What is the California state income tax rate for 2024? California’s income tax system is progressive, meaning rates increase as income rises, and if you’re looking to explore opportunities to boost your income through strategic partnerships, income-partners.net offers resources to help you navigate the income tax landscape. Discover more about forming effective partnerships for increased profitability through tax-efficient income strategies, including business alliances, joint ventures, and revenue sharing, which can help mitigate tax burdens.

1. Understanding California’s Income Tax Structure

Do you want to understand the complexities of California’s income tax system? California has a progressive income tax system, meaning the tax rate increases as your income goes higher. According to the Franchise Tax Board, California has a multi-bracket system, with rates varying based on income levels. It is critical to understand these brackets if you want to plan your finances effectively.

- Progressive System: Tax rates increase as income rises.

- Multiple Brackets: California has several income tax brackets.

- Varying Rates: Tax rates depend on income levels.

2. What Are the 2024 California Income Tax Brackets?

Are you curious about the specific income tax brackets for 2024 in California? In 2024, California has nine income tax brackets, ranging from 1% to 12.3%. Plus, there is an additional 1% tax on income over $1 million for mental health services. For example, in 2024, for single filers, the 1% rate applies to income up to $10,412, while the top rate of 12.3% applies to income over $698,271.

- Nine Brackets: Tax rates vary across different income levels.

- Range of Rates: From 1% to 12.3%.

- Millionaire’s Tax: An additional 1% on income above $1 million.

3. How Does California’s Income Tax Rate Compare to Other States?

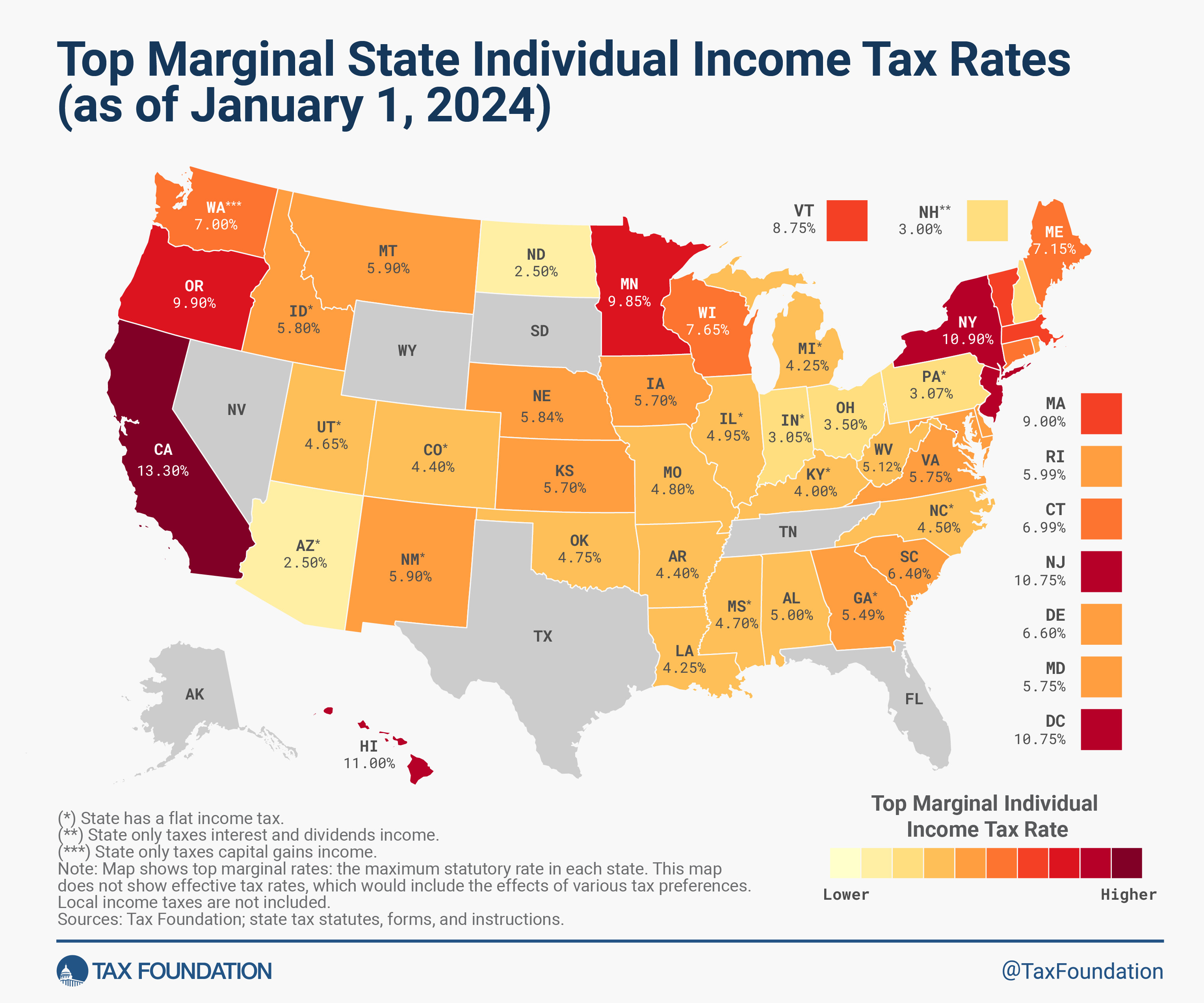

Do you wonder how California’s income tax rates stack up against those of other states? California has some of the highest income tax rates in the U.S. In 2024, the top marginal rate is 13.3% (including the 1% mental health services tax), which is significantly higher than the national average. States like Texas, Florida, and Washington have no state income tax, making California a high-tax state.

- Highest in the U.S.: Among the highest state income tax rates.

- High Top Rate: 13.3% top marginal rate.

- No Income Tax States: Texas, Florida, Washington, etc., have no state income tax.

4. What Factors Influence California’s Income Tax Rates?

Do you know what factors influence California’s income tax rates? Several factors influence California’s income tax rates, including state budget needs, economic conditions, and legislative changes. According to the California Budget & Policy Center, tax revenues are crucial for funding public services like education, healthcare, and infrastructure. Changes in these areas can lead to adjustments in income tax rates.

- State Budget Needs: Government funding requirements affect tax rates.

- Economic Conditions: Economic downturns or booms can lead to adjustments.

- Legislative Changes: Laws passed by the legislature can change rates and brackets.

5. How Can I Calculate My California State Income Tax?

Do you need help calculating your California state income tax? Calculating your California state income tax involves several steps. First, determine your total income, then subtract any deductions and exemptions. Next, use the tax brackets for your filing status (single, married, etc.) to calculate the tax owed for each bracket. Finally, add up the amounts from each bracket to find your total state income tax. The Franchise Tax Board provides worksheets and online tools to assist with this calculation.

- Determine Total Income: Calculate all sources of income.

- Subtract Deductions: Reduce taxable income with eligible deductions.

- Use Tax Brackets: Apply the appropriate tax rate for each income bracket.

6. What Are the Standard Deductions and Exemptions in California for 2024?

Are you familiar with California’s standard deductions and exemptions for 2024? In 2024, California offers a standard deduction to reduce your taxable income. For single filers, it’s $5,363, and for married couples filing jointly, it’s $10,726. Additionally, there are personal exemption credits and dependent credits available, which can further reduce your tax liability.

- Standard Deduction: $5,363 for single filers, $10,726 for married filing jointly.

- Personal Exemptions: Credits available to reduce tax liability.

- Dependent Credits: Additional credits for dependents.

7. What are Some Common Deductions to Reduce My California Income Tax?

Do you want to know about common deductions that can lower your California income tax? Several deductions can help lower your California income tax. Common deductions include contributions to retirement accounts (like 401(k)s and IRAs), health savings account (HSA) contributions, student loan interest, and itemized deductions like medical expenses and charitable contributions. The IRS and FTB websites provide detailed lists and requirements for each deduction.

- Retirement Contributions: Contributions to 401(k)s and IRAs.

- HSA Contributions: Contributions to Health Savings Accounts.

- Student Loan Interest: Deduction for student loan interest paid.

California Tax Form 540

California Tax Form 540

8. How Do Changes in Federal Tax Law Affect California State Income Tax?

Do you know how federal tax law changes affect California’s income tax? Changes in federal tax law can have a significant impact on California’s state income tax. California often conforms to federal tax laws, especially regarding deductions and exemptions. However, California may also decouple from certain federal provisions, meaning it maintains its own rules. For example, the Tax Cuts and Jobs Act (TCJA) of 2017 led to several changes that California partially conformed to, affecting both individual and business taxes.

- Conformity: California often aligns with federal tax laws.

- Decoupling: California can choose to maintain its own rules.

- TCJA Impact: The 2017 Tax Cuts and Jobs Act led to several changes.

9. How Do I File My California State Income Tax Return?

Are you trying to figure out how to file your California state income tax return? You can file your California state income tax return either online, through the mail, or with the help of a tax professional. The Franchise Tax Board (FTB) offers an online filing system called CalFile, which is free for those who qualify. Alternatively, you can download the necessary forms from the FTB website, complete them, and mail them to the address provided.

- Online Filing: Use CalFile, the FTB’s online system.

- Mail: Download, complete, and mail the forms.

- Tax Professional: Get help from a qualified tax preparer.

10. What are the Penalties for Late Filing or Non-Payment of California Income Tax?

Do you understand the penalties for late filing or non-payment of California income tax? Penalties for late filing or non-payment of California income tax can be significant. The penalty for filing late is 5% of the unpaid tax for each month or part of a month that the return is late, up to a maximum of 25%. The penalty for non-payment is 0.5% of the unpaid tax for each month or part of a month that the tax remains unpaid, also up to a maximum of 25%. According to the FTB, it’s crucial to file on time and pay your taxes to avoid these penalties.

- Late Filing Penalty: 5% per month, up to 25%.

- Non-Payment Penalty: 0.5% per month, up to 25%.

- Avoid Penalties: File and pay on time.

11. What is California’s “Millionaire Tax” and How Does It Work?

Are you curious about California’s “Millionaire Tax” and how it affects high-income earners? California’s “Millionaire Tax” is an additional tax on high-income earners. Specifically, it refers to the additional 1% tax on taxable income over $1 million, which is earmarked for mental health services.

- Additional Tax: Extra 1% tax on high incomes.

- Income Threshold: Applied to taxable income over $1 million.

- Purpose: Funds mental health services.

12. How Does California’s Income Tax System Affect Small Businesses?

How does California’s income tax system affect small businesses? California’s income tax system significantly impacts small businesses. Owners of pass-through entities like S corporations, partnerships, and sole proprietorships pay individual income tax rates on their business profits. According to the California Small Business Association, high tax rates can reduce the capital available for reinvestment and growth, affecting business competitiveness.

- Pass-Through Entities: Business profits taxed at individual rates.

- Impact on Reinvestment: High taxes reduce available capital.

- Competitiveness: Affects the ability of small businesses to compete.

13. Are There Any Tax Credits Available for California Residents?

Do you know about the various tax credits available for California residents? California offers several tax credits for its residents, including the Earned Income Tax Credit (EITC), the Child and Dependent Care Credit, and credits for solar energy systems. These credits can significantly reduce your tax liability. The Franchise Tax Board website provides detailed information on eligibility requirements and how to claim these credits.

- Earned Income Tax Credit (EITC): For low- to moderate-income workers and families.

- Child and Dependent Care Credit: For expenses related to caring for children and dependents.

- Solar Energy Credit: Incentives for installing solar energy systems.

14. How Can I Optimize My Tax Strategy in California?

Are you looking for ways to optimize your tax strategy in California? Optimizing your tax strategy in California involves careful planning and taking advantage of available deductions and credits. Strategies include maximizing retirement contributions, utilizing tax-advantaged accounts like HSAs, and carefully tracking deductible expenses. Additionally, consulting with a tax professional can provide personalized advice tailored to your financial situation.

- Maximize Retirement Contributions: Reduce taxable income with retirement savings.

- Utilize Tax-Advantaged Accounts: Use HSAs and other accounts to lower taxes.

- Track Deductible Expenses: Keep records of eligible deductions.

15. What Resources Are Available to Help Me Understand California Income Tax?

Do you need more resources to better understand California income tax? Several resources are available to help you understand California income tax. The Franchise Tax Board (FTB) website offers detailed information, forms, and publications. Additionally, the IRS website provides federal tax information, and tax preparation software like TurboTax and H&R Block can assist with filing your return.

- Franchise Tax Board (FTB): Provides state tax information.

- IRS Website: Offers federal tax resources.

- Tax Preparation Software: TurboTax, H&R Block, etc.

16. How Do Non-Residents Pay California Income Tax?

Do you understand how non-residents pay California income tax? Non-residents pay California income tax on income sourced from California. This includes income from employment, business activities, or the sale of property within the state. According to the Franchise Tax Board, non-residents must file Form 540NR to report and pay tax on their California-source income.

- California-Source Income: Taxed for non-residents.

- Form 540NR: Used to report California income.

- Employment and Business: Income from these activities is taxable.

17. What Is the Difference Between Taxable Income and Adjusted Gross Income (AGI) in California?

Are you aware of the difference between taxable income and Adjusted Gross Income (AGI) in California? The difference between taxable income and Adjusted Gross Income (AGI) is crucial in understanding your tax liability. Adjusted Gross Income (AGI) is your gross income (total income) minus certain deductions like contributions to IRAs, student loan interest, and health savings account (HSA) deductions. Taxable income, on the other hand, is your AGI minus itemized or standard deductions and exemptions.

- Adjusted Gross Income (AGI): Gross income minus certain deductions.

- Taxable Income: AGI minus standard or itemized deductions and exemptions.

- Key Difference: Taxable income is the base for calculating tax liability.

18. How Do I Amend My California State Income Tax Return?

Do you need to amend your California state income tax return? If you need to correct errors on your previously filed California state income tax return, you must amend it. To do so, you need to file Form 540X, Amended Individual Income Tax Return. You can download this form from the Franchise Tax Board (FTB) website, complete it with the corrected information, and mail it to the address provided on the form.

- Form 540X: Required to amend a tax return.

- Corrected Information: Include all necessary corrections.

- Mail to FTB: Submit the amended return via mail.

19. What Tax Changes Should California Residents Anticipate in the Coming Years?

What tax changes should California residents anticipate in the coming years? California residents should anticipate potential tax changes due to ongoing legislative efforts and economic conditions. According to the California Budget & Policy Center, possible changes include adjustments to tax brackets, deductions, and credits, particularly in response to state budget needs and economic fluctuations.

- Legislative Changes: New laws can affect tax rates and rules.

- Economic Conditions: Economic changes can lead to tax adjustments.

- Budget Needs: State budget requirements can influence tax policies.

California Tax Form 540

20. How Can Income-Partners.Net Help Me Navigate California’s Income Tax Landscape?

How can income-partners.net assist you in navigating California’s complex income tax landscape? Income-partners.net offers resources and strategies to optimize your income through strategic partnerships. By forming business alliances, joint ventures, and revenue-sharing agreements, you can potentially mitigate your tax burden and increase your overall profitability. Visit income-partners.net to discover opportunities and connect with partners that align with your financial goals, and find collaborative strategies for maximizing your earnings while minimizing your tax liabilities.

- Strategic Partnerships: Create alliances to boost income.

- Tax Mitigation: Reduce tax burden through partnerships.

- Maximize Profitability: Increase overall financial gains.

Understanding California’s income tax rates and regulations is vital for effective financial planning. income-partners.net offers a range of resources and connections to help you navigate this landscape, maximize your income, and minimize your tax liabilities. By exploring strategic partnerships, you can open doors to greater financial success and stability. Consider visiting income-partners.net today to explore the opportunities available to you, and discover the power of collaboration in achieving your financial goals.

FAQ: California State Income Tax

1. What is the California state income tax rate for 2024?

California has a progressive income tax system with rates ranging from 1% to 12.3% in 2024, plus an additional 1% for incomes over $1 million.

2. How many income tax brackets does California have in 2024?

California has nine income tax brackets in 2024.

3. What is the standard deduction for single filers in California for 2024?

The standard deduction for single filers in California for 2024 is $5,363.

4. What is the standard deduction for married couples filing jointly in California for 2024?

The standard deduction for married couples filing jointly in California for 2024 is $10,726.

5. What is the additional tax on high-income earners in California, often called the “Millionaire Tax”?

The additional tax on high-income earners in California is 1% on taxable income over $1 million, earmarked for mental health services.

6. How do non-residents pay California income tax?

Non-residents pay California income tax on income sourced from California, such as income from employment or business activities within the state, and they must file Form 540NR.

7. What is the penalty for late filing of California income tax?

The penalty for late filing is 5% of the unpaid tax for each month or part of a month that the return is late, up to a maximum of 25%.

8. What is the penalty for non-payment of California income tax?

The penalty for non-payment is 0.5% of the unpaid tax for each month or part of a month that the tax remains unpaid, up to a maximum of 25%.

9. How can I amend my California state income tax return?

You can amend your California state income tax return by filing Form 540X, Amended Individual Income Tax Return, with the corrected information.

10. What resources are available to help me understand California income tax?

Resources include the Franchise Tax Board (FTB) website, the IRS website, and tax preparation software like TurboTax and H&R Block.