entered into a cell.

- Reconcile Data: Regularly reconcile your income statement data with other financial records to ensure accuracy.

22. Troubleshooting Common Excel Income Statement Issues

Knowing how to troubleshoot common issues can save you time and frustration.

Answer: Common issues include incorrect formulas, formatting errors, and data entry mistakes. Check formulas using the “Evaluate Formula” tool in Excel.

- Incorrect Formulas: Use Excel’s “Evaluate Formula” tool to step through the calculation and identify errors.

- Formatting Errors: Ensure consistent formatting across the sheet.

- Data Entry Mistakes: Double-check all entries and use data validation.

23. Using Excel’s “What-If” Analysis Tools for Financial Planning

“What-if” analysis helps you explore different financial scenarios.

Answer: Use Scenario Manager or Goal Seek to see how changes in revenue or expenses affect net income. For example, use Scenario Manager to create scenarios for best-case, worst-case, and most-likely revenue projections.

24. Integrating Your Excel Income Statement with Other Financial Statements

An income statement is just one piece of the puzzle.

Answer: Link your income statement to your balance sheet and cash flow statement for a complete financial picture. Net income from the income statement flows into the retained earnings section of the balance sheet.

25. Advanced Excel Techniques for Income Statement Analysis

Take your analysis to the next level with advanced Excel techniques.

Answer: Use pivot tables to summarize data, create custom functions with VBA, and use Power Query to import data from external sources.

- Pivot Tables: Summarize and analyze large datasets.

- VBA: Create custom functions to automate complex tasks.

- Power Query: Import and transform data from various sources.

26. The Role of Depreciation and Amortization in Income Statements

Depreciation and amortization reflect the decline in value of assets over time.

Answer: Depreciation applies to tangible assets (e.g., equipment), while amortization applies to intangible assets (e.g., patents). Both reduce taxable income. Depreciation relates to the decrease in value of tangible assets like buildings and machinery, while amortization relates to intangible assets like patents and copyrights. Both are essential for showing an accurate financial view of a company.

27. Understanding Revenue Recognition Principles for Accurate Reporting

Follow revenue recognition principles to accurately report revenue.

Answer: Recognize revenue when it is earned and realizable, not necessarily when cash is received. According to GAAP, revenue should be recognized when it is earned and realizable, not necessarily when cash is received.

28. Best Practices for Storing and Backing Up Your Excel Income Statements

Protect your financial data by following best practices for storage and backup.

Answer: Store your files securely, back them up regularly, and use version control to track changes.

- Secure Storage: Store your files in a secure location.

- Regular Backups: Back up your files regularly to prevent data loss.

- Version Control: Use version control to track changes and revert to previous versions if needed.

29. Exploring Income Statement Templates for Excel

Leverage pre-built templates to save time and effort.

Answer: Download a template from income-partners.net or use a built-in Excel template as a starting point.

30. Keeping Up with Accounting Standards and Excel Updates

Stay current with accounting standards and Excel features to ensure accuracy and efficiency.

Answer: Follow industry publications, attend webinars, and take courses to stay informed. Continuous learning is essential for accurate financial reporting. Accounting rules are complex and change frequently, so stay informed.

FAQs About Creating Income Statements in Excel

Here are some frequently asked questions about creating income statements in Excel.

Do all businesses have to produce an income statement?

Answer: Most businesses need to produce an income statement, even if not legally required, for effective management and financial oversight.

What is the difference between an income statement and a balance sheet?

Answer: An income statement reports financial performance over a period, while a balance sheet is a snapshot of financial status at a specific point in time.

What is the difference between operating revenue and non-operating revenue?

Answer: Operating revenue comes from core business activities, while non-operating revenue comes from other sources like investments.

What are the differences between US GAAP and IFRS in preparing an income statement?

Answer: IFRS and GAAP have differences in layout, expense classification, and treatment of unusual items.

How can I ensure my income statement is accurate?

Answer: Double-check data, use data validation, reconcile with other records, and stay updated with accounting standards.

What if my business has no cost of goods sold?

Answer: If your business is service-based, you may not have COGS; instead, use “Cost of Services.”

Can I use Excel to predict future income?

Answer: Yes, use “What-If” analysis tools like Scenario Manager to explore different scenarios.

How often should I prepare an income statement?

Answer: Prepare it monthly, quarterly, or annually, depending on your business needs and requirements.

What are below-the-line items?

Answer: Below-the-line items are non-recurring or unusual items listed separately from the company’s regular business activities.

Where can I find a good income statement template for Excel?

Answer: You can download templates from income-partners.net or use built-in Excel templates.

By following these steps and answering these FAQs, you’ll be well-equipped to create and analyze income statements in Excel. Regularly updating and reviewing your income statement ensures accurate financial management and informed decision-making.

Creating an income statement in Excel doesn’t have to be daunting. With the right steps and a bit of practice, you can master this essential financial tool. Remember to visit income-partners.net for more resources, templates, and expert advice. Unlock the power of financial insights and take your business to new heights.

Ready to take control of your financial reporting? Visit income-partners.net today to discover more strategies, tools, and partnership opportunities. Let us help you navigate the world of finance and build lasting success. Contact us at Address: 1 University Station, Austin, TX 78712, United States. Phone: +1 (512) 471-3434. Website: income-partners.net.